Download as docx, pdf, or txt

You might also like

- CPA Review Notes 2019 - FAR (Financial Accounting and Reporting)From EverandCPA Review Notes 2019 - FAR (Financial Accounting and Reporting)Rating: 3.5 out of 5 stars3.5/5 (17)

- Assignment 1: AP1-5A CL SI CL NCA CA SI SCF SI SC CA NCLDocument10 pagesAssignment 1: AP1-5A CL SI CL NCA CA SI SCF SI SC CA NCLAsad MahmoodNo ratings yet

- CH 10Document32 pagesCH 10Gaurav KarkiNo ratings yet

- Sapp - Deloitte Entrance TestDocument19 pagesSapp - Deloitte Entrance TestTran Pham Quoc ThuyNo ratings yet

- Final PB FAR Batch 7 Sept 2023Document38 pagesFinal PB FAR Batch 7 Sept 2023Leo M. SalibioNo ratings yet

- Afar 02 - Partnership DissolutionDocument8 pagesAfar 02 - Partnership DissolutionMarie GonzalesNo ratings yet

- 2021 - A2S2 Solution-OplossingDocument19 pages2021 - A2S2 Solution-OplossingmeghdyckNo ratings yet

- Liabilities 31.3.20X1 Rs 31.3.20X2 Rs Assets: Course: Fac Quiz:5 Section B DATE: 02/09/2019Document3 pagesLiabilities 31.3.20X1 Rs 31.3.20X2 Rs Assets: Course: Fac Quiz:5 Section B DATE: 02/09/2019Amit GodaraNo ratings yet

- Chap 12 NotesDocument3 pagesChap 12 NotesrbarronsolutionsNo ratings yet

- Ass in Ia 3 Act. 3Document7 pagesAss in Ia 3 Act. 3Resty VillaroelNo ratings yet

- Partnership Q1 To Q3 SolutionsDocument8 pagesPartnership Q1 To Q3 SolutionsJAYARAJALAKSHMI IlangoNo ratings yet

- Lab Pengantar AkuntansiDocument6 pagesLab Pengantar Akuntansirahadatul aishyNo ratings yet

- Consolidated FsDocument45 pagesConsolidated FsNicat IsmayıloffNo ratings yet

- MyacccheatDocument5 pagesMyacccheatraygains23No ratings yet

- Perpetual Inventory Answer KeyDocument3 pagesPerpetual Inventory Answer KeyShane QuintoNo ratings yet

- CAF 06 - TaxationDocument7 pagesCAF 06 - TaxationKhurram ShahzadNo ratings yet

- Q1) May 2011 ZA Q1 - Ear, Mouth & Nose Mouth LTD Nose LTDDocument8 pagesQ1) May 2011 ZA Q1 - Ear, Mouth & Nose Mouth LTD Nose LTDduong duongNo ratings yet

- Adobe Scan Jan 30, 2023Document6 pagesAdobe Scan Jan 30, 2023Karan RajakNo ratings yet

- Chapter 5Document19 pagesChapter 5Izzy BNo ratings yet

- 7-3 PT Pandu Dan PT SadewaDocument2 pages7-3 PT Pandu Dan PT SadewaTeam 1No ratings yet

- 73264bos59105 Inter P1aDocument12 pages73264bos59105 Inter P1aRaish QURESHINo ratings yet

- Fa July2023-Far210-StudentDocument9 pagesFa July2023-Far210-Student2022613976No ratings yet

- ODCON CalculatorDocument6 pagesODCON CalculatorArul Johnson0% (1)

- Key To Correction Seatwork#5Document11 pagesKey To Correction Seatwork#5Shiela Mae CalangiNo ratings yet

- Chapter 12 QR SolutionsDocument14 pagesChapter 12 QR SolutionsNAITIK SHARMANo ratings yet

- Sample Test Mid SolutionsDocument3 pagesSample Test Mid SolutionsRirin Eka MustikasariNo ratings yet

- Tugas MK11Document2 pagesTugas MK11Nan BaeeeNo ratings yet

- Receivable FinancingDocument5 pagesReceivable FinancingSydney De Nieva100% (5)

- Solution Ultimate Sample Paper 2Document7 pagesSolution Ultimate Sample Paper 2Nitin KumarNo ratings yet

- RTP June 2018 AnsDocument29 pagesRTP June 2018 AnsbinuNo ratings yet

- Financial Management MidtermDocument4 pagesFinancial Management MidtermGrace Sinoy BastanteNo ratings yet

- Advanced Cases For Cfs - Testbank Case 1: 905,410 Tax Paid (Cash Payment) Interest Paid (Cash Payments)Document21 pagesAdvanced Cases For Cfs - Testbank Case 1: 905,410 Tax Paid (Cash Payment) Interest Paid (Cash Payments)Uyên Nguyễn Hoàng ThanhNo ratings yet

- Ageing Analysis, Bad Debts - PDDDocument3 pagesAgeing Analysis, Bad Debts - PDDRaman AgnihotriNo ratings yet

- Ratio Analysis Numericals Including Reverse RatiosDocument6 pagesRatio Analysis Numericals Including Reverse RatiosFunny ManNo ratings yet

- CLASS WORK 2 (7 DEC) CHP 6Document10 pagesCLASS WORK 2 (7 DEC) CHP 6Isha KatiyarNo ratings yet

- Accountancy Answer Key - II Puc Annual Exam March 2019Document8 pagesAccountancy Answer Key - II Puc Annual Exam March 2019Akash kNo ratings yet

- B USINESSDocument2 pagesB USINESSMeriam VertudezNo ratings yet

- Chapter 22 Financial Reporting in Hyperinflationary Eco Afar Part 2Document12 pagesChapter 22 Financial Reporting in Hyperinflationary Eco Afar Part 2Shane KimNo ratings yet

- Problem 8-9 Akl 2Document4 pagesProblem 8-9 Akl 2andi nanaNo ratings yet

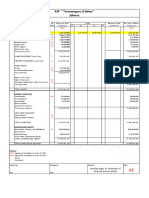

- KAP " Tarumanagara & Rekan" Jakarta: TB'20 TB'19 C E.1 E.2 F G.1 G.2 HDocument2 pagesKAP " Tarumanagara & Rekan" Jakarta: TB'20 TB'19 C E.1 E.2 F G.1 G.2 HAprijanti MalinoNo ratings yet

- Liquidation PQ SolDocument5 pagesLiquidation PQ SolKaran MokhaNo ratings yet

- ACC2001 Lecture 9 IllustrationDocument7 pagesACC2001 Lecture 9 Illustrationmichael krueseiNo ratings yet

- Ratio Analysis For CADocument7 pagesRatio Analysis For CAShahid MahmudNo ratings yet

- 1 RevaluationDocument38 pages1 RevaluationAbdul RaufNo ratings yet

- Sem6 RatioAnalysisLecture 6 JuhiJaiswal 19apr2020Document8 pagesSem6 RatioAnalysisLecture 6 JuhiJaiswal 19apr2020Hanabusa Kawaii IdouNo ratings yet

- Far Situational Solution-1Document6 pagesFar Situational Solution-1Baby BearNo ratings yet

- FAR - Derivatives and Other InvestmentsDocument8 pagesFAR - Derivatives and Other Investmentsmarlout.saritaNo ratings yet

- Pass The Journal Entries For The Following Transactions On The Dissolution of The Firm of P and Q After Various Assets - AccountancyDocument3 pagesPass The Journal Entries For The Following Transactions On The Dissolution of The Firm of P and Q After Various Assets - Accountancydhanya1995No ratings yet

- Ans m2 PaperDocument6 pagesAns m2 Paperbigab31327No ratings yet

- 18-5-SA-V1-S1 Solved Problem Cfs PDFDocument19 pages18-5-SA-V1-S1 Solved Problem Cfs PDFSubbu ..No ratings yet

- MA - Vertical Statement Question BankDocument18 pagesMA - Vertical Statement Question Bankmanav.vakhariaNo ratings yet

- Branch AccountsDocument9 pagesBranch AccountsKalpana SinghNo ratings yet

- XLSXDocument10 pagesXLSXezar zacharyNo ratings yet

- 04 Branch AccountsDocument23 pages04 Branch Accountslasix47725No ratings yet

- 04 Branch Accounts PQ SolDocument24 pages04 Branch Accounts PQ Soltyagivansh1200No ratings yet

- Chapter 22 Financial Reporting in Hyperinflationary Eco Afar Part 2Document11 pagesChapter 22 Financial Reporting in Hyperinflationary Eco Afar Part 2Kathrina RoxasNo ratings yet

- Fund Flow StatementDocument41 pagesFund Flow StatementMahima SinghNo ratings yet

- Introduction To LiabilitiesDocument4 pagesIntroduction To LiabilitiesversNo ratings yet

- FAR Material-2Document8 pagesFAR Material-2Blessy Zedlav LacbainNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- FM FunctionDocument10 pagesFM FunctionDawar Hussain (WT)No ratings yet

- IAS 38 - IntangiblesDocument2 pagesIAS 38 - IntangiblesDawar Hussain (WT)No ratings yet

- IFRS 15 - RevenueDocument15 pagesIFRS 15 - RevenueDawar Hussain (WT)No ratings yet

- Test-3 Obtaining An Engagement Ethics SolutionDocument3 pagesTest-3 Obtaining An Engagement Ethics SolutionDawar Hussain (WT)No ratings yet

- Ias 33 - Basic Earning Per Share: 1. Bonus/Scrip/Cap Issue/Split/ConsolidationDocument2 pagesIas 33 - Basic Earning Per Share: 1. Bonus/Scrip/Cap Issue/Split/ConsolidationDawar Hussain (WT)No ratings yet

- IAS 21 - Foreign Currency TransactionsDocument1 pageIAS 21 - Foreign Currency TransactionsDawar Hussain (WT)No ratings yet

- Ifrs 15Document11 pagesIfrs 15Dawar Hussain (WT)No ratings yet

- IAS 10 - Events After Reporting PeriodDocument1 pageIAS 10 - Events After Reporting PeriodDawar Hussain (WT)No ratings yet

- Ifrs 9 - Financial InstrumentsDocument7 pagesIfrs 9 - Financial InstrumentsDawar Hussain (WT)No ratings yet

- ConsolidationDocument2 pagesConsolidationDawar Hussain (WT)No ratings yet

- CH 03Document50 pagesCH 03lexfred55No ratings yet

- Financing Options - Focus On Excel - 2023 - Student2-1Document26 pagesFinancing Options - Focus On Excel - 2023 - Student2-1Aman DattaNo ratings yet

- BFIN525 - Chapter 11 - Problems & AKDocument10 pagesBFIN525 - Chapter 11 - Problems & AKmohamad yazbeckNo ratings yet

- Intercorporate Acquisitions and Investments in Other EntitiesDocument30 pagesIntercorporate Acquisitions and Investments in Other EntitiesParvez NahidNo ratings yet

- Court of Appeals: DecisionDocument20 pagesCourt of Appeals: DecisionBrian del MundoNo ratings yet

- BK - July Board 2023Document11 pagesBK - July Board 2023akshaydevendra09No ratings yet

- Ataa Educational CompanyDocument480 pagesAtaa Educational CompanyLaugh Trip TayoNo ratings yet

- Week 1 - Accounting EquationDocument23 pagesWeek 1 - Accounting EquationJannyfaye RallecaNo ratings yet

- Profit. Planning and ControlDocument16 pagesProfit. Planning and ControlNischal LawojuNo ratings yet

- GOVERNMENT GRANTS Supplementary Review MaterialDocument2 pagesGOVERNMENT GRANTS Supplementary Review MaterialCaseylyn RonquilloNo ratings yet

- Session1 Introduction To Book KeepingDocument37 pagesSession1 Introduction To Book KeepingSagar ParateNo ratings yet

- Sambhram Institute of Technology, Bangalore Department of Management Studies and Research MBA I Sem - III Internal Exams, December, 2014Document2 pagesSambhram Institute of Technology, Bangalore Department of Management Studies and Research MBA I Sem - III Internal Exams, December, 2014ravi_nyseNo ratings yet

- Earning Per Shares 1Document45 pagesEarning Per Shares 1kaviyapriyaNo ratings yet

- Summary of Cash Sweep ProgramDocument2 pagesSummary of Cash Sweep ProgramCarlos CrisostomoNo ratings yet

- DPR Format SipbDocument6 pagesDPR Format SipbNet PlaZaNo ratings yet

- Cashflow Coverage Ratio of Mga Likha Ni Inay CorporationDocument3 pagesCashflow Coverage Ratio of Mga Likha Ni Inay CorporationKcann ReyesNo ratings yet

- Template Kiwi Start-Ups Agreement For Future Equity: User NotesDocument15 pagesTemplate Kiwi Start-Ups Agreement For Future Equity: User NotesBohdan KozarNo ratings yet

- Manaois FinMan ESSAYDocument2 pagesManaois FinMan ESSAYNCP Shem ManaoisNo ratings yet

- P2mys 2009 Jun ADocument14 pagesP2mys 2009 Jun Aamrita tamangNo ratings yet

- 3rd India Family Office Summit & Awards 2024 - 30-01-2024Document10 pages3rd India Family Office Summit & Awards 2024 - 30-01-2024sreewealthNo ratings yet

- PFRS 11-17Document8 pagesPFRS 11-17Merie Flor BasinilloNo ratings yet

- MidtermsDocument10 pagesMidtermsKIM RAGA0% (1)

- BUS FPX4060 - Assessment4 1Document12 pagesBUS FPX4060 - Assessment4 1AA TsolScholarNo ratings yet

- Ifrs 5 Non-Current Assets Held For Sale and Discontinued OperationsDocument16 pagesIfrs 5 Non-Current Assets Held For Sale and Discontinued OperationsAbdul Hadi SaleemNo ratings yet

- SBI Magnum Gilt Fund - Regular: HistoryDocument1 pageSBI Magnum Gilt Fund - Regular: HistoryVishnu VarshneyNo ratings yet

- 8 Company Auditor: JectivesDocument6 pages8 Company Auditor: JectivesRishabh GuptaNo ratings yet

- Business & Profession Q - A 02.9.2020Document42 pagesBusiness & Profession Q - A 02.9.2020shyamiliNo ratings yet

- Question One Statement of Affairs Disposal AccountDocument11 pagesQuestion One Statement of Affairs Disposal AccountNajah BwalyaNo ratings yet

- Merger Acquisition and Corporate RestructuringDocument30 pagesMerger Acquisition and Corporate Restructuringtafese kuracheNo ratings yet