Download as pdf or txt

You might also like

- Progjyoti Joining LetterDocument6 pagesProgjyoti Joining LetterPorag Jyoti Neog75% (4)

- ct52010 2013Document162 pagesct52010 2013Wei SeongNo ratings yet

- Group Report For NX0441Document25 pagesGroup Report For NX0441Avinash AsokanNo ratings yet

- Subjectct52005 2009 PDFDocument181 pagesSubjectct52005 2009 PDFpaul.tsho7504No ratings yet

- SM 08182019Document10 pagesSM 08182019Anikala Mahadevan100% (1)

- Institute and Faculty of Actuaries: Subject CT5 - Contingencies Core TechnicalDocument19 pagesInstitute and Faculty of Actuaries: Subject CT5 - Contingencies Core TechnicalNayaz NMNo ratings yet

- Courier Service PlanDocument28 pagesCourier Service PlanSimon Lim100% (2)

- Institute and Faculty of Actuaries: Subject CT5 - Contingencies Core TechnicalDocument20 pagesInstitute and Faculty of Actuaries: Subject CT5 - Contingencies Core TechnicalKashif KhalidNo ratings yet

- 114 008 1 ct5Document8 pages114 008 1 ct5Wei SeongNo ratings yet

- IandF CT5 201604 ExamDocument7 pagesIandF CT5 201604 ExamPatrick MugoNo ratings yet

- P&RLIP Unit 2 PracticeQuestionsDocument11 pagesP&RLIP Unit 2 PracticeQuestionsSamyak ZaveriNo ratings yet

- PRLIP Assignment1Document8 pagesPRLIP Assignment1Poorva ShindeNo ratings yet

- FandI CT5 200509 ExampaperDocument8 pagesFandI CT5 200509 ExampaperEuston ChinharaNo ratings yet

- Actuarial CT5 General Insurance, Life and Health Contingencies Sample Paper 2011Document11 pagesActuarial CT5 General Insurance, Life and Health Contingencies Sample Paper 2011ActuarialAnswers50% (2)

- CT5 2015-2Document46 pagesCT5 2015-2Corry CarltonNo ratings yet

- Kotak Assured Income PlanDocument9 pagesKotak Assured Income Plandinesh2u85No ratings yet

- Institute and Faculty of Actuaries: Subject CT5 - Contingencies Core TechnicalDocument7 pagesInstitute and Faculty of Actuaries: Subject CT5 - Contingencies Core TechnicalMadonnaNo ratings yet

- CIN4110200905 Actuarial Mathematics IIADocument6 pagesCIN4110200905 Actuarial Mathematics IIAKimondo KingNo ratings yet

- ENDOWMENT PLAN - (Table No. 14) Benefit Illustration: Guaranteed Surrender ValueDocument3 pagesENDOWMENT PLAN - (Table No. 14) Benefit Illustration: Guaranteed Surrender ValueGBKNo ratings yet

- Cm1a April23 Exam Clean-ProofDocument6 pagesCm1a April23 Exam Clean-ProofShuvrajyoti BhattacharjeeNo ratings yet

- MONEY BACK PLAN - (Table No. 75) Benefit IllustrationDocument4 pagesMONEY BACK PLAN - (Table No. 75) Benefit IllustrationVinayak DhotreNo ratings yet

- Module 6 ExercisesDocument12 pagesModule 6 Exerciseskenny013No ratings yet

- IandF CM1B 202009 ExamPaperDocument3 pagesIandF CM1B 202009 ExamPaperVaibhav SharmaNo ratings yet

- Ko Tak Term PlanDocument8 pagesKo Tak Term PlanRKNo ratings yet

- A213 October 2019 Written ExamDocument6 pagesA213 October 2019 Written ExamRishi KumarNo ratings yet

- Ko Tak Assured in Come PlanDocument12 pagesKo Tak Assured in Come Planbvvrao787669No ratings yet

- Great Cash Wonder (Launch) Write-UpDocument8 pagesGreat Cash Wonder (Launch) Write-UpAlex GeorgeNo ratings yet

- 825 E-Term 288V01 SLDocument5 pages825 E-Term 288V01 SLIncredible MediaNo ratings yet

- CM1B CH 26-28 003 QN (Profit Test With Surrenders) V01 GokuDocument2 pagesCM1B CH 26-28 003 QN (Profit Test With Surrenders) V01 GokuManjit BhusalNo ratings yet

- 821 MoneyBack25 278V01 SLDocument8 pages821 MoneyBack25 278V01 SLdvk.dummymailNo ratings yet

- Jeevan Anurag: Assured BenefitDocument10 pagesJeevan Anurag: Assured BenefitMandheer ChitnavisNo ratings yet

- Lic'S Bima Account - I (Plan No. 805) (UIN: 512N263V01)Document8 pagesLic'S Bima Account - I (Plan No. 805) (UIN: 512N263V01)Niten GuptaNo ratings yet

- Bima Nivesh Triple Cover Table NoDocument3 pagesBima Nivesh Triple Cover Table Noravirawat15No ratings yet

- As The Name ExplainsDocument29 pagesAs The Name ExplainsJeriin Joy ThomasNo ratings yet

- Insurance Pension PlansDocument35 pagesInsurance Pension Plansedrich1932No ratings yet

- Aviva I-Growth BrochureDocument1 pageAviva I-Growth BrochureVarun SharmaNo ratings yet

- Insurance Ia 2Document6 pagesInsurance Ia 2Vikrant SinghNo ratings yet

- Bajaj Allianz Cash Gain Platinum 116N019V01Document6 pagesBajaj Allianz Cash Gain Platinum 116N019V01Suresh BabuNo ratings yet

- Iandf Ct5 201204 Exam FinalDocument6 pagesIandf Ct5 201204 Exam FinalEuston ChinharaNo ratings yet

- Examination: Subject CT5 Contingencies Core TechnicalDocument181 pagesExamination: Subject CT5 Contingencies Core Technicalchan chadoNo ratings yet

- FandI CT5 200504 ExampaperDocument7 pagesFandI CT5 200504 ExampaperClerry SamuelNo ratings yet

- Life Insurance Life Insurance Corporation of IndiaDocument7 pagesLife Insurance Life Insurance Corporation of IndiaYatheendra KumarNo ratings yet

- Life Gain Premier BrochureDocument12 pagesLife Gain Premier BrochureNeeralNo ratings yet

- Computation of Premium of Life Insurance PlansDocument9 pagesComputation of Premium of Life Insurance PlansAbhishek Singh PariharNo ratings yet

- Salient Features:: LIC Introduces New Jeevan Nidhi' - Deferred Pension PlanDocument5 pagesSalient Features:: LIC Introduces New Jeevan Nidhi' - Deferred Pension PlanPramod Kumar SaxenaNo ratings yet

- Sales Brochure LIC-s E-Term Rev PDFDocument3 pagesSales Brochure LIC-s E-Term Rev PDFRamesh ThumburuNo ratings yet

- Money Back PlusDocument4 pagesMoney Back Plusvek80No ratings yet

- AR Educare Advantage Insurance Plan 5 May 2014Document6 pagesAR Educare Advantage Insurance Plan 5 May 2014ÌmřańNo ratings yet

- Smart Term Plan ProspectusDocument36 pagesSmart Term Plan Prospectusmantoo kumarNo ratings yet

- New Pension PlusDocument2 pagesNew Pension Plusrsgk75No ratings yet

- Pension PlusDocument4 pagesPension PlusChiranjivi Maruthi RaoNo ratings yet

- 836 JeevanLabh 304V01 SLDocument9 pages836 JeevanLabh 304V01 SLPriya PahujaNo ratings yet

- 836 JeevanLabh 304V01 SLDocument9 pages836 JeevanLabh 304V01 SLPriya PahujaNo ratings yet

- Endowment Plus: in This Policy, The Investment Risk in Investment Portfolio Is Borne by The PolicyholderDocument13 pagesEndowment Plus: in This Policy, The Investment Risk in Investment Portfolio Is Borne by The Policyholderas12df34gh56No ratings yet

- LIC S Bima Gold - 512N231V01 PDFDocument8 pagesLIC S Bima Gold - 512N231V01 PDFPooja ReddyNo ratings yet

- Kotak Endowment PlanDocument2 pagesKotak Endowment PlanMichael GreenNo ratings yet

- Exide Life Secured Income Insurance RPDocument10 pagesExide Life Secured Income Insurance RPrahul sarmaNo ratings yet

- Assignment On Padma Islami Life Insurance Co. Ltd.Document21 pagesAssignment On Padma Islami Life Insurance Co. Ltd.Muktadirhasan100% (3)

- GSIP BrochureDocument2 pagesGSIP Brochureabdul.nm4064No ratings yet

- Eligibility Conditions and Other Restriction:: Date of Commencement of Risk Under The PlanDocument5 pagesEligibility Conditions and Other Restriction:: Date of Commencement of Risk Under The PlansyedNo ratings yet

- The Handbook for Reading and Preparing Proxy Statements: A Guide to the SEC Disclosure Rules for Executive and Director Compensation, 6th EditionFrom EverandThe Handbook for Reading and Preparing Proxy Statements: A Guide to the SEC Disclosure Rules for Executive and Director Compensation, 6th EditionNo ratings yet

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- Variable Costing and Full CostingDocument2 pagesVariable Costing and Full CostingSiti WidiasariNo ratings yet

- Oriental Insurance Nagrik Suraksha Proposal FormDocument2 pagesOriental Insurance Nagrik Suraksha Proposal FormArijeet MondalNo ratings yet

- Practice Activity - SolvedDocument1 pagePractice Activity - SolvedanzarNo ratings yet

- Kapatagan NHS Opcr Mio Target Sy 2020 2021Document79 pagesKapatagan NHS Opcr Mio Target Sy 2020 2021Dhann Cromente100% (1)

- CF 19-03-21 (BudgetDocument21 pagesCF 19-03-21 (BudgetTarisya PermatasariNo ratings yet

- Reason-Rupe April 2014 National Telephone PollDocument10 pagesReason-Rupe April 2014 National Telephone PollEmily McClintock EkinsNo ratings yet

- Running Head: Corporate Performance Evaluation For Facebook 1Document12 pagesRunning Head: Corporate Performance Evaluation For Facebook 1Mohammad KhataybehNo ratings yet

- Fu-Wang Foods Ltd. AnalysisDocument27 pagesFu-Wang Foods Ltd. AnalysisAynul Bashar AmitNo ratings yet

- BrandVal JBM10Document38 pagesBrandVal JBM10Ronald RunruilNo ratings yet

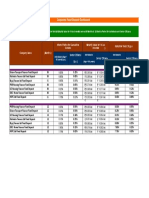

- Corporate Fixed Deposit DashboardDocument1 pageCorporate Fixed Deposit DashboardWealth Maker BuddyNo ratings yet

- UG022510 International GCSE in Business Studies 4BS0 For WebDocument57 pagesUG022510 International GCSE in Business Studies 4BS0 For WebAnonymous 8aj9gk7GCLNo ratings yet

- Problem Set: 1 IntroductionDocument5 pagesProblem Set: 1 IntroductionSumit GuptaNo ratings yet

- Financial Feasibility AnalysisDocument14 pagesFinancial Feasibility AnalysisSanjeet Pandey100% (2)

- Final Order - Case No 38 of 2014Document148 pagesFinal Order - Case No 38 of 2014sachinoilNo ratings yet

- Econ 100.1 - ReviewerDocument34 pagesEcon 100.1 - ReviewerLianne Angelico Depante100% (1)

- Ankitastic Exams SolutionsDocument30 pagesAnkitastic Exams SolutionsAnkitastic tutoring ServicesNo ratings yet

- MACR L&T Takeover of MindtreeDocument24 pagesMACR L&T Takeover of Mindtreeswapnil tyagi50% (2)

- Application For Salary IncreaseDocument3 pagesApplication For Salary IncreaseAllamsNo ratings yet

- Cup - AuditDocument7 pagesCup - AuditJerauld BucolNo ratings yet

- Accounting and Auditing Laws Rules and Regulations Atty Billy Joe Ivan DarbinDocument57 pagesAccounting and Auditing Laws Rules and Regulations Atty Billy Joe Ivan DarbinAyan Vico100% (3)

- FIX ASSET&INTANGIBLE ASSET Kel. 1 AKM 1 PDFDocument6 pagesFIX ASSET&INTANGIBLE ASSET Kel. 1 AKM 1 PDFAdindaNo ratings yet

- Engleza EconomicaDocument58 pagesEngleza EconomicaIonela AnghelinaNo ratings yet

- Zee Learn Analyst PresentationDocument58 pagesZee Learn Analyst PresentationAsha PrabhacarNo ratings yet

- AFA1-3C - Assignment 2Document10 pagesAFA1-3C - Assignment 2Segarambal MasilamoneyNo ratings yet

- Bata Annual Report 2012Document72 pagesBata Annual Report 2012md abdul khalekNo ratings yet