Download as pdf or txt

You might also like

- 12 LBO Model Seven Days Case StudyDocument6 pages12 LBO Model Seven Days Case StudyDNo ratings yet

- ODUSOLA RISIKAT OLADUNNI - Mar - 2023 PDFDocument1 pageODUSOLA RISIKAT OLADUNNI - Mar - 2023 PDFOluwayemisi EbijimiNo ratings yet

- Quarterly Review and Outlook: Growth Recession Continues Fiscal Policy in NeutralDocument6 pagesQuarterly Review and Outlook: Growth Recession Continues Fiscal Policy in NeutralHonza MynarNo ratings yet

- Van Hoisington Letter, Q3 2011Document5 pagesVan Hoisington Letter, Q3 2011Elliott WaveNo ratings yet

- Lacy Hunt - Hoisington - Quartely Review Q1 2015Document5 pagesLacy Hunt - Hoisington - Quartely Review Q1 2015TREND_7425No ratings yet

- Hoisington Q4Document6 pagesHoisington Q4ZerohedgeNo ratings yet

- CIO CMO - The Pressure's On Emerging Market Central BanksDocument9 pagesCIO CMO - The Pressure's On Emerging Market Central BanksRCS_CFANo ratings yet

- RCSI Weekly Bull/Bear Recap: Nov. 18-22, 2013Document7 pagesRCSI Weekly Bull/Bear Recap: Nov. 18-22, 2013RCS_CFANo ratings yet

- CIO CMO - Approving Fiscal BoostersDocument10 pagesCIO CMO - Approving Fiscal BoostersRCS_CFANo ratings yet

- CIO Weekly Letter - Mexico The Global PiñataDocument4 pagesCIO Weekly Letter - Mexico The Global PiñataRCS_CFANo ratings yet

- Global Forecast: UpdateDocument6 pagesGlobal Forecast: Updatebkginting6300No ratings yet

- IMF World Economic and Financial Surveys Consolidated Multilateral Surveillance Report Sept 2011Document12 pagesIMF World Economic and Financial Surveys Consolidated Multilateral Surveillance Report Sept 2011babstar999No ratings yet

- Mizuho EconomicOutlook 17.5.29Document3 pagesMizuho EconomicOutlook 17.5.29abraNo ratings yet

- Economic Insights 25 02 13Document16 pagesEconomic Insights 25 02 13vikashpunglia@rediffmail.comNo ratings yet

- Quarterly Market Review: Second Quarter 2016Document15 pagesQuarterly Market Review: Second Quarter 2016Anonymous Ht0MIJNo ratings yet

- Gic WeeklyDocument12 pagesGic WeeklycampiyyyyoNo ratings yet

- Understanding Vietnam - A Look Beyond The Facts and PDFDocument24 pagesUnderstanding Vietnam - A Look Beyond The Facts and PDFDawood GacayanNo ratings yet

- The End of An Era: Uarterly EtterDocument10 pagesThe End of An Era: Uarterly EtterthickskinNo ratings yet

- GMO Quarterly Letter-My Sister's Pension Assets 0412 GMO-GranthamDocument11 pagesGMO Quarterly Letter-My Sister's Pension Assets 0412 GMO-GranthamMarko AleksicNo ratings yet

- Charlie McElligott Transcript Nov 14th - 2019Document16 pagesCharlie McElligott Transcript Nov 14th - 2019ZerohedgeNo ratings yet

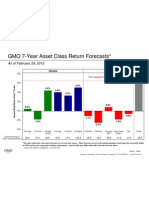

- GMO 7-Year Forecast - Feb '12Document1 pageGMO 7-Year Forecast - Feb '12Douglas RattrayNo ratings yet

- Euro Themes - SpainDocument22 pagesEuro Themes - SpainGuy DviriNo ratings yet

- Second Quarter 2010 GTAA EquitiesDocument68 pagesSecond Quarter 2010 GTAA EquitiesZerohedge100% (1)

- Capital Flow AnalysisDocument8 pagesCapital Flow AnalysisNak-Gyun KimNo ratings yet

- Grantham Quarterly Dec 2011Document4 pagesGrantham Quarterly Dec 2011careyescapitalNo ratings yet

- Second Quarter 2010 GTAA Fixed IncomeDocument32 pagesSecond Quarter 2010 GTAA Fixed IncomeZerohedge100% (1)

- Hayman July 07Document5 pagesHayman July 07grumpyfeckerNo ratings yet

- 7-Year Asset Class Real Return Forecasts : As of May 31, 2019Document1 page7-Year Asset Class Real Return Forecasts : As of May 31, 2019Tim TruaxNo ratings yet

- GMO Grantham July 09Document6 pagesGMO Grantham July 09rodmorleyNo ratings yet

- 7YrForecasts 111Document1 page7YrForecasts 111maxiannozziNo ratings yet

- 16.02 RWC GIAA PresentationDocument35 pages16.02 RWC GIAA PresentationGIAANo ratings yet

- 7YrForecasts 813Document1 page7YrForecasts 813CanadianValueNo ratings yet

- Grantham 4-25-11 Letter Part 1Document19 pagesGrantham 4-25-11 Letter Part 1wompyfratNo ratings yet

- Aig Best of Bernstein SlidesDocument50 pagesAig Best of Bernstein SlidesYA2301100% (1)

- Sustainability of Govt DebtDocument8 pagesSustainability of Govt DebtSpencer RascoffNo ratings yet

- Global Markets Chart Book: High-Grade Bond Yields Plunge To Record LowsDocument12 pagesGlobal Markets Chart Book: High-Grade Bond Yields Plunge To Record LowslosdiabloNo ratings yet

- JPM Global Data Watch Se 2012-09-21 946463Document88 pagesJPM Global Data Watch Se 2012-09-21 946463Siddhartha SinghNo ratings yet

- Yearly Outlook 2011Document36 pagesYearly Outlook 2011Trading FloorNo ratings yet

- How Urban Planners Caused The Housing Bubble, Cato Policy Analysis No. 646Document28 pagesHow Urban Planners Caused The Housing Bubble, Cato Policy Analysis No. 646Cato InstituteNo ratings yet

- Third Quarter 2010 GTAA EquitiesDocument70 pagesThird Quarter 2010 GTAA EquitiesZerohedge100% (1)

- The GIC Weekly Update November 2015Document12 pagesThe GIC Weekly Update November 2015John MathiasNo ratings yet

- GMO 7 Year Asset Class Forecast Apr 14Document1 pageGMO 7 Year Asset Class Forecast Apr 14CanadianValueNo ratings yet

- Economics Docs 2022 184258.ashxDocument65 pagesEconomics Docs 2022 184258.ashxTshepo ThaisiNo ratings yet

- RCSI Presentation - China's Threats: Deflation & Slowing GrowthDocument10 pagesRCSI Presentation - China's Threats: Deflation & Slowing GrowthRCS_CFANo ratings yet

- Gmo Quarterly Letter Q4 2018Document17 pagesGmo Quarterly Letter Q4 2018Stirling AdelhelmNo ratings yet

- Across - The - Curve - in - Rates - and - Structured - Products - and - Across - The - Grade - in - Credit - Products - December 19, 2006 - (Bear, - Stearns - & - Co. - Inc.) PDFDocument60 pagesAcross - The - Curve - in - Rates - and - Structured - Products - and - Across - The - Grade - in - Credit - Products - December 19, 2006 - (Bear, - Stearns - & - Co. - Inc.) PDFQuantDev-MNo ratings yet

- April Commodity OutlookDocument18 pagesApril Commodity OutlookSoren K. Group100% (1)

- Bar Cap 3Document11 pagesBar Cap 3Aquila99999No ratings yet

- Gundlach 6-14-16 Total Return Webcast Slides - Final - UnlockedDocument73 pagesGundlach 6-14-16 Total Return Webcast Slides - Final - UnlockedZerohedge100% (1)

- Global Investment Returns Yearbook 2014Document68 pagesGlobal Investment Returns Yearbook 2014Rosetta RennerNo ratings yet

- PT. Mirae Asset Sekuritas Indonesia - Initiation Report PDFDocument75 pagesPT. Mirae Asset Sekuritas Indonesia - Initiation Report PDFLia HafizaNo ratings yet

- Constructing Low Volatility Strategies: Understanding Factor InvestingDocument33 pagesConstructing Low Volatility Strategies: Understanding Factor InvestingLoulou DePanamNo ratings yet

- GS 2024 MacroDocument28 pagesGS 2024 Macroxiongfeng aiNo ratings yet

- ASEAN Corporate Governance Scorecard Country Reports and Assessments 2019From EverandASEAN Corporate Governance Scorecard Country Reports and Assessments 2019No ratings yet

- Financial Soundness Indicators for Financial Sector Stability in Viet NamFrom EverandFinancial Soundness Indicators for Financial Sector Stability in Viet NamNo ratings yet

- Him Co Interim Update 201611Document2 pagesHim Co Interim Update 201611hedgie58No ratings yet

- Weekly ArgusDocument66 pagesWeekly Argusjean pierreNo ratings yet

- Breakfast With Dave 111610Document5 pagesBreakfast With Dave 111610adam2938No ratings yet

- BUE Report 2018 - Q2Document19 pagesBUE Report 2018 - Q2eric_stNo ratings yet

- Global M A Activity Latest BCG Perpsective 1569564066Document36 pagesGlobal M A Activity Latest BCG Perpsective 1569564066l0ngj0hnsilv3rNo ratings yet

- Baltimore Metropolitan Area: Market ReportDocument18 pagesBaltimore Metropolitan Area: Market ReportKevin ParkerNo ratings yet

- Year in Review: Crude Causes ProblemsDocument1 pageYear in Review: Crude Causes ProblemsAdrian BrownNo ratings yet

- CDC Entry Gate Pass Vibro SandDocument1 pageCDC Entry Gate Pass Vibro Sandcharleejoy0124No ratings yet

- 452B - International BusinessDocument24 pages452B - International BusinessJay Patel88% (8)

- BP SFSF PY ERP607 Wagetypes Catalog Workbook en USDocument48 pagesBP SFSF PY ERP607 Wagetypes Catalog Workbook en USMahmoud ElManakhlyNo ratings yet

- Pre-Test 9Document3 pagesPre-Test 9BLACKPINKLisaRoseJisooJennieNo ratings yet

- Complete 5 - KeyDocument23 pagesComplete 5 - KeyNgânNo ratings yet

- The Foreign Exchange MarketDocument40 pagesThe Foreign Exchange MarketabateNo ratings yet

- (BCTTCK) -TRỊNH HUYỀN LINH-K56CLC3-1701015421Document53 pages(BCTTCK) -TRỊNH HUYỀN LINH-K56CLC3-1701015421Trịnh Huyền LinhNo ratings yet

- SIES School of Business StudiesDocument9 pagesSIES School of Business Studiesansh dengreNo ratings yet

- CII Innovation Awards 2024 BrochureDocument14 pagesCII Innovation Awards 2024 BrochurePreeti Sharma EEELNo ratings yet

- Zimbabwe School Examinations Council: General Certificate of Education Advanced Level 6001/3Document7 pagesZimbabwe School Examinations Council: General Certificate of Education Advanced Level 6001/3chauromweaNo ratings yet

- Session 5 - Basic Tools of FinanceDocument17 pagesSession 5 - Basic Tools of FinanceViviene Seth Alvarez LigonNo ratings yet

- Sunteck Realty LTD.: Rachana Vipul HingarajiaDocument317 pagesSunteck Realty LTD.: Rachana Vipul HingarajiaMr. S0UR48HNo ratings yet

- UMAM Fee Structure EditedVer2Document1 pageUMAM Fee Structure EditedVer2AKMA SAUPINo ratings yet

- SwiggyDocument1 pageSwiggyDoniv VinodNo ratings yet

- Correct Amount of Inventory 677,500Document8 pagesCorrect Amount of Inventory 677,500Maria Kathreena Andrea AdevaNo ratings yet

- Zook On The CoreDocument9 pagesZook On The CoreThu NguyenNo ratings yet

- 581815-K FHC 11112021 En-1Document2 pages581815-K FHC 11112021 En-1Fad Izham LemanNo ratings yet

- Payment Under ProtestDocument2 pagesPayment Under ProtestNorman CorreaNo ratings yet

- Micro Q13 and Key Answer 2017Document9 pagesMicro Q13 and Key Answer 2017Bee FeeNo ratings yet

- GayathriDocument2 pagesGayathrishaikhNo ratings yet

- MegabookDocument23 pagesMegabookHuynh KhuongNo ratings yet

- This Paper Is Not To Be Removed From The Examination HallsDocument54 pagesThis Paper Is Not To Be Removed From The Examination HallskikiNo ratings yet

- Group 1 - Understanding EconomicsDocument30 pagesGroup 1 - Understanding EconomicsVina NallaresNo ratings yet

- Nama: Redi Perdiansyah NIM: 55120110139 Quiz Ke: 9: Stock X Stock y Stock ZDocument5 pagesNama: Redi Perdiansyah NIM: 55120110139 Quiz Ke: 9: Stock X Stock y Stock ZFikky Chandra SilabanNo ratings yet

- Earnings Per ShareDocument2 pagesEarnings Per ShareJohn Ace MadriagaNo ratings yet

- Shapiro Chapter 05 SolutionsDocument18 pagesShapiro Chapter 05 SolutionsRuiting ChenNo ratings yet

- Background: Chapter 11 Debtor/telecommunications Carrier and Its Debtor-Subsidiary Brought AdversaryDocument10 pagesBackground: Chapter 11 Debtor/telecommunications Carrier and Its Debtor-Subsidiary Brought AdversaryJun MaNo ratings yet

- V1 Exam 2 PMDocument31 pagesV1 Exam 2 PMNeerajNo ratings yet