Download as pdf or txt

You might also like

- Duluth Public Schools' Preliminary 2023-2024 BudgetDocument39 pagesDuluth Public Schools' Preliminary 2023-2024 BudgetJoe BowenNo ratings yet

- Solution Manual International Accounting 4th Edition by Timothy Doupnik SLM1123Document10 pagesSolution Manual International Accounting 4th Edition by Timothy Doupnik SLM1123Thar AdeleiNo ratings yet

- Question and Answer - 14Document31 pagesQuestion and Answer - 14acc-expert0% (2)

- Role of Mncs in Tax Evasion and Tax Avoidance in An Underdeveloped Country: The Economy of Nigeria and An Overview of Its Tax SystemDocument11 pagesRole of Mncs in Tax Evasion and Tax Avoidance in An Underdeveloped Country: The Economy of Nigeria and An Overview of Its Tax SystemchitraNo ratings yet

- The Shirts Off Their Backs How Tax Policies Fleece The Poor: September 2005Document23 pagesThe Shirts Off Their Backs How Tax Policies Fleece The Poor: September 2005Alif NurjanahNo ratings yet

- Csae2015 1093 2Document19 pagesCsae2015 1093 2Ishmael OneyaNo ratings yet

- 2000 Oxfam Tax Havens Releasing Hidden Billions To Poverty EradicationDocument26 pages2000 Oxfam Tax Havens Releasing Hidden Billions To Poverty EradicationJuan Enrique ValerdiNo ratings yet

- Fiscal ParadiseDocument24 pagesFiscal ParadiseAndreea Telegdi MoodyNo ratings yet

- Tax 2222Document5 pagesTax 2222GeofreyNo ratings yet

- Tax Evasion and Tax AvoidanceDocument14 pagesTax Evasion and Tax AvoidanceGarySinyangweNo ratings yet

- MaltaDocument16 pagesMaltaMarceloNo ratings yet

- CTPD - Fools Paradise - Zambia Mining Tax Regime Briefing Paper FinalDocument20 pagesCTPD - Fools Paradise - Zambia Mining Tax Regime Briefing Paper FinalSavior MwambwaNo ratings yet

- Tax Haven BriefingDocument2 pagesTax Haven BriefingWilliam SmithNo ratings yet

- Escaping True Tax Liability of The Government Amidst PandemicsDocument7 pagesEscaping True Tax Liability of The Government Amidst PandemicsMaria Carla Roan AbelindeNo ratings yet

- MAKNET Policy Brief No 1Document6 pagesMAKNET Policy Brief No 1Martha KhungwaNo ratings yet

- Punishing Evaders 02-05Document1 pagePunishing Evaders 02-05Izhar MakhdoomNo ratings yet

- Fair Taxation For Poverty by Dr. IkramDocument8 pagesFair Taxation For Poverty by Dr. IkramHamid Saeed-KhanNo ratings yet

- Tax For Inclusive GrowthDocument19 pagesTax For Inclusive GrowthMercedes Baño HifóngNo ratings yet

- Challenges of Tax Administration in IndiaDocument6 pagesChallenges of Tax Administration in IndiaRishabh GuptaNo ratings yet

- Tax Effort Assignment-1Document7 pagesTax Effort Assignment-1Abigal MakwecheNo ratings yet

- Reviewer ContempDocument2 pagesReviewer ContempVanessa BaguiNo ratings yet

- Systems, Processes and Challenges of Public Revenue Collection in ZimbabweDocument12 pagesSystems, Processes and Challenges of Public Revenue Collection in ZimbabwePrince Wayne SibandaNo ratings yet

- Ethics of Tax AvoidanceDocument13 pagesEthics of Tax AvoidanceRashmi SharmaNo ratings yet

- Questions For Question & Answer SessionDocument12 pagesQuestions For Question & Answer Sessionapi-284426542No ratings yet

- CSO Submission On Tax & IFF Aspects To Africa Regional Consultations On FFD - March 24. 2015Document9 pagesCSO Submission On Tax & IFF Aspects To Africa Regional Consultations On FFD - March 24. 2015Kwesi_WNo ratings yet

- ICRICT - Dereje Alemayehu - Presentation - March 2015Document7 pagesICRICT - Dereje Alemayehu - Presentation - March 2015Kwesi_WNo ratings yet

- Ending The Era of Tax Havens: Why The UK Government Must Lead The WayDocument40 pagesEnding The Era of Tax Havens: Why The UK Government Must Lead The WayOxfamNo ratings yet

- Addressing Tax Evasion and AvoidanceDocument43 pagesAddressing Tax Evasion and Avoidancek2a2m2No ratings yet

- The Problem With Our Tax System and How It Affects UsDocument65 pagesThe Problem With Our Tax System and How It Affects Ussan pedro jailNo ratings yet

- Taxation Assignment BcaDocument12 pagesTaxation Assignment BcaJeniffer TracyNo ratings yet

- TP - Action Aid (2012) SABMILLARDocument40 pagesTP - Action Aid (2012) SABMILLARabel chalamilaNo ratings yet

- An Investigation of Factors Leading Low Tax Collection Among Informal Businesses in Dar Es Salaam City Council Fabian Respy (DR Pastory)Document19 pagesAn Investigation of Factors Leading Low Tax Collection Among Informal Businesses in Dar Es Salaam City Council Fabian Respy (DR Pastory)pastorysimioNo ratings yet

- Public Fiscal Report ScriptDocument8 pagesPublic Fiscal Report ScriptMIS Informal Settler FamiliesNo ratings yet

- Question 1-Answers. A)Document7 pagesQuestion 1-Answers. A)salongo geofNo ratings yet

- Tax Administration in Lagos StateDocument87 pagesTax Administration in Lagos Statealphatrade500No ratings yet

- Tax Haven BriefingDocument2 pagesTax Haven BriefingelcivilengNo ratings yet

- What Is Wrong With African Tax Administration?Document33 pagesWhat Is Wrong With African Tax Administration?mick mooreNo ratings yet

- Tax EvasionDocument1 pageTax EvasionAce D aceNo ratings yet

- Effectiveness of Tax Deduction at Source (TDS) in IndiaDocument4 pagesEffectiveness of Tax Deduction at Source (TDS) in IndiaIJEMR JournalNo ratings yet

- 'Ttax Haven'Document5 pages'Ttax Haven'JIYA DOSHINo ratings yet

- AIDC Submission To The Zondo Commission of InquiryDocument20 pagesAIDC Submission To The Zondo Commission of InquirySizweNo ratings yet

- The Polytechnic, Ibadan: Kayode Oladipupo OlayemiDocument38 pagesThe Polytechnic, Ibadan: Kayode Oladipupo OlayemiSuleiman Abubakar AuduNo ratings yet

- Tax Evasion CHPT 1-5Document38 pagesTax Evasion CHPT 1-5KAYODE OLADIPUPO100% (5)

- Ghana Tax Exemption Regime and Impplication On The Economy (A Case Study at Gra and Ghana Nut Company Limited - Bono East Techiman)Document33 pagesGhana Tax Exemption Regime and Impplication On The Economy (A Case Study at Gra and Ghana Nut Company Limited - Bono East Techiman)Dangyi GodSeesNo ratings yet

- PW Tax EvasionDocument16 pagesPW Tax EvasionGAURAV KUMARNo ratings yet

- Policy Recommendation To Promote Growth and Development, Given The Current Global Financial CrisisDocument22 pagesPolicy Recommendation To Promote Growth and Development, Given The Current Global Financial CrisisBablu ShawNo ratings yet

- Speech - FDG - 20120905 PDFDocument4 pagesSpeech - FDG - 20120905 PDFPrateek HerpersadNo ratings yet

- Tax Havens and Money Laundering in IndiaDocument12 pagesTax Havens and Money Laundering in IndiaVaishali RathiNo ratings yet

- The Reforms To Enhance Tax Culture in PakistanDocument2 pagesThe Reforms To Enhance Tax Culture in PakistanAamir AliNo ratings yet

- Emerging International Taxation IssuesDocument8 pagesEmerging International Taxation IssuesSaksham AroraNo ratings yet

- Factiva 20191022 1026 PDFDocument2 pagesFactiva 20191022 1026 PDFAnonymous tTk3g8No ratings yet

- Why Is Tax Important For The Company of A Country?: T + S + M I + X + GDocument2 pagesWhy Is Tax Important For The Company of A Country?: T + S + M I + X + GAnonymous rcCVWoM8bNo ratings yet

- Moses Kulaba - How To Curb Transfer Mispricing and Illicit Tax Evasion in The Extractive Sector 2020Document7 pagesMoses Kulaba - How To Curb Transfer Mispricing and Illicit Tax Evasion in The Extractive Sector 2020Moses KulabaNo ratings yet

- Hon. Irene Ovonji-Odida, Member Au/ Uneca High Level Panel On Iffs From Africa, Outgoing Chair Actionaid Int., Ceo Fida-UgandaDocument14 pagesHon. Irene Ovonji-Odida, Member Au/ Uneca High Level Panel On Iffs From Africa, Outgoing Chair Actionaid Int., Ceo Fida-Ugandaapi-272780637No ratings yet

- Ưu Như C C A ETDocument21 pagesƯu Như C C A ETLam HảiNo ratings yet

- Capital Gains Taxes and Offshore Indirect TransfersDocument30 pagesCapital Gains Taxes and Offshore Indirect TransfersReagan SsebbaaleNo ratings yet

- Research Final Draft 010516Document68 pagesResearch Final Draft 010516Norman MberiNo ratings yet

- Why Is Country-by-Country Financial Reporting by Multinational Companies So Important?Document2 pagesWhy Is Country-by-Country Financial Reporting by Multinational Companies So Important?gigi_17No ratings yet

- MunDocument3 pagesMunGirish SreeneebusNo ratings yet

- URA FY 201516 - 27th July 2016Document15 pagesURA FY 201516 - 27th July 2016The Independent MagazineNo ratings yet

- Tax EvasionDocument1 pageTax EvasionMhaiel EscalNo ratings yet

- Learning to Love Form 1040: Two Cheers for the Return-Based Mass Income TaxFrom EverandLearning to Love Form 1040: Two Cheers for the Return-Based Mass Income TaxNo ratings yet

- Automate Bank Reconciliations With Excel Power Quer1Document5 pagesAutomate Bank Reconciliations With Excel Power Quer1johnkwashanaiNo ratings yet

- Succeeding As A New Cfo Keys To The First 100 DaysDocument30 pagesSucceeding As A New Cfo Keys To The First 100 DaysjohnkwashanaiNo ratings yet

- Setting The Right Stretch TargetsDocument12 pagesSetting The Right Stretch TargetsjohnkwashanaiNo ratings yet

- Business Partnering e BookDocument20 pagesBusiness Partnering e BookjohnkwashanaiNo ratings yet

- Stock ControlDocument28 pagesStock ControljohnkwashanaiNo ratings yet

- 2014 Refresher Best Practices in Inventory ManagementDocument12 pages2014 Refresher Best Practices in Inventory ManagementjohnkwashanaiNo ratings yet

- Citrus Budget Handbook 2018 7 3Document130 pagesCitrus Budget Handbook 2018 7 3johnkwashanaiNo ratings yet

- Bata Shoes BrochureDocument14 pagesBata Shoes BrochurejohnkwashanaiNo ratings yet

- Open Letter To His Excellency DR Lazurus M. Chakwera 13th September 2022Document5 pagesOpen Letter To His Excellency DR Lazurus M. Chakwera 13th September 2022johnkwashanaiNo ratings yet

- REM1 Hand OutDocument42 pagesREM1 Hand OutFrancis LNo ratings yet

- Bank MCQ & Written MATH ReviewDocument5 pagesBank MCQ & Written MATH ReviewNahidNo ratings yet

- Labour Law Makumira NotesDocument256 pagesLabour Law Makumira NotesSteven MapimaNo ratings yet

- December 23, 2015 Tribune-PhonographDocument16 pagesDecember 23, 2015 Tribune-PhonographcwmediaNo ratings yet

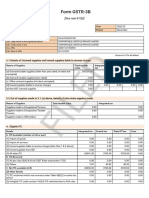

- Filed: Form GSTR-3BDocument2 pagesFiled: Form GSTR-3Bkrishswat7912No ratings yet

- EC Geography Grade 12 September 2023 P2 and MemoDocument41 pagesEC Geography Grade 12 September 2023 P2 and Memomabelenglehlohonolo3No ratings yet

- Cotxa2 B11 AssignmentDocument10 pagesCotxa2 B11 Assignmentfs5kxrcn2gNo ratings yet

- 30 - CIR V Botelho Shipping CorpDocument2 pages30 - CIR V Botelho Shipping CorpDoel LozanoNo ratings yet

- Soumya Agrawal BVDocument18 pagesSoumya Agrawal BVSoumya AgrawalNo ratings yet

- The Coca Cola Exports v. CIR, CTA Case No. 5238, Dec. 19, 1997Document6 pagesThe Coca Cola Exports v. CIR, CTA Case No. 5238, Dec. 19, 1997SGNo ratings yet

- International Financial Management Notes Unit-1Document15 pagesInternational Financial Management Notes Unit-1Geetha aptdcNo ratings yet

- Office of The CGDA, West Block-V, R.K.Puram, New Delhi-60S Pro IFA WingDocument11 pagesOffice of The CGDA, West Block-V, R.K.Puram, New Delhi-60S Pro IFA WingsmNo ratings yet

- Module 01 Fundamrental Principles of TaxationDocument21 pagesModule 01 Fundamrental Principles of TaxationDonna Mae FernandezNo ratings yet

- TOA AnswerKey PDFDocument12 pagesTOA AnswerKey PDFJc QuismundoNo ratings yet

- Tax 1 Cases On Allowable DeductionsDocument45 pagesTax 1 Cases On Allowable DeductionsREJFREEFALLNo ratings yet

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Sumit Kumar KarmakarNo ratings yet

- Net Pay: Earnings Amount Deductions AmountDocument1 pageNet Pay: Earnings Amount Deductions AmountkartamaNo ratings yet

- JK01P1207Document1 pageJK01P1207Bhat EnterprisesNo ratings yet

- Gender Budgeting PDFDocument20 pagesGender Budgeting PDFHIMANSHI HIMANSHINo ratings yet

- Questions On Pricing Procedure in SAP SDDocument5 pagesQuestions On Pricing Procedure in SAP SDAnand PattedNo ratings yet

- City of Iloilo v. PPADocument15 pagesCity of Iloilo v. PPAarlene punioNo ratings yet

- Punong Bayan and Araullo Firm PresentationDocument12 pagesPunong Bayan and Araullo Firm PresentationBianca Jane MaaliwNo ratings yet

- Construction: MR Prabhu Lal JatDocument3 pagesConstruction: MR Prabhu Lal JatRahulNo ratings yet

- CVP ExercisesDocument3 pagesCVP ExercisesObamamanam100% (1)

- RMC No 63-2012Document4 pagesRMC No 63-2012veraNo ratings yet

- ANALYSIS of FINANCIAL STATEMENT Using Technique of Ratio Analysis by Furkan KamdarDocument72 pagesANALYSIS of FINANCIAL STATEMENT Using Technique of Ratio Analysis by Furkan Kamdarhumayunrashid84No ratings yet

- Commissioner of Internal Revenue Vs The Court of Appeals, The Court of Tax Appeals and Ateneo de Manila UniversityDocument2 pagesCommissioner of Internal Revenue Vs The Court of Appeals, The Court of Tax Appeals and Ateneo de Manila UniversityRae Angela GarciaNo ratings yet