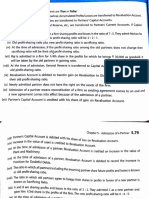

BSBFIM601Appendices 2 V2.0

BSBFIM601Appendices 2 V2.0

You might also like

- Mid-Term Exam: Professor: Kevin Petit-Frère Duration: 180 MinutesDocument7 pagesMid-Term Exam: Professor: Kevin Petit-Frère Duration: 180 MinutesAbby Hacther0% (2)

- Manage Finances 1Document9 pagesManage Finances 1Ashish Jaat100% (1)

- Prepare Budgets: Performance ObjectiveDocument25 pagesPrepare Budgets: Performance ObjectiveTanushree JawariyaNo ratings yet

- Bsbfim601 Mustafa's ReportDocument12 pagesBsbfim601 Mustafa's Reportmustafa mohammedNo ratings yet

- Financial Aspect - Feasibility StudyDocument33 pagesFinancial Aspect - Feasibility StudyAgayatak Sa Manen55% (20)

- Catalytic Solutions, Inc.Document1 pageCatalytic Solutions, Inc.Xin GongNo ratings yet

- 5 Construction Accounting MethodsDocument8 pages5 Construction Accounting MethodsNikki Jane SolterasNo ratings yet

- HDEC 2021 Annual ReportDocument174 pagesHDEC 2021 Annual Reportagust.abcNo ratings yet

- Acct3044 Tutorial 2 SolutionDocument4 pagesAcct3044 Tutorial 2 SolutionJENNIFER LEGGNo ratings yet

- As 01Document9 pagesAs 01Dipak UgaleNo ratings yet

- BSBFIM501 - Assessment Task 1Document7 pagesBSBFIM501 - Assessment Task 1babluanandNo ratings yet

- ESG Year End Instructions 2022Document11 pagesESG Year End Instructions 2022cabaroNo ratings yet

- Audit Consideration - Construction & Real StateDocument6 pagesAudit Consideration - Construction & Real StateAngelica BuenaventuraNo ratings yet

- Lecture 0924Document38 pagesLecture 0924jasonnumahnalkelNo ratings yet

- LG Chem 2020 Contingent Financial StatementsDocument102 pagesLG Chem 2020 Contingent Financial StatementsAyushika SinghNo ratings yet

- Emperical ProjectDocument11 pagesEmperical ProjectSajal ChakarvartyNo ratings yet

- University of CTGDocument31 pagesUniversity of CTGRumi RahmanNo ratings yet

- AA-AuditingDocument6 pagesAA-AuditingKim Ngọc HuyềnNo ratings yet

- NCERT Questions - Financial Statements (Final Accounts) - Evero PDFDocument53 pagesNCERT Questions - Financial Statements (Final Accounts) - Evero PDFYogendra PatelNo ratings yet

- AuditDocument10 pagesAuditlucinossNo ratings yet

- Vanraj Smart Task 2Document4 pagesVanraj Smart Task 2Vanraj MakwanaNo ratings yet

- Smc-Sec Form 17-A (04.17.2023) Part2-FinalDocument305 pagesSmc-Sec Form 17-A (04.17.2023) Part2-FinalRenneth Ena OdeNo ratings yet

- SECL - Audit Report - FY22 - Sign - ENGDocument101 pagesSECL - Audit Report - FY22 - Sign - ENGJAMES ANDROE TANNo ratings yet

- BSBFIM501 Manage Budgets and Financial Plans Learner Instructions 1 (Plan Financial Management Approaches)Document8 pagesBSBFIM501 Manage Budgets and Financial Plans Learner Instructions 1 (Plan Financial Management Approaches)vipulclasses01 vipulclassNo ratings yet

- AS Theory CA IPCC I & IIDocument19 pagesAS Theory CA IPCC I & IICaramakr ManthaNo ratings yet

- Analysis of Financial Reports: Submitted byDocument17 pagesAnalysis of Financial Reports: Submitted byMalik Muhammad Ali EhsanNo ratings yet

- Indian Accounting Standard 34Document17 pagesIndian Accounting Standard 34Reetika VaidNo ratings yet

- Accounting StandardsDocument10 pagesAccounting StandardsSakshi JaiswalNo ratings yet

- Simer Project On Non Performing Assets..Document61 pagesSimer Project On Non Performing Assets..Simer KaurNo ratings yet

- BSBFIM601 Hints For Task 2Document32 pagesBSBFIM601 Hints For Task 2Marwan Issa71% (7)

- BSBFIM601 Hints For Task 2Document32 pagesBSBFIM601 Hints For Task 2Mohammed MGNo ratings yet

- BSBFIM601 Manage Finances AwserDocument27 pagesBSBFIM601 Manage Finances AwserPriyanka Aggarwal100% (2)

- Prepare Budgets: Submission DetailsDocument22 pagesPrepare Budgets: Submission DetailsTanushree JawariyaNo ratings yet

- APDocument12 pagesAPf15215No ratings yet

- 2021 LG Chem Consolidated Financial Statements enDocument113 pages2021 LG Chem Consolidated Financial Statements enAyushika SinghNo ratings yet

- 1408 22 5 30to8 30pm 2Document155 pages1408 22 5 30to8 30pm 2Devi SreeNo ratings yet

- Introducing A New Business As An AccountantDocument6 pagesIntroducing A New Business As An AccountantRameen SyedNo ratings yet

- BudgetingDocument4 pagesBudgetingshielamaelbaisacNo ratings yet

- SECTION E - 23 ArchidplyDocument24 pagesSECTION E - 23 ArchidplyazharNo ratings yet

- Lesson 4 Part 1 Budget PreparationDocument19 pagesLesson 4 Part 1 Budget PreparationmariannedakilaNo ratings yet

- Revenue Recognition IssuesDocument15 pagesRevenue Recognition IssuesDaud Farook IINo ratings yet

- BudgetingDocument35 pagesBudgetingRisty Ridharty DimanNo ratings yet

- Capital Conservation MeasuresDocument2 pagesCapital Conservation MeasuresrajkaushikNo ratings yet

- Quarterly Outlook June 2017Document29 pagesQuarterly Outlook June 2017Chessking Siew HeeNo ratings yet

- FIN 302 Notes 1Document55 pagesFIN 302 Notes 1Tekego TlakaleNo ratings yet

- Original 1436552353 VICTORIA ProjectDocument12 pagesOriginal 1436552353 VICTORIA ProjectShashank SharanNo ratings yet

- AAA Question PracticeDocument8 pagesAAA Question PracticenishantsayshiNo ratings yet

- Planning and Working Capital Management Part 1Document31 pagesPlanning and Working Capital Management Part 1Michelle RotairoNo ratings yet

- SITXFIN003 - Manage Finances With in The Budget NEWDocument33 pagesSITXFIN003 - Manage Finances With in The Budget NEWpablo zarate0% (1)

- BSBFIM501 ASS3 NiranDocument14 pagesBSBFIM501 ASS3 NiranMaykiza NiranpakornNo ratings yet

- Natura 2016 AR Engl PDFDocument140 pagesNatura 2016 AR Engl PDFManuel CámacNo ratings yet

- My Final ProjectDocument68 pagesMy Final ProjectSAINo ratings yet

- Financial Planning and ToolsDocument41 pagesFinancial Planning and ToolsShalom BuenafeNo ratings yet

- Bsbfia401 Amit ChhetriDocument20 pagesBsbfia401 Amit Chhetriamitchettri419No ratings yet

- Group 1 Budget ProcessDocument26 pagesGroup 1 Budget ProcessCassie ParkNo ratings yet

- Paper TAKDocument11 pagesPaper TAKHayyin Nur AdisaNo ratings yet

- TOR For Project Financial Management SpecialistDocument4 pagesTOR For Project Financial Management SpecialistEmil LeauNo ratings yet

- Accounting IC AR ExampleDocument3 pagesAccounting IC AR Exampleayuadeanggariani96No ratings yet

- Gemoknyer Soalan..Document6 pagesGemoknyer Soalan..Nurulizwa Bte Abdul RashidNo ratings yet

- Preparation of Financial BudgetDocument10 pagesPreparation of Financial Budgetarshad rahmanNo ratings yet

- Financial Accounting - Want to Become Financial Accountant in 30 Days?From EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Rating: 3.5 out of 5 stars3.5/5 (2)

- Logistics Management - SSRMDocument8 pagesLogistics Management - SSRMmitu lead01No ratings yet

- Strategic Management and Business Policy Globalization Innovation and Sustainability 14th Edition Wheelen Solutions ManualDocument20 pagesStrategic Management and Business Policy Globalization Innovation and Sustainability 14th Edition Wheelen Solutions Manualequally.ungown.q5sgg100% (16)

- Oveheads Practice QuestionsDocument674 pagesOveheads Practice Questionsyashwant ashokNo ratings yet

- Difference Between Financial & Managerial AccountingDocument3 pagesDifference Between Financial & Managerial AccountingAnisa LabibaNo ratings yet

- Strategic Management and Buisness Poilcy - CadburyDocument14 pagesStrategic Management and Buisness Poilcy - CadburyMohit KakkarNo ratings yet

- Sarbanes-Oxley Act, Internal Control, and Management AccountingDocument2 pagesSarbanes-Oxley Act, Internal Control, and Management Accountingalexandro_novora6396No ratings yet

- Q1. What Is Organized Retail? What Is Modern Trade? Elaborate With ExamplesDocument2 pagesQ1. What Is Organized Retail? What Is Modern Trade? Elaborate With ExamplesRAHUL PATHAKNo ratings yet

- PAS 16 Property, Plant and EquipmentDocument4 pagesPAS 16 Property, Plant and Equipmentpanda 1No ratings yet

- Goal Congruence Problems With Cost Plus Transfer Pricing MethodsDocument1 pageGoal Congruence Problems With Cost Plus Transfer Pricing Methodstrilocksp SinghNo ratings yet

- Pas 1Document26 pagesPas 1Princess Jullyn ClaudioNo ratings yet

- 10 HR Metrics Every Company Should Track + 5 Advanced Metrics To Know PDFDocument44 pages10 HR Metrics Every Company Should Track + 5 Advanced Metrics To Know PDFSangar AhmedNo ratings yet

- 17 - The IPSASB's Next Strategy and Work Program - FinalDocument23 pages17 - The IPSASB's Next Strategy and Work Program - FinalMuh BaraNo ratings yet

- PErakaunan AsignmentDocument9 pagesPErakaunan AsignmentolymenaNo ratings yet

- Objective Type Questions: True or FalseDocument25 pagesObjective Type Questions: True or Falsesameeksha kosariaNo ratings yet

- E-Commerce: Digital Markets, Digital Goods: Managing The Digital Firm, 12 Edition Global EditionDocument28 pagesE-Commerce: Digital Markets, Digital Goods: Managing The Digital Firm, 12 Edition Global EditionMintu ranaNo ratings yet

- Assessing The Internal Environment of The Firm: EducationDocument14 pagesAssessing The Internal Environment of The Firm: EducationVikasNo ratings yet

- Chit Fund FormsDocument45 pagesChit Fund Formssaisankar ladiNo ratings yet

- Chapter 3Document7 pagesChapter 3Jarra AbdurahmanNo ratings yet

- Audit Report Template Final Pub 70121 Clean - 0Document19 pagesAudit Report Template Final Pub 70121 Clean - 0Bhavana CMNo ratings yet

- Disbursement Voucher (New Orence)Document4 pagesDisbursement Voucher (New Orence)user computerNo ratings yet

- Final Project HimanshuDocument35 pagesFinal Project HimanshuHimanshu SinghNo ratings yet

- Ali ExpressDocument3 pagesAli ExpressAnsa AhmedNo ratings yet

- Business EnvironmentDocument25 pagesBusiness EnvironmentMalik UzairNo ratings yet

- Caie As Level: BUSINESS (9609)Document44 pagesCaie As Level: BUSINESS (9609)Shahriar OntherunNo ratings yet

- IMC PptsDocument270 pagesIMC Pptssamaya pypNo ratings yet

- Companies Interview Questions: Bhawan Cyber TechDocument17 pagesCompanies Interview Questions: Bhawan Cyber TechharifavouriteenglishNo ratings yet

- Practice Test For Midte...Document22 pagesPractice Test For Midte...DhrushiNo ratings yet

- A Project Report ON Industrial Visit AT: M. K. School of Business Management, PatanDocument63 pagesA Project Report ON Industrial Visit AT: M. K. School of Business Management, Patanj_d19912009No ratings yet

Download as pdf or txt

You might also like

- Mid-Term Exam: Professor: Kevin Petit-Frère Duration: 180 MinutesDocument7 pagesMid-Term Exam: Professor: Kevin Petit-Frère Duration: 180 MinutesAbby Hacther0% (2)

- Manage Finances 1Document9 pagesManage Finances 1Ashish Jaat100% (1)

- Prepare Budgets: Performance ObjectiveDocument25 pagesPrepare Budgets: Performance ObjectiveTanushree JawariyaNo ratings yet

- Bsbfim601 Mustafa's ReportDocument12 pagesBsbfim601 Mustafa's Reportmustafa mohammedNo ratings yet

- Financial Aspect - Feasibility StudyDocument33 pagesFinancial Aspect - Feasibility StudyAgayatak Sa Manen55% (20)

- Catalytic Solutions, Inc.Document1 pageCatalytic Solutions, Inc.Xin GongNo ratings yet

- 5 Construction Accounting MethodsDocument8 pages5 Construction Accounting MethodsNikki Jane SolterasNo ratings yet

- HDEC 2021 Annual ReportDocument174 pagesHDEC 2021 Annual Reportagust.abcNo ratings yet

- Acct3044 Tutorial 2 SolutionDocument4 pagesAcct3044 Tutorial 2 SolutionJENNIFER LEGGNo ratings yet

- As 01Document9 pagesAs 01Dipak UgaleNo ratings yet

- BSBFIM501 - Assessment Task 1Document7 pagesBSBFIM501 - Assessment Task 1babluanandNo ratings yet

- ESG Year End Instructions 2022Document11 pagesESG Year End Instructions 2022cabaroNo ratings yet

- Audit Consideration - Construction & Real StateDocument6 pagesAudit Consideration - Construction & Real StateAngelica BuenaventuraNo ratings yet

- Lecture 0924Document38 pagesLecture 0924jasonnumahnalkelNo ratings yet

- LG Chem 2020 Contingent Financial StatementsDocument102 pagesLG Chem 2020 Contingent Financial StatementsAyushika SinghNo ratings yet

- Emperical ProjectDocument11 pagesEmperical ProjectSajal ChakarvartyNo ratings yet

- University of CTGDocument31 pagesUniversity of CTGRumi RahmanNo ratings yet

- AA-AuditingDocument6 pagesAA-AuditingKim Ngọc HuyềnNo ratings yet

- NCERT Questions - Financial Statements (Final Accounts) - Evero PDFDocument53 pagesNCERT Questions - Financial Statements (Final Accounts) - Evero PDFYogendra PatelNo ratings yet

- AuditDocument10 pagesAuditlucinossNo ratings yet

- Vanraj Smart Task 2Document4 pagesVanraj Smart Task 2Vanraj MakwanaNo ratings yet

- Smc-Sec Form 17-A (04.17.2023) Part2-FinalDocument305 pagesSmc-Sec Form 17-A (04.17.2023) Part2-FinalRenneth Ena OdeNo ratings yet

- SECL - Audit Report - FY22 - Sign - ENGDocument101 pagesSECL - Audit Report - FY22 - Sign - ENGJAMES ANDROE TANNo ratings yet

- BSBFIM501 Manage Budgets and Financial Plans Learner Instructions 1 (Plan Financial Management Approaches)Document8 pagesBSBFIM501 Manage Budgets and Financial Plans Learner Instructions 1 (Plan Financial Management Approaches)vipulclasses01 vipulclassNo ratings yet

- AS Theory CA IPCC I & IIDocument19 pagesAS Theory CA IPCC I & IICaramakr ManthaNo ratings yet

- Analysis of Financial Reports: Submitted byDocument17 pagesAnalysis of Financial Reports: Submitted byMalik Muhammad Ali EhsanNo ratings yet

- Indian Accounting Standard 34Document17 pagesIndian Accounting Standard 34Reetika VaidNo ratings yet

- Accounting StandardsDocument10 pagesAccounting StandardsSakshi JaiswalNo ratings yet

- Simer Project On Non Performing Assets..Document61 pagesSimer Project On Non Performing Assets..Simer KaurNo ratings yet

- BSBFIM601 Hints For Task 2Document32 pagesBSBFIM601 Hints For Task 2Marwan Issa71% (7)

- BSBFIM601 Hints For Task 2Document32 pagesBSBFIM601 Hints For Task 2Mohammed MGNo ratings yet

- BSBFIM601 Manage Finances AwserDocument27 pagesBSBFIM601 Manage Finances AwserPriyanka Aggarwal100% (2)

- Prepare Budgets: Submission DetailsDocument22 pagesPrepare Budgets: Submission DetailsTanushree JawariyaNo ratings yet

- APDocument12 pagesAPf15215No ratings yet

- 2021 LG Chem Consolidated Financial Statements enDocument113 pages2021 LG Chem Consolidated Financial Statements enAyushika SinghNo ratings yet

- 1408 22 5 30to8 30pm 2Document155 pages1408 22 5 30to8 30pm 2Devi SreeNo ratings yet

- Introducing A New Business As An AccountantDocument6 pagesIntroducing A New Business As An AccountantRameen SyedNo ratings yet

- BudgetingDocument4 pagesBudgetingshielamaelbaisacNo ratings yet

- SECTION E - 23 ArchidplyDocument24 pagesSECTION E - 23 ArchidplyazharNo ratings yet

- Lesson 4 Part 1 Budget PreparationDocument19 pagesLesson 4 Part 1 Budget PreparationmariannedakilaNo ratings yet

- Revenue Recognition IssuesDocument15 pagesRevenue Recognition IssuesDaud Farook IINo ratings yet

- BudgetingDocument35 pagesBudgetingRisty Ridharty DimanNo ratings yet

- Capital Conservation MeasuresDocument2 pagesCapital Conservation MeasuresrajkaushikNo ratings yet

- Quarterly Outlook June 2017Document29 pagesQuarterly Outlook June 2017Chessking Siew HeeNo ratings yet

- FIN 302 Notes 1Document55 pagesFIN 302 Notes 1Tekego TlakaleNo ratings yet

- Original 1436552353 VICTORIA ProjectDocument12 pagesOriginal 1436552353 VICTORIA ProjectShashank SharanNo ratings yet

- AAA Question PracticeDocument8 pagesAAA Question PracticenishantsayshiNo ratings yet

- Planning and Working Capital Management Part 1Document31 pagesPlanning and Working Capital Management Part 1Michelle RotairoNo ratings yet

- SITXFIN003 - Manage Finances With in The Budget NEWDocument33 pagesSITXFIN003 - Manage Finances With in The Budget NEWpablo zarate0% (1)

- BSBFIM501 ASS3 NiranDocument14 pagesBSBFIM501 ASS3 NiranMaykiza NiranpakornNo ratings yet

- Natura 2016 AR Engl PDFDocument140 pagesNatura 2016 AR Engl PDFManuel CámacNo ratings yet

- My Final ProjectDocument68 pagesMy Final ProjectSAINo ratings yet

- Financial Planning and ToolsDocument41 pagesFinancial Planning and ToolsShalom BuenafeNo ratings yet

- Bsbfia401 Amit ChhetriDocument20 pagesBsbfia401 Amit Chhetriamitchettri419No ratings yet

- Group 1 Budget ProcessDocument26 pagesGroup 1 Budget ProcessCassie ParkNo ratings yet

- Paper TAKDocument11 pagesPaper TAKHayyin Nur AdisaNo ratings yet

- TOR For Project Financial Management SpecialistDocument4 pagesTOR For Project Financial Management SpecialistEmil LeauNo ratings yet

- Accounting IC AR ExampleDocument3 pagesAccounting IC AR Exampleayuadeanggariani96No ratings yet

- Gemoknyer Soalan..Document6 pagesGemoknyer Soalan..Nurulizwa Bte Abdul RashidNo ratings yet

- Preparation of Financial BudgetDocument10 pagesPreparation of Financial Budgetarshad rahmanNo ratings yet

- Financial Accounting - Want to Become Financial Accountant in 30 Days?From EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Rating: 3.5 out of 5 stars3.5/5 (2)

- Logistics Management - SSRMDocument8 pagesLogistics Management - SSRMmitu lead01No ratings yet

- Strategic Management and Business Policy Globalization Innovation and Sustainability 14th Edition Wheelen Solutions ManualDocument20 pagesStrategic Management and Business Policy Globalization Innovation and Sustainability 14th Edition Wheelen Solutions Manualequally.ungown.q5sgg100% (16)

- Oveheads Practice QuestionsDocument674 pagesOveheads Practice Questionsyashwant ashokNo ratings yet

- Difference Between Financial & Managerial AccountingDocument3 pagesDifference Between Financial & Managerial AccountingAnisa LabibaNo ratings yet

- Strategic Management and Buisness Poilcy - CadburyDocument14 pagesStrategic Management and Buisness Poilcy - CadburyMohit KakkarNo ratings yet

- Sarbanes-Oxley Act, Internal Control, and Management AccountingDocument2 pagesSarbanes-Oxley Act, Internal Control, and Management Accountingalexandro_novora6396No ratings yet

- Q1. What Is Organized Retail? What Is Modern Trade? Elaborate With ExamplesDocument2 pagesQ1. What Is Organized Retail? What Is Modern Trade? Elaborate With ExamplesRAHUL PATHAKNo ratings yet

- PAS 16 Property, Plant and EquipmentDocument4 pagesPAS 16 Property, Plant and Equipmentpanda 1No ratings yet

- Goal Congruence Problems With Cost Plus Transfer Pricing MethodsDocument1 pageGoal Congruence Problems With Cost Plus Transfer Pricing Methodstrilocksp SinghNo ratings yet

- Pas 1Document26 pagesPas 1Princess Jullyn ClaudioNo ratings yet

- 10 HR Metrics Every Company Should Track + 5 Advanced Metrics To Know PDFDocument44 pages10 HR Metrics Every Company Should Track + 5 Advanced Metrics To Know PDFSangar AhmedNo ratings yet

- 17 - The IPSASB's Next Strategy and Work Program - FinalDocument23 pages17 - The IPSASB's Next Strategy and Work Program - FinalMuh BaraNo ratings yet

- PErakaunan AsignmentDocument9 pagesPErakaunan AsignmentolymenaNo ratings yet

- Objective Type Questions: True or FalseDocument25 pagesObjective Type Questions: True or Falsesameeksha kosariaNo ratings yet

- E-Commerce: Digital Markets, Digital Goods: Managing The Digital Firm, 12 Edition Global EditionDocument28 pagesE-Commerce: Digital Markets, Digital Goods: Managing The Digital Firm, 12 Edition Global EditionMintu ranaNo ratings yet

- Assessing The Internal Environment of The Firm: EducationDocument14 pagesAssessing The Internal Environment of The Firm: EducationVikasNo ratings yet

- Chit Fund FormsDocument45 pagesChit Fund Formssaisankar ladiNo ratings yet

- Chapter 3Document7 pagesChapter 3Jarra AbdurahmanNo ratings yet

- Audit Report Template Final Pub 70121 Clean - 0Document19 pagesAudit Report Template Final Pub 70121 Clean - 0Bhavana CMNo ratings yet

- Disbursement Voucher (New Orence)Document4 pagesDisbursement Voucher (New Orence)user computerNo ratings yet

- Final Project HimanshuDocument35 pagesFinal Project HimanshuHimanshu SinghNo ratings yet

- Ali ExpressDocument3 pagesAli ExpressAnsa AhmedNo ratings yet

- Business EnvironmentDocument25 pagesBusiness EnvironmentMalik UzairNo ratings yet

- Caie As Level: BUSINESS (9609)Document44 pagesCaie As Level: BUSINESS (9609)Shahriar OntherunNo ratings yet

- IMC PptsDocument270 pagesIMC Pptssamaya pypNo ratings yet

- Companies Interview Questions: Bhawan Cyber TechDocument17 pagesCompanies Interview Questions: Bhawan Cyber TechharifavouriteenglishNo ratings yet

- Practice Test For Midte...Document22 pagesPractice Test For Midte...DhrushiNo ratings yet

- A Project Report ON Industrial Visit AT: M. K. School of Business Management, PatanDocument63 pagesA Project Report ON Industrial Visit AT: M. K. School of Business Management, Patanj_d19912009No ratings yet