Download as pdf or txt

You might also like

- Final Test Fin533 January 2024Document13 pagesFinal Test Fin533 January 20242023607226No ratings yet

- Assignment 1 Fin533 PDFDocument20 pagesAssignment 1 Fin533 PDFSyafizah Mohd Ali83% (6)

- Financial Asset FV Martin SalipadaDocument18 pagesFinancial Asset FV Martin SalipadaKaren Joy Magsayo100% (2)

- Exhibit D Tenant Rental Ledger Tenant Rental Ledger CardDocument1 pageExhibit D Tenant Rental Ledger Tenant Rental Ledger CardStephanie KaitlynNo ratings yet

- Personal Financial PlanningDocument7 pagesPersonal Financial Planningatma afisah100% (2)

- Case 4-4 Waltham Oil & Lube Center, Inc.: $40,000 Deposit With NationalDocument5 pagesCase 4-4 Waltham Oil & Lube Center, Inc.: $40,000 Deposit With NationalCyd Marie VictorianoNo ratings yet

- Personal Financial PlanningDocument14 pagesPersonal Financial Planningsuhana safieeNo ratings yet

- Family's Financial PlanningDocument25 pagesFamily's Financial PlanningsyafiqahanidaNo ratings yet

- FAMILY'S FINANCIAL PLANNING - Kak FazilahDocument25 pagesFAMILY'S FINANCIAL PLANNING - Kak FazilahsyafiqahanidaNo ratings yet

- Fin 533 Individual Assignment ShafiqulDocument14 pagesFin 533 Individual Assignment Shafiqulhaziq hazrieyNo ratings yet

- Individual Assignment FIN533Document16 pagesIndividual Assignment FIN533SHAHRIZMAN INDRANo ratings yet

- FADLI & MOGAN - TMS COSTINGDocument6 pagesFADLI & MOGAN - TMS COSTINGMogan RajaNo ratings yet

- Laundry Dobi4Share ProjectionDocument13 pagesLaundry Dobi4Share ProjectionTalk 2meNo ratings yet

- Fin533 Individual Assingment (Afiq Hafizi Bin Junaidi) (2023248696) 2Document30 pagesFin533 Individual Assingment (Afiq Hafizi Bin Junaidi) (2023248696) 2afiqh495No ratings yet

- Individual Assignment Muhammad Atiq 2020165909Document11 pagesIndividual Assignment Muhammad Atiq 2020165909Muhammad AtiqNo ratings yet

- Family Financial Planning FIN533Document22 pagesFamily Financial Planning FIN533SITI FATIMAH AMALINA ABDUL RAZAKNo ratings yet

- Bensil Mobil: Finance Staff Hrga Finance OfficerDocument6 pagesBensil Mobil: Finance Staff Hrga Finance Officernasir nasutionNo ratings yet

- Multi A SDN BHDDocument15 pagesMulti A SDN BHDMUHAMMAD AZIB ZAKHWAN BIN ZAKARIA (BG)No ratings yet

- Ayisha PayDocument3 pagesAyisha Paycontact.fidbankNo ratings yet

- Principle of Accounting (DAC2013)Document8 pagesPrinciple of Accounting (DAC2013)Hidayatul HikmahNo ratings yet

- JAYME, Marx Yuri - 2BSMA-B - PAYROLLDocument42 pagesJAYME, Marx Yuri - 2BSMA-B - PAYROLLMarx Yuri JaymeNo ratings yet

- FIN 533 INDIVIDUAL ASSIGNMENT OTW NewDocument30 pagesFIN 533 INDIVIDUAL ASSIGNMENT OTW Newsyed hakeemNo ratings yet

- Personal Assigment PDFDocument13 pagesPersonal Assigment PDFImran Azizi Zulkifli67% (3)

- 2015BDocument236 pages2015Bs88831139No ratings yet

- Hot Qus Class 12thDocument13 pagesHot Qus Class 12thNaveen ShahNo ratings yet

- Individual Assignment - EffaDocument16 pagesIndividual Assignment - EffayuhanaNo ratings yet

- United Architects of The Philippines: - Application Form Amnesty ProgramDocument2 pagesUnited Architects of The Philippines: - Application Form Amnesty ProgramEmir Jan MateoNo ratings yet

- Sample Payroll Calculation - July 2020Document37 pagesSample Payroll Calculation - July 2020Htet NaungNo ratings yet

- Jinkosolar Holding Co., LTD.: Q3 2017 Earnings Call PresentationDocument10 pagesJinkosolar Holding Co., LTD.: Q3 2017 Earnings Call PresentationAshutosh KumarNo ratings yet

- FinancialsDocument10 pagesFinancialskamlesh_kumarNo ratings yet

- Iriz Price List (05 Aug)Document1 pageIriz Price List (05 Aug)Teoh Yun ShengNo ratings yet

- Budgeting Template by RCODocument31 pagesBudgeting Template by RCOrolly_obedencioNo ratings yet

- 10th Module ELearningDocument68 pages10th Module ELearningMahalingam RamasamyNo ratings yet

- Income Statement For 3 YearsDocument5 pagesIncome Statement For 3 YearsATticFistNo ratings yet

- Trading & Profit & Loss Sheet 3Document2 pagesTrading & Profit & Loss Sheet 3Anshul JainNo ratings yet

- Assignment - Operating Lease & Direct Financing LeaseDocument8 pagesAssignment - Operating Lease & Direct Financing Leaseangelian bagadiongNo ratings yet

- Individual AssignmentDocument9 pagesIndividual AssignmentSITI NUR AISYAH MD ROSTANNo ratings yet

- Monthly ExpensesDocument1 pageMonthly Expensesaqilharith69No ratings yet

- KS SDN BHD - Account AdjustmentsDocument6 pagesKS SDN BHD - Account Adjustmentsalia_aziziNo ratings yet

- Ntambara - For MergeDocument6 pagesNtambara - For MergeEmery MugishaNo ratings yet

- Assignment (Repaired)Document11 pagesAssignment (Repaired)nisrinanajihah28No ratings yet

- Individual Assignment FIN 533 - Nur Malinda - BA2501 LatestDocument19 pagesIndividual Assignment FIN 533 - Nur Malinda - BA2501 Latestnuraz3169No ratings yet

- Paf 3023 - Adjusting Entries Exercise SkemaDocument6 pagesPaf 3023 - Adjusting Entries Exercise SkemaLIM LEE THONGNo ratings yet

- Muhamad NadjmiDocument3 pagesMuhamad Nadjmi4B MUHAMAD NADJMI BIN MUHAMAD SHETHNo ratings yet

- Tutorial 1 - Estate Settlement (Q)Document9 pagesTutorial 1 - Estate Settlement (Q)Xin RuNo ratings yet

- Sample Payroll Calculation - June 2020Document37 pagesSample Payroll Calculation - June 2020Htet NaungNo ratings yet

- S1 BookKeep 2nd Sem Final ExamDocument3 pagesS1 BookKeep 2nd Sem Final ExamTan Shu YuinNo ratings yet

- Loan Details Charges: Customer Portal ExperiaDocument4 pagesLoan Details Charges: Customer Portal ExperiaAlpesh KuleNo ratings yet

- Installment CalculatorDocument2 pagesInstallment CalculatorNaveed ArifNo ratings yet

- Bop Kzar ConsultancyDocument40 pagesBop Kzar Consultancyapi-628837449100% (1)

- Abid AliDocument1 pageAbid AliXen cdh818No ratings yet

- Acct225 Cap3Document17 pagesAcct225 Cap3devoflashNo ratings yet

- FIN 533 INDIVIDUAL ASSIGNMENT OTW New - OrganizedDocument30 pagesFIN 533 INDIVIDUAL ASSIGNMENT OTW New - Organizedsyed hakeemNo ratings yet

- Rincian PengeluaranDocument6 pagesRincian PengeluaranAnha RianaNo ratings yet

- Subject: Merit Increase: Emp Code: 901105 Name: Ashish Kumar Singh Designation: Officer Department: ProductionDocument4 pagesSubject: Merit Increase: Emp Code: 901105 Name: Ashish Kumar Singh Designation: Officer Department: ProductionAshish SinghNo ratings yet

- Account AssignmentDocument10 pagesAccount AssignmentkanchanghengNo ratings yet

- FinancialDocument1 pageFinancialWan Ameera DaniaNo ratings yet

- Current Month April To Date Entitlement Amount Deductions Amount DeductionsDocument1 pageCurrent Month April To Date Entitlement Amount Deductions Amount DeductionsBIPINNo ratings yet

- Ae211 Finals QuizDocument20 pagesAe211 Finals QuizDJAN IHIAZEL DELA CUADRANo ratings yet

- 1) Assignment ACC PDFDocument18 pages1) Assignment ACC PDFMashitah ShuibNo ratings yet

- Reforms, Opportunities, and Challenges for State-Owned EnterprisesFrom EverandReforms, Opportunities, and Challenges for State-Owned EnterprisesNo ratings yet

- StockbrokerDocument4 pagesStockbrokerNiño Rey LopezNo ratings yet

- Credit Card BrochureDocument13 pagesCredit Card BrochureA Man GamesNo ratings yet

- Aaicp3718k 2023Document9 pagesAaicp3718k 2023Kamlesh KumarNo ratings yet

- 1.MEFA Final Question Bank (CSE, CSIT, ECE)Document10 pages1.MEFA Final Question Bank (CSE, CSIT, ECE)sravaniNo ratings yet

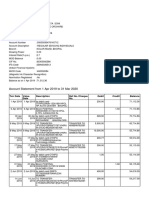

- Account Statement From 1 Apr 2019 To 31 Mar 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument5 pagesAccount Statement From 1 Apr 2019 To 31 Mar 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceVikram SoniNo ratings yet

- IAS 16 PPE Lecture Slides (Updated)Document39 pagesIAS 16 PPE Lecture Slides (Updated)Ndila mangalisoNo ratings yet

- Belgium Private Equity FinancingDocument32 pagesBelgium Private Equity FinancingepithomyNo ratings yet

- AF2108 Week 1-4 StudentDocument6 pagesAF2108 Week 1-4 Studentw.leeNo ratings yet

- WC MGMT Draft 1Document9 pagesWC MGMT Draft 1api-311798551No ratings yet

- World Bank SME FinanceDocument8 pagesWorld Bank SME Financepaynow580No ratings yet

- Final Account Numerical ProblemDocument56 pagesFinal Account Numerical ProblemPrasad BhanageNo ratings yet

- Question Review-Managerial Finance PDFDocument6 pagesQuestion Review-Managerial Finance PDFBang ManroeNo ratings yet

- Kid Deriv CFD Synthetic IndicesDocument5 pagesKid Deriv CFD Synthetic IndicesSamir Ciro Acosta100% (1)

- Fabm 1 - Q2 - Week 1 - Module 1 - Preparing Adjusting Entries of A Service Business - For ReproductionDocument16 pagesFabm 1 - Q2 - Week 1 - Module 1 - Preparing Adjusting Entries of A Service Business - For ReproductionJosephine C QuibidoNo ratings yet

- Buy Bitcoin With Credit Card or Debit Card Immediatelyxberg PDFDocument2 pagesBuy Bitcoin With Credit Card or Debit Card Immediatelyxberg PDFVargas33Cross100% (1)

- I3investor - A Free and Independent Stock Investors PortalDocument3 pagesI3investor - A Free and Independent Stock Investors PortalleekiangyenNo ratings yet

- Fabm 1-PTDocument12 pagesFabm 1-PTMaxene YbañezNo ratings yet

- 23014359-1 23014359 Invoice 160220234Document1 page23014359-1 23014359 Invoice 160220234san_misusNo ratings yet

- GCC Private Banking 2010-2011: Successful Growth Strategies After The Perfect StormDocument60 pagesGCC Private Banking 2010-2011: Successful Growth Strategies After The Perfect StormMark LanyonNo ratings yet

- Chapter 7 - Measurement Application: Section 7.2: Current Value Accounting 7.2.1 Two Versions of Current Value AccountingDocument6 pagesChapter 7 - Measurement Application: Section 7.2: Current Value Accounting 7.2.1 Two Versions of Current Value AccountingNaurah Atika DinaNo ratings yet

- Financial AnalysisDocument25 pagesFinancial AnalysisJason Bernard F. RanasNo ratings yet

- Business Finance Semi ExamDocument1 pageBusiness Finance Semi ExamAimelenne Jay Aninion100% (1)

- Equity Investments in Unlisted CompaniesDocument32 pagesEquity Investments in Unlisted CompaniesANo ratings yet

- Macroeconomics - Introduction and Goals Lecture 1Document32 pagesMacroeconomics - Introduction and Goals Lecture 1enigmaticansh100% (1)

- Islamic Banking QuestionnaireDocument2 pagesIslamic Banking QuestionnaireThe CSS PointNo ratings yet

- Econ 314 - Quiz 1 - Term 2Document2 pagesEcon 314 - Quiz 1 - Term 2Jamie WoodsNo ratings yet

- TaxReturn GuideDocument32 pagesTaxReturn Guideehsany100% (1)

- Introduction To Mutual Fund and Its Various AspectsDocument7 pagesIntroduction To Mutual Fund and Its Various AspectsUzairKhanNo ratings yet