Download as pdf or txt

You might also like

- Your Statement: Ultimate Awards Credit CardDocument12 pagesYour Statement: Ultimate Awards Credit CardLiza LayaNo ratings yet

- Acct For ConsignmnetDocument12 pagesAcct For Consignmnetsamuel debebe100% (2)

- Bill of ExchangeDocument18 pagesBill of ExchangeDark XYNo ratings yet

- Bills of ExchangeDocument22 pagesBills of ExchangePRAKHAR GUPTANo ratings yet

- Ch.6 Bills of Exchange Principles of Accounting NotesDocument7 pagesCh.6 Bills of Exchange Principles of Accounting NotesMUHAMMAD AMIRNo ratings yet

- BOE ConceptDocument4 pagesBOE ConceptNaman MalaniNo ratings yet

- Bills of ExchangeDocument2 pagesBills of Exchangesubba199533333350% (2)

- Consignment AccountsDocument23 pagesConsignment AccountsDr. Avijit Roychoudhury100% (1)

- Consignment Account TheoryDocument3 pagesConsignment Account TheoryPrincess AmmyNo ratings yet

- ConsignmentDocument9 pagesConsignmentthella deva prasadNo ratings yet

- In The Books of AcceptorDocument2 pagesIn The Books of Acceptormanan tyagiNo ratings yet

- Key Terms and Chapter Summary 8Document3 pagesKey Terms and Chapter Summary 8Devansh DwivediNo ratings yet

- Chapter 8Document18 pagesChapter 8Mishu GuptaNo ratings yet

- Journal Entries in The Books of DrawerDocument2 pagesJournal Entries in The Books of DrawerAMIN BUHARI ABDUL KHADER67% (3)

- Journal Entries in The Books of Drawer.Document1 pageJournal Entries in The Books of Drawer.AMIN BUHARI ABDUL KHADERNo ratings yet

- Class Notes of Consignor & ConsigneeDocument13 pagesClass Notes of Consignor & ConsigneeDb100% (1)

- Chapter 6Document11 pagesChapter 6Gautam KumarNo ratings yet

- Cbse Xi Compiled by Sudhir Sinha AccountsDocument2 pagesCbse Xi Compiled by Sudhir Sinha AccountsSudhir SinhaNo ratings yet

- SGR WAGH Bills of Exchange Full - 20210819 - 210205Document59 pagesSGR WAGH Bills of Exchange Full - 20210819 - 210205UrfiNo ratings yet

- Accounts and RulesDocument2 pagesAccounts and RulesKishore MurugananthamNo ratings yet

- Ledger and Trial BalanceDocument24 pagesLedger and Trial BalanceMd.Amir hossain khan100% (1)

- Model Journal Entries: If CreditDocument3 pagesModel Journal Entries: If Creditjaivik_ce7584No ratings yet

- ConsignmentDocument22 pagesConsignmentAkshat jainNo ratings yet

- Ca FND Accounting Process - IiDocument11 pagesCa FND Accounting Process - IiPraveen kumarNo ratings yet

- Acquisition of BusinessDocument14 pagesAcquisition of BusinessTholai Nokku [ தொலை நோக்கு ]No ratings yet

- Class 11 Accountancy Chapter-8 Bill of ExchangeDocument6 pagesClass 11 Accountancy Chapter-8 Bill of ExchangeGoutham GouthamNo ratings yet

- Hire Purchase, Lease and Instalment PurchaseDocument30 pagesHire Purchase, Lease and Instalment PurchaseMunmun MishraNo ratings yet

- Bill of ExchangeDocument12 pagesBill of ExchangeSunday Ngbede ocholaNo ratings yet

- Control Accounts NotesDocument7 pagesControl Accounts NotesRithvik SangilirajNo ratings yet

- 5 6197227591506591842 PDFDocument8 pages5 6197227591506591842 PDFphani chowdaryNo ratings yet

- CCP302Document27 pagesCCP302api-3849444No ratings yet

- JDocument13 pagesJpalash khannaNo ratings yet

- International PaymentDocument24 pagesInternational PaymentAgung WidyadnyanaNo ratings yet

- ConsignmentDocument16 pagesConsignmentMayank GamingNo ratings yet

- Basis of AccountingDocument10 pagesBasis of AccountingDiahNo ratings yet

- CONSIGNMENT ACCOUNT - Docx2Document8 pagesCONSIGNMENT ACCOUNT - Docx2Gamer nestNo ratings yet

- Key Terms and Chapter Summary-9Document2 pagesKey Terms and Chapter Summary-9Rudravisek SahuNo ratings yet

- Summary of Accounting EntriesDocument7 pagesSummary of Accounting EntriesABINASHNo ratings yet

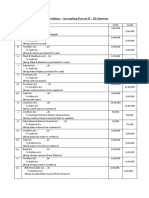

- Solutions To Revisionary ProblemsDocument58 pagesSolutions To Revisionary ProblemsM JEEVARATHNAM NAIDUNo ratings yet

- Solutions To Revisionary Problems IIDocument53 pagesSolutions To Revisionary Problems IIM JEEVARATHNAM NAIDUNo ratings yet

- Types of Transaction: Being Name of Person's Cheque Returned ChequeDocument2 pagesTypes of Transaction: Being Name of Person's Cheque Returned ChequeDipendra GiriNo ratings yet

- Imp Banking TransactionsDocument1 pageImp Banking Transactionsbabumosaai3No ratings yet

- 110-Chapter 3 - Books of Original Entry-Journal - WMDocument21 pages110-Chapter 3 - Books of Original Entry-Journal - WMaaditya kumar jhaNo ratings yet

- Consignment Accounts: 2.0 ObjectiveDocument16 pagesConsignment Accounts: 2.0 ObjectivevasanthaNo ratings yet

- MBA Accounts For ManagerDocument3 pagesMBA Accounts For ManagerGayathri GopiramnathNo ratings yet

- ConsignmentDocument11 pagesConsignmentprince1900No ratings yet

- Comparative Study of Subsidiary BooksDocument4 pagesComparative Study of Subsidiary Booksbhawanar674No ratings yet

- AccountsDocument13 pagesAccountspalash khannaNo ratings yet

- Bills of Exchange1Document16 pagesBills of Exchange1qtpfwlyv34No ratings yet

- Bills PayableDocument2 pagesBills Payablei readyNo ratings yet

- Board Paper-2022-XIDocument8 pagesBoard Paper-2022-XIRn GuptaNo ratings yet

- Kendriya Vidyalaya Sangathan, Lucknow Region TERM-II 2021-22 Marking Scheme Class - XI Subject - AccountancyDocument4 pagesKendriya Vidyalaya Sangathan, Lucknow Region TERM-II 2021-22 Marking Scheme Class - XI Subject - AccountancyThe Web RendezvousNo ratings yet

- Principales of AccountingDocument30 pagesPrincipales of AccountinggaurabNo ratings yet

- Chapter 5 - Perpetual Vs Periodic SystemDocument4 pagesChapter 5 - Perpetual Vs Periodic SystemkanyaNo ratings yet

- ProblemsDocument12 pagesProblemsShereen FathimaNo ratings yet

- 11 Ac JournalDocument3 pages11 Ac Journalidumban_chandraNo ratings yet

- Bills of ExchangeDocument8 pagesBills of ExchangeAnonymous MhCdtwxQINo ratings yet

- Hire Purchases System-Dr. S.K.GuptaDocument7 pagesHire Purchases System-Dr. S.K.GuptaVasundhara DNo ratings yet

- Mr. Honey's Small Banking Dictionary (English-German)From EverandMr. Honey's Small Banking Dictionary (English-German)Rating: 1 out of 5 stars1/5 (2)

- Chapter-16.ms Office SuiteDocument26 pagesChapter-16.ms Office SuiteRaj Srivastav RJNo ratings yet

- Chapter 14. DatabaseDocument11 pagesChapter 14. DatabaseRaj Srivastav RJNo ratings yet

- Uppcs One: Click To Join Our Telegram ChannelDocument14 pagesUppcs One: Click To Join Our Telegram ChannelRaj Srivastav RJNo ratings yet

- Indian Institute of Technology Kanpur: Recruitment SectionDocument11 pagesIndian Institute of Technology Kanpur: Recruitment SectionRaj Srivastav RJNo ratings yet

- Smart Task-1 (VCE)Document3 pagesSmart Task-1 (VCE)Pampana Bala Sai Saroj RamNo ratings yet

- Payslip 147988 202312-27Document1 pagePayslip 147988 202312-27SUNKARA ISNo ratings yet

- Ibs Kuala Pilah 1 31/05/23Document9 pagesIbs Kuala Pilah 1 31/05/23NATASHANo ratings yet

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument3 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceNARENDER AINGHNo ratings yet

- New File-5.09.2023Document3 pagesNew File-5.09.2023vasivanathNo ratings yet

- Gmail - Re - '414598210' NO OBJECTION CERTIFICATE ISSUANCE REQUESTDocument2 pagesGmail - Re - '414598210' NO OBJECTION CERTIFICATE ISSUANCE REQUESTajeetsinghrajput143No ratings yet

- Company Name Name of The PersonDocument6 pagesCompany Name Name of The PersonAnand JohnNo ratings yet

- Chapter 1 IntroductionDocument10 pagesChapter 1 Introductionshrikrushna javanjalNo ratings yet

- Notice of Assessment 2019 04 29 02 32 21 264865Document4 pagesNotice of Assessment 2019 04 29 02 32 21 264865Dennis EnnsNo ratings yet

- HSC Past Paper Questions 2u Maths - Time Payments 1Document1 pageHSC Past Paper Questions 2u Maths - Time Payments 1greycouncilNo ratings yet

- Indeminity BondDocument3 pagesIndeminity BondAli KhanNo ratings yet

- Cibil - Saurabh RaskarDocument4 pagesCibil - Saurabh RaskarSaurabh RaskarNo ratings yet

- PrefrDocument2 pagesPrefrsoniNo ratings yet

- IRCTC Next Generation Eticketing SystemDocument2 pagesIRCTC Next Generation Eticketing SystemTushar SinghNo ratings yet

- Irs Dsa Pia Pod FormDocument3 pagesIrs Dsa Pia Pod Formapi-326615022No ratings yet

- Current Account: Co-Operativebank - Co.uk Phone +44 (0) 3457 212 212Document2 pagesCurrent Account: Co-Operativebank - Co.uk Phone +44 (0) 3457 212 212johncampbell5No ratings yet

- Web Payslip 332429 202305 PDFDocument3 pagesWeb Payslip 332429 202305 PDFN.SATHYAMOORTHY MoorthyNo ratings yet

- CCF21042023Document1 pageCCF21042023Dharshini.SNo ratings yet

- WelcomeLetter C022100601030822 18 09 23Document3 pagesWelcomeLetter C022100601030822 18 09 23The Cool Telly UpdateNo ratings yet

- PLDT SOA-unlockedDocument4 pagesPLDT SOA-unlockedJessa AbadianoNo ratings yet

- Lesson 1.3 - Time Value of Money Part 1Document44 pagesLesson 1.3 - Time Value of Money Part 1glenn cardonaNo ratings yet

- Savings Account Statement: Capitec B AnkDocument6 pagesSavings Account Statement: Capitec B Anksipho gumbiNo ratings yet

- Lecture No.3 Proof of CashDocument2 pagesLecture No.3 Proof of Cashdelrosario.kenneth996No ratings yet

- 6th Progress Report WCRC-RevDocument6 pages6th Progress Report WCRC-RevRishabh SinghNo ratings yet

- 4572XXXXXXXXXX99 - 13 12 2023Document5 pages4572XXXXXXXXXX99 - 13 12 2023balwant.bhansaliNo ratings yet

- Chapter 8 Time Value of Money - SolutionDocument7 pagesChapter 8 Time Value of Money - SolutionanjaliNo ratings yet

- Faks Borang Pemindahan Baki: Langkah 1Document1 pageFaks Borang Pemindahan Baki: Langkah 1Mazlan AmingNo ratings yet

- OpTransactionHistory17 08 2020Document5 pagesOpTransactionHistory17 08 2020mouna guruNo ratings yet

- FINVA100 B TimeValueAnalysis Estares JohnReyDocument6 pagesFINVA100 B TimeValueAnalysis Estares JohnReyJohnRey EstaresNo ratings yet