Download as docx, pdf, or txt

You might also like

- Assignment HPGD2203 Educational Management January 2023 Semester - Specific InstructionDocument10 pagesAssignment HPGD2203 Educational Management January 2023 Semester - Specific InstructionSITI RUHAIDA BINTI MUSTAFA STUDENTNo ratings yet

- AB3601 - Strategic Management Course Outline 2021 - 2022 S2Document15 pagesAB3601 - Strategic Management Course Outline 2021 - 2022 S2Joelle LimNo ratings yet

- Courseworkbbmf 2093 Jun 19Document9 pagesCourseworkbbmf 2093 Jun 19bubbleteaNo ratings yet

- Family Pension For W.b.govt Employees (Death Case)Document2 pagesFamily Pension For W.b.govt Employees (Death Case)Pranab Banerjee100% (1)

- UntitledDocument52 pagesUntitledYEN YEN CHONGNo ratings yet

- Group Assignment Guideline - Strategic Management - 2022 Sem 1Document6 pagesGroup Assignment Guideline - Strategic Management - 2022 Sem 1yohan madushankaNo ratings yet

- Group Assignment - 2210Document7 pagesGroup Assignment - 2210LAU CHENG JIANo ratings yet

- Unit Guide - Corporate FinanceDocument10 pagesUnit Guide - Corporate FinanceAn Pham ThuyNo ratings yet

- Analysis of Financial StatementsDocument8 pagesAnalysis of Financial StatementsAsger Richard Steffen HansenNo ratings yet

- Soc 101Document7 pagesSoc 101Sikder MizanNo ratings yet

- INC3701 2022 JanFeb ExaminationDocument4 pagesINC3701 2022 JanFeb ExaminationDeutro HeavysideNo ratings yet

- Unit IntroductionDocument7 pagesUnit IntroductionHuyen NguyenNo ratings yet

- Group Research Plan Form TemplateDocument4 pagesGroup Research Plan Form TemplateMargie JavierNo ratings yet

- Tan Yee Ling 2RFI12Document33 pagesTan Yee Ling 2RFI12MIN ZHE ONGNo ratings yet

- 6.1 Assignment C - ADT204 Campaign Execution - 202304 - 20%Document11 pages6.1 Assignment C - ADT204 Campaign Execution - 202304 - 20%huilisiew0116No ratings yet

- MAN201 - Organizational Behavior - Trimester 3.2022 - 2023 by Chau Ly Updated 23 May 2023 - OB 48 - 1Document11 pagesMAN201 - Organizational Behavior - Trimester 3.2022 - 2023 by Chau Ly Updated 23 May 2023 - OB 48 - 1Tiến PhạmNo ratings yet

- OBD-Individual-Final-Project-Exam-Equivalent 2023-2024-1Document5 pagesOBD-Individual-Final-Project-Exam-Equivalent 2023-2024-1yogen thiranNo ratings yet

- Case Study Presentation (Modus Operandi) With APPENDIX-ADocument3 pagesCase Study Presentation (Modus Operandi) With APPENDIX-Asakshi raiNo ratings yet

- Null 2Document10 pagesNull 2Brian Takudzwa MuzembaNo ratings yet

- BUSI 1215-S12 Fall 2023 Charlton PeterDocument4 pagesBUSI 1215-S12 Fall 2023 Charlton PetergurdevdddNo ratings yet

- I2F Individual Assignment QA Aug 2020Document4 pagesI2F Individual Assignment QA Aug 2020Dylan Rabin PereiraNo ratings yet

- SBFS1103 Thinking Skills and Problem SolvingDocument13 pagesSBFS1103 Thinking Skills and Problem SolvingSimon RajNo ratings yet

- (HUMBUS3) (RX-28) Human Resource Management 3 (July 2016) v5Document8 pages(HUMBUS3) (RX-28) Human Resource Management 3 (July 2016) v5waltdynasty777No ratings yet

- Financial Data AnalysisDocument8 pagesFinancial Data AnalysisAsger Richard Steffen HansenNo ratings yet

- Msw2ndyr (E) 2Document11 pagesMsw2ndyr (E) 2sadib91609No ratings yet

- Universal Human Values (All Branches) 3 /0 /0 /3Document3 pagesUniversal Human Values (All Branches) 3 /0 /0 /3JaneeraNo ratings yet

- Vocational Guidance ManualDocument13 pagesVocational Guidance ManualScribdTranslationsNo ratings yet

- BR2210 OutlineDocument6 pagesBR2210 OutlineSherry SherryNo ratings yet

- MAAN-ASG-Second Year (July 2022 January 2023)Document13 pagesMAAN-ASG-Second Year (July 2022 January 2023)Debsruti SahaNo ratings yet

- Bachelor of Engineering (Honours) Biomedical Engineering Bachelor of Engineering (Honours) Mechatronics EngineeringDocument11 pagesBachelor of Engineering (Honours) Biomedical Engineering Bachelor of Engineering (Honours) Mechatronics EngineeringEsther LuehNo ratings yet

- Assignment Submission and Assessment BBSS1103 Statistical Method / Kaedah Statistik September 2018Document9 pagesAssignment Submission and Assessment BBSS1103 Statistical Method / Kaedah Statistik September 2018azrulfazwanNo ratings yet

- Statistics 4th Edition Agresti Test BankDocument27 pagesStatistics 4th Edition Agresti Test Banksamuelsalaswfspqdaoyi100% (16)

- 4 5938531815663866064Document70 pages4 5938531815663866064helawi'sNo ratings yet

- Rubrik Solving ProblemDocument10 pagesRubrik Solving ProblemSjkt TajulNo ratings yet

- Assignment / TugasanDocument10 pagesAssignment / TugasanSaran CoddyNo ratings yet

- ABMF3184 AssignmentDocument10 pagesABMF3184 AssignmentChristyNo ratings yet

- CSEC Social Studies Exam Prep 2024 May 1Document58 pagesCSEC Social Studies Exam Prep 2024 May 1armstrongdonroy934No ratings yet

- Risk ManagementDocument107 pagesRisk ManagementBill GideonsNo ratings yet

- SSS1133 - Thinking and Intelligence Nov '19Document8 pagesSSS1133 - Thinking and Intelligence Nov '19Theeban GovindosamyNo ratings yet

- BDS CurriculumDocument81 pagesBDS CurriculumRayhan SKNo ratings yet

- B.B.a. Degree and Honours Curriculum 2022-23 (With STR)Document187 pagesB.B.a. Degree and Honours Curriculum 2022-23 (With STR)141. Siddiqui RizwanNo ratings yet

- Roleplay DIS 2020Document1 pageRoleplay DIS 2020Oiyvea JawanNo ratings yet

- CBSE Class 12 Psychology Question Paper 2013Document16 pagesCBSE Class 12 Psychology Question Paper 2013fighterplaneNo ratings yet

- MAT112 GROUP ASS (QUESTION) OCT 2023 (FIinal Copy)Document6 pagesMAT112 GROUP ASS (QUESTION) OCT 2023 (FIinal Copy)annfredy64No ratings yet

- 5569-Management and OrganizationDocument9 pages5569-Management and Organizationbilal132No ratings yet

- Assessment Handout February 2021 (Project 2) Community Service Mpu2192u4Document15 pagesAssessment Handout February 2021 (Project 2) Community Service Mpu2192u4rofiq wibawantoNo ratings yet

- Item Details: Outline For The Course On Dual Purpose Organizations and Social Enterprises (DPOSE) Course InstructorsDocument4 pagesItem Details: Outline For The Course On Dual Purpose Organizations and Social Enterprises (DPOSE) Course InstructorsPriya AgarwalNo ratings yet

- BBCM2013 Mid Term - OB - 202005 - AL - PJ 06072020Document3 pagesBBCM2013 Mid Term - OB - 202005 - AL - PJ 06072020Tvyan RaajNo ratings yet

- PGDmF10 - Research Methodology in Micro FinanceDocument2 pagesPGDmF10 - Research Methodology in Micro FinanceJammy MaNo ratings yet

- Group Assignment (IFA)Document12 pagesGroup Assignment (IFA)Jen SonNo ratings yet

- GP Life Orientation Grade 10 June 2024 QP OnlyDocument9 pagesGP Life Orientation Grade 10 June 2024 QP Onlyslindile.b.ntusiNo ratings yet

- 3 Credits, Prerequisite: All Core CoursesDocument5 pages3 Credits, Prerequisite: All Core CoursesSubrata RoyNo ratings yet

- PSY491 Research 1 Spring 2022Document8 pagesPSY491 Research 1 Spring 2022w.onlyonceNo ratings yet

- Assignment HMEF5023 - V2 Educational Leadership May 2020 SemesterDocument5 pagesAssignment HMEF5023 - V2 Educational Leadership May 2020 Semesterchang muiyunNo ratings yet

- Bbcm2013 Mid Term - Ob - 202205Document3 pagesBbcm2013 Mid Term - Ob - 202205Letchumy MuthuNo ratings yet

- F 13 Teaching Demo ObservationDocument2 pagesF 13 Teaching Demo ObservationMIKE CABALTEANo ratings yet

- ProgramproposalDocument11 pagesProgramproposalapi-301334614No ratings yet

- MHRD Two Year Full Time Programme Course Structure and SyllabusDocument59 pagesMHRD Two Year Full Time Programme Course Structure and SyllabusPriyank JainNo ratings yet

- Transforming Central Finance Agencies in Poor Countries: A Political Economy ApproachFrom EverandTransforming Central Finance Agencies in Poor Countries: A Political Economy ApproachNo ratings yet

- e-StatementBRImo 032001062853500 Oct2023 20231023 135624Document2 pagese-StatementBRImo 032001062853500 Oct2023 20231023 135624PANJI ADITYANNo ratings yet

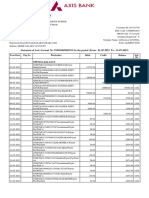

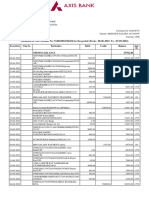

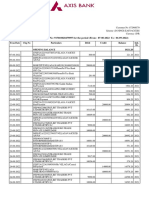

- Axis Bank Statement - 3monthsDocument4 pagesAxis Bank Statement - 3monthsnazeerhussain133No ratings yet

- Amendment To MasterlistDocument2 pagesAmendment To MasterlistArnie CatarininNo ratings yet

- Interest Rate W.E.F From 01.10.2019Document7 pagesInterest Rate W.E.F From 01.10.2019GaurangNo ratings yet

- Basic Examples and Calculations in Life InsuranceDocument42 pagesBasic Examples and Calculations in Life Insurancebranmondi8676No ratings yet

- Customer Details Branch & Account Details: Statement For Account No 60371781119 From 01/04/2022 To 30/09/2022Document25 pagesCustomer Details Branch & Account Details: Statement For Account No 60371781119 From 01/04/2022 To 30/09/2022JAISHANKAR NADARNo ratings yet

- Acct Statement - XX8434 - 07092022Document7 pagesAcct Statement - XX8434 - 07092022Suhail KhanNo ratings yet

- Result Amazon OsirishDocument3 pagesResult Amazon OsirishRoby WahyudiNo ratings yet

- Nk-Statement 5Document3 pagesNk-Statement 5Avtar SNo ratings yet

- 17345Document31 pages17345alicewilliams83nNo ratings yet

- Lalu Muhamad Akbar JanDocument3 pagesLalu Muhamad Akbar JanMobilkamu JakartaNo ratings yet

- Estatement20230706 000233440Document3 pagesEstatement20230706 000233440Mia NahilaNo ratings yet

- Teil - 17 - Foreclosure FraudDocument151 pagesTeil - 17 - Foreclosure FraudNathan BeamNo ratings yet

- Financial Peace University - Member WorkbookDocument153 pagesFinancial Peace University - Member Workbookkate1mayfield-1100% (2)

- Account Statement For The Account: 1926010003332: Branch DetailsDocument7 pagesAccount Statement For The Account: 1926010003332: Branch DetailsOp MassNo ratings yet

- Contemporary Business Mathematics Canadian 11th Edition Hummelbrunner Test BankDocument44 pagesContemporary Business Mathematics Canadian 11th Edition Hummelbrunner Test Bankdieulienheipgo100% (38)

- 4080CDJL956903 Statement of AccountDocument3 pages4080CDJL956903 Statement of AccountJanakiram TammineniNo ratings yet

- StatementDocument4 pagesStatementfinape6897No ratings yet

- CASA Statement May2022 12032023091704Document3 pagesCASA Statement May2022 12032023091704rafa HasyimNo ratings yet

- Relief PackageDocument2 pagesRelief PackageMohammad Imran FarooqiNo ratings yet

- Foreclosure Prevention & Refinance Report: Federal Property Manager'S Report Second Quarter 2021Document50 pagesForeclosure Prevention & Refinance Report: Federal Property Manager'S Report Second Quarter 2021Foreclosure Fraud100% (1)

- Statement Dec 22 XXXXXXXX3948Document31 pagesStatement Dec 22 XXXXXXXX3948Md AdilNo ratings yet

- e-StatementBRImo 459501040308532 May2023 20230615 102222Document3 pagese-StatementBRImo 459501040308532 May2023 20230615 102222Donni AdvNo ratings yet

- Jan 2023Document4 pagesJan 2023divania fonsecaNo ratings yet

- Mortgage and Its Types: Pallavi Chopra Omama Iqbal Shubham Agarwal Anurat Singh Mohit Sharma Vinay VermaDocument11 pagesMortgage and Its Types: Pallavi Chopra Omama Iqbal Shubham Agarwal Anurat Singh Mohit Sharma Vinay VermaSomesh SiddharthNo ratings yet

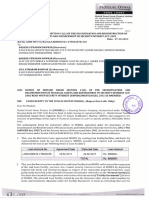

- BANK NOTICE Chandrakant SirDocument8 pagesBANK NOTICE Chandrakant SirAdv. Pranjali DesaiNo ratings yet

- Statement For A/c XXXXXXXXX5471 For The Period 26-Mar-2023 To 04-Apr-2023Document13 pagesStatement For A/c XXXXXXXXX5471 For The Period 26-Mar-2023 To 04-Apr-2023Jadhav PawanNo ratings yet

- Account STMTDocument5 pagesAccount STMTvamsiNo ratings yet

- CNLYw FBP BPKBV TunDocument3 pagesCNLYw FBP BPKBV TunSUBHALAXMI DASNo ratings yet