Download as pdf or txt

You might also like

- Chapter 2 Lesson 3 - Discount, Inflation, and TaxDocument9 pagesChapter 2 Lesson 3 - Discount, Inflation, and TaxMae AsuncionNo ratings yet

- Unfinished Agenda Access To FinanceDocument14 pagesUnfinished Agenda Access To Financeliemuel100% (1)

- Europe Industry Analysis On Elevator & Escalator Key Players, Size, Trends, Opportunities and Growth Analysis - Facts and TrendsDocument2 pagesEurope Industry Analysis On Elevator & Escalator Key Players, Size, Trends, Opportunities and Growth Analysis - Facts and Trendssurendra choudharyNo ratings yet

- Jurnal 6Document11 pagesJurnal 6tikotokt203No ratings yet

- Gathergood 2011Document13 pagesGathergood 2011AnonimousssNo ratings yet

- A Luksandera 2014 2Document22 pagesA Luksandera 2014 2zoe regina castroNo ratings yet

- 2022 - June Skills - Thesis Topics Final PDFDocument50 pages2022 - June Skills - Thesis Topics Final PDFJovan PetronijevićNo ratings yet

- The Transformation of Retail Credit Financing in The Wake of The Crises in HungaryDocument15 pagesThe Transformation of Retail Credit Financing in The Wake of The Crises in HungaryGlobal Research and Development ServicesNo ratings yet

- Too Much Debt Will Kill YouDocument22 pagesToo Much Debt Will Kill YouSehat Dinati SimamoraNo ratings yet

- Office Contact Information: Keyu Jin (金 刻羽)Document4 pagesOffice Contact Information: Keyu Jin (金 刻羽)Stephanie CeeNo ratings yet

- Sciencedirect: Financial Education and Financial Literacy in The Czech Education SystemDocument9 pagesSciencedirect: Financial Education and Financial Literacy in The Czech Education SystemAna MariaNo ratings yet

- Binder2023005 PDFDocument25 pagesBinder2023005 PDFRatri PLaksmiNo ratings yet

- 1 s2.0 S0304405X11000717 MainDocument24 pages1 s2.0 S0304405X11000717 MainAmmi JulianNo ratings yet

- Twin Triple DicificDocument17 pagesTwin Triple DicificLe Tieu Ngoc LienNo ratings yet

- Does A Financial Crisis Make Consumers Increasingly Prudent?Document22 pagesDoes A Financial Crisis Make Consumers Increasingly Prudent?Yee Sook YingNo ratings yet

- The Analysis of Evolution and Financing Policies of The Budget Deficit in Romania, in The Period 2007 - 2012Document10 pagesThe Analysis of Evolution and Financing Policies of The Budget Deficit in Romania, in The Period 2007 - 2012AndoNo ratings yet

- Understanding Material Deprivation - A Comparative European AnalysisDocument15 pagesUnderstanding Material Deprivation - A Comparative European AnalysisCatarina ReisNo ratings yet

- Infrastucture and EqauolityDocument14 pagesInfrastucture and Eqauolityitang siatanNo ratings yet

- Anderson 2018Document12 pagesAnderson 2018212011443No ratings yet

- Education, Income Distribution and InnovationDocument34 pagesEducation, Income Distribution and InnovationthanhrexNo ratings yet

- Access To Banking, Savings and Consumption Smoothing in Rural IndiaDocument13 pagesAccess To Banking, Savings and Consumption Smoothing in Rural IndiaRahmat Pasaribu OfficialNo ratings yet

- The Relationship Between Alternative Measures of Social Spending and Poverty RatesDocument16 pagesThe Relationship Between Alternative Measures of Social Spending and Poverty RatesSteev Vega GutierrezNo ratings yet

- (Ir) Rational Households' Saving Behavior? An Empirical InvestigationDocument9 pages(Ir) Rational Households' Saving Behavior? An Empirical InvestigationTrix CCNo ratings yet

- BE Finance GrowthDocument46 pagesBE Finance GrowthStelios KaragiannisNo ratings yet

- Advanced Economicsciencesprize2019Document43 pagesAdvanced Economicsciencesprize2019Avishek Ved DuttaNo ratings yet

- Household Financial Planning and Savings BehaviorDocument13 pagesHousehold Financial Planning and Savings Behavioradek wahyuNo ratings yet

- 2014 - Acar - The Dynamics of Multidimensional Poverty in TurkeyDocument27 pages2014 - Acar - The Dynamics of Multidimensional Poverty in TurkeyTuğçe KılıçNo ratings yet

- Working Paper Series: Household Debt Sustainability What Explains Household Non-Performing Loans? An Empirical AnalysisDocument45 pagesWorking Paper Series: Household Debt Sustainability What Explains Household Non-Performing Loans? An Empirical AnalysisStelios KaragiannisNo ratings yet

- Social Economy Literature ReviewDocument4 pagesSocial Economy Literature Reviewea7gpeqm100% (1)

- Vanrooij2011 4Document16 pagesVanrooij2011 4khueleee999No ratings yet

- 40 Years of Dutch Disease Literature Lessons For DDocument34 pages40 Years of Dutch Disease Literature Lessons For DchichidimoNo ratings yet

- The Borrowing Behaviour of Households: Evidence From The Cyprus Family Expenditure SurveysDocument27 pagesThe Borrowing Behaviour of Households: Evidence From The Cyprus Family Expenditure SurveysMada ẞunNo ratings yet

- Budget Rules and Resource Booms and Busts: A Dynamic Stochastic General Equilibrium AnalysisDocument26 pagesBudget Rules and Resource Booms and Busts: A Dynamic Stochastic General Equilibrium AnalysisShanta DevarajanNo ratings yet

- Journal of Contemporary EducationDocument12 pagesJournal of Contemporary EducationMik AeweNo ratings yet

- Financial Development and Income InequalityDocument47 pagesFinancial Development and Income InequalityPrranjali RaneNo ratings yet

- Debt and Distress - Evaluating The Psychological Cost of CreditDocument22 pagesDebt and Distress - Evaluating The Psychological Cost of CreditPusatStudyPerilakuEkonomiNo ratings yet

- Research in Economics: Arkadiusz Siero NDocument10 pagesResearch in Economics: Arkadiusz Siero NJózsef PataiNo ratings yet

- Thesis Euro CrisisDocument8 pagesThesis Euro Crisisjackieramirezpaterson100% (2)

- Dev't Economics Seminar Zemene Adane 1Document18 pagesDev't Economics Seminar Zemene Adane 1atalo adaneNo ratings yet

- Debt-Driven Growth? Wealth, Distribution and Demand in OECD CountriesDocument32 pagesDebt-Driven Growth? Wealth, Distribution and Demand in OECD CountriesIsmith PokhrelNo ratings yet

- Determinants of Household Savings in EU:What Policies For Increasing Savings?Document10 pagesDeterminants of Household Savings in EU:What Policies For Increasing Savings?aina sofiyaNo ratings yet

- Poverty Dissertation PDFDocument8 pagesPoverty Dissertation PDFBuyingCollegePapersOnlineCanada100% (1)

- Baker DebtConsumptionDocument46 pagesBaker DebtConsumptionMada ẞunNo ratings yet

- CriticalSociology Debt PDFDocument16 pagesCriticalSociology Debt PDFchechula12No ratings yet

- Arndt, Garcia, Tarp, Thurlow (2012) Poverty Reduction & Economic Structure - Comparative Path Analyis For Mozambique & VietnamDocument23 pagesArndt, Garcia, Tarp, Thurlow (2012) Poverty Reduction & Economic Structure - Comparative Path Analyis For Mozambique & VietnamNajaha GasimNo ratings yet

- Broberg 2014 Experimental WTP Public Good and IncomeCERE - WP2014-6Document18 pagesBroberg 2014 Experimental WTP Public Good and IncomeCERE - WP2014-6Adrian SerranoNo ratings yet

- 1 s2.0 S2212567115008230 MainDocument7 pages1 s2.0 S2212567115008230 Mainmlank211No ratings yet

- Research Paper On European Debt CrisisDocument8 pagesResearch Paper On European Debt Crisisjzczyfvkg100% (1)

- Financial LiteracyDocument27 pagesFinancial LiteracyyoseptianNo ratings yet

- Monetary and Multidimensional Child Poverty: A Contradiction in Terms?Document32 pagesMonetary and Multidimensional Child Poverty: A Contradiction in Terms?Lucía AndreozziNo ratings yet

- Financial Dollarization: The Role of Banks and Interest RatesDocument70 pagesFinancial Dollarization: The Role of Banks and Interest RatesNikola DragaševićNo ratings yet

- The Cultural Dimension of The CreditDocument12 pagesThe Cultural Dimension of The Creditdr m s s el namakiNo ratings yet

- KHARCHENKODocument64 pagesKHARCHENKOAditya Hikmat DestuprajaNo ratings yet

- Kel. 4Document35 pagesKel. 4yogoNo ratings yet

- Essays On DesignDocument5 pagesEssays On Designezmxjw15100% (2)

- Education and PovertyDocument9 pagesEducation and PovertyMuhammad TaufiqNo ratings yet

- Financial Inclusion and Development: Recent Impact EvidenceDocument12 pagesFinancial Inclusion and Development: Recent Impact EvidenceCGAP PublicationsNo ratings yet

- Financial Awareness in Everyday Life Due To The Pandemic, Based On The Results of A Hungarian Questionnaire SurveyDocument13 pagesFinancial Awareness in Everyday Life Due To The Pandemic, Based On The Results of A Hungarian Questionnaire SurveyGlobal Research and Development ServicesNo ratings yet

- Relationship Between The Financial and The Real Economy A Bibliometric AnalysisDocument21 pagesRelationship Between The Financial and The Real Economy A Bibliometric AnalysisDhriti DhingraNo ratings yet

- Central Banking For A Socio-Ecological TransformationDocument32 pagesCentral Banking For A Socio-Ecological TransformationLudovicoNo ratings yet

- From Extraction to Creation: Towards a Stakeholder EconomyFrom EverandFrom Extraction to Creation: Towards a Stakeholder EconomyNo ratings yet

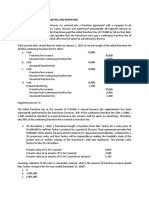

- Advanced Financial Accounting and ReportingDocument18 pagesAdvanced Financial Accounting and Reportingedrick LouiseNo ratings yet

- The Anti-Politics Machine: "Development" and Bureaucratic Power in LesothoDocument6 pagesThe Anti-Politics Machine: "Development" and Bureaucratic Power in Lesotholili gaoNo ratings yet

- Determination of Commercial Banking Liquidsystematic ReviewDocument3 pagesDetermination of Commercial Banking Liquidsystematic ReviewHempstone KimaniNo ratings yet

- 149 - Aerial Concepts 22 Nov 2023 RETAILDocument5 pages149 - Aerial Concepts 22 Nov 2023 RETAILMandy McInnesNo ratings yet

- Assignment Individual 1Document9 pagesAssignment Individual 1syeda salmaNo ratings yet

- Chapter 9 - Multifactor Models of Risk & ReturnDocument10 pagesChapter 9 - Multifactor Models of Risk & ReturnImejah FaviNo ratings yet

- Project Report On Punjab National Bank AakashDocument68 pagesProject Report On Punjab National Bank Aakashaakash_saxena8235356681% (16)

- Quote 3 Alibaba Manufacturer DirectoryDocument1 pageQuote 3 Alibaba Manufacturer Directorymuhamadrafie1975No ratings yet

- Chapter 25 - Evaluation of Portfolio PerformanceDocument16 pagesChapter 25 - Evaluation of Portfolio PerformanceJoseph LangitNo ratings yet

- Sal 16Document2 pagesSal 16Rafi AzamNo ratings yet

- Full Download Economics of Money Banking and Financial Markets Global 10th Edition Mishkin Solutions ManualDocument36 pagesFull Download Economics of Money Banking and Financial Markets Global 10th Edition Mishkin Solutions Manualmac2reyes100% (36)

- 49304752.xls / Sheet1 1Document3 pages49304752.xls / Sheet1 1LaSassyMeliNo ratings yet

- Chapter 8 MBA 65Document40 pagesChapter 8 MBA 65Al Rashedin KawserNo ratings yet

- Syllabus For 5 SemesterDocument7 pagesSyllabus For 5 SemesterhashikaNo ratings yet

- Higher Education in Vietnam: Industries & MarketsDocument28 pagesHigher Education in Vietnam: Industries & MarketsNguyễn ChiNo ratings yet

- CNR Istanbul 2019 BrochureDocument2 pagesCNR Istanbul 2019 Brochurenarender241No ratings yet

- IBS Lecture Week 4 Chapter 3Document33 pagesIBS Lecture Week 4 Chapter 3Tran LouisNo ratings yet

- 436 Roa - Pt. Gratia Lima DuaDocument2 pages436 Roa - Pt. Gratia Lima DuaDngall 88No ratings yet

- 04 Receivables - Additional DrillsDocument2 pages04 Receivables - Additional DrillsRazel MhinNo ratings yet

- The Unece Report On Achieving The Millennium Development Goals in Europe and Central Asia, 2012Document184 pagesThe Unece Report On Achieving The Millennium Development Goals in Europe and Central Asia, 2012UNDP Türkiye100% (1)

- Tut 3Document7 pagesTut 3Chi QuỳnhNo ratings yet

- Cost and Cost ClassificationDocument10 pagesCost and Cost ClassificationAmod YadavNo ratings yet

- Ambika: Tax Invoice OriginalDocument3 pagesAmbika: Tax Invoice OriginalDare DevilNo ratings yet

- First National Bank of Botswana Pricing Review: Revised Tariff Guide of Frequently Used ServicesDocument1 pageFirst National Bank of Botswana Pricing Review: Revised Tariff Guide of Frequently Used ServicesTek Sub U buS keTNo ratings yet

- Kunal Uniforms CNB TxnsDocument2 pagesKunal Uniforms CNB TxnsJanu JanuNo ratings yet

- Od429034304829954100 2Document2 pagesOd429034304829954100 2christinNo ratings yet

- Chapter 5 Regulations of Financial Market S and InstitutionsDocument7 pagesChapter 5 Regulations of Financial Market S and InstitutionsShimelis Tesema100% (1)

- Dr. Azlin Shafinaz Mohamad Arshad: Theories & Concept of EntrepreneurshipDocument24 pagesDr. Azlin Shafinaz Mohamad Arshad: Theories & Concept of EntrepreneurshipBukhari SuhaidinNo ratings yet