EA EA2 SU3 Outline

EA EA2 SU3 Outline

You might also like

- Accounting For Income TaxesDocument17 pagesAccounting For Income TaxesKenn Adam Johan Gajudo70% (10)

- Norsk Standard Kontoplan Prevod ENGDocument25 pagesNorsk Standard Kontoplan Prevod ENGMladenPetkovićNo ratings yet

- Legit LLC Seller PermitDocument1 pageLegit LLC Seller PermitAly BenNo ratings yet

- Quiz Bee - Leases (With Ans)Document3 pagesQuiz Bee - Leases (With Ans)Richard Sarra Mantilla88% (8)

- Lecture Week 5Document56 pagesLecture Week 5朱潇妤100% (1)

- Lease Financing PDFDocument31 pagesLease Financing PDFreshma100% (5)

- ACC226 Lease AccountingDocument18 pagesACC226 Lease AccountingJaneth Barrete100% (2)

- NAS 17 LeasesDocument16 pagesNAS 17 LeasesbinuNo ratings yet

- Lease PART 1 and 2Document6 pagesLease PART 1 and 2shadowlord468No ratings yet

- LEASESDocument5 pagesLEASESHappy MagdangalNo ratings yet

- 07 Income From Property (50 59)Document11 pages07 Income From Property (50 59)jafferyasim100% (2)

- Module 1 LeasesDocument12 pagesModule 1 LeasesMon RamNo ratings yet

- LeasesDocument5 pagesLeasesElla Montefalco50% (2)

- Lecture Outline: Part A: Identifying A Lease Arrangement, Lease Versus Non-Lease Components, and Lease TermDocument6 pagesLecture Outline: Part A: Identifying A Lease Arrangement, Lease Versus Non-Lease Components, and Lease TermDivine CuasayNo ratings yet

- Module 8-OPERATING LESSEE-LESSORDocument5 pagesModule 8-OPERATING LESSEE-LESSORJeanivyle CarmonaNo ratings yet

- Property Income - July 2023Document5 pagesProperty Income - July 2023maharajabby81No ratings yet

- Ch. 6Document11 pagesCh. 6Ali nawazNo ratings yet

- Fair RentDocument19 pagesFair RentProf. Vandana Tiwari SrivastavaNo ratings yet

- Chapter 13 LeasesDocument4 pagesChapter 13 LeasesAngelica Joy ManaoisNo ratings yet

- (uploadMB - Com) 18 - House PropertyDocument22 pages(uploadMB - Com) 18 - House PropertyhariomnarayanNo ratings yet

- IA2 LIABILITIES p4 Lease VDocument33 pagesIA2 LIABILITIES p4 Lease VAzaria MatiasNo ratings yet

- IntAcc 2 - CHAPTER 12 NotesDocument4 pagesIntAcc 2 - CHAPTER 12 NotesikiNo ratings yet

- Leases 23022024 025635pmDocument14 pagesLeases 23022024 025635pmMaham TurkNo ratings yet

- ACCO 20103 Notes 4 IFRS 16 (Leases) Notes Part IIDocument5 pagesACCO 20103 Notes 4 IFRS 16 (Leases) Notes Part IIVincent Luigil AlceraNo ratings yet

- LeaseDocument8 pagesLeaseAlyssa AnnNo ratings yet

- Term Paper # 1. Definition and Meaning of Lease FinancingDocument16 pagesTerm Paper # 1. Definition and Meaning of Lease FinancingAniket PuriNo ratings yet

- Accounting For Leases Fra 2012Document8 pagesAccounting For Leases Fra 2012Srishti ShawNo ratings yet

- Income From HP PDFDocument14 pagesIncome From HP PDFNanda NanduNo ratings yet

- LEASESDocument46 pagesLEASESdantekailey9No ratings yet

- 15) IFRS-16 IBCOM-FinalDocument20 pages15) IFRS-16 IBCOM-Finalmanvi jainNo ratings yet

- Leases ExercisessDocument6 pagesLeases ExercisessdorothyannvillamoraaNo ratings yet

- PDF Quiz Bee Leases With Ans Copy - CompressDocument3 pagesPDF Quiz Bee Leases With Ans Copy - CompressGarp BarrocaNo ratings yet

- Rent Control Law 2Document28 pagesRent Control Law 2Cari Mangalindan MacaalayNo ratings yet

- S021 - Haroon Shaik DIT AssignmentDocument10 pagesS021 - Haroon Shaik DIT AssignmentHaroonNo ratings yet

- 1644473426SLFRS 16 - Part 2Document8 pages1644473426SLFRS 16 - Part 2mg21138No ratings yet

- Part - 1 - Dashboard - LeasesDocument4 pagesPart - 1 - Dashboard - LeasesbagayaobNo ratings yet

- LEASESDocument12 pagesLEASESIrvin OngyacoNo ratings yet

- LEASES Notes and Illustrations For The StudentsDocument4 pagesLEASES Notes and Illustrations For The StudentsEmmanuelNo ratings yet

- 4222 CH 20 Slides From PDFDocument17 pages4222 CH 20 Slides From PDFAn NaNo ratings yet

- Lesson 2 LeaseDocument26 pagesLesson 2 Leaselil telNo ratings yet

- Pre-Exam Marathon 3 - House Property, Capital Gains, IFOS, Salaries, PGBP, TDS, TCS, Advance Tax, PDFDocument106 pagesPre-Exam Marathon 3 - House Property, Capital Gains, IFOS, Salaries, PGBP, TDS, TCS, Advance Tax, PDFParmeet NainNo ratings yet

- AS 19 Accounting For LeasesDocument5 pagesAS 19 Accounting For LeasesRemeshNo ratings yet

- LEASE FINANCINGDocument10 pagesLEASE FINANCINGcliffton malcolm tshumaNo ratings yet

- 21 ChapterDocument30 pages21 Chapteribrahim javedNo ratings yet

- PDF Document AB2D94598B09 1Document28 pagesPDF Document AB2D94598B09 120BRM051 Sukant SNo ratings yet

- 3 1+Lessee+AccountingDocument46 pages3 1+Lessee+AccountingKate ParanaNo ratings yet

- Chapter 21 (Group 2)Document20 pagesChapter 21 (Group 2)Josua PranataNo ratings yet

- Int.-Acctg.-3 Valix2019 Chapter28Document25 pagesInt.-Acctg.-3 Valix2019 Chapter28Toni Rose Hernandez LualhatiNo ratings yet

- Leases StudentsDocument5 pagesLeases StudentsRaezel Carla Santos FontanillaNo ratings yet

- Gov - of.AB - Rental - Security - DepositDocument8 pagesGov - of.AB - Rental - Security - DepositLeslie CrapoNo ratings yet

- Baf 223 Accounting For Liabilities - Accounting For LeasesDocument8 pagesBaf 223 Accounting For Liabilities - Accounting For Leasesaroridouglas880No ratings yet

- FRS117 SlidesDocument38 pagesFRS117 SlidesjaywymNo ratings yet

- Income Approach To ValuationDocument35 pagesIncome Approach To Valuation054 Modi TanviNo ratings yet

- Financial Services 2Document21 pagesFinancial Services 2Uma NNo ratings yet

- CH 12 Operating Lease - LessorDocument2 pagesCH 12 Operating Lease - LessorGenebabe LoquiasNo ratings yet

- Non Banking Financial Institutions: by Sudev Jyothisi FN-92 Scms-CochinDocument18 pagesNon Banking Financial Institutions: by Sudev Jyothisi FN-92 Scms-CochinSUDEVJYOTHISINo ratings yet

- LEASESDocument5 pagesLEASESsino akoNo ratings yet

- Lease - Lessee's Perspective: Lecture NotesDocument9 pagesLease - Lessee's Perspective: Lecture NotesDonise Ronadel SantosNo ratings yet

- Lease Financing: Learning OutcomesDocument31 pagesLease Financing: Learning Outcomesravi sharma100% (1)

- New Final Updated IFRS 16Document98 pagesNew Final Updated IFRS 16murshidalbimaanyNo ratings yet

- Chapter 8 Leases Part 2Document14 pagesChapter 8 Leases Part 2maria isabellaNo ratings yet

- Ankit Thakur Assistant Professor Civil EngineeringDocument53 pagesAnkit Thakur Assistant Professor Civil EngineeringAditiNo ratings yet

- Relieving Letter FormatDocument1 pageRelieving Letter FormatAdil AliNo ratings yet

- Types of Product CostsDocument1 pageTypes of Product CostsAdil AliNo ratings yet

- Ea Ea2 Su19 OutlineDocument17 pagesEa Ea2 Su19 OutlineAdil AliNo ratings yet

- Ea Ea3 Su7 OutlineDocument18 pagesEa Ea3 Su7 OutlineAdil AliNo ratings yet

- Investigatory Project On The Contents of ColdrinksDocument1 pageInvestigatory Project On The Contents of ColdrinksAdil AliNo ratings yet

- Analytical Issue in in Financial Accounting Q&A 20Document1 pageAnalytical Issue in in Financial Accounting Q&A 20Adil AliNo ratings yet

- Ea Ea2 Su10 OutlineDocument16 pagesEa Ea2 Su10 OutlineAdil AliNo ratings yet

- Process Improvement ToolsDocument4 pagesProcess Improvement ToolsAdil AliNo ratings yet

- Error in Inventory ExampleDocument1 pageError in Inventory ExampleAdil AliNo ratings yet

- Financial Instruments and Cost of CapitalDocument2 pagesFinancial Instruments and Cost of CapitalAdil AliNo ratings yet

- Sailboad QuestionDocument6 pagesSailboad QuestionAdil AliNo ratings yet

- Accounting For InvestmentDocument1 pageAccounting For InvestmentAdil AliNo ratings yet

- Comprehensive Income Statement ExampleDocument1 pageComprehensive Income Statement ExampleAdil AliNo ratings yet

- The Master Budget ProcessDocument1 pageThe Master Budget ProcessAdil AliNo ratings yet

- Financial Statement AnalysisDocument1 pageFinancial Statement AnalysisAdil AliNo ratings yet

- Accounting For Investments in Debt SecuritiesDocument1 pageAccounting For Investments in Debt SecuritiesAdil AliNo ratings yet

- Accounting For Investment ExampleDocument1 pageAccounting For Investment ExampleAdil AliNo ratings yet

- CBSE 2015 Syllabus 12 Accountancy NewDocument5 pagesCBSE 2015 Syllabus 12 Accountancy NewAdil AliNo ratings yet

- Chicken Jalfrezi Recipe by Sanjeev KapoorDocument1 pageChicken Jalfrezi Recipe by Sanjeev KapoorAdil AliNo ratings yet

- Anuj Aggarwal GST DetailsDocument5 pagesAnuj Aggarwal GST DetailsDeepak DahiyaNo ratings yet

- IT-AE-41-G02 - Guide To Complete The Tax Directive Application Forms - External GuideDocument50 pagesIT-AE-41-G02 - Guide To Complete The Tax Directive Application Forms - External GuidercpretoriusNo ratings yet

- HP MouseDocument1 pageHP MousevishwanathNo ratings yet

- Unaccounted DepositsDocument2 pagesUnaccounted DepositsJonabelle BiliganNo ratings yet

- CIR vs. Magsaysay LinesDocument1 pageCIR vs. Magsaysay Lineskaira marie carlosNo ratings yet

- Deposit Slip For Bank: Amount Advance Tax Sales Tax/Excise Duty Total (RS.)Document2 pagesDeposit Slip For Bank: Amount Advance Tax Sales Tax/Excise Duty Total (RS.)Muhammad IrfanNo ratings yet

- Einv 1Document1 pageEinv 1Tarun DiwakarNo ratings yet

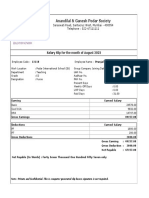

- Anandilal & Ganesh Podar Society: Salary Slip For The Month of August 2022Document1 pageAnandilal & Ganesh Podar Society: Salary Slip For The Month of August 2022Pradnyesh GuramNo ratings yet

- 3 DR KBL MathurDocument31 pages3 DR KBL MathurAkhilesh MishraNo ratings yet

- Train LawDocument2 pagesTrain LawMicah AtienzaNo ratings yet

- Financial Affidavit BlankDocument10 pagesFinancial Affidavit BlankNicole FloresNo ratings yet

- Chapter 4 To 6Document32 pagesChapter 4 To 6solomonaauNo ratings yet

- Court of Tax Appeals Quezon City: Second DivisionDocument49 pagesCourt of Tax Appeals Quezon City: Second DivisionJomel ManaigNo ratings yet

- Commission Structure & Earning Potential - GST Suvidha Kendra PDFDocument4 pagesCommission Structure & Earning Potential - GST Suvidha Kendra PDFvikasNo ratings yet

- YyreDocument22 pagesYyresri gadis wulandariNo ratings yet

- Aguinaldo Industries v. CIRDocument1 pageAguinaldo Industries v. CIRTon Ton CananeaNo ratings yet

- IRAS E-Tax Guide: Deductibility of "Keyman" Insurance PremiumsDocument8 pagesIRAS E-Tax Guide: Deductibility of "Keyman" Insurance PremiumsSampath VimalaNo ratings yet

- General Principles of TaxationDocument58 pagesGeneral Principles of TaxationMarriz Bustaliño TanNo ratings yet

- Mepco Full BillDocument1 pageMepco Full Billfaheemhashmi7050No ratings yet

- Amarylis Putri - KERTAS KERJA JURNAL - Sent2Document6 pagesAmarylis Putri - KERTAS KERJA JURNAL - Sent2SatriaArdya10No ratings yet

- BCom Business Taxation Income Tax and Sales Tax Numerical 2018Document5 pagesBCom Business Taxation Income Tax and Sales Tax Numerical 2018AHSAN LASHARINo ratings yet

- Sre 2022 and 2023Document4 pagesSre 2022 and 2023barangaymaharlikawest017No ratings yet

- Chapter 11 Current LiabilitiesDocument51 pagesChapter 11 Current LiabilitiesMuhammad DanishNo ratings yet

- RMO No. 14-2021 - DigestDocument3 pagesRMO No. 14-2021 - DigestMike Ferdinand SantosNo ratings yet

- 1st Exam Income TaxDocument8 pages1st Exam Income TaxCrystal Jenn BalabaNo ratings yet

- Introduction To Goods and Services Tax (GST)Document7 pagesIntroduction To Goods and Services Tax (GST)Anjali PawarNo ratings yet

- GST - Unit 2 (Illustration Sums)Document10 pagesGST - Unit 2 (Illustration Sums)subash minecraft creatorNo ratings yet

Download as pdf or txt

You might also like

- Accounting For Income TaxesDocument17 pagesAccounting For Income TaxesKenn Adam Johan Gajudo70% (10)

- Norsk Standard Kontoplan Prevod ENGDocument25 pagesNorsk Standard Kontoplan Prevod ENGMladenPetkovićNo ratings yet

- Legit LLC Seller PermitDocument1 pageLegit LLC Seller PermitAly BenNo ratings yet

- Quiz Bee - Leases (With Ans)Document3 pagesQuiz Bee - Leases (With Ans)Richard Sarra Mantilla88% (8)

- Lecture Week 5Document56 pagesLecture Week 5朱潇妤100% (1)

- Lease Financing PDFDocument31 pagesLease Financing PDFreshma100% (5)

- ACC226 Lease AccountingDocument18 pagesACC226 Lease AccountingJaneth Barrete100% (2)

- NAS 17 LeasesDocument16 pagesNAS 17 LeasesbinuNo ratings yet

- Lease PART 1 and 2Document6 pagesLease PART 1 and 2shadowlord468No ratings yet

- LEASESDocument5 pagesLEASESHappy MagdangalNo ratings yet

- 07 Income From Property (50 59)Document11 pages07 Income From Property (50 59)jafferyasim100% (2)

- Module 1 LeasesDocument12 pagesModule 1 LeasesMon RamNo ratings yet

- LeasesDocument5 pagesLeasesElla Montefalco50% (2)

- Lecture Outline: Part A: Identifying A Lease Arrangement, Lease Versus Non-Lease Components, and Lease TermDocument6 pagesLecture Outline: Part A: Identifying A Lease Arrangement, Lease Versus Non-Lease Components, and Lease TermDivine CuasayNo ratings yet

- Module 8-OPERATING LESSEE-LESSORDocument5 pagesModule 8-OPERATING LESSEE-LESSORJeanivyle CarmonaNo ratings yet

- Property Income - July 2023Document5 pagesProperty Income - July 2023maharajabby81No ratings yet

- Ch. 6Document11 pagesCh. 6Ali nawazNo ratings yet

- Fair RentDocument19 pagesFair RentProf. Vandana Tiwari SrivastavaNo ratings yet

- Chapter 13 LeasesDocument4 pagesChapter 13 LeasesAngelica Joy ManaoisNo ratings yet

- (uploadMB - Com) 18 - House PropertyDocument22 pages(uploadMB - Com) 18 - House PropertyhariomnarayanNo ratings yet

- IA2 LIABILITIES p4 Lease VDocument33 pagesIA2 LIABILITIES p4 Lease VAzaria MatiasNo ratings yet

- IntAcc 2 - CHAPTER 12 NotesDocument4 pagesIntAcc 2 - CHAPTER 12 NotesikiNo ratings yet

- Leases 23022024 025635pmDocument14 pagesLeases 23022024 025635pmMaham TurkNo ratings yet

- ACCO 20103 Notes 4 IFRS 16 (Leases) Notes Part IIDocument5 pagesACCO 20103 Notes 4 IFRS 16 (Leases) Notes Part IIVincent Luigil AlceraNo ratings yet

- LeaseDocument8 pagesLeaseAlyssa AnnNo ratings yet

- Term Paper # 1. Definition and Meaning of Lease FinancingDocument16 pagesTerm Paper # 1. Definition and Meaning of Lease FinancingAniket PuriNo ratings yet

- Accounting For Leases Fra 2012Document8 pagesAccounting For Leases Fra 2012Srishti ShawNo ratings yet

- Income From HP PDFDocument14 pagesIncome From HP PDFNanda NanduNo ratings yet

- LEASESDocument46 pagesLEASESdantekailey9No ratings yet

- 15) IFRS-16 IBCOM-FinalDocument20 pages15) IFRS-16 IBCOM-Finalmanvi jainNo ratings yet

- Leases ExercisessDocument6 pagesLeases ExercisessdorothyannvillamoraaNo ratings yet

- PDF Quiz Bee Leases With Ans Copy - CompressDocument3 pagesPDF Quiz Bee Leases With Ans Copy - CompressGarp BarrocaNo ratings yet

- Rent Control Law 2Document28 pagesRent Control Law 2Cari Mangalindan MacaalayNo ratings yet

- S021 - Haroon Shaik DIT AssignmentDocument10 pagesS021 - Haroon Shaik DIT AssignmentHaroonNo ratings yet

- 1644473426SLFRS 16 - Part 2Document8 pages1644473426SLFRS 16 - Part 2mg21138No ratings yet

- Part - 1 - Dashboard - LeasesDocument4 pagesPart - 1 - Dashboard - LeasesbagayaobNo ratings yet

- LEASESDocument12 pagesLEASESIrvin OngyacoNo ratings yet

- LEASES Notes and Illustrations For The StudentsDocument4 pagesLEASES Notes and Illustrations For The StudentsEmmanuelNo ratings yet

- 4222 CH 20 Slides From PDFDocument17 pages4222 CH 20 Slides From PDFAn NaNo ratings yet

- Lesson 2 LeaseDocument26 pagesLesson 2 Leaselil telNo ratings yet

- Pre-Exam Marathon 3 - House Property, Capital Gains, IFOS, Salaries, PGBP, TDS, TCS, Advance Tax, PDFDocument106 pagesPre-Exam Marathon 3 - House Property, Capital Gains, IFOS, Salaries, PGBP, TDS, TCS, Advance Tax, PDFParmeet NainNo ratings yet

- AS 19 Accounting For LeasesDocument5 pagesAS 19 Accounting For LeasesRemeshNo ratings yet

- LEASE FINANCINGDocument10 pagesLEASE FINANCINGcliffton malcolm tshumaNo ratings yet

- 21 ChapterDocument30 pages21 Chapteribrahim javedNo ratings yet

- PDF Document AB2D94598B09 1Document28 pagesPDF Document AB2D94598B09 120BRM051 Sukant SNo ratings yet

- 3 1+Lessee+AccountingDocument46 pages3 1+Lessee+AccountingKate ParanaNo ratings yet

- Chapter 21 (Group 2)Document20 pagesChapter 21 (Group 2)Josua PranataNo ratings yet

- Int.-Acctg.-3 Valix2019 Chapter28Document25 pagesInt.-Acctg.-3 Valix2019 Chapter28Toni Rose Hernandez LualhatiNo ratings yet

- Leases StudentsDocument5 pagesLeases StudentsRaezel Carla Santos FontanillaNo ratings yet

- Gov - of.AB - Rental - Security - DepositDocument8 pagesGov - of.AB - Rental - Security - DepositLeslie CrapoNo ratings yet

- Baf 223 Accounting For Liabilities - Accounting For LeasesDocument8 pagesBaf 223 Accounting For Liabilities - Accounting For Leasesaroridouglas880No ratings yet

- FRS117 SlidesDocument38 pagesFRS117 SlidesjaywymNo ratings yet

- Income Approach To ValuationDocument35 pagesIncome Approach To Valuation054 Modi TanviNo ratings yet

- Financial Services 2Document21 pagesFinancial Services 2Uma NNo ratings yet

- CH 12 Operating Lease - LessorDocument2 pagesCH 12 Operating Lease - LessorGenebabe LoquiasNo ratings yet

- Non Banking Financial Institutions: by Sudev Jyothisi FN-92 Scms-CochinDocument18 pagesNon Banking Financial Institutions: by Sudev Jyothisi FN-92 Scms-CochinSUDEVJYOTHISINo ratings yet

- LEASESDocument5 pagesLEASESsino akoNo ratings yet

- Lease - Lessee's Perspective: Lecture NotesDocument9 pagesLease - Lessee's Perspective: Lecture NotesDonise Ronadel SantosNo ratings yet

- Lease Financing: Learning OutcomesDocument31 pagesLease Financing: Learning Outcomesravi sharma100% (1)

- New Final Updated IFRS 16Document98 pagesNew Final Updated IFRS 16murshidalbimaanyNo ratings yet

- Chapter 8 Leases Part 2Document14 pagesChapter 8 Leases Part 2maria isabellaNo ratings yet

- Ankit Thakur Assistant Professor Civil EngineeringDocument53 pagesAnkit Thakur Assistant Professor Civil EngineeringAditiNo ratings yet

- Relieving Letter FormatDocument1 pageRelieving Letter FormatAdil AliNo ratings yet

- Types of Product CostsDocument1 pageTypes of Product CostsAdil AliNo ratings yet

- Ea Ea2 Su19 OutlineDocument17 pagesEa Ea2 Su19 OutlineAdil AliNo ratings yet

- Ea Ea3 Su7 OutlineDocument18 pagesEa Ea3 Su7 OutlineAdil AliNo ratings yet

- Investigatory Project On The Contents of ColdrinksDocument1 pageInvestigatory Project On The Contents of ColdrinksAdil AliNo ratings yet

- Analytical Issue in in Financial Accounting Q&A 20Document1 pageAnalytical Issue in in Financial Accounting Q&A 20Adil AliNo ratings yet

- Ea Ea2 Su10 OutlineDocument16 pagesEa Ea2 Su10 OutlineAdil AliNo ratings yet

- Process Improvement ToolsDocument4 pagesProcess Improvement ToolsAdil AliNo ratings yet

- Error in Inventory ExampleDocument1 pageError in Inventory ExampleAdil AliNo ratings yet

- Financial Instruments and Cost of CapitalDocument2 pagesFinancial Instruments and Cost of CapitalAdil AliNo ratings yet

- Sailboad QuestionDocument6 pagesSailboad QuestionAdil AliNo ratings yet

- Accounting For InvestmentDocument1 pageAccounting For InvestmentAdil AliNo ratings yet

- Comprehensive Income Statement ExampleDocument1 pageComprehensive Income Statement ExampleAdil AliNo ratings yet

- The Master Budget ProcessDocument1 pageThe Master Budget ProcessAdil AliNo ratings yet

- Financial Statement AnalysisDocument1 pageFinancial Statement AnalysisAdil AliNo ratings yet

- Accounting For Investments in Debt SecuritiesDocument1 pageAccounting For Investments in Debt SecuritiesAdil AliNo ratings yet

- Accounting For Investment ExampleDocument1 pageAccounting For Investment ExampleAdil AliNo ratings yet

- CBSE 2015 Syllabus 12 Accountancy NewDocument5 pagesCBSE 2015 Syllabus 12 Accountancy NewAdil AliNo ratings yet

- Chicken Jalfrezi Recipe by Sanjeev KapoorDocument1 pageChicken Jalfrezi Recipe by Sanjeev KapoorAdil AliNo ratings yet

- Anuj Aggarwal GST DetailsDocument5 pagesAnuj Aggarwal GST DetailsDeepak DahiyaNo ratings yet

- IT-AE-41-G02 - Guide To Complete The Tax Directive Application Forms - External GuideDocument50 pagesIT-AE-41-G02 - Guide To Complete The Tax Directive Application Forms - External GuidercpretoriusNo ratings yet

- HP MouseDocument1 pageHP MousevishwanathNo ratings yet

- Unaccounted DepositsDocument2 pagesUnaccounted DepositsJonabelle BiliganNo ratings yet

- CIR vs. Magsaysay LinesDocument1 pageCIR vs. Magsaysay Lineskaira marie carlosNo ratings yet

- Deposit Slip For Bank: Amount Advance Tax Sales Tax/Excise Duty Total (RS.)Document2 pagesDeposit Slip For Bank: Amount Advance Tax Sales Tax/Excise Duty Total (RS.)Muhammad IrfanNo ratings yet

- Einv 1Document1 pageEinv 1Tarun DiwakarNo ratings yet

- Anandilal & Ganesh Podar Society: Salary Slip For The Month of August 2022Document1 pageAnandilal & Ganesh Podar Society: Salary Slip For The Month of August 2022Pradnyesh GuramNo ratings yet

- 3 DR KBL MathurDocument31 pages3 DR KBL MathurAkhilesh MishraNo ratings yet

- Train LawDocument2 pagesTrain LawMicah AtienzaNo ratings yet

- Financial Affidavit BlankDocument10 pagesFinancial Affidavit BlankNicole FloresNo ratings yet

- Chapter 4 To 6Document32 pagesChapter 4 To 6solomonaauNo ratings yet

- Court of Tax Appeals Quezon City: Second DivisionDocument49 pagesCourt of Tax Appeals Quezon City: Second DivisionJomel ManaigNo ratings yet

- Commission Structure & Earning Potential - GST Suvidha Kendra PDFDocument4 pagesCommission Structure & Earning Potential - GST Suvidha Kendra PDFvikasNo ratings yet

- YyreDocument22 pagesYyresri gadis wulandariNo ratings yet

- Aguinaldo Industries v. CIRDocument1 pageAguinaldo Industries v. CIRTon Ton CananeaNo ratings yet

- IRAS E-Tax Guide: Deductibility of "Keyman" Insurance PremiumsDocument8 pagesIRAS E-Tax Guide: Deductibility of "Keyman" Insurance PremiumsSampath VimalaNo ratings yet

- General Principles of TaxationDocument58 pagesGeneral Principles of TaxationMarriz Bustaliño TanNo ratings yet

- Mepco Full BillDocument1 pageMepco Full Billfaheemhashmi7050No ratings yet

- Amarylis Putri - KERTAS KERJA JURNAL - Sent2Document6 pagesAmarylis Putri - KERTAS KERJA JURNAL - Sent2SatriaArdya10No ratings yet

- BCom Business Taxation Income Tax and Sales Tax Numerical 2018Document5 pagesBCom Business Taxation Income Tax and Sales Tax Numerical 2018AHSAN LASHARINo ratings yet

- Sre 2022 and 2023Document4 pagesSre 2022 and 2023barangaymaharlikawest017No ratings yet

- Chapter 11 Current LiabilitiesDocument51 pagesChapter 11 Current LiabilitiesMuhammad DanishNo ratings yet

- RMO No. 14-2021 - DigestDocument3 pagesRMO No. 14-2021 - DigestMike Ferdinand SantosNo ratings yet

- 1st Exam Income TaxDocument8 pages1st Exam Income TaxCrystal Jenn BalabaNo ratings yet

- Introduction To Goods and Services Tax (GST)Document7 pagesIntroduction To Goods and Services Tax (GST)Anjali PawarNo ratings yet

- GST - Unit 2 (Illustration Sums)Document10 pagesGST - Unit 2 (Illustration Sums)subash minecraft creatorNo ratings yet