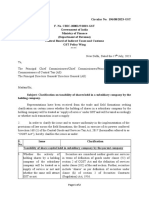

Circular No 13 2023 Service in Cinema

Circular No 13 2023 Service in Cinema

You might also like

- Sci Kcpe 2023 AnalysisDocument29 pagesSci Kcpe 2023 Analysisworldnet cyber100% (4)

- GST 50th Council Press ReleaseDocument8 pagesGST 50th Council Press ReleaseDharma Krishnan RajaNo ratings yet

- Clarifications Regarding Applicability GST Certain ServicesDocument5 pagesClarifications Regarding Applicability GST Certain ServicesMohammed IsmailNo ratings yet

- Circular - 109-03-2009-STDocument2 pagesCircular - 109-03-2009-STjayamurli19547922100% (2)

- GST Amendments: CS - Executive/Professional Ca - Inter/FinalDocument36 pagesGST Amendments: CS - Executive/Professional Ca - Inter/Finalbandaragamini525No ratings yet

- IDT AMENDMENTS AND STATUTORY UPDATES FOR MAY 2019 by Mahesh Gour PDFDocument69 pagesIDT AMENDMENTS AND STATUTORY UPDATES FOR MAY 2019 by Mahesh Gour PDFfarhana shaikNo ratings yet

- 37th GSTC MeetingDocument3 pages37th GSTC MeetingKalpeshh G BhavsarNo ratings yet

- Organised By:: National Conference On GSTDocument19 pagesOrganised By:: National Conference On GSTSunil ShahNo ratings yet

- CA Final Amendments For May 24 ExamsDocument38 pagesCA Final Amendments For May 24 ExamsMahalakshmi MahendranNo ratings yet

- OS Employees ExtensionDocument4 pagesOS Employees ExtensionpraweenNo ratings yet

- 2KU CBEC Policy Wing Clarifications Dated 26-07-2017 On Export Related Issues On LUT Bond Bank Gurantee EOUs SEZsDocument4 pages2KU CBEC Policy Wing Clarifications Dated 26-07-2017 On Export Related Issues On LUT Bond Bank Gurantee EOUs SEZsSantosh JaiswalNo ratings yet

- Ca Inter Amendments For May 24 Exams 2Document25 pagesCa Inter Amendments For May 24 Exams 2RajaramNo ratings yet

- Press Release 52 GST CouncilDocument6 pagesPress Release 52 GST CouncilCA Thirumalesu ENo ratings yet

- GST Amendment SheetDocument31 pagesGST Amendment Sheet10poolcardNo ratings yet

- Writeup Circular 86-05-2019Document3 pagesWriteup Circular 86-05-2019Mithun KhatryNo ratings yet

- Circulars 1623948051Document14 pagesCirculars 1623948051C DavidNo ratings yet

- Press Information Bureau Government of India Ministry of FinanceDocument3 pagesPress Information Bureau Government of India Ministry of Financekumar45caNo ratings yet

- 02 Final - Borivali SC of WIRC - Issues in Hospitality Industry - 020624Document113 pages02 Final - Borivali SC of WIRC - Issues in Hospitality Industry - 020624Crystal CrystalNo ratings yet

- IDT ICAI AmendmentsDocument38 pagesIDT ICAI Amendmentsgvramani51233No ratings yet

- CGST CircularsDocument431 pagesCGST CircularsRohan KulkarniNo ratings yet

- GST Update126 PDFDocument4 pagesGST Update126 PDFTharun RajNo ratings yet

- Paper 8: Indirect Tax Laws Statutory Update For May 2022 ExaminationDocument25 pagesPaper 8: Indirect Tax Laws Statutory Update For May 2022 Examinationparam.ginniNo ratings yet

- Circular CGST 119Document3 pagesCircular CGST 119CA Keshav MadaanNo ratings yet

- Circular No. 151/07/2021-GST: RD THDocument3 pagesCircular No. 151/07/2021-GST: RD THShivansh MishraNo ratings yet

- Signed Minutes - 35th GST Council MeetingDocument76 pagesSigned Minutes - 35th GST Council Meetingvinod.sale1No ratings yet

- JS Outsourcing GODocument4 pagesJS Outsourcing GOpraweenNo ratings yet

- Circularno 44 CGSTDocument2 pagesCircularno 44 CGSTconnectsujata1No ratings yet

- G S T MaterialDocument20 pagesG S T MaterialGonella NagamallikaNo ratings yet

- Goods and Services Tax Council Standing Committee On Capacity Building and FacilitationDocument61 pagesGoods and Services Tax Council Standing Committee On Capacity Building and FacilitationJeyakar PrabakarNo ratings yet

- Circular CGST 130 NewDocument2 pagesCircular CGST 130 NewSivasankariNo ratings yet

- Trade Notice No 09-CGST & CX-MUMBAI Zone-2021 Dated 22september2021Document6 pagesTrade Notice No 09-CGST & CX-MUMBAI Zone-2021 Dated 22september2021Gautam jainNo ratings yet

- Ca Suraj Satija Ssguru GST Amendment: Introduction To GST Charge of GSTDocument7 pagesCa Suraj Satija Ssguru GST Amendment: Introduction To GST Charge of GSTkinnar2013No ratings yet

- Reverse Charge MechanismDocument19 pagesReverse Charge MechanismSayyadNo ratings yet

- Circular CGST 196Document2 pagesCircular CGST 196Jaipur-B Gr-2No ratings yet

- Indirect Tax Newsletter - July 2023Document15 pagesIndirect Tax Newsletter - July 2023ELP LawNo ratings yet

- GST ProjectDocument13 pagesGST ProjectBS SAILAJANo ratings yet

- Tamil Nadu Government Gazette: Part III-Section 1 (A)Document18 pagesTamil Nadu Government Gazette: Part III-Section 1 (A)SathishNo ratings yet

- Circular No. 159 - 14 - 2021 - GSTDocument5 pagesCircular No. 159 - 14 - 2021 - GSTCA Hiloni GalaNo ratings yet

- CA. Mithun Khatry 9810100520Document3 pagesCA. Mithun Khatry 9810100520Mithun KhatryNo ratings yet

- F. No. 354/263/2017-TRU Government of India Ministry of Finance Department of Revenue Tax Research Unit North Block, New Delhi 20 November 2017Document2 pagesF. No. 354/263/2017-TRU Government of India Ministry of Finance Department of Revenue Tax Research Unit North Block, New Delhi 20 November 2017Sahil KumarNo ratings yet

- Amendment Recruitment Rules 24082023Document3 pagesAmendment Recruitment Rules 24082023Dilip BannerjiNo ratings yet

- Customs Circular-No-18-2023Document1 pageCustoms Circular-No-18-2023Raja SinghNo ratings yet

- GST Amendments For Circulation - Nov 2018 UploadedDocument20 pagesGST Amendments For Circulation - Nov 2018 UploadedJay SuchakNo ratings yet

- CA Inter IPCC IDT Amendments May2020 ExamDocument25 pagesCA Inter IPCC IDT Amendments May2020 ExamMohammed IbrahimNo ratings yet

- Whether This Notice Can Be Considered As Legally Valid?Document9 pagesWhether This Notice Can Be Considered As Legally Valid?Sambasivam GanesanNo ratings yet

- Circular CGST 120Document2 pagesCircular CGST 120CA Keshav MadaanNo ratings yet

- Budget 23 Tax Proposals S&NDocument10 pagesBudget 23 Tax Proposals S&NPankaj Dharamshi & CoNo ratings yet

- Amendment Recruitment Rules 11092023Document3 pagesAmendment Recruitment Rules 110920238793160048ajayNo ratings yet

- Blocked Credits Under GST Section 17 (5) of CGST ACT, 2017Document8 pagesBlocked Credits Under GST Section 17 (5) of CGST ACT, 2017ajayNo ratings yet

- Press Release 53rd MeetingDocument10 pagesPress Release 53rd Meetingsuresh kumarNo ratings yet

- Circularno 34 CGSTDocument3 pagesCircularno 34 CGSTjainrushab55No ratings yet

- CB LICENCE IS LIFE TIME Circular-No-17-2021-rDocument2 pagesCB LICENCE IS LIFE TIME Circular-No-17-2021-rganeshNo ratings yet

- Paper 4B: Indirect Taxes Statutory Update For November 2020 ExaminationDocument28 pagesPaper 4B: Indirect Taxes Statutory Update For November 2020 ExaminationShafira AryandiniNo ratings yet

- Special Economic Zone (SEZ) Under GST - Taxguru - inDocument3 pagesSpecial Economic Zone (SEZ) Under GST - Taxguru - inAKSHITA SRIVASTAVANo ratings yet

- Circular For Discount (Commercial Credit Note)Document3 pagesCircular For Discount (Commercial Credit Note)rajanbardiaNo ratings yet

- Circular 36 2018 CustomsDocument2 pagesCircular 36 2018 CustomsIAS MeenaNo ratings yet

- PIB2027982Document9 pagesPIB2027982suresh kumarNo ratings yet

- Circular 23 2017Document2 pagesCircular 23 2017Singh SranNo ratings yet

- 9 (3&4) of CGSTDocument4 pages9 (3&4) of CGSTsumit jhaNo ratings yet

- Circular CGST 117Document2 pagesCircular CGST 117SAKSHI INSTITUTE OF MARITIME FOUNDATIONNo ratings yet

- Marketing Project: by Adithya Suresh Class: Xii B2 FOR THE YEAR 2021-22Document48 pagesMarketing Project: by Adithya Suresh Class: Xii B2 FOR THE YEAR 2021-22Adi100% (1)

- Pasta ShapesDocument5 pagesPasta Shapesj66711845No ratings yet

- How To Eat A Fig - 14 Steps (With Pictures) - WikihowDocument1 pageHow To Eat A Fig - 14 Steps (With Pictures) - WikihowNouka VENo ratings yet

- Exposition Text Exercise ZenowskyDocument8 pagesExposition Text Exercise ZenowskyZenowsky Wira Efrata SianturiNo ratings yet

- Review: Different Activities of Moringa Oleifera TreeDocument4 pagesReview: Different Activities of Moringa Oleifera TreeInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Prueba de Acceso A La UniversidadDocument3 pagesPrueba de Acceso A La UniversidadnoemiNo ratings yet

- Macronutrients ProteinsDocument2 pagesMacronutrients ProteinsEllice O. MonizNo ratings yet

- Mark HymanDocument14 pagesMark HymanMax meNo ratings yet

- 1 s2.0 S0926669023017028 MainDocument7 pages1 s2.0 S0926669023017028 MainTHƯ ĐÀO TUẤNNo ratings yet

- The Story of Goldilocks and The Three Bears: by Robert Southey Report By: JM SabatinDocument14 pagesThe Story of Goldilocks and The Three Bears: by Robert Southey Report By: JM SabatinJM SabatinNo ratings yet

- Effect of Apple Pomace Powder On The Quality Attributes of Fish FingersDocument10 pagesEffect of Apple Pomace Powder On The Quality Attributes of Fish FingersOliver EvrotNo ratings yet

- Vestige E-Catalogue May 2021Document143 pagesVestige E-Catalogue May 2021Rameez FaroukNo ratings yet

- Pulp Fiction by Quentin Tarantino & Roger AvaryDocument126 pagesPulp Fiction by Quentin Tarantino & Roger AvaryVan Engelen PantoNo ratings yet

- Lime and Pistachio Tartelette by Miquel Guarro: Related RecipesDocument1 pageLime and Pistachio Tartelette by Miquel Guarro: Related RecipesAhmedsabri SabriNo ratings yet

- Chapter 2 - Ecosystem NewDocument38 pagesChapter 2 - Ecosystem NewZubair HUssainNo ratings yet

- SPM 2021 - English Writing 5TGDocument35 pagesSPM 2021 - English Writing 5TGmunaizim-1No ratings yet

- 2035 6820 1 PBDocument8 pages2035 6820 1 PBAgral SilabanNo ratings yet

- Efa 2014 SP IdaDocument57 pagesEfa 2014 SP IdaMauriceStapelton78No ratings yet

- CBLM HSKPNG Common FinalDocument31 pagesCBLM HSKPNG Common FinalWela Jane Patrimonio RarugalNo ratings yet

- FILE - 20210127 - 142514 - BULLE Catalog2019Document31 pagesFILE - 20210127 - 142514 - BULLE Catalog2019Thanh NgocNo ratings yet

- Catalog: Polish Confectionery Plotters ManufacturerDocument16 pagesCatalog: Polish Confectionery Plotters ManufacturerDav GarcíaNo ratings yet

- Practice For Final ExamDocument4 pagesPractice For Final ExamAlicia ANo ratings yet

- Probability JeopardyDocument53 pagesProbability JeopardyReygie FabrigaNo ratings yet

- Ordering Food at A RestaurantDocument2 pagesOrdering Food at A RestaurantAna MariaNo ratings yet

- Wisma Tani, Podium Block, Lot 4G1, Precinct 4 Federal Government Administration CentreDocument13 pagesWisma Tani, Podium Block, Lot 4G1, Precinct 4 Federal Government Administration CentreTun Izlinda Tun BahardinNo ratings yet

- Aravinna 2016Document12 pagesAravinna 2016natss mateoNo ratings yet

- DHBB - Practice Test 6Document14 pagesDHBB - Practice Test 6Vi Tạ HữuNo ratings yet

- 2. 씨드Document2 pages2. 씨드님누구세요No ratings yet

- Single Malt WhiskyDocument15 pagesSingle Malt WhiskyHiok Kui LeeNo ratings yet

Download as pdf or txt

You might also like

- Sci Kcpe 2023 AnalysisDocument29 pagesSci Kcpe 2023 Analysisworldnet cyber100% (4)

- GST 50th Council Press ReleaseDocument8 pagesGST 50th Council Press ReleaseDharma Krishnan RajaNo ratings yet

- Clarifications Regarding Applicability GST Certain ServicesDocument5 pagesClarifications Regarding Applicability GST Certain ServicesMohammed IsmailNo ratings yet

- Circular - 109-03-2009-STDocument2 pagesCircular - 109-03-2009-STjayamurli19547922100% (2)

- GST Amendments: CS - Executive/Professional Ca - Inter/FinalDocument36 pagesGST Amendments: CS - Executive/Professional Ca - Inter/Finalbandaragamini525No ratings yet

- IDT AMENDMENTS AND STATUTORY UPDATES FOR MAY 2019 by Mahesh Gour PDFDocument69 pagesIDT AMENDMENTS AND STATUTORY UPDATES FOR MAY 2019 by Mahesh Gour PDFfarhana shaikNo ratings yet

- 37th GSTC MeetingDocument3 pages37th GSTC MeetingKalpeshh G BhavsarNo ratings yet

- Organised By:: National Conference On GSTDocument19 pagesOrganised By:: National Conference On GSTSunil ShahNo ratings yet

- CA Final Amendments For May 24 ExamsDocument38 pagesCA Final Amendments For May 24 ExamsMahalakshmi MahendranNo ratings yet

- OS Employees ExtensionDocument4 pagesOS Employees ExtensionpraweenNo ratings yet

- 2KU CBEC Policy Wing Clarifications Dated 26-07-2017 On Export Related Issues On LUT Bond Bank Gurantee EOUs SEZsDocument4 pages2KU CBEC Policy Wing Clarifications Dated 26-07-2017 On Export Related Issues On LUT Bond Bank Gurantee EOUs SEZsSantosh JaiswalNo ratings yet

- Ca Inter Amendments For May 24 Exams 2Document25 pagesCa Inter Amendments For May 24 Exams 2RajaramNo ratings yet

- Press Release 52 GST CouncilDocument6 pagesPress Release 52 GST CouncilCA Thirumalesu ENo ratings yet

- GST Amendment SheetDocument31 pagesGST Amendment Sheet10poolcardNo ratings yet

- Writeup Circular 86-05-2019Document3 pagesWriteup Circular 86-05-2019Mithun KhatryNo ratings yet

- Circulars 1623948051Document14 pagesCirculars 1623948051C DavidNo ratings yet

- Press Information Bureau Government of India Ministry of FinanceDocument3 pagesPress Information Bureau Government of India Ministry of Financekumar45caNo ratings yet

- 02 Final - Borivali SC of WIRC - Issues in Hospitality Industry - 020624Document113 pages02 Final - Borivali SC of WIRC - Issues in Hospitality Industry - 020624Crystal CrystalNo ratings yet

- IDT ICAI AmendmentsDocument38 pagesIDT ICAI Amendmentsgvramani51233No ratings yet

- CGST CircularsDocument431 pagesCGST CircularsRohan KulkarniNo ratings yet

- GST Update126 PDFDocument4 pagesGST Update126 PDFTharun RajNo ratings yet

- Paper 8: Indirect Tax Laws Statutory Update For May 2022 ExaminationDocument25 pagesPaper 8: Indirect Tax Laws Statutory Update For May 2022 Examinationparam.ginniNo ratings yet

- Circular CGST 119Document3 pagesCircular CGST 119CA Keshav MadaanNo ratings yet

- Circular No. 151/07/2021-GST: RD THDocument3 pagesCircular No. 151/07/2021-GST: RD THShivansh MishraNo ratings yet

- Signed Minutes - 35th GST Council MeetingDocument76 pagesSigned Minutes - 35th GST Council Meetingvinod.sale1No ratings yet

- JS Outsourcing GODocument4 pagesJS Outsourcing GOpraweenNo ratings yet

- Circularno 44 CGSTDocument2 pagesCircularno 44 CGSTconnectsujata1No ratings yet

- G S T MaterialDocument20 pagesG S T MaterialGonella NagamallikaNo ratings yet

- Goods and Services Tax Council Standing Committee On Capacity Building and FacilitationDocument61 pagesGoods and Services Tax Council Standing Committee On Capacity Building and FacilitationJeyakar PrabakarNo ratings yet

- Circular CGST 130 NewDocument2 pagesCircular CGST 130 NewSivasankariNo ratings yet

- Trade Notice No 09-CGST & CX-MUMBAI Zone-2021 Dated 22september2021Document6 pagesTrade Notice No 09-CGST & CX-MUMBAI Zone-2021 Dated 22september2021Gautam jainNo ratings yet

- Ca Suraj Satija Ssguru GST Amendment: Introduction To GST Charge of GSTDocument7 pagesCa Suraj Satija Ssguru GST Amendment: Introduction To GST Charge of GSTkinnar2013No ratings yet

- Reverse Charge MechanismDocument19 pagesReverse Charge MechanismSayyadNo ratings yet

- Circular CGST 196Document2 pagesCircular CGST 196Jaipur-B Gr-2No ratings yet

- Indirect Tax Newsletter - July 2023Document15 pagesIndirect Tax Newsletter - July 2023ELP LawNo ratings yet

- GST ProjectDocument13 pagesGST ProjectBS SAILAJANo ratings yet

- Tamil Nadu Government Gazette: Part III-Section 1 (A)Document18 pagesTamil Nadu Government Gazette: Part III-Section 1 (A)SathishNo ratings yet

- Circular No. 159 - 14 - 2021 - GSTDocument5 pagesCircular No. 159 - 14 - 2021 - GSTCA Hiloni GalaNo ratings yet

- CA. Mithun Khatry 9810100520Document3 pagesCA. Mithun Khatry 9810100520Mithun KhatryNo ratings yet

- F. No. 354/263/2017-TRU Government of India Ministry of Finance Department of Revenue Tax Research Unit North Block, New Delhi 20 November 2017Document2 pagesF. No. 354/263/2017-TRU Government of India Ministry of Finance Department of Revenue Tax Research Unit North Block, New Delhi 20 November 2017Sahil KumarNo ratings yet

- Amendment Recruitment Rules 24082023Document3 pagesAmendment Recruitment Rules 24082023Dilip BannerjiNo ratings yet

- Customs Circular-No-18-2023Document1 pageCustoms Circular-No-18-2023Raja SinghNo ratings yet

- GST Amendments For Circulation - Nov 2018 UploadedDocument20 pagesGST Amendments For Circulation - Nov 2018 UploadedJay SuchakNo ratings yet

- CA Inter IPCC IDT Amendments May2020 ExamDocument25 pagesCA Inter IPCC IDT Amendments May2020 ExamMohammed IbrahimNo ratings yet

- Whether This Notice Can Be Considered As Legally Valid?Document9 pagesWhether This Notice Can Be Considered As Legally Valid?Sambasivam GanesanNo ratings yet

- Circular CGST 120Document2 pagesCircular CGST 120CA Keshav MadaanNo ratings yet

- Budget 23 Tax Proposals S&NDocument10 pagesBudget 23 Tax Proposals S&NPankaj Dharamshi & CoNo ratings yet

- Amendment Recruitment Rules 11092023Document3 pagesAmendment Recruitment Rules 110920238793160048ajayNo ratings yet

- Blocked Credits Under GST Section 17 (5) of CGST ACT, 2017Document8 pagesBlocked Credits Under GST Section 17 (5) of CGST ACT, 2017ajayNo ratings yet

- Press Release 53rd MeetingDocument10 pagesPress Release 53rd Meetingsuresh kumarNo ratings yet

- Circularno 34 CGSTDocument3 pagesCircularno 34 CGSTjainrushab55No ratings yet

- CB LICENCE IS LIFE TIME Circular-No-17-2021-rDocument2 pagesCB LICENCE IS LIFE TIME Circular-No-17-2021-rganeshNo ratings yet

- Paper 4B: Indirect Taxes Statutory Update For November 2020 ExaminationDocument28 pagesPaper 4B: Indirect Taxes Statutory Update For November 2020 ExaminationShafira AryandiniNo ratings yet

- Special Economic Zone (SEZ) Under GST - Taxguru - inDocument3 pagesSpecial Economic Zone (SEZ) Under GST - Taxguru - inAKSHITA SRIVASTAVANo ratings yet

- Circular For Discount (Commercial Credit Note)Document3 pagesCircular For Discount (Commercial Credit Note)rajanbardiaNo ratings yet

- Circular 36 2018 CustomsDocument2 pagesCircular 36 2018 CustomsIAS MeenaNo ratings yet

- PIB2027982Document9 pagesPIB2027982suresh kumarNo ratings yet

- Circular 23 2017Document2 pagesCircular 23 2017Singh SranNo ratings yet

- 9 (3&4) of CGSTDocument4 pages9 (3&4) of CGSTsumit jhaNo ratings yet

- Circular CGST 117Document2 pagesCircular CGST 117SAKSHI INSTITUTE OF MARITIME FOUNDATIONNo ratings yet

- Marketing Project: by Adithya Suresh Class: Xii B2 FOR THE YEAR 2021-22Document48 pagesMarketing Project: by Adithya Suresh Class: Xii B2 FOR THE YEAR 2021-22Adi100% (1)

- Pasta ShapesDocument5 pagesPasta Shapesj66711845No ratings yet

- How To Eat A Fig - 14 Steps (With Pictures) - WikihowDocument1 pageHow To Eat A Fig - 14 Steps (With Pictures) - WikihowNouka VENo ratings yet

- Exposition Text Exercise ZenowskyDocument8 pagesExposition Text Exercise ZenowskyZenowsky Wira Efrata SianturiNo ratings yet

- Review: Different Activities of Moringa Oleifera TreeDocument4 pagesReview: Different Activities of Moringa Oleifera TreeInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Prueba de Acceso A La UniversidadDocument3 pagesPrueba de Acceso A La UniversidadnoemiNo ratings yet

- Macronutrients ProteinsDocument2 pagesMacronutrients ProteinsEllice O. MonizNo ratings yet

- Mark HymanDocument14 pagesMark HymanMax meNo ratings yet

- 1 s2.0 S0926669023017028 MainDocument7 pages1 s2.0 S0926669023017028 MainTHƯ ĐÀO TUẤNNo ratings yet

- The Story of Goldilocks and The Three Bears: by Robert Southey Report By: JM SabatinDocument14 pagesThe Story of Goldilocks and The Three Bears: by Robert Southey Report By: JM SabatinJM SabatinNo ratings yet

- Effect of Apple Pomace Powder On The Quality Attributes of Fish FingersDocument10 pagesEffect of Apple Pomace Powder On The Quality Attributes of Fish FingersOliver EvrotNo ratings yet

- Vestige E-Catalogue May 2021Document143 pagesVestige E-Catalogue May 2021Rameez FaroukNo ratings yet

- Pulp Fiction by Quentin Tarantino & Roger AvaryDocument126 pagesPulp Fiction by Quentin Tarantino & Roger AvaryVan Engelen PantoNo ratings yet

- Lime and Pistachio Tartelette by Miquel Guarro: Related RecipesDocument1 pageLime and Pistachio Tartelette by Miquel Guarro: Related RecipesAhmedsabri SabriNo ratings yet

- Chapter 2 - Ecosystem NewDocument38 pagesChapter 2 - Ecosystem NewZubair HUssainNo ratings yet

- SPM 2021 - English Writing 5TGDocument35 pagesSPM 2021 - English Writing 5TGmunaizim-1No ratings yet

- 2035 6820 1 PBDocument8 pages2035 6820 1 PBAgral SilabanNo ratings yet

- Efa 2014 SP IdaDocument57 pagesEfa 2014 SP IdaMauriceStapelton78No ratings yet

- CBLM HSKPNG Common FinalDocument31 pagesCBLM HSKPNG Common FinalWela Jane Patrimonio RarugalNo ratings yet

- FILE - 20210127 - 142514 - BULLE Catalog2019Document31 pagesFILE - 20210127 - 142514 - BULLE Catalog2019Thanh NgocNo ratings yet

- Catalog: Polish Confectionery Plotters ManufacturerDocument16 pagesCatalog: Polish Confectionery Plotters ManufacturerDav GarcíaNo ratings yet

- Practice For Final ExamDocument4 pagesPractice For Final ExamAlicia ANo ratings yet

- Probability JeopardyDocument53 pagesProbability JeopardyReygie FabrigaNo ratings yet

- Ordering Food at A RestaurantDocument2 pagesOrdering Food at A RestaurantAna MariaNo ratings yet

- Wisma Tani, Podium Block, Lot 4G1, Precinct 4 Federal Government Administration CentreDocument13 pagesWisma Tani, Podium Block, Lot 4G1, Precinct 4 Federal Government Administration CentreTun Izlinda Tun BahardinNo ratings yet

- Aravinna 2016Document12 pagesAravinna 2016natss mateoNo ratings yet

- DHBB - Practice Test 6Document14 pagesDHBB - Practice Test 6Vi Tạ HữuNo ratings yet

- 2. 씨드Document2 pages2. 씨드님누구세요No ratings yet

- Single Malt WhiskyDocument15 pagesSingle Malt WhiskyHiok Kui LeeNo ratings yet