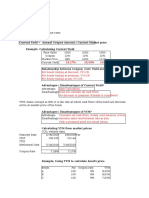

Compute Clean Price, Total Price and Modified Duration

Compute Clean Price, Total Price and Modified Duration

You might also like

- FA DCF Modelling Test 1Document17 pagesFA DCF Modelling Test 1honeymakrani220% (1)

- CFA Level 1 Calculation Workbook: 300 Calculations to Prepare for the CFA Level 1 Exam (2023 Edition)From EverandCFA Level 1 Calculation Workbook: 300 Calculations to Prepare for the CFA Level 1 Exam (2023 Edition)Rating: 4.5 out of 5 stars4.5/5 (5)

- Day 1Document11 pagesDay 1Abdullah EjazNo ratings yet

- Your Business Advantage Relationship Banking Preferred Rewards For Bus PlatinumDocument12 pagesYour Business Advantage Relationship Banking Preferred Rewards For Bus PlatinumUsm am50% (2)

- Sip ReportDocument40 pagesSip ReportShefali ShrivastavaNo ratings yet

- Tugas ObligasiDocument15 pagesTugas Obligasiwahdah ulin nafisahNo ratings yet

- Aaaaa 1Document52 pagesAaaaa 1Kath LeynesNo ratings yet

- Tut Lec 5 - Chap 80Document6 pagesTut Lec 5 - Chap 80Bella SeahNo ratings yet

- Financial Risk Management: A Simple IntroductionFrom EverandFinancial Risk Management: A Simple IntroductionRating: 4.5 out of 5 stars4.5/5 (7)

- Introduction To Business Government and SocietyDocument4 pagesIntroduction To Business Government and SocietyMd Imran HossainNo ratings yet

- Sample RESULTS AND DISCUSSIONDocument5 pagesSample RESULTS AND DISCUSSIONexquisiteNo ratings yet

- Fixed Income Class Examples ADocument9 pagesFixed Income Class Examples ADebashis MallickNo ratings yet

- Valuation of Bonds NumericalsDocument30 pagesValuation of Bonds NumericalsankitNo ratings yet

- (A.2) Liabilities - Practice ExercisesDocument8 pages(A.2) Liabilities - Practice ExercisesFrances Nicole Doria MoralesNo ratings yet

- Assignment No 6 - FM Actual Summer 2020 Furqan Farooq-18292Document37 pagesAssignment No 6 - FM Actual Summer 2020 Furqan Farooq-18292Furqan Farooq Vadharia100% (1)

- IAS 32, IFRS7,9 Financial InstrumentsDocument6 pagesIAS 32, IFRS7,9 Financial InstrumentsMazni Hanisah100% (2)

- FM12 CH 05 Tool KitDocument31 pagesFM12 CH 05 Tool KitJamie RossNo ratings yet

- Fedillaga Case13Document19 pagesFedillaga Case13Luke Ysmael FedillagaNo ratings yet

- Module 8 - ReviewerDocument8 pagesModule 8 - ReviewerFiona MiralpesNo ratings yet

- Bond StrategiesDocument6 pagesBond Strategiesamitva2007No ratings yet

- Interest Rates and Bond Valuation: BloombergDocument12 pagesInterest Rates and Bond Valuation: BloombergSatyajit RoyNo ratings yet

- Lã Minh Ngọc - 18071385 - INS3007Document15 pagesLã Minh Ngọc - 18071385 - INS3007Ming NgọhNo ratings yet

- Debt MarketDocument25 pagesDebt MarketSuraj DasNo ratings yet

- Long-Term Debt FinancingDocument53 pagesLong-Term Debt FinancingGaluh Boga KuswaraNo ratings yet

- Chapter 9Document58 pagesChapter 9sasaNo ratings yet

- Chapter 2 TB - Long Term Liabilities StudentsDocument7 pagesChapter 2 TB - Long Term Liabilities StudentsMohammed Al-ghamdiNo ratings yet

- CA Final SFM RTP For May 2023Document18 pagesCA Final SFM RTP For May 2023remoratilemothekheNo ratings yet

- Financial Analyst G&M - Real Estate Test & Case Study (SUMAN SAURABH)Document24 pagesFinancial Analyst G&M - Real Estate Test & Case Study (SUMAN SAURABH)sourabh sinhaNo ratings yet

- Final Practice Questions and SolutionsDocument12 pagesFinal Practice Questions and Solutionsshaikhnazneen100No ratings yet

- Financial Analyst G&M - Real Estate Test & Case StudyDocument19 pagesFinancial Analyst G&M - Real Estate Test & Case StudyDhruv ShahNo ratings yet

- Corp Fin Session 9-10 Bond ValuationDocument20 pagesCorp Fin Session 9-10 Bond Valuationmansi agrawalNo ratings yet

- Final Exam IntermediateDocument24 pagesFinal Exam IntermediateIrene Grace Edralin AdenaNo ratings yet

- Chapters 12B and 12CDocument42 pagesChapters 12B and 12CCarlos VillanuevaNo ratings yet

- Commercial Real Estate Valuation ModelDocument6 pagesCommercial Real Estate Valuation Modelkaran yadavNo ratings yet

- Financial Management Assignment 6 Fixed Investment Management Submitted By-Faisal Ishaq B17079 Case BackgroundDocument6 pagesFinancial Management Assignment 6 Fixed Investment Management Submitted By-Faisal Ishaq B17079 Case BackgroundfaisalNo ratings yet

- Ebersoll Manufacturing CoDocument5 pagesEbersoll Manufacturing CoShemu PlcNo ratings yet

- Quiz - Chapter 3 - Bonds Payable Other ConceptsDocument7 pagesQuiz - Chapter 3 - Bonds Payable Other ConceptsRica Jane Oraiz Lloren89% (9)

- Assessment Task 3Document5 pagesAssessment Task 3Christian N MagsinoNo ratings yet

- Fixed Investment ManagementDocument7 pagesFixed Investment ManagementAmanNo ratings yet

- FE (201312) Paper II - Answer PDFDocument12 pagesFE (201312) Paper II - Answer PDFgaryNo ratings yet

- Strategic Financial Management PDFDocument18 pagesStrategic Financial Management PDFUpkar SinghNo ratings yet

- Ch05 Mini CaseDocument8 pagesCh05 Mini CaseTia1977No ratings yet

- Excel FinanceDocument28 pagesExcel FinanceabdullahNo ratings yet

- Bond Portfolio MGTDocument22 pagesBond Portfolio MGTChandrabhan NathawatNo ratings yet

- 67488bos54240 Cp12ciDocument30 pages67488bos54240 Cp12ciKhawaish MittalNo ratings yet

- 08 Bond InvestmentDocument3 pages08 Bond InvestmentAllegria Alamo100% (1)

- Financial Instrument CIMADocument5 pagesFinancial Instrument CIMAwaqas ahmadNo ratings yet

- Solution Manual For Financial Institutions Markets and Money Kidwell Blackwell Whidbee Sias 11th EditionDocument8 pagesSolution Manual For Financial Institutions Markets and Money Kidwell Blackwell Whidbee Sias 11th EditionAmandaMartinxdwj100% (40)

- BFC5935 - Tutorial 7 SolutionsDocument4 pagesBFC5935 - Tutorial 7 SolutionsXue XuNo ratings yet

- Combinepdf 1 PDFDocument16 pagesCombinepdf 1 PDFandrea arapocNo ratings yet

- Valuation of Financial AssetsDocument47 pagesValuation of Financial AssetsprashantkumbhaniNo ratings yet

- Famba6e Quiz Mod07 032014Document4 pagesFamba6e Quiz Mod07 032014aparna jethaniNo ratings yet

- Chapter 1 - CompleteDocument27 pagesChapter 1 - Completemohsin razaNo ratings yet

- MVJUSTINIANI - BAFACR16 - INTERIM ASSESSMENT 1 - 3T - AY2022 23 With Answer KeysDocument4 pagesMVJUSTINIANI - BAFACR16 - INTERIM ASSESSMENT 1 - 3T - AY2022 23 With Answer KeysDe Gala ShailynNo ratings yet

- MNGT 604 Day2 Problem Set Solutions-2Document7 pagesMNGT 604 Day2 Problem Set Solutions-2harini muthuNo ratings yet

- Question No. 1 Is Compulsory. Attempt Any Four Questions From The Remaining Five Questions. Working Notes Should Form Part of The AnswerDocument5 pagesQuestion No. 1 Is Compulsory. Attempt Any Four Questions From The Remaining Five Questions. Working Notes Should Form Part of The Answeradarsh agrawalNo ratings yet

- Quiz Chapter+3 Bonds+PayableDocument3 pagesQuiz Chapter+3 Bonds+PayableRena Jocelle NalzaroNo ratings yet

- Answer To Q On IFRS 9Document4 pagesAnswer To Q On IFRS 9johny SahaNo ratings yet

- Auditing Problem Final Exam With Answer Only, No SolutionDocument23 pagesAuditing Problem Final Exam With Answer Only, No SolutionRheu Reyes100% (1)

- SFM Q MTP 1 Final May22Document5 pagesSFM Q MTP 1 Final May22Divya AggarwalNo ratings yet

- Accounting 1Document10 pagesAccounting 1Jay EbuenNo ratings yet

- CPK Case AnalysisDocument11 pagesCPK Case AnalysisVikas MotwaniNo ratings yet

- Personal Money Management Made Simple with MS Excel: How to save, invest and borrow wiselyFrom EverandPersonal Money Management Made Simple with MS Excel: How to save, invest and borrow wiselyNo ratings yet

- Cairns Merger With VedantaDocument34 pagesCairns Merger With Vedantaparv salechaNo ratings yet

- Debt Markets - N - 2Document34 pagesDebt Markets - N - 2parv salechaNo ratings yet

- The Boeing Company: FORM 10-QDocument105 pagesThe Boeing Company: FORM 10-Qparv salechaNo ratings yet

- Eco Proj 2Document12 pagesEco Proj 2parv salechaNo ratings yet

- Reading 37 Measuring and Managing Market Risk - AnswersDocument11 pagesReading 37 Measuring and Managing Market Risk - Answerstristan.riolsNo ratings yet

- Answer Key of Ppe Recognition ProblemDocument19 pagesAnswer Key of Ppe Recognition ProblemJaneNo ratings yet

- Report On General Banking Activity of Jamuna BankDocument41 pagesReport On General Banking Activity of Jamuna BankHarunur RashidNo ratings yet

- Are Loyalty Program Members Really EngagedDocument15 pagesAre Loyalty Program Members Really Engagedzoe_zoeNo ratings yet

- BSC (Hons) Business Management (: BMP6003 International HRMDocument25 pagesBSC (Hons) Business Management (: BMP6003 International HRMNazmus Sakib RahatNo ratings yet

- Continuous Improvement Task1Document2 pagesContinuous Improvement Task1pravesh bhattaraiNo ratings yet

- Soal Uts Dak Fo TeoryDocument5 pagesSoal Uts Dak Fo Teorykomang olinNo ratings yet

- Case Study Unit 2Document2 pagesCase Study Unit 2Nga LêNo ratings yet

- LSS ScoDocument3 pagesLSS ScoerwinantokaNo ratings yet

- Inventory KPI - SAP TransactionsDocument3 pagesInventory KPI - SAP TransactionsGabrielNo ratings yet

- Articles of Incorporation-Stock Corp - CNL Management CorpDocument7 pagesArticles of Incorporation-Stock Corp - CNL Management CorpKevin CastrojasNo ratings yet

- Afar1 Grp4 Acctng4materials Jit BackflushDocument39 pagesAfar1 Grp4 Acctng4materials Jit BackflushAngela Miles DizonNo ratings yet

- Discover The Finest Indian Flavors at The Indian Bazaar New Jersey's Premier Indian Grocery StoreDocument2 pagesDiscover The Finest Indian Flavors at The Indian Bazaar New Jersey's Premier Indian Grocery StoreIsabella DillonNo ratings yet

- Pengajuan Soal Uts Dari Kelas EDocument1 pagePengajuan Soal Uts Dari Kelas EHikmatullahNo ratings yet

- A Project Lifecycle Perspective On Stakeholder Influence Strategies in Global ProjectsDocument17 pagesA Project Lifecycle Perspective On Stakeholder Influence Strategies in Global Projectsnromy2006No ratings yet

- Mubarok Hossain CVDocument3 pagesMubarok Hossain CVsharif261No ratings yet

- Chaitanya Investors Presentation Dec 2014Document33 pagesChaitanya Investors Presentation Dec 2014CA Pavan KumarNo ratings yet

- Damodaram Sanjivayya National Law University Visakhapatnam, A.P., IndiaDocument19 pagesDamodaram Sanjivayya National Law University Visakhapatnam, A.P., IndiaAbhijit Singh ChaturvediNo ratings yet

- Symbiosis Institute of Management Studies: Assignment OnDocument10 pagesSymbiosis Institute of Management Studies: Assignment OnamitcmsNo ratings yet

- Department of Education: Region Iv-A Calabarzon Schools Division of BatangasDocument6 pagesDepartment of Education: Region Iv-A Calabarzon Schools Division of BatangasRoylendel HernandezNo ratings yet

- Academy: Soil Stabilised Brick (SSB) Production Training Course For Contractors & Construction EntrepreneursDocument4 pagesAcademy: Soil Stabilised Brick (SSB) Production Training Course For Contractors & Construction Entrepreneurspquiroga2No ratings yet

- Zinka Logistics Solutions - R-25092020Document8 pagesZinka Logistics Solutions - R-25092020Atiqur Rahman BarbhuiyaNo ratings yet

- Varun Manian, MD Radiance Realty, Ranks Among The Top Entrepreneurs in The CountryDocument8 pagesVarun Manian, MD Radiance Realty, Ranks Among The Top Entrepreneurs in The CountryAkansha SinghNo ratings yet

- Ford MotorDocument27 pagesFord MotorBahar Uddin100% (8)

- DWS LIST - Ao 11 2Document66 pagesDWS LIST - Ao 11 2sei gosaNo ratings yet

- Key Unit 1 - 1Document24 pagesKey Unit 1 - 1Ezequiel VerbauwedeNo ratings yet

Download as xlsx, pdf, or txt

You might also like

- FA DCF Modelling Test 1Document17 pagesFA DCF Modelling Test 1honeymakrani220% (1)

- CFA Level 1 Calculation Workbook: 300 Calculations to Prepare for the CFA Level 1 Exam (2023 Edition)From EverandCFA Level 1 Calculation Workbook: 300 Calculations to Prepare for the CFA Level 1 Exam (2023 Edition)Rating: 4.5 out of 5 stars4.5/5 (5)

- Day 1Document11 pagesDay 1Abdullah EjazNo ratings yet

- Your Business Advantage Relationship Banking Preferred Rewards For Bus PlatinumDocument12 pagesYour Business Advantage Relationship Banking Preferred Rewards For Bus PlatinumUsm am50% (2)

- Sip ReportDocument40 pagesSip ReportShefali ShrivastavaNo ratings yet

- Tugas ObligasiDocument15 pagesTugas Obligasiwahdah ulin nafisahNo ratings yet

- Aaaaa 1Document52 pagesAaaaa 1Kath LeynesNo ratings yet

- Tut Lec 5 - Chap 80Document6 pagesTut Lec 5 - Chap 80Bella SeahNo ratings yet

- Financial Risk Management: A Simple IntroductionFrom EverandFinancial Risk Management: A Simple IntroductionRating: 4.5 out of 5 stars4.5/5 (7)

- Introduction To Business Government and SocietyDocument4 pagesIntroduction To Business Government and SocietyMd Imran HossainNo ratings yet

- Sample RESULTS AND DISCUSSIONDocument5 pagesSample RESULTS AND DISCUSSIONexquisiteNo ratings yet

- Fixed Income Class Examples ADocument9 pagesFixed Income Class Examples ADebashis MallickNo ratings yet

- Valuation of Bonds NumericalsDocument30 pagesValuation of Bonds NumericalsankitNo ratings yet

- (A.2) Liabilities - Practice ExercisesDocument8 pages(A.2) Liabilities - Practice ExercisesFrances Nicole Doria MoralesNo ratings yet

- Assignment No 6 - FM Actual Summer 2020 Furqan Farooq-18292Document37 pagesAssignment No 6 - FM Actual Summer 2020 Furqan Farooq-18292Furqan Farooq Vadharia100% (1)

- IAS 32, IFRS7,9 Financial InstrumentsDocument6 pagesIAS 32, IFRS7,9 Financial InstrumentsMazni Hanisah100% (2)

- FM12 CH 05 Tool KitDocument31 pagesFM12 CH 05 Tool KitJamie RossNo ratings yet

- Fedillaga Case13Document19 pagesFedillaga Case13Luke Ysmael FedillagaNo ratings yet

- Module 8 - ReviewerDocument8 pagesModule 8 - ReviewerFiona MiralpesNo ratings yet

- Bond StrategiesDocument6 pagesBond Strategiesamitva2007No ratings yet

- Interest Rates and Bond Valuation: BloombergDocument12 pagesInterest Rates and Bond Valuation: BloombergSatyajit RoyNo ratings yet

- Lã Minh Ngọc - 18071385 - INS3007Document15 pagesLã Minh Ngọc - 18071385 - INS3007Ming NgọhNo ratings yet

- Debt MarketDocument25 pagesDebt MarketSuraj DasNo ratings yet

- Long-Term Debt FinancingDocument53 pagesLong-Term Debt FinancingGaluh Boga KuswaraNo ratings yet

- Chapter 9Document58 pagesChapter 9sasaNo ratings yet

- Chapter 2 TB - Long Term Liabilities StudentsDocument7 pagesChapter 2 TB - Long Term Liabilities StudentsMohammed Al-ghamdiNo ratings yet

- CA Final SFM RTP For May 2023Document18 pagesCA Final SFM RTP For May 2023remoratilemothekheNo ratings yet

- Financial Analyst G&M - Real Estate Test & Case Study (SUMAN SAURABH)Document24 pagesFinancial Analyst G&M - Real Estate Test & Case Study (SUMAN SAURABH)sourabh sinhaNo ratings yet

- Final Practice Questions and SolutionsDocument12 pagesFinal Practice Questions and Solutionsshaikhnazneen100No ratings yet

- Financial Analyst G&M - Real Estate Test & Case StudyDocument19 pagesFinancial Analyst G&M - Real Estate Test & Case StudyDhruv ShahNo ratings yet

- Corp Fin Session 9-10 Bond ValuationDocument20 pagesCorp Fin Session 9-10 Bond Valuationmansi agrawalNo ratings yet

- Final Exam IntermediateDocument24 pagesFinal Exam IntermediateIrene Grace Edralin AdenaNo ratings yet

- Chapters 12B and 12CDocument42 pagesChapters 12B and 12CCarlos VillanuevaNo ratings yet

- Commercial Real Estate Valuation ModelDocument6 pagesCommercial Real Estate Valuation Modelkaran yadavNo ratings yet

- Financial Management Assignment 6 Fixed Investment Management Submitted By-Faisal Ishaq B17079 Case BackgroundDocument6 pagesFinancial Management Assignment 6 Fixed Investment Management Submitted By-Faisal Ishaq B17079 Case BackgroundfaisalNo ratings yet

- Ebersoll Manufacturing CoDocument5 pagesEbersoll Manufacturing CoShemu PlcNo ratings yet

- Quiz - Chapter 3 - Bonds Payable Other ConceptsDocument7 pagesQuiz - Chapter 3 - Bonds Payable Other ConceptsRica Jane Oraiz Lloren89% (9)

- Assessment Task 3Document5 pagesAssessment Task 3Christian N MagsinoNo ratings yet

- Fixed Investment ManagementDocument7 pagesFixed Investment ManagementAmanNo ratings yet

- FE (201312) Paper II - Answer PDFDocument12 pagesFE (201312) Paper II - Answer PDFgaryNo ratings yet

- Strategic Financial Management PDFDocument18 pagesStrategic Financial Management PDFUpkar SinghNo ratings yet

- Ch05 Mini CaseDocument8 pagesCh05 Mini CaseTia1977No ratings yet

- Excel FinanceDocument28 pagesExcel FinanceabdullahNo ratings yet

- Bond Portfolio MGTDocument22 pagesBond Portfolio MGTChandrabhan NathawatNo ratings yet

- 67488bos54240 Cp12ciDocument30 pages67488bos54240 Cp12ciKhawaish MittalNo ratings yet

- 08 Bond InvestmentDocument3 pages08 Bond InvestmentAllegria Alamo100% (1)

- Financial Instrument CIMADocument5 pagesFinancial Instrument CIMAwaqas ahmadNo ratings yet

- Solution Manual For Financial Institutions Markets and Money Kidwell Blackwell Whidbee Sias 11th EditionDocument8 pagesSolution Manual For Financial Institutions Markets and Money Kidwell Blackwell Whidbee Sias 11th EditionAmandaMartinxdwj100% (40)

- BFC5935 - Tutorial 7 SolutionsDocument4 pagesBFC5935 - Tutorial 7 SolutionsXue XuNo ratings yet

- Combinepdf 1 PDFDocument16 pagesCombinepdf 1 PDFandrea arapocNo ratings yet

- Valuation of Financial AssetsDocument47 pagesValuation of Financial AssetsprashantkumbhaniNo ratings yet

- Famba6e Quiz Mod07 032014Document4 pagesFamba6e Quiz Mod07 032014aparna jethaniNo ratings yet

- Chapter 1 - CompleteDocument27 pagesChapter 1 - Completemohsin razaNo ratings yet

- MVJUSTINIANI - BAFACR16 - INTERIM ASSESSMENT 1 - 3T - AY2022 23 With Answer KeysDocument4 pagesMVJUSTINIANI - BAFACR16 - INTERIM ASSESSMENT 1 - 3T - AY2022 23 With Answer KeysDe Gala ShailynNo ratings yet

- MNGT 604 Day2 Problem Set Solutions-2Document7 pagesMNGT 604 Day2 Problem Set Solutions-2harini muthuNo ratings yet

- Question No. 1 Is Compulsory. Attempt Any Four Questions From The Remaining Five Questions. Working Notes Should Form Part of The AnswerDocument5 pagesQuestion No. 1 Is Compulsory. Attempt Any Four Questions From The Remaining Five Questions. Working Notes Should Form Part of The Answeradarsh agrawalNo ratings yet

- Quiz Chapter+3 Bonds+PayableDocument3 pagesQuiz Chapter+3 Bonds+PayableRena Jocelle NalzaroNo ratings yet

- Answer To Q On IFRS 9Document4 pagesAnswer To Q On IFRS 9johny SahaNo ratings yet

- Auditing Problem Final Exam With Answer Only, No SolutionDocument23 pagesAuditing Problem Final Exam With Answer Only, No SolutionRheu Reyes100% (1)

- SFM Q MTP 1 Final May22Document5 pagesSFM Q MTP 1 Final May22Divya AggarwalNo ratings yet

- Accounting 1Document10 pagesAccounting 1Jay EbuenNo ratings yet

- CPK Case AnalysisDocument11 pagesCPK Case AnalysisVikas MotwaniNo ratings yet

- Personal Money Management Made Simple with MS Excel: How to save, invest and borrow wiselyFrom EverandPersonal Money Management Made Simple with MS Excel: How to save, invest and borrow wiselyNo ratings yet

- Cairns Merger With VedantaDocument34 pagesCairns Merger With Vedantaparv salechaNo ratings yet

- Debt Markets - N - 2Document34 pagesDebt Markets - N - 2parv salechaNo ratings yet

- The Boeing Company: FORM 10-QDocument105 pagesThe Boeing Company: FORM 10-Qparv salechaNo ratings yet

- Eco Proj 2Document12 pagesEco Proj 2parv salechaNo ratings yet

- Reading 37 Measuring and Managing Market Risk - AnswersDocument11 pagesReading 37 Measuring and Managing Market Risk - Answerstristan.riolsNo ratings yet

- Answer Key of Ppe Recognition ProblemDocument19 pagesAnswer Key of Ppe Recognition ProblemJaneNo ratings yet

- Report On General Banking Activity of Jamuna BankDocument41 pagesReport On General Banking Activity of Jamuna BankHarunur RashidNo ratings yet

- Are Loyalty Program Members Really EngagedDocument15 pagesAre Loyalty Program Members Really Engagedzoe_zoeNo ratings yet

- BSC (Hons) Business Management (: BMP6003 International HRMDocument25 pagesBSC (Hons) Business Management (: BMP6003 International HRMNazmus Sakib RahatNo ratings yet

- Continuous Improvement Task1Document2 pagesContinuous Improvement Task1pravesh bhattaraiNo ratings yet

- Soal Uts Dak Fo TeoryDocument5 pagesSoal Uts Dak Fo Teorykomang olinNo ratings yet

- Case Study Unit 2Document2 pagesCase Study Unit 2Nga LêNo ratings yet

- LSS ScoDocument3 pagesLSS ScoerwinantokaNo ratings yet

- Inventory KPI - SAP TransactionsDocument3 pagesInventory KPI - SAP TransactionsGabrielNo ratings yet

- Articles of Incorporation-Stock Corp - CNL Management CorpDocument7 pagesArticles of Incorporation-Stock Corp - CNL Management CorpKevin CastrojasNo ratings yet

- Afar1 Grp4 Acctng4materials Jit BackflushDocument39 pagesAfar1 Grp4 Acctng4materials Jit BackflushAngela Miles DizonNo ratings yet

- Discover The Finest Indian Flavors at The Indian Bazaar New Jersey's Premier Indian Grocery StoreDocument2 pagesDiscover The Finest Indian Flavors at The Indian Bazaar New Jersey's Premier Indian Grocery StoreIsabella DillonNo ratings yet

- Pengajuan Soal Uts Dari Kelas EDocument1 pagePengajuan Soal Uts Dari Kelas EHikmatullahNo ratings yet

- A Project Lifecycle Perspective On Stakeholder Influence Strategies in Global ProjectsDocument17 pagesA Project Lifecycle Perspective On Stakeholder Influence Strategies in Global Projectsnromy2006No ratings yet

- Mubarok Hossain CVDocument3 pagesMubarok Hossain CVsharif261No ratings yet

- Chaitanya Investors Presentation Dec 2014Document33 pagesChaitanya Investors Presentation Dec 2014CA Pavan KumarNo ratings yet

- Damodaram Sanjivayya National Law University Visakhapatnam, A.P., IndiaDocument19 pagesDamodaram Sanjivayya National Law University Visakhapatnam, A.P., IndiaAbhijit Singh ChaturvediNo ratings yet

- Symbiosis Institute of Management Studies: Assignment OnDocument10 pagesSymbiosis Institute of Management Studies: Assignment OnamitcmsNo ratings yet

- Department of Education: Region Iv-A Calabarzon Schools Division of BatangasDocument6 pagesDepartment of Education: Region Iv-A Calabarzon Schools Division of BatangasRoylendel HernandezNo ratings yet

- Academy: Soil Stabilised Brick (SSB) Production Training Course For Contractors & Construction EntrepreneursDocument4 pagesAcademy: Soil Stabilised Brick (SSB) Production Training Course For Contractors & Construction Entrepreneurspquiroga2No ratings yet

- Zinka Logistics Solutions - R-25092020Document8 pagesZinka Logistics Solutions - R-25092020Atiqur Rahman BarbhuiyaNo ratings yet

- Varun Manian, MD Radiance Realty, Ranks Among The Top Entrepreneurs in The CountryDocument8 pagesVarun Manian, MD Radiance Realty, Ranks Among The Top Entrepreneurs in The CountryAkansha SinghNo ratings yet

- Ford MotorDocument27 pagesFord MotorBahar Uddin100% (8)

- DWS LIST - Ao 11 2Document66 pagesDWS LIST - Ao 11 2sei gosaNo ratings yet

- Key Unit 1 - 1Document24 pagesKey Unit 1 - 1Ezequiel VerbauwedeNo ratings yet