Download as docx, pdf, or txt

You might also like

- Bill 10296080Document1 pageBill 10296080luminitamihai775No ratings yet

- Notification of Change of OwnershipDocument3 pagesNotification of Change of OwnershipMark BurkeNo ratings yet

- Test Bank 3 - GitmanDocument62 pagesTest Bank 3 - GitmanCamille Santos20% (5)

- Supply and Demand How To Find and Trade The Best ZonesNew PDFDocument25 pagesSupply and Demand How To Find and Trade The Best ZonesNew PDFYagnesh Patel100% (12)

- Summer Internship Project Report On "Overview Study of Stock Exchange Market of India" Submitted byDocument31 pagesSummer Internship Project Report On "Overview Study of Stock Exchange Market of India" Submitted byDurgesh YadavNo ratings yet

- Agreement On Rentage of Cocoa Farm LandDocument1 pageAgreement On Rentage of Cocoa Farm LandAlex100% (1)

- Parcel Perfect Integration Service - v7Document8 pagesParcel Perfect Integration Service - v7Ross SaundersNo ratings yet

- Standard Operating Procedure For Collecting CASH On DELIVERYDocument2 pagesStandard Operating Procedure For Collecting CASH On DELIVERYKartik Bhandari100% (3)

- 100kg Fco Trial Shipment of Alluvial Au Gold Dust Available Urgent For Shipment To Buyers IonDocument2 pages100kg Fco Trial Shipment of Alluvial Au Gold Dust Available Urgent For Shipment To Buyers IonSte Desire SarlNo ratings yet

- Introduction Letter - Postnet The Glen: Theglen@Postnet - Co.ZaDocument2 pagesIntroduction Letter - Postnet The Glen: Theglen@Postnet - Co.ZaSimbarashe MarisaNo ratings yet

- CMR Consignment Note FormDocument5 pagesCMR Consignment Note FormGlobal NegotiatorNo ratings yet

- Ms Word Format Audit Engagement Letter Cos Act 2013Document10 pagesMs Word Format Audit Engagement Letter Cos Act 2013kanavNo ratings yet

- Application Form For Foreign Exchange Services: Specify)Document7 pagesApplication Form For Foreign Exchange Services: Specify)Reena Rizza Ocampo0% (1)

- KYC Form (Final)Document1 pageKYC Form (Final)plr.postNo ratings yet

- 2018-11-01 DNA Magazine PDFDocument103 pages2018-11-01 DNA Magazine PDFShane Erasmus20% (5)

- Consignment Accounts: Consignment-What Is It?Document6 pagesConsignment Accounts: Consignment-What Is It?neeraj goyal100% (1)

- CONSIGNMENT ACCOUNT - Docx2Document8 pagesCONSIGNMENT ACCOUNT - Docx2Gamer nestNo ratings yet

- Summary of Accounting EntriesDocument7 pagesSummary of Accounting EntriesABINASHNo ratings yet

- A1 For Import Goods PaymentsDocument3 pagesA1 For Import Goods PaymentskollarajasekharNo ratings yet

- KYC DocumentsDocument3 pagesKYC DocumentsnaseemNo ratings yet

- Customs AssignmentDocument6 pagesCustoms AssignmentBlessing MapokaNo ratings yet

- Advance Payment DisbursementDocument4 pagesAdvance Payment DisbursementAb WahabNo ratings yet

- PB Fees and ChargesDocument32 pagesPB Fees and ChargesechipbkNo ratings yet

- 1 Sea Logistics Business Operation Process Management System 1.1 PurposeDocument6 pages1 Sea Logistics Business Operation Process Management System 1.1 PurposeK58 Phạm Thị Hồng NgọcNo ratings yet

- Military Leave Approval LetterDocument2 pagesMilitary Leave Approval LetterMy love of LifeNo ratings yet

- Investment Application FormDocument2 pagesInvestment Application FormAdnan Zahid100% (1)

- Dormant CompanyDocument3 pagesDormant CompanyAvaniJainNo ratings yet

- Vintage Animal Shippers: Vintage Animalshippers Refunds Form G43Document1 pageVintage Animal Shippers: Vintage Animalshippers Refunds Form G43ABS CONSULTORIANo ratings yet

- Gold ProceduresDocument4 pagesGold ProceduresHoainam2468No ratings yet

- Proof of Funds Letter Template 05Document1 pageProof of Funds Letter Template 05Dk KimNo ratings yet

- How The Shipping Process Works Step by SDocument10 pagesHow The Shipping Process Works Step by SPablo Godoy OssesNo ratings yet

- Hazardous Waste Consignee ReturnsDocument26 pagesHazardous Waste Consignee ReturnsanyinyiaungNo ratings yet

- Attorney and Agent FeesDocument55 pagesAttorney and Agent FeesJimNo ratings yet

- Shipping & Delivery PDFDocument14 pagesShipping & Delivery PDFDozami MarketingNo ratings yet

- Application Format Application For The Post of by AbsorptionDocument3 pagesApplication Format Application For The Post of by Absorptionbonat07No ratings yet

- Build Card Military Lending Act Cardholder AgreementDocument8 pagesBuild Card Military Lending Act Cardholder Agreementprateekmehta92No ratings yet

- Courier 7.18.12Document20 pagesCourier 7.18.12Claremont CourierNo ratings yet

- Letter FormateDocument6 pagesLetter FormateRobin SahaNo ratings yet

- Export Procedure in IndiaDocument16 pagesExport Procedure in IndiaRohan AroraNo ratings yet

- Business Proposition From Dr. Aminudin Abdul KarimDocument2 pagesBusiness Proposition From Dr. Aminudin Abdul KarimViji Raj KumarNo ratings yet

- Management Practices At: Orient Cargo (PVT) LTDDocument16 pagesManagement Practices At: Orient Cargo (PVT) LTDKhuram ManzoorNo ratings yet

- 1 - Engagement Letter FormatDocument3 pages1 - Engagement Letter FormatMuhammad AsimNo ratings yet

- Client Care LetterDocument6 pagesClient Care Letteranh98762No ratings yet

- US Payroll SetupDocument43 pagesUS Payroll Setupgkumarraos100% (1)

- Mcs Depot Drop Ship AgreementDocument5 pagesMcs Depot Drop Ship Agreementpeshkov7No ratings yet

- Letter of Certification - Marital StatusDocument1 pageLetter of Certification - Marital Statusมดน้อย ผู้น่ารักNo ratings yet

- Georgian Customs SystemDocument22 pagesGeorgian Customs SystemRajesh GuptaNo ratings yet

- Courier FormDocument1 pageCourier FormArooz Paul Paul SinghNo ratings yet

- Subscription AgreementDocument5 pagesSubscription AgreementjfmohamadNo ratings yet

- 1.3 Export Shipping DocDocument9 pages1.3 Export Shipping Docjayesh vasaniNo ratings yet

- Trust DeedDocument2 pagesTrust DeedLorrenzo Public SchoolNo ratings yet

- Cash Against DocumentsDocument4 pagesCash Against DocumentsKureshi Sana100% (2)

- Used Cars For Sale Offer FormDocument3 pagesUsed Cars For Sale Offer FormRaymond GabrielNo ratings yet

- Introduction and Brief History of Fund (Read Deligently)Document2 pagesIntroduction and Brief History of Fund (Read Deligently)አረጋዊ ሐይለማርያምNo ratings yet

- Congratulation Contact United Nations Office LondonDocument7 pagesCongratulation Contact United Nations Office Londonmanjeet.singh837824No ratings yet

- Export-Import DocumentationDocument34 pagesExport-Import DocumentationSiddharth OjahNo ratings yet

- APPENDIX 25 B (Legal Agreement-Undertaking Format)Document4 pagesAPPENDIX 25 B (Legal Agreement-Undertaking Format)PrashantNo ratings yet

- Export Customs ProcedureDocument3 pagesExport Customs Procedurefaz_abbasNo ratings yet

- Futro Terms and ConditionsDocument3 pagesFutro Terms and ConditionsMohitNo ratings yet

- MD Riyad VisaDocument3 pagesMD Riyad Visamzu2441139No ratings yet

- Billing and CollectionDocument24 pagesBilling and CollectionRoby IbeNo ratings yet

- Montana LLC Articles of OrgranizationDocument3 pagesMontana LLC Articles of OrgranizationRocketLawyerNo ratings yet

- The Declaration-Cum-Undertaking Under Sec 10 (5), Chapter III of FEMA, 1999 Is Enclosed As UnderDocument1 pageThe Declaration-Cum-Undertaking Under Sec 10 (5), Chapter III of FEMA, 1999 Is Enclosed As UnderarvinfoNo ratings yet

- My Online Dating Experience: I Believe in My Success and Yours TooFrom EverandMy Online Dating Experience: I Believe in My Success and Yours TooNo ratings yet

- 2848 Unit 1 Specialized Financial Accounting Chapter - 1 Consignment RevisedDocument12 pages2848 Unit 1 Specialized Financial Accounting Chapter - 1 Consignment RevisedKersey AquinoNo ratings yet

- TelephoneBill 8253069363Document3 pagesTelephoneBill 8253069363sourajpatelNo ratings yet

- Fin C 000002Document14 pagesFin C 000002Nageshwar SinghNo ratings yet

- Financial Management PORTFOLIO MidDocument8 pagesFinancial Management PORTFOLIO MidMyka Marie CruzNo ratings yet

- FLS011 Application For PenCon Special STLDocument2 pagesFLS011 Application For PenCon Special STLwillienorNo ratings yet

- 77 FDocument3 pages77 FJohn CalvinNo ratings yet

- Housing Development Finance Corporation LimitedDocument3 pagesHousing Development Finance Corporation LimitedHoney AliNo ratings yet

- EBIT - EPS QuestionsDocument6 pagesEBIT - EPS QuestionsTaliya ShaikhNo ratings yet

- Tutorial 5Document5 pagesTutorial 5Jian Zhi TehNo ratings yet

- Lecture 14Document57 pagesLecture 14Billiee ButccherNo ratings yet

- ReceiptDocument1 pageReceiptjohn belhaNo ratings yet

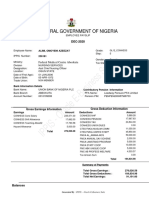

- IPPIS - Oracle E-Business Suite: Federal Government of NigeriaDocument1 pageIPPIS - Oracle E-Business Suite: Federal Government of NigeriaAlimi kehinde100% (1)

- FM CH 2Document18 pagesFM CH 2sosina eseyewNo ratings yet

- Advantages and Disadvantages of Equity SharesDocument2 pagesAdvantages and Disadvantages of Equity Sharespiyush chauhanNo ratings yet

- Lembar Kerja Mengelola Buku Jurnal: Praktek Akuntansi Keuangan (Manual)Document11 pagesLembar Kerja Mengelola Buku Jurnal: Praktek Akuntansi Keuangan (Manual)Putri AgustinaNo ratings yet

- Muthoot Fincorp CalrificationsDocument6 pagesMuthoot Fincorp CalrificationslulughoshNo ratings yet

- Cash and CequizDocument5 pagesCash and CequizMaria Emarla Grace CanozaNo ratings yet

- Case 3 CemexDocument20 pagesCase 3 CemexAsep KurniawanNo ratings yet

- Ecovisionnaire Most Expected TopicsDocument4 pagesEcovisionnaire Most Expected Topicsmayank698945No ratings yet

- Business and MoneyDocument4 pagesBusiness and MoneyPaz MorenoNo ratings yet

- Cash and Proof of Cash ProblemsDocument2 pagesCash and Proof of Cash ProblemsDivine MungcalNo ratings yet

- Money Laundering in IndiaDocument9 pagesMoney Laundering in IndiaRajhas PoonuruNo ratings yet

- Corporation TaxationDocument16 pagesCorporation TaxationMeg Lee0% (1)

- Telus 40042789 2023 03 25Document10 pagesTelus 40042789 2023 03 25Harold KumarNo ratings yet

- 93f9821f Fee Schedule 2023 2024Document16 pages93f9821f Fee Schedule 2023 2024ismaelomugshaNo ratings yet

- Assotech Windsor Court Price ListDocument3 pagesAssotech Windsor Court Price ListGreen Realtech Projects Pvt LtdNo ratings yet