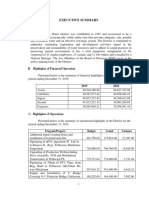

Pozorrubio Water District Executive Summary 2016

Pozorrubio Water District Executive Summary 2016

You might also like

- CS Form No. 6 Revised 2020 Application For Leave Fillable 1Document2 pagesCS Form No. 6 Revised 2020 Application For Leave Fillable 1Leo Artemio PuertosNo ratings yet

- Commission On Audit Office of The Regional Director Regional Office No. IDocument6 pagesCommission On Audit Office of The Regional Director Regional Office No. IEG ReyesNo ratings yet

- 02-PSU2016 Transmittal Letter To Board Of-RegentsDocument2 pages02-PSU2016 Transmittal Letter To Board Of-Regentsjaymark camachoNo ratings yet

- IliganCity2018 Audit ReportDocument378 pagesIliganCity2018 Audit ReportYak IvonNo ratings yet

- 01-LapulapuCity2012 Audit ReportDocument83 pages01-LapulapuCity2012 Audit ReportnelggkramNo ratings yet

- BinalonanWD-R1 ES2018Document4 pagesBinalonanWD-R1 ES2018J JaNo ratings yet

- Moalboal Executive Summary 2018Document5 pagesMoalboal Executive Summary 2018Reyna YlenaNo ratings yet

- NFC 2019Document73 pagesNFC 2019Catherine AgyaoNo ratings yet

- BAAR 2016-2017 - AwihaoDocument43 pagesBAAR 2016-2017 - AwihaoJerwin Cases Tiamson100% (1)

- Transmittal NewDocument4 pagesTransmittal NewAbraham JunioNo ratings yet

- 01 TC2018 Audit Report ADocument114 pages01 TC2018 Audit Report AJerwin Cases TiamsonNo ratings yet

- 05 DILG2017 Part1 Auditor's ReportDocument3 pages05 DILG2017 Part1 Auditor's ReportbolNo ratings yet

- Lingayen Water District Executive Summary 2016Document4 pagesLingayen Water District Executive Summary 2016Paul De LeonNo ratings yet

- Annual Audit Report: Republic of The Philippines Regional Office No. XIII Butuan CityDocument34 pagesAnnual Audit Report: Republic of The Philippines Regional Office No. XIII Butuan Citysandra bolokNo ratings yet

- Binalonan Water District Pangasinan Executive Summary 2019Document4 pagesBinalonan Water District Pangasinan Executive Summary 2019Glen CastroNo ratings yet

- Part I - Audited Financial StatementsDocument3 pagesPart I - Audited Financial Statementssandra bolokNo ratings yet

- Taytay09 Audit ReportDocument57 pagesTaytay09 Audit ReportIpah L. SaidNo ratings yet

- Hinigaran2017 Audit ReportDocument146 pagesHinigaran2017 Audit ReportChito BarsabalNo ratings yet

- 03-PSU2016 Transmittal Letter To The PresidentDocument2 pages03-PSU2016 Transmittal Letter To The Presidentjaymark camachoNo ratings yet

- Lugait Executive Summary 2018Document4 pagesLugait Executive Summary 2018OZ La NB AnamiNo ratings yet

- San Miguel Executive Summary 2011Document12 pagesSan Miguel Executive Summary 2011Justine CastilloNo ratings yet

- 01-Anda2015 Audit ReportDocument92 pages01-Anda2015 Audit ReportoabeljeanmoniqueNo ratings yet

- 2017 Internal Auditor ReportDocument3 pages2017 Internal Auditor ReportMicka EllahNo ratings yet

- Taytay Water District Executive Summary 2018Document6 pagesTaytay Water District Executive Summary 2018Allan SobrepeñaNo ratings yet

- PantaoRagatMun2017 Audit ReportDocument90 pagesPantaoRagatMun2017 Audit ReportMubarrach MatabalaoNo ratings yet

- Metro Kidapawan Water District Kidapawan City Executive Summary 2021Document6 pagesMetro Kidapawan Water District Kidapawan City Executive Summary 2021PaulDanielDeLeonNo ratings yet

- Cabadbaran City Executive Summary 2011Document4 pagesCabadbaran City Executive Summary 2011Frannie PastorNo ratings yet

- 01-Mun of Himamaylan09 Audit Report - COA ANNUAL AUDIT REPORT 2009Document50 pages01-Mun of Himamaylan09 Audit Report - COA ANNUAL AUDIT REPORT 2009himamaylancitywatchNo ratings yet

- Executive Summary: Highlights of Financial OperationsDocument12 pagesExecutive Summary: Highlights of Financial OperationsJaniceNo ratings yet

- 01-LBP2016 Transmittal LettersDocument6 pages01-LBP2016 Transmittal LettersADRIAN 18No ratings yet

- Rizal Executive Summary 2015Document4 pagesRizal Executive Summary 2015Sittie RahmaNo ratings yet

- Commission On Audit Local Government Sector: Republic of The PhilippinesDocument2 pagesCommission On Audit Local Government Sector: Republic of The PhilippinesJonson PalmaresNo ratings yet

- Motiong Executive Summary 2017Document7 pagesMotiong Executive Summary 2017Ronel CadelinoNo ratings yet

- San Agustin Executive Summary 2018Document4 pagesSan Agustin Executive Summary 2018minds2magicNo ratings yet

- CamiguinProv2018 Audit ReportDocument159 pagesCamiguinProv2018 Audit ReporthazelNo ratings yet

- Agusan Del Sur Executive Summary 2018Document8 pagesAgusan Del Sur Executive Summary 2018Sittie Fatma ReporsNo ratings yet

- Commission On AuditDocument2 pagesCommission On AuditJerome MangundayaoNo ratings yet

- 01-Minglanilla2014 Audit ReportDocument45 pages01-Minglanilla2014 Audit ReportZarah Mae UmaliNo ratings yet

- Part Ii - Detailed Observations and RecommendationsDocument16 pagesPart Ii - Detailed Observations and RecommendationsAlicia NhsNo ratings yet

- KalingaProv ES2015Document4 pagesKalingaProv ES2015J JaNo ratings yet

- Northern Kabuntalan Executive Summary 2018Document4 pagesNorthern Kabuntalan Executive Summary 2018Angelo GuevarraNo ratings yet

- Cordon Isabela ES2018Document5 pagesCordon Isabela ES2018MelvinBuyagawonNo ratings yet

- QuezonMetropolitanWD2017 Audit Report PDFDocument196 pagesQuezonMetropolitanWD2017 Audit Report PDFJojoMagnoNo ratings yet

- Baar LabelDocument61 pagesBaar LabelJerwin Cases TiamsonNo ratings yet

- 05 PUP2017 Part1 Auditors ReportDocument3 pages05 PUP2017 Part1 Auditors ReportLet it beNo ratings yet

- Titay ZS ES2016Document5 pagesTitay ZS ES2016J JaNo ratings yet

- 01-Angadanan2020 Transmittal LettersDocument14 pages01-Angadanan2020 Transmittal LettersAlicia NhsNo ratings yet

- Anda Executive Summary 2010Document5 pagesAnda Executive Summary 2010Henry AunzoNo ratings yet

- Commission On Audit: Management's Responsibility For The Financial StatementsDocument3 pagesCommission On Audit: Management's Responsibility For The Financial StatementsVinNo ratings yet

- Lapu Lapu City Executive Summary 2018Document110 pagesLapu Lapu City Executive Summary 2018mharaynel.afableNo ratings yet

- Magallanes Executive Summary 2011Document5 pagesMagallanes Executive Summary 2011Ronel CadelinoNo ratings yet

- San Carlos City Water District Executive Summary 2016Document5 pagesSan Carlos City Water District Executive Summary 2016Mary Grace MaticNo ratings yet

- SurigaoDelNorte ES2010Document5 pagesSurigaoDelNorte ES2010J JaNo ratings yet

- 01-TalisayCity2012 Audit ReportDocument147 pages01-TalisayCity2012 Audit ReportGilbert Dela Serna IINo ratings yet

- Malimono SDN ES2018Document10 pagesMalimono SDN ES2018Joseph Raymund BautistaNo ratings yet

- 10-COA2017 Part3-Status of PYs RecommDocument24 pages10-COA2017 Part3-Status of PYs RecommjoevincentgrisolaNo ratings yet

- Commission On Audit National Government Sector Cluster 1 - Executive OfficesDocument2 pagesCommission On Audit National Government Sector Cluster 1 - Executive OfficesEmosNo ratings yet

- Ruben G. Tecson: Independent Auditor'S ReportDocument5 pagesRuben G. Tecson: Independent Auditor'S Reportfranchesca marie t. uyNo ratings yet

- 03-AuroraWD2018 Executive SummaryDocument5 pages03-AuroraWD2018 Executive SummaryEG ReyesNo ratings yet

- Malabang Executive Summary 2018Document5 pagesMalabang Executive Summary 2018Evan LoirtNo ratings yet

- Mastering Bookkeeping: Unveiling the Key to Financial SuccessFrom EverandMastering Bookkeeping: Unveiling the Key to Financial SuccessNo ratings yet

- QMS Summary MSD NCsDocument29 pagesQMS Summary MSD NCsLeo Artemio PuertosNo ratings yet

- Customer Statement-C200015165-31 Jul 23Document1 pageCustomer Statement-C200015165-31 Jul 23Leo Artemio PuertosNo ratings yet

- Exam Schedule 2nd SemDocument23 pagesExam Schedule 2nd SemLeo Artemio PuertosNo ratings yet

- No. 129595, January 31, 2000) : Rule 76 Allowance or Disallowance of WillDocument1 pageNo. 129595, January 31, 2000) : Rule 76 Allowance or Disallowance of WillLeo Artemio PuertosNo ratings yet

- Prov Rem TSN Part 2Document44 pagesProv Rem TSN Part 2Leo Artemio PuertosNo ratings yet

- ACC311Document9 pagesACC311Leo Artemio PuertosNo ratings yet

- NCA AnalysisDocument1 pageNCA AnalysisLeo Artemio PuertosNo ratings yet

- Natres Digest 2018Document26 pagesNatres Digest 2018Leo Artemio PuertosNo ratings yet

- Spec Pro TSNDocument18 pagesSpec Pro TSNLeo Artemio PuertosNo ratings yet

- Cong. Hermilando Mandanas, Et - Al Vs Executive Secretary Ochoa (GR No. 199802, July 03, 2018)Document8 pagesCong. Hermilando Mandanas, Et - Al Vs Executive Secretary Ochoa (GR No. 199802, July 03, 2018)Leo Artemio PuertosNo ratings yet

- Election Law CaselistDocument3 pagesElection Law CaselistLeo Artemio PuertosNo ratings yet

- Case Digest Acop v. PirasoDocument1 pageCase Digest Acop v. PirasoLeo Artemio PuertosNo ratings yet

- SpecPro Final Exam Coverage TSN 1Document74 pagesSpecPro Final Exam Coverage TSN 1Leo Artemio PuertosNo ratings yet

- Jose Maria College Criminal Law I Review Course Syllabus Week 7 Modification and Extinction of Criminal LiabilityDocument2 pagesJose Maria College Criminal Law I Review Course Syllabus Week 7 Modification and Extinction of Criminal LiabilityLeo Artemio PuertosNo ratings yet

- Caballero v. Commission On Elections G.R. No. 209835 FactsDocument8 pagesCaballero v. Commission On Elections G.R. No. 209835 FactsLeo Artemio PuertosNo ratings yet

- ReportDocument115 pagesReportSamNo ratings yet

- Requirements FOR PAS 701: Key Audit MattersDocument3 pagesRequirements FOR PAS 701: Key Audit MattersRenella Dane H PinedaNo ratings yet

- RESA AT PreWeek (B43)Document7 pagesRESA AT PreWeek (B43)MellaniNo ratings yet

- Kotak Bank Annual ReportDocument196 pagesKotak Bank Annual ReportCaCs Piyush SarupriaNo ratings yet

- 1 - Overview of AuditingDocument13 pages1 - Overview of AuditingZooeyNo ratings yet

- PT Barito Pacific TBK - Fy 2020Document210 pagesPT Barito Pacific TBK - Fy 2020Muhammad MuhammadNo ratings yet

- P4 - Fraud and ErrorDocument19 pagesP4 - Fraud and ErrorHaNguyenNo ratings yet

- Auditing Theory Cabrera 2010 Chap 2Document8 pagesAuditing Theory Cabrera 2010 Chap 2Squishy potatoNo ratings yet

- Internal AuditingDocument4 pagesInternal Auditingsyahirah zulkarnaenNo ratings yet

- The Impact of Audit Quality On The Financial Performance of Listed Companies NigeriaDocument6 pagesThe Impact of Audit Quality On The Financial Performance of Listed Companies NigeriaKathlyn BrawleyNo ratings yet

- AAA Webinar 6 Semester 1 2020 For DownloadDocument38 pagesAAA Webinar 6 Semester 1 2020 For DownloadPeggy ChuNo ratings yet

- Mis and Cost AuditDocument12 pagesMis and Cost AuditFarhanAhmedChowdharyNo ratings yet

- LLP Agreement (As Per Section 23 (4) of LLP Act, 2008)Document19 pagesLLP Agreement (As Per Section 23 (4) of LLP Act, 2008)rishabh raj singh bhadwariyaNo ratings yet

- CA IPCC Auditing Suggested Answer Nov 2015Document12 pagesCA IPCC Auditing Suggested Answer Nov 2015Siva Narayana Phani MouliNo ratings yet

- Chapter 3 One Audit PlanningDocument36 pagesChapter 3 One Audit PlanningTesfaye DesalegnNo ratings yet

- Audit and Assurance: Solutions Manual To AccompanyDocument7 pagesAudit and Assurance: Solutions Manual To AccompanyTooshrinaNo ratings yet

- Memory Based MCQ'S of Ca - Ipcc May-19 ExamDocument5 pagesMemory Based MCQ'S of Ca - Ipcc May-19 Examvitika pandeyNo ratings yet

- Booths 2023 Companies - House - DocumentDocument46 pagesBooths 2023 Companies - House - DocumenttuyreNo ratings yet

- The Audit ProcessDocument31 pagesThe Audit ProcessRay Jhon Ortiz100% (1)

- Waste ManagementDocument3 pagesWaste ManagementAgenttZeeroOutsiderNo ratings yet

- Sample Auditor LetterDocument1 pageSample Auditor Letternithyasree1994No ratings yet

- At 9201Document12 pagesAt 9201Shefannie PaynanteNo ratings yet

- Balance SheetDocument28 pagesBalance SheetbosemahatmaNo ratings yet

- Talbot SlidesCarnivalDocument38 pagesTalbot SlidesCarnivalLester Glenn LimheyaNo ratings yet

- Audit of Banks 1 2Document10 pagesAudit of Banks 1 2Khrisstal BalatbatNo ratings yet

- DasdsaDocument3 pagesDasdsaCleinJonTiuNo ratings yet

- Auuditing Theory CHAPTER 1 5Document16 pagesAuuditing Theory CHAPTER 1 5Dummy GoogleNo ratings yet

- Kunci Jawaban Module 1-4Document10 pagesKunci Jawaban Module 1-4meyyNo ratings yet

- Ra 9520Document6 pagesRa 9520John Michael BabasNo ratings yet

- AuditingDocument19 pagesAuditingEliza BethNo ratings yet

Download as pdf or txt

You might also like

- CS Form No. 6 Revised 2020 Application For Leave Fillable 1Document2 pagesCS Form No. 6 Revised 2020 Application For Leave Fillable 1Leo Artemio PuertosNo ratings yet

- Commission On Audit Office of The Regional Director Regional Office No. IDocument6 pagesCommission On Audit Office of The Regional Director Regional Office No. IEG ReyesNo ratings yet

- 02-PSU2016 Transmittal Letter To Board Of-RegentsDocument2 pages02-PSU2016 Transmittal Letter To Board Of-Regentsjaymark camachoNo ratings yet

- IliganCity2018 Audit ReportDocument378 pagesIliganCity2018 Audit ReportYak IvonNo ratings yet

- 01-LapulapuCity2012 Audit ReportDocument83 pages01-LapulapuCity2012 Audit ReportnelggkramNo ratings yet

- BinalonanWD-R1 ES2018Document4 pagesBinalonanWD-R1 ES2018J JaNo ratings yet

- Moalboal Executive Summary 2018Document5 pagesMoalboal Executive Summary 2018Reyna YlenaNo ratings yet

- NFC 2019Document73 pagesNFC 2019Catherine AgyaoNo ratings yet

- BAAR 2016-2017 - AwihaoDocument43 pagesBAAR 2016-2017 - AwihaoJerwin Cases Tiamson100% (1)

- Transmittal NewDocument4 pagesTransmittal NewAbraham JunioNo ratings yet

- 01 TC2018 Audit Report ADocument114 pages01 TC2018 Audit Report AJerwin Cases TiamsonNo ratings yet

- 05 DILG2017 Part1 Auditor's ReportDocument3 pages05 DILG2017 Part1 Auditor's ReportbolNo ratings yet

- Lingayen Water District Executive Summary 2016Document4 pagesLingayen Water District Executive Summary 2016Paul De LeonNo ratings yet

- Annual Audit Report: Republic of The Philippines Regional Office No. XIII Butuan CityDocument34 pagesAnnual Audit Report: Republic of The Philippines Regional Office No. XIII Butuan Citysandra bolokNo ratings yet

- Binalonan Water District Pangasinan Executive Summary 2019Document4 pagesBinalonan Water District Pangasinan Executive Summary 2019Glen CastroNo ratings yet

- Part I - Audited Financial StatementsDocument3 pagesPart I - Audited Financial Statementssandra bolokNo ratings yet

- Taytay09 Audit ReportDocument57 pagesTaytay09 Audit ReportIpah L. SaidNo ratings yet

- Hinigaran2017 Audit ReportDocument146 pagesHinigaran2017 Audit ReportChito BarsabalNo ratings yet

- 03-PSU2016 Transmittal Letter To The PresidentDocument2 pages03-PSU2016 Transmittal Letter To The Presidentjaymark camachoNo ratings yet

- Lugait Executive Summary 2018Document4 pagesLugait Executive Summary 2018OZ La NB AnamiNo ratings yet

- San Miguel Executive Summary 2011Document12 pagesSan Miguel Executive Summary 2011Justine CastilloNo ratings yet

- 01-Anda2015 Audit ReportDocument92 pages01-Anda2015 Audit ReportoabeljeanmoniqueNo ratings yet

- 2017 Internal Auditor ReportDocument3 pages2017 Internal Auditor ReportMicka EllahNo ratings yet

- Taytay Water District Executive Summary 2018Document6 pagesTaytay Water District Executive Summary 2018Allan SobrepeñaNo ratings yet

- PantaoRagatMun2017 Audit ReportDocument90 pagesPantaoRagatMun2017 Audit ReportMubarrach MatabalaoNo ratings yet

- Metro Kidapawan Water District Kidapawan City Executive Summary 2021Document6 pagesMetro Kidapawan Water District Kidapawan City Executive Summary 2021PaulDanielDeLeonNo ratings yet

- Cabadbaran City Executive Summary 2011Document4 pagesCabadbaran City Executive Summary 2011Frannie PastorNo ratings yet

- 01-Mun of Himamaylan09 Audit Report - COA ANNUAL AUDIT REPORT 2009Document50 pages01-Mun of Himamaylan09 Audit Report - COA ANNUAL AUDIT REPORT 2009himamaylancitywatchNo ratings yet

- Executive Summary: Highlights of Financial OperationsDocument12 pagesExecutive Summary: Highlights of Financial OperationsJaniceNo ratings yet

- 01-LBP2016 Transmittal LettersDocument6 pages01-LBP2016 Transmittal LettersADRIAN 18No ratings yet

- Rizal Executive Summary 2015Document4 pagesRizal Executive Summary 2015Sittie RahmaNo ratings yet

- Commission On Audit Local Government Sector: Republic of The PhilippinesDocument2 pagesCommission On Audit Local Government Sector: Republic of The PhilippinesJonson PalmaresNo ratings yet

- Motiong Executive Summary 2017Document7 pagesMotiong Executive Summary 2017Ronel CadelinoNo ratings yet

- San Agustin Executive Summary 2018Document4 pagesSan Agustin Executive Summary 2018minds2magicNo ratings yet

- CamiguinProv2018 Audit ReportDocument159 pagesCamiguinProv2018 Audit ReporthazelNo ratings yet

- Agusan Del Sur Executive Summary 2018Document8 pagesAgusan Del Sur Executive Summary 2018Sittie Fatma ReporsNo ratings yet

- Commission On AuditDocument2 pagesCommission On AuditJerome MangundayaoNo ratings yet

- 01-Minglanilla2014 Audit ReportDocument45 pages01-Minglanilla2014 Audit ReportZarah Mae UmaliNo ratings yet

- Part Ii - Detailed Observations and RecommendationsDocument16 pagesPart Ii - Detailed Observations and RecommendationsAlicia NhsNo ratings yet

- KalingaProv ES2015Document4 pagesKalingaProv ES2015J JaNo ratings yet

- Northern Kabuntalan Executive Summary 2018Document4 pagesNorthern Kabuntalan Executive Summary 2018Angelo GuevarraNo ratings yet

- Cordon Isabela ES2018Document5 pagesCordon Isabela ES2018MelvinBuyagawonNo ratings yet

- QuezonMetropolitanWD2017 Audit Report PDFDocument196 pagesQuezonMetropolitanWD2017 Audit Report PDFJojoMagnoNo ratings yet

- Baar LabelDocument61 pagesBaar LabelJerwin Cases TiamsonNo ratings yet

- 05 PUP2017 Part1 Auditors ReportDocument3 pages05 PUP2017 Part1 Auditors ReportLet it beNo ratings yet

- Titay ZS ES2016Document5 pagesTitay ZS ES2016J JaNo ratings yet

- 01-Angadanan2020 Transmittal LettersDocument14 pages01-Angadanan2020 Transmittal LettersAlicia NhsNo ratings yet

- Anda Executive Summary 2010Document5 pagesAnda Executive Summary 2010Henry AunzoNo ratings yet

- Commission On Audit: Management's Responsibility For The Financial StatementsDocument3 pagesCommission On Audit: Management's Responsibility For The Financial StatementsVinNo ratings yet

- Lapu Lapu City Executive Summary 2018Document110 pagesLapu Lapu City Executive Summary 2018mharaynel.afableNo ratings yet

- Magallanes Executive Summary 2011Document5 pagesMagallanes Executive Summary 2011Ronel CadelinoNo ratings yet

- San Carlos City Water District Executive Summary 2016Document5 pagesSan Carlos City Water District Executive Summary 2016Mary Grace MaticNo ratings yet

- SurigaoDelNorte ES2010Document5 pagesSurigaoDelNorte ES2010J JaNo ratings yet

- 01-TalisayCity2012 Audit ReportDocument147 pages01-TalisayCity2012 Audit ReportGilbert Dela Serna IINo ratings yet

- Malimono SDN ES2018Document10 pagesMalimono SDN ES2018Joseph Raymund BautistaNo ratings yet

- 10-COA2017 Part3-Status of PYs RecommDocument24 pages10-COA2017 Part3-Status of PYs RecommjoevincentgrisolaNo ratings yet

- Commission On Audit National Government Sector Cluster 1 - Executive OfficesDocument2 pagesCommission On Audit National Government Sector Cluster 1 - Executive OfficesEmosNo ratings yet

- Ruben G. Tecson: Independent Auditor'S ReportDocument5 pagesRuben G. Tecson: Independent Auditor'S Reportfranchesca marie t. uyNo ratings yet

- 03-AuroraWD2018 Executive SummaryDocument5 pages03-AuroraWD2018 Executive SummaryEG ReyesNo ratings yet

- Malabang Executive Summary 2018Document5 pagesMalabang Executive Summary 2018Evan LoirtNo ratings yet

- Mastering Bookkeeping: Unveiling the Key to Financial SuccessFrom EverandMastering Bookkeeping: Unveiling the Key to Financial SuccessNo ratings yet

- QMS Summary MSD NCsDocument29 pagesQMS Summary MSD NCsLeo Artemio PuertosNo ratings yet

- Customer Statement-C200015165-31 Jul 23Document1 pageCustomer Statement-C200015165-31 Jul 23Leo Artemio PuertosNo ratings yet

- Exam Schedule 2nd SemDocument23 pagesExam Schedule 2nd SemLeo Artemio PuertosNo ratings yet

- No. 129595, January 31, 2000) : Rule 76 Allowance or Disallowance of WillDocument1 pageNo. 129595, January 31, 2000) : Rule 76 Allowance or Disallowance of WillLeo Artemio PuertosNo ratings yet

- Prov Rem TSN Part 2Document44 pagesProv Rem TSN Part 2Leo Artemio PuertosNo ratings yet

- ACC311Document9 pagesACC311Leo Artemio PuertosNo ratings yet

- NCA AnalysisDocument1 pageNCA AnalysisLeo Artemio PuertosNo ratings yet

- Natres Digest 2018Document26 pagesNatres Digest 2018Leo Artemio PuertosNo ratings yet

- Spec Pro TSNDocument18 pagesSpec Pro TSNLeo Artemio PuertosNo ratings yet

- Cong. Hermilando Mandanas, Et - Al Vs Executive Secretary Ochoa (GR No. 199802, July 03, 2018)Document8 pagesCong. Hermilando Mandanas, Et - Al Vs Executive Secretary Ochoa (GR No. 199802, July 03, 2018)Leo Artemio PuertosNo ratings yet

- Election Law CaselistDocument3 pagesElection Law CaselistLeo Artemio PuertosNo ratings yet

- Case Digest Acop v. PirasoDocument1 pageCase Digest Acop v. PirasoLeo Artemio PuertosNo ratings yet

- SpecPro Final Exam Coverage TSN 1Document74 pagesSpecPro Final Exam Coverage TSN 1Leo Artemio PuertosNo ratings yet

- Jose Maria College Criminal Law I Review Course Syllabus Week 7 Modification and Extinction of Criminal LiabilityDocument2 pagesJose Maria College Criminal Law I Review Course Syllabus Week 7 Modification and Extinction of Criminal LiabilityLeo Artemio PuertosNo ratings yet

- Caballero v. Commission On Elections G.R. No. 209835 FactsDocument8 pagesCaballero v. Commission On Elections G.R. No. 209835 FactsLeo Artemio PuertosNo ratings yet

- ReportDocument115 pagesReportSamNo ratings yet

- Requirements FOR PAS 701: Key Audit MattersDocument3 pagesRequirements FOR PAS 701: Key Audit MattersRenella Dane H PinedaNo ratings yet

- RESA AT PreWeek (B43)Document7 pagesRESA AT PreWeek (B43)MellaniNo ratings yet

- Kotak Bank Annual ReportDocument196 pagesKotak Bank Annual ReportCaCs Piyush SarupriaNo ratings yet

- 1 - Overview of AuditingDocument13 pages1 - Overview of AuditingZooeyNo ratings yet

- PT Barito Pacific TBK - Fy 2020Document210 pagesPT Barito Pacific TBK - Fy 2020Muhammad MuhammadNo ratings yet

- P4 - Fraud and ErrorDocument19 pagesP4 - Fraud and ErrorHaNguyenNo ratings yet

- Auditing Theory Cabrera 2010 Chap 2Document8 pagesAuditing Theory Cabrera 2010 Chap 2Squishy potatoNo ratings yet

- Internal AuditingDocument4 pagesInternal Auditingsyahirah zulkarnaenNo ratings yet

- The Impact of Audit Quality On The Financial Performance of Listed Companies NigeriaDocument6 pagesThe Impact of Audit Quality On The Financial Performance of Listed Companies NigeriaKathlyn BrawleyNo ratings yet

- AAA Webinar 6 Semester 1 2020 For DownloadDocument38 pagesAAA Webinar 6 Semester 1 2020 For DownloadPeggy ChuNo ratings yet

- Mis and Cost AuditDocument12 pagesMis and Cost AuditFarhanAhmedChowdharyNo ratings yet

- LLP Agreement (As Per Section 23 (4) of LLP Act, 2008)Document19 pagesLLP Agreement (As Per Section 23 (4) of LLP Act, 2008)rishabh raj singh bhadwariyaNo ratings yet

- CA IPCC Auditing Suggested Answer Nov 2015Document12 pagesCA IPCC Auditing Suggested Answer Nov 2015Siva Narayana Phani MouliNo ratings yet

- Chapter 3 One Audit PlanningDocument36 pagesChapter 3 One Audit PlanningTesfaye DesalegnNo ratings yet

- Audit and Assurance: Solutions Manual To AccompanyDocument7 pagesAudit and Assurance: Solutions Manual To AccompanyTooshrinaNo ratings yet

- Memory Based MCQ'S of Ca - Ipcc May-19 ExamDocument5 pagesMemory Based MCQ'S of Ca - Ipcc May-19 Examvitika pandeyNo ratings yet

- Booths 2023 Companies - House - DocumentDocument46 pagesBooths 2023 Companies - House - DocumenttuyreNo ratings yet

- The Audit ProcessDocument31 pagesThe Audit ProcessRay Jhon Ortiz100% (1)

- Waste ManagementDocument3 pagesWaste ManagementAgenttZeeroOutsiderNo ratings yet

- Sample Auditor LetterDocument1 pageSample Auditor Letternithyasree1994No ratings yet

- At 9201Document12 pagesAt 9201Shefannie PaynanteNo ratings yet

- Balance SheetDocument28 pagesBalance SheetbosemahatmaNo ratings yet

- Talbot SlidesCarnivalDocument38 pagesTalbot SlidesCarnivalLester Glenn LimheyaNo ratings yet

- Audit of Banks 1 2Document10 pagesAudit of Banks 1 2Khrisstal BalatbatNo ratings yet

- DasdsaDocument3 pagesDasdsaCleinJonTiuNo ratings yet

- Auuditing Theory CHAPTER 1 5Document16 pagesAuuditing Theory CHAPTER 1 5Dummy GoogleNo ratings yet

- Kunci Jawaban Module 1-4Document10 pagesKunci Jawaban Module 1-4meyyNo ratings yet

- Ra 9520Document6 pagesRa 9520John Michael BabasNo ratings yet

- AuditingDocument19 pagesAuditingEliza BethNo ratings yet