Download as pdf or txt

You might also like

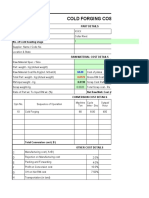

- 94.cold Forging Cost Estimation SheetDocument5 pages94.cold Forging Cost Estimation SheetVenkateswaran venkateswaranNo ratings yet

- 2020 Proteus Offshore, LLC Form 1065 Partnerships Tax Return - FilingDocument17 pages2020 Proteus Offshore, LLC Form 1065 Partnerships Tax Return - FilingPeter Kitchen100% (2)

- Biryani Research PaperDocument11 pagesBiryani Research PaperRaamji Mp100% (1)

- JCB Case StudyDocument9 pagesJCB Case StudyPanma PatelNo ratings yet

- Unit-3 Human Resource Planning ProcessDocument5 pagesUnit-3 Human Resource Planning ProcessSujan Chaudhary100% (1)

- Word FilesDocument5 pagesWord Filesrabia khanNo ratings yet

- Topic 4Document37 pagesTopic 4glenettearizala18No ratings yet

- A Study On Whistle Blowing - InfosysDocument61 pagesA Study On Whistle Blowing - InfosysRajesh BathulaNo ratings yet

- EthicsDocument18 pagesEthicsPrahlad RaiNo ratings yet

- Andika Daffa Elianto - 12010119190124 - UAS Business Ethics - IUPDocument5 pagesAndika Daffa Elianto - 12010119190124 - UAS Business Ethics - IUPAndika Daffa EliantoNo ratings yet

- Whistleblower PolicyDocument7 pagesWhistleblower PolicyAbhijeetNo ratings yet

- Meeting 6Document6 pagesMeeting 6p aloaNo ratings yet

- Professional Ethics: Elaine Capili Christine TeodoroDocument65 pagesProfessional Ethics: Elaine Capili Christine TeodoroJoyce Anne GarduqueNo ratings yet

- Q.3 Ethics AssignmentDocument3 pagesQ.3 Ethics AssignmentShashank VarmaNo ratings yet

- Whisle Blowing 1Document10 pagesWhisle Blowing 1Arun Gireesh100% (1)

- BA4 Notes CimaDocument25 pagesBA4 Notes CimakateNo ratings yet

- Business Ethics (Unit 4)Document8 pagesBusiness Ethics (Unit 4)prabhav1822001No ratings yet

- The Ethico-Legal Framework - CullingsDocument19 pagesThe Ethico-Legal Framework - CullingsAkash PanigrahiNo ratings yet

- SSRN Id2258296 PDFDocument10 pagesSSRN Id2258296 PDFVed VyasNo ratings yet

- SSRN Id2258296 PDFDocument10 pagesSSRN Id2258296 PDFVed VyasNo ratings yet

- A Project On Whistle Blowing (Business Ethics)Document14 pagesA Project On Whistle Blowing (Business Ethics)Kiran moreNo ratings yet

- OHS135 - Module 3 - Ethics For OHS ProfessionalsDocument16 pagesOHS135 - Module 3 - Ethics For OHS ProfessionalsdknausNo ratings yet

- Part 6-1 PDFDocument22 pagesPart 6-1 PDFanvesh MININGNo ratings yet

- Chapter 4 Professional EthicsDocument45 pagesChapter 4 Professional EthicsitsmefxezNo ratings yet

- Toshiba SaudDocument3 pagesToshiba SaudFaiq HashmiNo ratings yet

- Unit 123Document22 pagesUnit 123Khushal GargNo ratings yet

- C10 GovernanceDocument7 pagesC10 GovernanceBernice CheongNo ratings yet

- Group#5 Corruption and Ethics in Global BusinessDocument37 pagesGroup#5 Corruption and Ethics in Global BusinessTricia Angel P. BantigueNo ratings yet

- Whistel Blower PolicyDocument16 pagesWhistel Blower PolicyPoonam SonvaniNo ratings yet

- Assessing and Managing The Risk of ReprisalDocument9 pagesAssessing and Managing The Risk of ReprisalDavid Paul HensonNo ratings yet

- Whistle-Blowing Booklet 2023 IndoDocument32 pagesWhistle-Blowing Booklet 2023 IndoBetta LoverNo ratings yet

- Acc 2214 - Whistle BlowingDocument5 pagesAcc 2214 - Whistle BlowingSunday OcheNo ratings yet

- Ethics Exam SuggasationDocument10 pagesEthics Exam SuggasationFuck YouNo ratings yet

- White Collar SessionalDocument20 pagesWhite Collar SessionalBinit PandeyNo ratings yet

- Wenjun Herminado QuizzzzzDocument3 pagesWenjun Herminado QuizzzzzWenjunNo ratings yet

- Auditing I CH 2Document36 pagesAuditing I CH 2Hussien AdemNo ratings yet

- Building A Culture of CandourDocument44 pagesBuilding A Culture of CandourharliestudieNo ratings yet

- Why Should A Business Be Ethically Sensitive?: The Social Function of BusinessDocument3 pagesWhy Should A Business Be Ethically Sensitive?: The Social Function of BusinessKassandra VenzueloNo ratings yet

- Key Concepts in AccountingDocument9 pagesKey Concepts in AccountingSunday OcheNo ratings yet

- Business Ethics ModuleDocument7 pagesBusiness Ethics ModuleRica Canaba100% (2)

- ترجمة قانونيةDocument40 pagesترجمة قانونيةAhmedNo ratings yet

- Final-Notes BEDocument9 pagesFinal-Notes BEBùi Diễm QuỳnhNo ratings yet

- BE Module 5Document5 pagesBE Module 5Thanmayi VanteruNo ratings yet

- Ethics Chapter 1: The Responsibility of EngineersDocument24 pagesEthics Chapter 1: The Responsibility of EngineersNguyễn QuỳnhNo ratings yet

- Whistle BlowingDocument7 pagesWhistle Blowingsruthi karthiNo ratings yet

- Whistleblowing Policy - V1.4Document5 pagesWhistleblowing Policy - V1.4Zinko ThuNo ratings yet

- Chap 4 Whistle BlowingDocument7 pagesChap 4 Whistle BlowingMyaNo ratings yet

- Topic 2Document7 pagesTopic 2Casio ManikNo ratings yet

- Sample in House Whistle Blowing Training Programme For Cipd Members 2014Document2 pagesSample in House Whistle Blowing Training Programme For Cipd Members 2014Monkey D. LuffyNo ratings yet

- Audit-Professional EthicsDocument5 pagesAudit-Professional EthicsRhn Habib RehmanNo ratings yet

- Whistle BlowingDocument6 pagesWhistle BlowingVinay Ramane50% (4)

- Whistle BlowingDocument24 pagesWhistle BlowingTati Mansur100% (4)

- Whistle Blowing NotesDocument6 pagesWhistle Blowing NotesRathin BanerjeeNo ratings yet

- BMU 08104: Business Ethics: For BMU 08104-III Semester IDocument169 pagesBMU 08104: Business Ethics: For BMU 08104-III Semester Ially jumanneNo ratings yet

- Ethics Unit 3Document14 pagesEthics Unit 3Tarun KumarNo ratings yet

- Policy On Preventing and Addressing RetaliationDocument13 pagesPolicy On Preventing and Addressing RetaliationOmar FilaliNo ratings yet

- Practice Advisory 1210 (1) .A2-2 Rev 4 27 2006Document5 pagesPractice Advisory 1210 (1) .A2-2 Rev 4 27 2006linghongcNo ratings yet

- Chapter 2 NotesDocument7 pagesChapter 2 NotesKrisha Therese PajarilloNo ratings yet

- Code of Conduct and Whistle BlowerDocument17 pagesCode of Conduct and Whistle BlowerSandeep KaurNo ratings yet

- Sartorius Anti-Corruption CodeDocument12 pagesSartorius Anti-Corruption CodeRanjith LMNo ratings yet

- Corporate Law CIA-3Document2 pagesCorporate Law CIA-3Dhruvraj SolankiNo ratings yet

- Les Chapter 03 Part 4 Session 2Document26 pagesLes Chapter 03 Part 4 Session 2Henok AsemahugnNo ratings yet

- Exam 3 NotesDocument20 pagesExam 3 NotesVince Cinco ParconNo ratings yet

- Whistle Blowing Part of CH 13Document9 pagesWhistle Blowing Part of CH 1342MD ASIFUR RAHMAN ASIFNo ratings yet

- The Whistleblowing Program Handbook: A practical guide to running a whistleblowing program in AustraliaFrom EverandThe Whistleblowing Program Handbook: A practical guide to running a whistleblowing program in AustraliaNo ratings yet

- ACC 182 Accounting For Government ExpenditureDocument40 pagesACC 182 Accounting For Government ExpenditureniggerNo ratings yet

- Purdue University Contract With Ibram KendiDocument8 pagesPurdue University Contract With Ibram KendiThe College FixNo ratings yet

- Balance ConfirmationDocument11 pagesBalance Confirmationeastern arteqaNo ratings yet

- Course: Marketing Research: Faculty of International Economic Relations Semester 1, 2021 - 2022Document2 pagesCourse: Marketing Research: Faculty of International Economic Relations Semester 1, 2021 - 2022Thảo NguyễnNo ratings yet

- Masterglenium Ace: Solutions For The Pre-Cast IndustryDocument7 pagesMasterglenium Ace: Solutions For The Pre-Cast IndustryAlanNo ratings yet

- Golden Star Resources Reports ResultsDocument20 pagesGolden Star Resources Reports ResultsFuaad DodooNo ratings yet

- Test Bank For Intermediate Accounting 17th Edition Donald e Kieso DownloadDocument56 pagesTest Bank For Intermediate Accounting 17th Edition Donald e Kieso DownloadTeresaMoorecsrby100% (45)

- 11 QueuingDocument39 pages11 QueuingArihant patilNo ratings yet

- Group-4 STM28 Scientific-PosterDocument1 pageGroup-4 STM28 Scientific-Postercesxzhoran hahaNo ratings yet

- HO-Venn Diagram: Directions For Questions 1 and 5: Answer The Questions On The Basis of The Following DataDocument4 pagesHO-Venn Diagram: Directions For Questions 1 and 5: Answer The Questions On The Basis of The Following Dataankit singhNo ratings yet

- Project CharterDocument9 pagesProject CharterKomal SoomroNo ratings yet

- KEPCO - Consolidated - FY 2018 - FinalDocument175 pagesKEPCO - Consolidated - FY 2018 - FinalJenna GanNo ratings yet

- MGT 162 Group Assignments 25Document20 pagesMGT 162 Group Assignments 25MUHAMMAD FAUZAN ABU BAKARNo ratings yet

- Posco Inv.Document6 pagesPosco Inv.dhawalhemantNo ratings yet

- Odoo v15Document5 pagesOdoo v15t.nominerdene99No ratings yet

- When in Doubt Blame The Accountants Said Mathew Ingram inDocument2 pagesWhen in Doubt Blame The Accountants Said Mathew Ingram inLet's Talk With HassanNo ratings yet

- My IdolDocument1 pageMy IdolSyed FarisNo ratings yet

- Coa M2020-026Document18 pagesCoa M2020-026Justine CastilloNo ratings yet

- MayaSavings SoA 2023OCTDocument17 pagesMayaSavings SoA 2023OCTfitdaddyphNo ratings yet

- Dragoneante of The Inpec: Jhon Jairo Ortiz RodrguezDocument3 pagesDragoneante of The Inpec: Jhon Jairo Ortiz RodrguezJOHN JAIRO ORTIZ RODRIGUEZNo ratings yet

- Project Report FormatDocument8 pagesProject Report FormatBhartiNo ratings yet

- Group B Code of Ethics Caselet 245Document2 pagesGroup B Code of Ethics Caselet 245BSA3Tagum MariletNo ratings yet

- Module 3 Exam - Attempt Review Netacad ITE 6301Document6 pagesModule 3 Exam - Attempt Review Netacad ITE 6301Allen JoshuaNo ratings yet

- Fmda GST RCDocument3 pagesFmda GST RCDipankar BarmanNo ratings yet

- Younity's 3 Year Young Anniv Flash Sale PDFDocument1 pageYounity's 3 Year Young Anniv Flash Sale PDFIvy NinjaNo ratings yet