Download as pdf or txt

You might also like

- HDB Sor Jan 2020Document242 pagesHDB Sor Jan 2020kokuei79% (14)

- BCA Unit RatesDocument34 pagesBCA Unit Rateskokuei93% (14)

- Sample Railing Calculation To Euro CodeDocument4 pagesSample Railing Calculation To Euro CodeEric Ng S L100% (6)

- Residential LeaseDocument5 pagesResidential LeasecaplerhomesNo ratings yet

- FIDIC Launches New Yellow Book Subcontract PDFDocument5 pagesFIDIC Launches New Yellow Book Subcontract PDFjenniferipNo ratings yet

- Mason C-RE 585 TDS 2017 (Email)Document31 pagesMason C-RE 585 TDS 2017 (Email)Eric Ng S LNo ratings yet

- Chapter 6 Plant Assets Exercises T3AY2021Document8 pagesChapter 6 Plant Assets Exercises T3AY2021Carl Vincent BarituaNo ratings yet

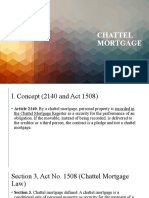

- Chattel Mortgage-Ppt - RFBT 3Document22 pagesChattel Mortgage-Ppt - RFBT 316 Dela Cerna, RonaldNo ratings yet

- PROKON User's Guide PDFDocument636 pagesPROKON User's Guide PDFSAMERJARRAR12394% (17)

- Houses in Multiple Occupation Model Tenancy Agreement: O:ecorri/gen/tenagreeDocument8 pagesHouses in Multiple Occupation Model Tenancy Agreement: O:ecorri/gen/tenagreeSamir SaxenaNo ratings yet

- Boarding House Tenancy AgreementDocument4 pagesBoarding House Tenancy Agreementavalonrun100% (1)

- Zico Law Covid Bill Part 1Document4 pagesZico Law Covid Bill Part 1c2mengNo ratings yet

- Governor Signed 9/1/20: Assembly Bill No. 3088Document72 pagesGovernor Signed 9/1/20: Assembly Bill No. 3088Elisa GetlawgirlNo ratings yet

- COVID Update Guidance Document Draft Final - June 24 PDFDocument9 pagesCOVID Update Guidance Document Draft Final - June 24 PDFJuan Sinhué Flores-OcampoNo ratings yet

- FIDIC FAQs and ResourcesDocument6 pagesFIDIC FAQs and ResourcesGerard BoyleNo ratings yet

- Zico Law Covid Bill Part 2Document2 pagesZico Law Covid Bill Part 2c2mengNo ratings yet

- Quick Guide Unpaid Rent Eviction Guide During COVID Protected and Transition Periods 21621Document2 pagesQuick Guide Unpaid Rent Eviction Guide During COVID Protected and Transition Periods 21621jaydourman2020No ratings yet

- Zico Law Covid Bill Part 3Document4 pagesZico Law Covid Bill Part 3c2mengNo ratings yet

- 2009 Revised IRR For PD 957 HereDocument2 pages2009 Revised IRR For PD 957 HereDianne ComonNo ratings yet

- Ca Covid Tenant Relief Act Info 10-1-21Document2 pagesCa Covid Tenant Relief Act Info 10-1-21Darlene GoldmanNo ratings yet

- Rent Forbearance Agreement That Defers All or A Portion of The Rent Due When Tenants Are Directly Impacted by The Covid-19 CrisisDocument3 pagesRent Forbearance Agreement That Defers All or A Portion of The Rent Due When Tenants Are Directly Impacted by The Covid-19 CrisisRobynNo ratings yet

- Gide Clientalert Covid19 Fidic en 01july2020Document5 pagesGide Clientalert Covid19 Fidic en 01july2020JAZPAKNo ratings yet

- Charges - Company LawDocument39 pagesCharges - Company LawParag Jain DugarNo ratings yet

- Credit FinalsDocument59 pagesCredit FinalsNoel Cagigas FelongcoNo ratings yet

- IBC Short NotesDocument4 pagesIBC Short Notessana khanNo ratings yet

- Obligations and Contracts4Document3 pagesObligations and Contracts4Sha NapolesNo ratings yet

- ECV - Contractual Considerations Under FIDIC Contracts When A Force Majuere Event OccursDocument6 pagesECV - Contractual Considerations Under FIDIC Contracts When A Force Majuere Event OccursRazvan DonciuNo ratings yet

- CSOS 1819 GP 23 Adjudication OrderDocument10 pagesCSOS 1819 GP 23 Adjudication OrderpvtNo ratings yet

- Real Estate and InsolvencyDocument10 pagesReal Estate and InsolvencyharshitaNo ratings yet

- Alert Libyan Civil UnrestDocument3 pagesAlert Libyan Civil UnrestIzo SeremNo ratings yet

- Time, Payment, Performance Bonds and Termination Under The 1999 FIDIC Red Book - LexologyDocument5 pagesTime, Payment, Performance Bonds and Termination Under The 1999 FIDIC Red Book - LexologydadNo ratings yet

- Interim PaymentsDocument29 pagesInterim PaymentsthimirabandaraNo ratings yet

- 19 Sps. Tecklo Vs Rural Bank of PamplonaDocument2 pages19 Sps. Tecklo Vs Rural Bank of PamplonaAngelo NavarroNo ratings yet

- Consolidation Notes: Leaseholds: Property Law & PracticeDocument35 pagesConsolidation Notes: Leaseholds: Property Law & PracticeHedley Horler (scribd)No ratings yet

- Recto and MacedaDocument3 pagesRecto and MacedaDeness Caoili-MarceloNo ratings yet

- Muzyamba V Sinabbomba and Others Case PresentationDocument13 pagesMuzyamba V Sinabbomba and Others Case PresentationNicodemus MwimbaNo ratings yet

- Executions of Collateral During The COVID-19 Pandemic PDFDocument8 pagesExecutions of Collateral During The COVID-19 Pandemic PDFElisabeth BarasantiNo ratings yet

- What Are The Differences Between FIDIC 1999 and 2017 Claims Resolution Procedures - Contract BitesDocument9 pagesWhat Are The Differences Between FIDIC 1999 and 2017 Claims Resolution Procedures - Contract BitesahamedmubeenNo ratings yet

- 2 COTMA Overview Amanda Koh 2Document22 pages2 COTMA Overview Amanda Koh 2Angie Siok Ting LimNo ratings yet

- Fort Bonifacio Vs YllasDocument4 pagesFort Bonifacio Vs Yllascheryl talisikNo ratings yet

- Rented Premises ActDocument36 pagesRented Premises ActHassam Tariq SulehriaNo ratings yet

- Dubai LawDocument16 pagesDubai LawJohn WilliamNo ratings yet

- Summary of The Temporary Measures For Reducing The Impact of Coronavirus DISEASE 2019 (COVID-19) ACT 2020 (ACT 829)Document6 pagesSummary of The Temporary Measures For Reducing The Impact of Coronavirus DISEASE 2019 (COVID-19) ACT 2020 (ACT 829)Jia WeiNo ratings yet

- Formation of Reinsurance AgreementsDocument28 pagesFormation of Reinsurance AgreementsDean RodriguezNo ratings yet

- Janeth Andal - Summary of The CaseDocument6 pagesJaneth Andal - Summary of The CaseShine BillonesNo ratings yet

- MEDIA RELEASE The Impact On Construction Contract ClaimsDocument5 pagesMEDIA RELEASE The Impact On Construction Contract ClaimsAlenNo ratings yet

- Sumangali ArbDocument58 pagesSumangali ArbGopal BhaskarNo ratings yet

- Session 3 - Global Compliance Customs PortDocument25 pagesSession 3 - Global Compliance Customs PortMadhukar AnanaNo ratings yet

- Ground Lease AgreementDocument7 pagesGround Lease AgreementjantravoltamanipodNo ratings yet

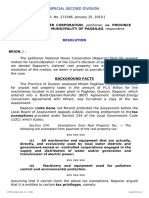

- NAPOCOR vs. Province of QuezonDocument16 pagesNAPOCOR vs. Province of QuezonJay GeeNo ratings yet

- Clause-20 Fidic 1999 - Complete NarrativeDocument55 pagesClause-20 Fidic 1999 - Complete NarrativeUsmanNo ratings yet

- SLQS Qatar CPD No. 101 - Payment Delays in The Construction Industry by Mr. Uditha Tharanga - PresentationDocument31 pagesSLQS Qatar CPD No. 101 - Payment Delays in The Construction Industry by Mr. Uditha Tharanga - Presentationben hurNo ratings yet

- Real Estate: (Regulation & Development)Document17 pagesReal Estate: (Regulation & Development)Vivek KumarNo ratings yet

- Case Digest - Obligations and ContractsDocument7 pagesCase Digest - Obligations and ContractsHurjae Soriano LubagNo ratings yet

- Pledge CasesDocument9 pagesPledge CasesmenforeverNo ratings yet

- PLP Leaseholds PDFDocument33 pagesPLP Leaseholds PDFHedley Horler (scribd)No ratings yet

- Fortnightly Progress Payment Claims in Public Sector Construction ProjectsDocument1 pageFortnightly Progress Payment Claims in Public Sector Construction ProjectsPeter NgNo ratings yet

- 33 Rowland Hill CourtDocument19 pages33 Rowland Hill CourtFlavia!No ratings yet

- Local Mid Sem.Document13 pagesLocal Mid Sem.HanzalaahmedNo ratings yet

- LecA8-SC Mgmt-Determination - UpdatedDocument49 pagesLecA8-SC Mgmt-Determination - UpdatedpablueNo ratings yet

- Uae Vat FaqDocument11 pagesUae Vat FaqTripti Chaturvedi 874No ratings yet

- Clause 20Document54 pagesClause 20Aamer HameedNo ratings yet

- Ebcl Update June 2019 PDFDocument22 pagesEbcl Update June 2019 PDFShreya ManjariNo ratings yet

- Quiz 2 Finals AgraDocument4 pagesQuiz 2 Finals AgraKevin John ArellanoNo ratings yet

- Bank of The Philippine Islands Vs CirDocument8 pagesBank of The Philippine Islands Vs CirmelfabianNo ratings yet

- 026 Philex Mining Co. Vs CIRDocument3 pages026 Philex Mining Co. Vs CIRkeith105No ratings yet

- Mason C-RE 585 TDS 2017 (Email)Document31 pagesMason C-RE 585 TDS 2017 (Email)Eric Ng S LNo ratings yet

- P1 Topical Review Numbers To 20Document2 pagesP1 Topical Review Numbers To 20Eric Ng S LNo ratings yet

- MASON C-RE 585 CSTB 4hrs Fire Test ReportDocument1 pageMASON C-RE 585 CSTB 4hrs Fire Test ReportEric Ng S LNo ratings yet

- Mason C-RE HDB Test Report - Shear 2016Document5 pagesMason C-RE HDB Test Report - Shear 2016Eric Ng S LNo ratings yet

- Mason C-RE HDB Test Report - Tensile 2016Document5 pagesMason C-RE HDB Test Report - Tensile 2016Eric Ng S LNo ratings yet

- 6) Mason Wedge Anchor HDB Approval M12Document1 page6) Mason Wedge Anchor HDB Approval M12Eric Ng S LNo ratings yet

- 5) Mason Wedge Anchor HDB Approval M10Document1 page5) Mason Wedge Anchor HDB Approval M10Eric Ng S LNo ratings yet

- Mason C-RE 585 SDS 2017 (Email)Document24 pagesMason C-RE 585 SDS 2017 (Email)Eric Ng S LNo ratings yet

- Singapore Building Fire Safety Act - Defination of MAADocument2 pagesSingapore Building Fire Safety Act - Defination of MAAEric Ng S LNo ratings yet

- SD01Document1 pageSD01Eric Ng S LNo ratings yet

- Detail of Temporary Site AccessDocument2 pagesDetail of Temporary Site AccessEric Ng S LNo ratings yet

- Structural Fire Precautions: 3.1 GeneralDocument39 pagesStructural Fire Precautions: 3.1 GeneralEric Ng S LNo ratings yet

- ADVERSE POSSESSION by SMT SRIDEVI SHANKER PRL JCJ SIRICILLADocument15 pagesADVERSE POSSESSION by SMT SRIDEVI SHANKER PRL JCJ SIRICILLAParitosh Rachna GargNo ratings yet

- Quiet Title Action - Definition - How It Works - Uses - and CostDocument5 pagesQuiet Title Action - Definition - How It Works - Uses - and CostJohnny LolNo ratings yet

- DEED OF CONVEYANCE MRS. OKWUDIRI NewDocument4 pagesDEED OF CONVEYANCE MRS. OKWUDIRI Newhopecomfort29No ratings yet

- TopaDocument268 pagesTopachotu shahNo ratings yet

- Fundamental Analysis: Capital MarketsDocument19 pagesFundamental Analysis: Capital MarketsIT GAMINGNo ratings yet

- Q. Define Immovable Property. What Property Can Be Transferred ?Document4 pagesQ. Define Immovable Property. What Property Can Be Transferred ?zishanNo ratings yet

- Ifa-I AssDocument3 pagesIfa-I Assnatiman090909No ratings yet

- Deed of Sale of Motor VehicleDocument2 pagesDeed of Sale of Motor VehicleCyrus ArmamentoNo ratings yet

- Problems of Leasehold ImprovementsDocument8 pagesProblems of Leasehold ImprovementsDoren Joy Aguelo BatucanNo ratings yet

- DRAFT Minutes of Sutton Civic Society General Meeting 26.10.22Document3 pagesDRAFT Minutes of Sutton Civic Society General Meeting 26.10.22etajohnNo ratings yet

- Essential Conditions of Transfer of Property Under Transfer of Property Act, 1882 (Act 4 of 1882)Document6 pagesEssential Conditions of Transfer of Property Under Transfer of Property Act, 1882 (Act 4 of 1882)Vidya Bhaskar Singh Nandiyal76% (21)

- Listing Agreement Josh Villa MelastiDocument4 pagesListing Agreement Josh Villa Melastiipo throwdownNo ratings yet

- 1 Jorge de Ocampo vs. Jose OlleroDocument2 pages1 Jorge de Ocampo vs. Jose Olleromei atienza100% (1)

- Pre-Trial Brief 1Document6 pagesPre-Trial Brief 1Paris ValenciaNo ratings yet

- ROD ComplaintDocument15 pagesROD ComplaintK FineNo ratings yet

- Unit Converter: All in One: Ropani System Bigha System Square Feet Square MeterDocument3 pagesUnit Converter: All in One: Ropani System Bigha System Square Feet Square Meterपोखराको घरNo ratings yet

- Samboan FSDocument6 pagesSamboan FSalvic rodaNo ratings yet

- S.no Zone Site ID Site NameDocument33 pagesS.no Zone Site ID Site NamemanojbaislaNo ratings yet

- Payoneer Rental Agreement - Docx FinalDocument2 pagesPayoneer Rental Agreement - Docx Finalteri41248No ratings yet

- Understanding Tax Increment Financing (TIF)Document30 pagesUnderstanding Tax Increment Financing (TIF)David DillnerNo ratings yet

- 6 Monthly Report Sep 2022Document11 pages6 Monthly Report Sep 2022MANDEEP SINGHNo ratings yet

- Dispute Settlement Mechanisms - Land Law PSDADocument7 pagesDispute Settlement Mechanisms - Land Law PSDALuv SharmaNo ratings yet

- Acorn Demographics 2013 PDFDocument108 pagesAcorn Demographics 2013 PDFIon CristianNo ratings yet

- 2 Parameters of Site Selection and Analysis PDFDocument48 pages2 Parameters of Site Selection and Analysis PDFmark joseph100% (1)

- Calculating Your Net Worth: Assets LiabilitiesDocument1 pageCalculating Your Net Worth: Assets LiabilitiesgowthamNo ratings yet

- Audit of PPE Initial MeasurementDocument2 pagesAudit of PPE Initial MeasurementGwyneth TorrefloresNo ratings yet

- Miraflor, Hector (AREM 124)Document5 pagesMiraflor, Hector (AREM 124)Hector MiraflorNo ratings yet