Download as pdf or txt

You might also like

- MB On PEDocument22 pagesMB On PEfinaarthikaNo ratings yet

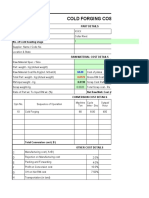

- 94.cold Forging Cost Estimation SheetDocument5 pages94.cold Forging Cost Estimation SheetVenkateswaran venkateswaranNo ratings yet

- Chapter 11 Financial Statement AnalysisDocument3 pagesChapter 11 Financial Statement AnalysisgoerginamarquezNo ratings yet

- 250 High CPC Adsene Ad Network Lists-Technical24x7Document5 pages250 High CPC Adsene Ad Network Lists-Technical24x7Shubham Singh Mehra0% (1)

- Resumen FinancesDocument11 pagesResumen Financesfranchesca guillenNo ratings yet

- Financial Markets and Instruments 6Document33 pagesFinancial Markets and Instruments 6Zhichang ZhangNo ratings yet

- Absolute Vs Relative ValuationDocument3 pagesAbsolute Vs Relative ValuationLilliane EstrellaNo ratings yet

- Business 2 2023Document10 pagesBusiness 2 2023group0840No ratings yet

- Valcom D3Document4 pagesValcom D3Ivan Jay E. EsminoNo ratings yet

- Controllership REVIEWERDocument10 pagesControllership REVIEWERDanielle AndreiNo ratings yet

- Week 2 FINA2207Document31 pagesWeek 2 FINA2207blythe shengNo ratings yet

- Financial Ratios 4Document4 pagesFinancial Ratios 4Natasha Claire MangulabnanNo ratings yet

- Session 21 & 22 (CH 17,18,19 & 20 - RV)Document65 pagesSession 21 & 22 (CH 17,18,19 & 20 - RV)Arun KumarNo ratings yet

- Using Industry Average Multiples For ValuationDocument8 pagesUsing Industry Average Multiples For ValuationSaad AliNo ratings yet

- Valuation ModelsDocument22 pagesValuation Modelsshristy2026No ratings yet

- Chapter 14Document9 pagesChapter 14Kimberly LimNo ratings yet

- FIN-573 - Lecture 5 - Feb 18 2021Document41 pagesFIN-573 - Lecture 5 - Feb 18 2021Abdul BaigNo ratings yet

- 017 Strategy Chapter 9 Strategy Evaluation SlidesDocument32 pages017 Strategy Chapter 9 Strategy Evaluation SlidesNash AsanaNo ratings yet

- Chapter 8 Relative & Real Option Valuation BasicsDocument8 pagesChapter 8 Relative & Real Option Valuation Basics1954032027cucNo ratings yet

- Stock ValuationDocument7 pagesStock ValuationBrenner BolasocNo ratings yet

- Corporate Valuation Mod IDocument29 pagesCorporate Valuation Mod IRavichandran RamadassNo ratings yet

- Module 11-13 (April 26-27, 2023)Document10 pagesModule 11-13 (April 26-27, 2023)Paulo Emmanuel SantosNo ratings yet

- Proprietary Trading - Truth and FictionDocument3 pagesProprietary Trading - Truth and Fictionclmagnaye100% (4)

- 3 Company AnalysisDocument23 pages3 Company AnalysisRasesh ShahNo ratings yet

- Security ValuationDocument10 pagesSecurity ValuationShilpi GuptaNo ratings yet

- 2018 03 10 Screening Jaclyn McclellanDocument52 pages2018 03 10 Screening Jaclyn McclellanYudhi GendutNo ratings yet

- Dark Side of Valuation NotesDocument11 pagesDark Side of Valuation Notesad9292No ratings yet

- PrelimDocument8 pagesPrelimEllah MaeNo ratings yet

- Valuation Final ReviewerDocument43 pagesValuation Final ReviewercamilleNo ratings yet

- Technical Interview Questions - MenakaDocument15 pagesTechnical Interview Questions - Menakajohnathan_alexande_1No ratings yet

- CVP Analysis. Profit AnalysisDocument40 pagesCVP Analysis. Profit AnalysisCherry Mae Nillas CastilloNo ratings yet

- Equity AnalysisDocument6 pagesEquity AnalysisVarsha Sukhramani100% (1)

- AFM NotesDocument4 pagesAFM NotesPhotos Back up 2No ratings yet

- Financial Accounting and ReportingDocument10 pagesFinancial Accounting and ReportingHoneylyn V. ChavitNo ratings yet

- PrelimsDocument6 pagesPrelimsJanna Grace Dela CruzNo ratings yet

- Basic Long Term Financial ConceptsDocument8 pagesBasic Long Term Financial ConceptsJohnpaul FloranzaNo ratings yet

- Dividend Discount ModelDocument17 pagesDividend Discount ModelNirmal ShresthaNo ratings yet

- Presented by - Snibdhatambe, 11 Shreeti Daddha, 09 (Bvimsr)Document39 pagesPresented by - Snibdhatambe, 11 Shreeti Daddha, 09 (Bvimsr)Daddha ShreetiNo ratings yet

- Classification of Financial Ratios On The Basis of FunctionDocument8 pagesClassification of Financial Ratios On The Basis of FunctionRagav AnNo ratings yet

- 06 Econ 118 ValuationDocument19 pages06 Econ 118 ValuationPaul KimNo ratings yet

- Market-Based Valuation: Price MultiplesDocument47 pagesMarket-Based Valuation: Price MultiplesSuci Putri LNo ratings yet

- Gprmo 0003Document1 pageGprmo 0003ApNo ratings yet

- Interpretation of Fin StatementsDocument22 pagesInterpretation of Fin StatementstinashekuzangaNo ratings yet

- 15.020 How Does The Earnings Power Valuation Technique (EPV) Work - Stockopedia FeaturesDocument2 pages15.020 How Does The Earnings Power Valuation Technique (EPV) Work - Stockopedia Featureskuruvillaj2217No ratings yet

- UntitledDocument12 pagesUntitledDanielle AndreiNo ratings yet

- READING 7 Dividend Discount Model (Equity Valuation)Document28 pagesREADING 7 Dividend Discount Model (Equity Valuation)DandyNo ratings yet

- Mauboussin Jan 2014Document22 pagesMauboussin Jan 2014clemloh100% (1)

- 4-Limitations of Valuation Models PDFDocument41 pages4-Limitations of Valuation Models PDFFlovgrNo ratings yet

- Stock ValuationDocument7 pagesStock ValuationYapKJNo ratings yet

- Financial AnalysisDocument15 pagesFinancial AnalysisremmymariethaNo ratings yet

- Valuing Companies in M&A TransactionsDocument24 pagesValuing Companies in M&A TransactionsParth SunejaNo ratings yet

- Equity Vs EVDocument9 pagesEquity Vs EVSudipta ChatterjeeNo ratings yet

- Rosenbaum and Pearl Investment Banking Summary Chps 1 To 3Document18 pagesRosenbaum and Pearl Investment Banking Summary Chps 1 To 3sgyn6cb4thNo ratings yet

- Valuation Theory M& ADocument6 pagesValuation Theory M& AbharatNo ratings yet

- Reading Material-Relative ValuationDocument4 pagesReading Material-Relative ValuationDheia BinoyaNo ratings yet

- Valuation AcquisitionDocument4 pagesValuation AcquisitionKnt Nallasamy GounderNo ratings yet

- Valuations (For Students)Document31 pagesValuations (For Students)Luyanda MhlongoNo ratings yet

- Task 3 - Investment AppraisalDocument12 pagesTask 3 - Investment AppraisalYashmi BhanderiNo ratings yet

- Accounting Ratios: Which Could Be CalculatedDocument9 pagesAccounting Ratios: Which Could Be CalculatedBaher WilliamNo ratings yet

- Analytical Corporate Valuation: Fundamental Analysis, Asset Pricing, and Company ValuationFrom EverandAnalytical Corporate Valuation: Fundamental Analysis, Asset Pricing, and Company ValuationNo ratings yet

- Control-M Agent InstallationDocument5 pagesControl-M Agent Installationrkruck100% (1)

- Study On Advertising Agency and Tourism Industry in NepalDocument5 pagesStudy On Advertising Agency and Tourism Industry in NepalSocial Science Journal for Advanced ResearchNo ratings yet

- 06.17.2021-2021-List of ClientDocument14 pages06.17.2021-2021-List of ClientAntonio NoblezaNo ratings yet

- Learnovate Ecommerce - Finance InternDocument9 pagesLearnovate Ecommerce - Finance Internyash kumar nayakNo ratings yet

- Mchpfsusb Library HelpDocument883 pagesMchpfsusb Library Helpgem1144aaNo ratings yet

- The Dow Chemical Company: Concrete Details Detail 101 Detail 101Document1 pageThe Dow Chemical Company: Concrete Details Detail 101 Detail 101Non Etabas GadnatamNo ratings yet

- Reserve Bank of IndiaDocument10 pagesReserve Bank of IndiasardeepanwitaNo ratings yet

- Annapurna ReportDocument31 pagesAnnapurna ReportPritish KumarNo ratings yet

- Beximco Textile LimitedDocument102 pagesBeximco Textile LimitedFahim100% (1)

- State Bank of India - Parivartan: Case StudyDocument4 pagesState Bank of India - Parivartan: Case StudyKunal BagdeNo ratings yet

- Canadian Business and Society Ethics Responsibilities and Sustainability Canadian 4th Edition Sexty Test BankDocument36 pagesCanadian Business and Society Ethics Responsibilities and Sustainability Canadian 4th Edition Sexty Test Banksyntaxmutuary.urqn100% (32)

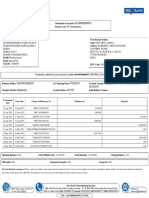

- Account Statement Last 10 TransactionsDocument2 pagesAccount Statement Last 10 TransactionsAshish kumarNo ratings yet

- IGCSE & OL Accounting Worksheets AnswersDocument53 pagesIGCSE & OL Accounting Worksheets Answerssana.ibrahimNo ratings yet

- DBS Bank India Limited Ground Floor, Express Towers, Nariman Point, Mumbai 400021 Maharashtra +91-22-66388888 DBSS0IN0811 400641002Document4 pagesDBS Bank India Limited Ground Floor, Express Towers, Nariman Point, Mumbai 400021 Maharashtra +91-22-66388888 DBSS0IN0811 400641002Isana SatishNo ratings yet

- Concrete Construction Practical Problems and Solutions Akhtar H. Surahyo 9780195797770 Amazon - Com Books PDFDocument3 pagesConcrete Construction Practical Problems and Solutions Akhtar H. Surahyo 9780195797770 Amazon - Com Books PDFJiabin LiNo ratings yet

- Scaling Your Business For Success: Overnight Successes Are Not Always "Overnight"Document6 pagesScaling Your Business For Success: Overnight Successes Are Not Always "Overnight"Invoice Out 2No ratings yet

- Application Form - 88Document2 pagesApplication Form - 88vanessanaobuNo ratings yet

- Metrodata Electronics TBK.: Company Report: January 2019 As of 31 January 2019Document3 pagesMetrodata Electronics TBK.: Company Report: January 2019 As of 31 January 2019Reza CahyaNo ratings yet

- DIGEST-5. Bank of America v. American Realty Corp.Document3 pagesDIGEST-5. Bank of America v. American Realty Corp.Karl EstavillaNo ratings yet

- 86 Inches Quotation For SmartboardDocument1 page86 Inches Quotation For SmartboardJohnson OnuigboNo ratings yet

- Media LiteracyDocument28 pagesMedia LiteracyMa. Shantel CamposanoNo ratings yet

- R Ates For Hiring Auditorium / Lecture Hall of The Convention CentreDocument2 pagesR Ates For Hiring Auditorium / Lecture Hall of The Convention CentreRaj ChouhanNo ratings yet

- Activity Template - Risk Management PlanDocument3 pagesActivity Template - Risk Management PlanSyeda AmeenaNo ratings yet

- Gay7e Irm Ch04Document18 pagesGay7e Irm Ch04Thùy Linh Lê ThịNo ratings yet

- Verdejo VDocument15 pagesVerdejo VCleinJonTiuNo ratings yet

- Industrial Growth in India PDFDocument66 pagesIndustrial Growth in India PDFatipriya choudhary100% (2)

- Tess Zero Accident Program For ZAP Conf 09Document29 pagesTess Zero Accident Program For ZAP Conf 09Armin GomezNo ratings yet

- Oracle Financials Functional Foundation Release 11 Volume 1 Instructor GuideDocument274 pagesOracle Financials Functional Foundation Release 11 Volume 1 Instructor GuideSrinivas GirnalaNo ratings yet