Download as docx, pdf, or txt

You might also like

- Learners'+Sheet Final Dec+CohortDocument23 pagesLearners'+Sheet Final Dec+Cohortpre.meh21No ratings yet

- Exercise 1: On December 31, Bryniuk's Company, The Accounting Records Showed The Following InformationDocument10 pagesExercise 1: On December 31, Bryniuk's Company, The Accounting Records Showed The Following InformationJohn Kenneth Bohol50% (2)

- Hul Ratio AnalysisDocument14 pagesHul Ratio Analysisvviek100% (1)

- Cash Basis Accrual Basis Exercises With AnswersDocument6 pagesCash Basis Accrual Basis Exercises With AnswersRNo ratings yet

- 02 - Business Combination Date of AcquisitionDocument5 pages02 - Business Combination Date of AcquisitionMelody Gumba100% (1)

- Fma (Repaired)Document12 pagesFma (Repaired)pappunaagraajNo ratings yet

- Financial Analysis of Tata Motors: Submitted by Binni.M Semester-2 Mba-Ib ROLL - No-6Document19 pagesFinancial Analysis of Tata Motors: Submitted by Binni.M Semester-2 Mba-Ib ROLL - No-6binnivenus100% (1)

- Accounts Project Rough DraftDocument10 pagesAccounts Project Rough DraftNakul TalwarNo ratings yet

- Working Capital: Apl Apollo Tubes LTDDocument17 pagesWorking Capital: Apl Apollo Tubes LTDDhirajsharma123No ratings yet

- Ratio Analysis SampleDocument16 pagesRatio Analysis SampleRitoshree paulNo ratings yet

- Corporate Finance (CF) Notes: What Is Accounting?Document11 pagesCorporate Finance (CF) Notes: What Is Accounting?Saumyadeep BardhanNo ratings yet

- Accounting 504 - Chapter 02 AnswersDocument19 pagesAccounting 504 - Chapter 02 AnswerspicassaaNo ratings yet

- Chapter-10 Accounting RatiosDocument18 pagesChapter-10 Accounting RatiosAlton D'silvaNo ratings yet

- Analysis of Financial StatementsDocument6 pagesAnalysis of Financial StatementsMandeep SharmaNo ratings yet

- Financial Ratio Analyses and Their Implications To ManagementDocument31 pagesFinancial Ratio Analyses and Their Implications To ManagementKeisha Kaye SaleraNo ratings yet

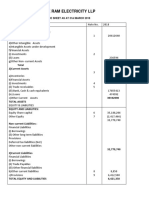

- Shree Ram Electricity LLP: 1) Non-Current AssetsDocument5 pagesShree Ram Electricity LLP: 1) Non-Current AssetsSaba MullaNo ratings yet

- Analysis of Financial Statement of Tata MotorsDocument16 pagesAnalysis of Financial Statement of Tata MotorsErya modiNo ratings yet

- Ees Cable Audit 2021 v1.0Document8 pagesEes Cable Audit 2021 v1.0Yakdhan YaseenNo ratings yet

- Unit 6 O Business Firm: Financial A YsisDocument18 pagesUnit 6 O Business Firm: Financial A YsisPooja PandeyNo ratings yet

- Wealth Managment 1Document73 pagesWealth Managment 1dashashutosh87No ratings yet

- Answers To Problem Sets: Financial AnalysisDocument11 pagesAnswers To Problem Sets: Financial AnalysisshikhaNo ratings yet

- Answers To Problem Sets: Financial AnalysisDocument11 pagesAnswers To Problem Sets: Financial AnalysisRamneek SinghNo ratings yet

- Fa 5Document14 pagesFa 5divyayella024No ratings yet

- Britannia Industries LTDDocument12 pagesBritannia Industries LTDStephen RajNo ratings yet

- Model Answers Subject - Working Capital Management Paper code-AS-2377Document8 pagesModel Answers Subject - Working Capital Management Paper code-AS-2377avni shrmaNo ratings yet

- Ias 7 Cash FlowDocument15 pagesIas 7 Cash FlowManda simzNo ratings yet

- Financial Accounting & AnalysisDocument6 pagesFinancial Accounting & AnalysisAmandeep SinghNo ratings yet

- Reliance Industries LTD.: Balance SheetDocument10 pagesReliance Industries LTD.: Balance SheetAayush PeriwalNo ratings yet

- Exercises: Method. Under This Form Expenses Are Aggregated According To Their Nature and NotDocument15 pagesExercises: Method. Under This Form Expenses Are Aggregated According To Their Nature and NotCherry Doong CuantiosoNo ratings yet

- MB20202 Corporate Finance Unit V Study MaterialsDocument33 pagesMB20202 Corporate Finance Unit V Study MaterialsSarath kumar CNo ratings yet

- Working Capital Management Related Report UtsavDocument8 pagesWorking Capital Management Related Report UtsavPradip MehtaNo ratings yet

- Financial Statement Analysis IDocument16 pagesFinancial Statement Analysis IA K MusicNo ratings yet

- Discussion Question #5 Solution-Table 1.0 Shows The Order of Current Assets in Terms of Liquidity (Most To Least) Current AssetsDocument7 pagesDiscussion Question #5 Solution-Table 1.0 Shows The Order of Current Assets in Terms of Liquidity (Most To Least) Current AssetsRijul DUbeyNo ratings yet

- Finals Exam - Valuation and ConceptsDocument7 pagesFinals Exam - Valuation and ConceptsSummer KorapatNo ratings yet

- ACCT 221 Chapter 2Document29 pagesACCT 221 Chapter 2Shane Hundley100% (1)

- CH 1 - End of Chapter Exercises SolutionsDocument37 pagesCH 1 - End of Chapter Exercises SolutionssaraNo ratings yet

- Aarthi S - FRA Final ProjectDocument15 pagesAarthi S - FRA Final ProjectaarthiNo ratings yet

- Afya 2021Document80 pagesAfya 2021Ayushika SinghNo ratings yet

- Review On Financial Standing of Saiddi AgriDocument3 pagesReview On Financial Standing of Saiddi AgriBilling ZamboecozoneNo ratings yet

- Basic Accounts Ca1Document5 pagesBasic Accounts Ca1shivanigas morwaNo ratings yet

- Solutions Ch2Document70 pagesSolutions Ch2annalisa.bissoliNo ratings yet

- Accounting Ratios For ProjectDocument13 pagesAccounting Ratios For ProjectRoyal ProjectsNo ratings yet

- Answers To Problem Sets Financial AnalysisDocument11 pagesAnswers To Problem Sets Financial AnalysisAerwyna AfarinNo ratings yet

- Answers To Problem Sets: Financial AnalysisDocument11 pagesAnswers To Problem Sets: Financial AnalysisLakshya KumarNo ratings yet

- Chapter 18Document11 pagesChapter 18Ngân HàNo ratings yet

- Answers To Problem Sets: Financial AnalysisDocument11 pagesAnswers To Problem Sets: Financial AnalysisSnehanshu SumanNo ratings yet

- Answers To Problem Sets: Financial AnalysisDocument11 pagesAnswers To Problem Sets: Financial AnalysisNgân HàNo ratings yet

- Answers To Problem Sets: Financial AnalysisDocument11 pagesAnswers To Problem Sets: Financial AnalysisIñigo López-ArandaNo ratings yet

- Company Profile: Liberty Plywood Pvt. Ltd. Is A Quality Driven Organization Offering A Wide Range of PreDocument50 pagesCompany Profile: Liberty Plywood Pvt. Ltd. Is A Quality Driven Organization Offering A Wide Range of PreparveenbilangNo ratings yet

- Accounting - UCO Bank - Assignment1Document1 pageAccounting - UCO Bank - Assignment1KummNo ratings yet

- Classification, Analysis & Interpretation of RatiosDocument26 pagesClassification, Analysis & Interpretation of RatiosPayal MahajanNo ratings yet

- Financial Statements & Analysis 2024 SPCCDocument29 pagesFinancial Statements & Analysis 2024 SPCCSaturo GojoNo ratings yet

- Financial Statement Analysis (Fsa)Document32 pagesFinancial Statement Analysis (Fsa)Shashank100% (1)

- Dharthi DredgingDocument6 pagesDharthi DredgingshankarswaminathanNo ratings yet

- Ratio AnalysisDocument16 pagesRatio Analysisabhishekanandsingh123goNo ratings yet

- Financial Accounting 7th Edition Libby Solutions ManualDocument48 pagesFinancial Accounting 7th Edition Libby Solutions ManualBrandonCoopergnzxy100% (14)

- Lecture 3 and 4 - Financial Statement Analysis of BanksDocument64 pagesLecture 3 and 4 - Financial Statement Analysis of BanksPratyush GoelNo ratings yet

- Chapter Three Firm'S Financial Operation: Prepared By: Nahom B. 1Document35 pagesChapter Three Firm'S Financial Operation: Prepared By: Nahom B. 1SemNo ratings yet

- PRESENTATION KKDocument26 pagesPRESENTATION KKKaram KaurNo ratings yet

- Document of FMA ProjectsDocument21 pagesDocument of FMA ProjectspappunaagraajNo ratings yet

- Camp DocumentsDocument4 pagesCamp DocumentspappunaagraajNo ratings yet

- A Project Report ON An Interpretation On Hathigumpha Inscription As Testament of Human HistoryDocument11 pagesA Project Report ON An Interpretation On Hathigumpha Inscription As Testament of Human HistorypappunaagraajNo ratings yet

- DeclarationDocument2 pagesDeclarationpappunaagraajNo ratings yet

- Bhargabee Dash PR 1Document11 pagesBhargabee Dash PR 1pappunaagraajNo ratings yet

- Project of AccountancyDocument6 pagesProject of AccountancypappunaagraajNo ratings yet

- Zoology AscriseDocument12 pagesZoology AscrisepappunaagraajNo ratings yet

- ACCOUNTSDocument18 pagesACCOUNTSpappunaagraajNo ratings yet

- British Poetry: Milton, Dryden, PopeDocument34 pagesBritish Poetry: Milton, Dryden, PopepappunaagraajNo ratings yet

- 1st Maa Samaleswari Cricket CLUB 1Document1 page1st Maa Samaleswari Cricket CLUB 1pappunaagraajNo ratings yet

- Unit Test FR PDocument1 pageUnit Test FR PpappunaagraajNo ratings yet

- Education in Japan Front PageDocument1 pageEducation in Japan Front PagepappunaagraajNo ratings yet

- Education 3rd Sem Front PageDocument1 pageEducation 3rd Sem Front PagepappunaagraajNo ratings yet

- A Project Report ON Flow of Odia Folklore in 21 CenturyDocument10 pagesA Project Report ON Flow of Odia Folklore in 21 CenturypappunaagraajNo ratings yet

- Wuthering Heights: K 68 First Floor West Patel Nagar New Delhi 08Document7 pagesWuthering Heights: K 68 First Floor West Patel Nagar New Delhi 08pappunaagraajNo ratings yet

- Education FPDocument1 pageEducation FPpappunaagraajNo ratings yet

- Nirmal Chhuria Front Page 2.12.2Document1 pageNirmal Chhuria Front Page 2.12.2pappunaagraajNo ratings yet

- Special Education 6 PrintDocument8 pagesSpecial Education 6 PrintpappunaagraajNo ratings yet

- The Prime of Miss Jean Brodie Is A Short Novel Written by MurielDocument6 pagesThe Prime of Miss Jean Brodie Is A Short Novel Written by MurielpappunaagraajNo ratings yet

- AC1025 2011-Principles of Accounting Main EQP and Commentaries AC1025 2011-Principles of Accounting Main EQP and CommentariesDocument68 pagesAC1025 2011-Principles of Accounting Main EQP and Commentaries AC1025 2011-Principles of Accounting Main EQP and Commentaries전민건No ratings yet

- Ias 1 7 8 10 ReviewerDocument13 pagesIas 1 7 8 10 ReviewerHazel Andrea Garduque LopezNo ratings yet

- Asset Recognition and Operating Assets: Fourth EditionDocument55 pagesAsset Recognition and Operating Assets: Fourth EditionAyush JainNo ratings yet

- RFM Annual Report Financial StatementDocument7 pagesRFM Annual Report Financial StatementMarceline AbadeerNo ratings yet

- Balance Sheet Quiz 1Document2 pagesBalance Sheet Quiz 1JDFunkyHomosapien100% (1)

- BIP-Week-13-14-with NotesDocument8 pagesBIP-Week-13-14-with NotesgelNo ratings yet

- Advac2 MidtermDocument5 pagesAdvac2 MidtermgeminailnaNo ratings yet

- Group Assignment On Fundamentals of Accounting IDocument6 pagesGroup Assignment On Fundamentals of Accounting IKaleab ShimelsNo ratings yet

- 澳亚 CPA 21S1 FR week2 M2&3Document89 pages澳亚 CPA 21S1 FR week2 M2&3Sijia TaoNo ratings yet

- Actoserba Active Wholesale Private Limited: Detailed ReportDocument11 pagesActoserba Active Wholesale Private Limited: Detailed Reportb0gm3n0tNo ratings yet

- Not-for-Profit Organizations - Answers: Advanced Level Examination - Unit 08Document12 pagesNot-for-Profit Organizations - Answers: Advanced Level Examination - Unit 08Dimuthu JayasuriyaNo ratings yet

- Funds Flow Statement FormatDocument2 pagesFunds Flow Statement FormatBheemeswar ReddyNo ratings yet

- 1q 2022 Fish Fks+Multi+Agro+TbkDocument123 pages1q 2022 Fish Fks+Multi+Agro+TbkCaster XampakhNo ratings yet

- Conceptual Framework and Accounting Standards Final ExamDocument59 pagesConceptual Framework and Accounting Standards Final ExamCleofe Mae Piñero AseñasNo ratings yet

- 19696ipcc Acc Vol2 Chapter14Document41 pages19696ipcc Acc Vol2 Chapter14Shivam TripathiNo ratings yet

- Diagnostic Level 3 AccountingDocument17 pagesDiagnostic Level 3 AccountingRobert CastilloNo ratings yet

- Chapter 3 Mid SlybusDocument15 pagesChapter 3 Mid SlybusImtiaz SultanNo ratings yet

- Reviewer Intangibles AssetsDocument4 pagesReviewer Intangibles AssetsPeter Elijah AntonioNo ratings yet

- PBRX Financial Report Dec 2018 (Audited)Document84 pagesPBRX Financial Report Dec 2018 (Audited)ronaldi lioeNo ratings yet

- FinancialAnalysis - EQUIPOS DEL NORTEDocument6 pagesFinancialAnalysis - EQUIPOS DEL NORTEOscar TrujilloNo ratings yet

- Advanced Financial Management - Finals-11Document2 pagesAdvanced Financial Management - Finals-11graalNo ratings yet

- Perpetual vs. Periodic Inventory System Journal EntriesDocument12 pagesPerpetual vs. Periodic Inventory System Journal EntriesMutia SefriliaNo ratings yet

- Pidilite Industries: ReduceDocument9 pagesPidilite Industries: ReduceIS group 7No ratings yet

- Landing On You Travel Services Company, A Company: Page 1 of 22Document22 pagesLanding On You Travel Services Company, A Company: Page 1 of 22LETS STUDY100% (2)

- Corporate Law Forum: Accounting Basics For LawyersDocument43 pagesCorporate Law Forum: Accounting Basics For LawyerszahirrayhanNo ratings yet

- Theories Accounting ProcessDocument5 pagesTheories Accounting Processshella vienNo ratings yet

- Financial and Managerial AccountingDocument1 pageFinancial and Managerial Accountingcons theNo ratings yet