Economics Formulas

Economics Formulas

You might also like

- Revlon Case Report - Big BossDocument32 pagesRevlon Case Report - Big BossMohd EizraNo ratings yet

- What Is National Final)Document49 pagesWhat Is National Final)Tong KakitNo ratings yet

- Stocks and Flows: Rules For Computing GDPDocument4 pagesStocks and Flows: Rules For Computing GDPEva DagusNo ratings yet

- Lesson 1 and Lesson 2Document21 pagesLesson 1 and Lesson 2Qui BuiNo ratings yet

- Concepts of Macroeconomics Lesson 1Document6 pagesConcepts of Macroeconomics Lesson 1Dj I amNo ratings yet

- Level of Sales Volume, Sales Value or Production at Which The Business Makes Neither A Profit Nor A Loss (The "Break-Even Point")Document23 pagesLevel of Sales Volume, Sales Value or Production at Which The Business Makes Neither A Profit Nor A Loss (The "Break-Even Point")Tekelemariam FitwiNo ratings yet

- Economic Growth Is Defined As TheDocument20 pagesEconomic Growth Is Defined As TheAsma ShamsNo ratings yet

- Macroeconomics: BY: Maria Deanna S. Salalima, Ed.DDocument7 pagesMacroeconomics: BY: Maria Deanna S. Salalima, Ed.DLerryNo ratings yet

- National IncomeDocument13 pagesNational IncomeMuzammil MotoorNo ratings yet

- Remigio G. TiambengDocument40 pagesRemigio G. TiambengRaissa Ericka RomanNo ratings yet

- Cross Elasticity of DemandDocument4 pagesCross Elasticity of DemandShaniya KoyaNo ratings yet

- The Fundamental Concepts of Macroeconomics: Erandathie PathirajaDocument69 pagesThe Fundamental Concepts of Macroeconomics: Erandathie PathirajaDK White LionNo ratings yet

- EC 124 Chap2 Part - II PDFDocument8 pagesEC 124 Chap2 Part - II PDFAnonymous wFIBMUmt100% (1)

- National Income and Other Social Accounts AnalysisDocument28 pagesNational Income and Other Social Accounts AnalysisJING LINo ratings yet

- Measures of National Income and OutputDocument10 pagesMeasures of National Income and OutputMohammed YunusNo ratings yet

- National IncomeDocument13 pagesNational IncomeEashwar ReddyNo ratings yet

- Presented By: Syndicate 6Document37 pagesPresented By: Syndicate 6suasiveNo ratings yet

- Lecture 3Document10 pagesLecture 3Hitisha agrawalNo ratings yet

- National Income ConceptsDocument25 pagesNational Income ConceptsAnjali ChaudharyNo ratings yet

- VIVADocument6 pagesVIVAkoushikNo ratings yet

- макра теорияDocument38 pagesмакра теорияVictoriaNo ratings yet

- МАКРАDocument11 pagesМАКРАДенис ДавшанNo ratings yet

- MacroeconomicsDocument4 pagesMacroeconomicskuashask2No ratings yet

- Fundamentals of MacroeconomicsDocument5 pagesFundamentals of MacroeconomicsElsa PucciniNo ratings yet

- Macroeconomics - MOCK TEST (Answers)Document54 pagesMacroeconomics - MOCK TEST (Answers)gr306688No ratings yet

- Total Cost in The Long-Run and The Isocost LineDocument11 pagesTotal Cost in The Long-Run and The Isocost LineSamia AfrinNo ratings yet

- Macroeconomics NotesDocument5 pagesMacroeconomics NotesJulian SerhanNo ratings yet

- Chapter 8 The Level of Overall Economic ActivityDocument8 pagesChapter 8 The Level of Overall Economic ActivityHieptaNo ratings yet

- Measures of National Income and OutputDocument6 pagesMeasures of National Income and OutputAJAYNo ratings yet

- Unit-1 - Macro TopicsDocument7 pagesUnit-1 - Macro TopicsKEERTHANA RNo ratings yet

- Macroeconomics CODE: BBF1201: Lecture: Dhanya Jagadeesh BAISAGO University CollegeDocument21 pagesMacroeconomics CODE: BBF1201: Lecture: Dhanya Jagadeesh BAISAGO University CollegeKeeme NaoNo ratings yet

- HUT300 M4 Ktunotes - inDocument21 pagesHUT300 M4 Ktunotes - inamithaanumadhusoodhananNo ratings yet

- Measurement of Economic PerformanceDocument14 pagesMeasurement of Economic PerformanceGodfrey RushabureNo ratings yet

- MacroeconomicsDocument291 pagesMacroeconomicskyawhtutNo ratings yet

- Macro NotesDocument49 pagesMacro NotesJakBlackNo ratings yet

- National Income AccountingDocument8 pagesNational Income AccountinganuhyaextraNo ratings yet

- ECO401 FinalTerm NotesDocument4 pagesECO401 FinalTerm NotesMuhammad FarooqNo ratings yet

- Team 4Document43 pagesTeam 4ANNTRESA MATHEWNo ratings yet

- The MacroeconomyDocument10 pagesThe MacroeconomyFergus DeanNo ratings yet

- National Income StatisticsDocument5 pagesNational Income StatisticsShingirayi MazingaizoNo ratings yet

- National IncomeDocument20 pagesNational IncomeoggyNo ratings yet

- Economics 20161Document9 pagesEconomics 20161chernet bekeleNo ratings yet

- CH 21 MacroDocument6 pagesCH 21 MacrowiwideeNo ratings yet

- Lectures 3 - 4Document54 pagesLectures 3 - 4fardin222No ratings yet

- Macro EconomicsDocument291 pagesMacro EconomicsCH Mehboob AhmadNo ratings yet

- Scope of Marco Economics: The Formula For Calculating GDP With The Expenditure Approach Is The FollowingDocument5 pagesScope of Marco Economics: The Formula For Calculating GDP With The Expenditure Approach Is The FollowingRaheel AyubNo ratings yet

- Canadian Securities: Overview of EconomicsDocument81 pagesCanadian Securities: Overview of EconomicsNikku SinghNo ratings yet

- Measuring The EconomyDocument34 pagesMeasuring The EconomyJoanaMarie CaisipNo ratings yet

- LECTURE 1, 2 AND 3-NI DETERMINATION-Completed-submitted-28102010Document18 pagesLECTURE 1, 2 AND 3-NI DETERMINATION-Completed-submitted-28102010kehindeadeniyiNo ratings yet

- Lecture 10 Introduction To Macro EconomicsDocument49 pagesLecture 10 Introduction To Macro EconomicsDevyansh GuptaNo ratings yet

- Measures of National Income and OutputDocument6 pagesMeasures of National Income and OutputNii AdjeiNo ratings yet

- Gross Domestic ProductDocument9 pagesGross Domestic ProductSiddesh YadavNo ratings yet

- Mep PDFDocument22 pagesMep PDFGyan PrakashNo ratings yet

- Measures of Economic PerformanceDocument6 pagesMeasures of Economic PerformanceMd. Tayabul HaqueNo ratings yet

- Notes On Ni - Year 3Document16 pagesNotes On Ni - Year 3ibrahim b s kamaraNo ratings yet

- Tema 1,2,3Document30 pagesTema 1,2,3SoniaNo ratings yet

- What Is Gross Domestic ProductDocument9 pagesWhat Is Gross Domestic ProductNico B.No ratings yet

- Module 4Document8 pagesModule 4Piyush AneejwalNo ratings yet

- RB CAGMAT REVIEW LEA Review - Macroeconomics - International TradeDocument99 pagesRB CAGMAT REVIEW LEA Review - Macroeconomics - International TradeShainabe RivaNo ratings yet

- CPA Review Notes 2019 - BEC (Business Environment Concepts)From EverandCPA Review Notes 2019 - BEC (Business Environment Concepts)Rating: 4 out of 5 stars4/5 (9)

- Renewable Energy Mir 20200330 Web PDFDocument31 pagesRenewable Energy Mir 20200330 Web PDFJuan Carlos CastroNo ratings yet

- Thomas Hobbes: Alarcon, Maria Teresa LDocument3 pagesThomas Hobbes: Alarcon, Maria Teresa LNievesAlarcon100% (1)

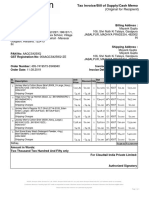

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document2 pagesTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)MAYANK GUPTANo ratings yet

- Twelve Steps Program PaperDocument5 pagesTwelve Steps Program Paperrobertobuezo2No ratings yet

- Baker HughesDocument92 pagesBaker HughesItalo Venegas100% (1)

- The Elephant Vanishes AnalysisDocument3 pagesThe Elephant Vanishes AnalysisDavid100% (1)

- External & Internal Communication: Standard Operating ProcedureDocument12 pagesExternal & Internal Communication: Standard Operating ProcedureAby FNo ratings yet

- Chapter 6 FeminismDocument20 pagesChapter 6 FeminismatelierimkellerNo ratings yet

- If The World Was Ending - JP SaxeDocument2 pagesIf The World Was Ending - JP SaxejobvandekampNo ratings yet

- List of Technical Agencies (TA) Empanelled Under SFURTI SchemeDocument10 pagesList of Technical Agencies (TA) Empanelled Under SFURTI SchemeRa ManNo ratings yet

- Syllabus: SPED 120 Introduction To Special EducationDocument15 pagesSyllabus: SPED 120 Introduction To Special EducationMaridel Mugot-DuranNo ratings yet

- The Silk Road: ¿What Is It?Document2 pagesThe Silk Road: ¿What Is It?Harold Stiven HERNANDEZ RAYONo ratings yet

- God Sees The Truth But WaitsDocument2 pagesGod Sees The Truth But WaitsrowenaNo ratings yet

- Chapter 4 Operation of Travel AgentDocument26 pagesChapter 4 Operation of Travel AgentJanella LlamasNo ratings yet

- 34 Chap - Module 5 - Direct MarketingDocument7 pages34 Chap - Module 5 - Direct MarketingraisehellNo ratings yet

- CDL Manual PDFDocument140 pagesCDL Manual PDFmarceloNo ratings yet

- Hermeneia 17 2016 Small-1Document291 pagesHermeneia 17 2016 Small-1Fanel SuteuNo ratings yet

- NTJD CURRICULUM CHECKLIST SHIFTEES 115, 116, 117, 118 VSN 3 0Document41 pagesNTJD CURRICULUM CHECKLIST SHIFTEES 115, 116, 117, 118 VSN 3 0Jappy AlonNo ratings yet

- ISFIF Programme Schedule - 08 12 2017Document31 pagesISFIF Programme Schedule - 08 12 2017Saurav DashNo ratings yet

- Entrepreneurial Journey of Richard BransonDocument7 pagesEntrepreneurial Journey of Richard Bransondolly saggarNo ratings yet

- People v. Manalo y CabisuelasDocument7 pagesPeople v. Manalo y CabisuelasdingNo ratings yet

- Synechron Corporate Apartments GuidelinesDocument4 pagesSynechron Corporate Apartments GuidelinesSree KrithNo ratings yet

- FinMod 2022-2023 Tutorial Exercise + Answers Week 6Document39 pagesFinMod 2022-2023 Tutorial Exercise + Answers Week 6jjpasemperNo ratings yet

- Paint Booth Calculator AdvancedDocument1 pagePaint Booth Calculator AdvancedSwastik AutomotiveNo ratings yet

- Moeller Consumer Units and The 17 Edition Wiring RegulationsDocument12 pagesMoeller Consumer Units and The 17 Edition Wiring RegulationsArvensisdesignNo ratings yet

- PMI Agile Certified Practitioner (PMI-ACP) HandbookDocument55 pagesPMI Agile Certified Practitioner (PMI-ACP) HandbookmicheledevasconcelosNo ratings yet

- Private International LawDocument16 pagesPrivate International LawMelvin PernezNo ratings yet

- Looking Beyond: Give Him Your Best A Deeper Exposure Global Newswatch Dare 4 MoreDocument20 pagesLooking Beyond: Give Him Your Best A Deeper Exposure Global Newswatch Dare 4 Morejimesh7825No ratings yet

- Narrative 1Document6 pagesNarrative 1Babiejoy Beltran AceloNo ratings yet

Download as pdf or txt

You might also like

- Revlon Case Report - Big BossDocument32 pagesRevlon Case Report - Big BossMohd EizraNo ratings yet

- What Is National Final)Document49 pagesWhat Is National Final)Tong KakitNo ratings yet

- Stocks and Flows: Rules For Computing GDPDocument4 pagesStocks and Flows: Rules For Computing GDPEva DagusNo ratings yet

- Lesson 1 and Lesson 2Document21 pagesLesson 1 and Lesson 2Qui BuiNo ratings yet

- Concepts of Macroeconomics Lesson 1Document6 pagesConcepts of Macroeconomics Lesson 1Dj I amNo ratings yet

- Level of Sales Volume, Sales Value or Production at Which The Business Makes Neither A Profit Nor A Loss (The "Break-Even Point")Document23 pagesLevel of Sales Volume, Sales Value or Production at Which The Business Makes Neither A Profit Nor A Loss (The "Break-Even Point")Tekelemariam FitwiNo ratings yet

- Economic Growth Is Defined As TheDocument20 pagesEconomic Growth Is Defined As TheAsma ShamsNo ratings yet

- Macroeconomics: BY: Maria Deanna S. Salalima, Ed.DDocument7 pagesMacroeconomics: BY: Maria Deanna S. Salalima, Ed.DLerryNo ratings yet

- National IncomeDocument13 pagesNational IncomeMuzammil MotoorNo ratings yet

- Remigio G. TiambengDocument40 pagesRemigio G. TiambengRaissa Ericka RomanNo ratings yet

- Cross Elasticity of DemandDocument4 pagesCross Elasticity of DemandShaniya KoyaNo ratings yet

- The Fundamental Concepts of Macroeconomics: Erandathie PathirajaDocument69 pagesThe Fundamental Concepts of Macroeconomics: Erandathie PathirajaDK White LionNo ratings yet

- EC 124 Chap2 Part - II PDFDocument8 pagesEC 124 Chap2 Part - II PDFAnonymous wFIBMUmt100% (1)

- National Income and Other Social Accounts AnalysisDocument28 pagesNational Income and Other Social Accounts AnalysisJING LINo ratings yet

- Measures of National Income and OutputDocument10 pagesMeasures of National Income and OutputMohammed YunusNo ratings yet

- National IncomeDocument13 pagesNational IncomeEashwar ReddyNo ratings yet

- Presented By: Syndicate 6Document37 pagesPresented By: Syndicate 6suasiveNo ratings yet

- Lecture 3Document10 pagesLecture 3Hitisha agrawalNo ratings yet

- National Income ConceptsDocument25 pagesNational Income ConceptsAnjali ChaudharyNo ratings yet

- VIVADocument6 pagesVIVAkoushikNo ratings yet

- макра теорияDocument38 pagesмакра теорияVictoriaNo ratings yet

- МАКРАDocument11 pagesМАКРАДенис ДавшанNo ratings yet

- MacroeconomicsDocument4 pagesMacroeconomicskuashask2No ratings yet

- Fundamentals of MacroeconomicsDocument5 pagesFundamentals of MacroeconomicsElsa PucciniNo ratings yet

- Macroeconomics - MOCK TEST (Answers)Document54 pagesMacroeconomics - MOCK TEST (Answers)gr306688No ratings yet

- Total Cost in The Long-Run and The Isocost LineDocument11 pagesTotal Cost in The Long-Run and The Isocost LineSamia AfrinNo ratings yet

- Macroeconomics NotesDocument5 pagesMacroeconomics NotesJulian SerhanNo ratings yet

- Chapter 8 The Level of Overall Economic ActivityDocument8 pagesChapter 8 The Level of Overall Economic ActivityHieptaNo ratings yet

- Measures of National Income and OutputDocument6 pagesMeasures of National Income and OutputAJAYNo ratings yet

- Unit-1 - Macro TopicsDocument7 pagesUnit-1 - Macro TopicsKEERTHANA RNo ratings yet

- Macroeconomics CODE: BBF1201: Lecture: Dhanya Jagadeesh BAISAGO University CollegeDocument21 pagesMacroeconomics CODE: BBF1201: Lecture: Dhanya Jagadeesh BAISAGO University CollegeKeeme NaoNo ratings yet

- HUT300 M4 Ktunotes - inDocument21 pagesHUT300 M4 Ktunotes - inamithaanumadhusoodhananNo ratings yet

- Measurement of Economic PerformanceDocument14 pagesMeasurement of Economic PerformanceGodfrey RushabureNo ratings yet

- MacroeconomicsDocument291 pagesMacroeconomicskyawhtutNo ratings yet

- Macro NotesDocument49 pagesMacro NotesJakBlackNo ratings yet

- National Income AccountingDocument8 pagesNational Income AccountinganuhyaextraNo ratings yet

- ECO401 FinalTerm NotesDocument4 pagesECO401 FinalTerm NotesMuhammad FarooqNo ratings yet

- Team 4Document43 pagesTeam 4ANNTRESA MATHEWNo ratings yet

- The MacroeconomyDocument10 pagesThe MacroeconomyFergus DeanNo ratings yet

- National Income StatisticsDocument5 pagesNational Income StatisticsShingirayi MazingaizoNo ratings yet

- National IncomeDocument20 pagesNational IncomeoggyNo ratings yet

- Economics 20161Document9 pagesEconomics 20161chernet bekeleNo ratings yet

- CH 21 MacroDocument6 pagesCH 21 MacrowiwideeNo ratings yet

- Lectures 3 - 4Document54 pagesLectures 3 - 4fardin222No ratings yet

- Macro EconomicsDocument291 pagesMacro EconomicsCH Mehboob AhmadNo ratings yet

- Scope of Marco Economics: The Formula For Calculating GDP With The Expenditure Approach Is The FollowingDocument5 pagesScope of Marco Economics: The Formula For Calculating GDP With The Expenditure Approach Is The FollowingRaheel AyubNo ratings yet

- Canadian Securities: Overview of EconomicsDocument81 pagesCanadian Securities: Overview of EconomicsNikku SinghNo ratings yet

- Measuring The EconomyDocument34 pagesMeasuring The EconomyJoanaMarie CaisipNo ratings yet

- LECTURE 1, 2 AND 3-NI DETERMINATION-Completed-submitted-28102010Document18 pagesLECTURE 1, 2 AND 3-NI DETERMINATION-Completed-submitted-28102010kehindeadeniyiNo ratings yet

- Lecture 10 Introduction To Macro EconomicsDocument49 pagesLecture 10 Introduction To Macro EconomicsDevyansh GuptaNo ratings yet

- Measures of National Income and OutputDocument6 pagesMeasures of National Income and OutputNii AdjeiNo ratings yet

- Gross Domestic ProductDocument9 pagesGross Domestic ProductSiddesh YadavNo ratings yet

- Mep PDFDocument22 pagesMep PDFGyan PrakashNo ratings yet

- Measures of Economic PerformanceDocument6 pagesMeasures of Economic PerformanceMd. Tayabul HaqueNo ratings yet

- Notes On Ni - Year 3Document16 pagesNotes On Ni - Year 3ibrahim b s kamaraNo ratings yet

- Tema 1,2,3Document30 pagesTema 1,2,3SoniaNo ratings yet

- What Is Gross Domestic ProductDocument9 pagesWhat Is Gross Domestic ProductNico B.No ratings yet

- Module 4Document8 pagesModule 4Piyush AneejwalNo ratings yet

- RB CAGMAT REVIEW LEA Review - Macroeconomics - International TradeDocument99 pagesRB CAGMAT REVIEW LEA Review - Macroeconomics - International TradeShainabe RivaNo ratings yet

- CPA Review Notes 2019 - BEC (Business Environment Concepts)From EverandCPA Review Notes 2019 - BEC (Business Environment Concepts)Rating: 4 out of 5 stars4/5 (9)

- Renewable Energy Mir 20200330 Web PDFDocument31 pagesRenewable Energy Mir 20200330 Web PDFJuan Carlos CastroNo ratings yet

- Thomas Hobbes: Alarcon, Maria Teresa LDocument3 pagesThomas Hobbes: Alarcon, Maria Teresa LNievesAlarcon100% (1)

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document2 pagesTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)MAYANK GUPTANo ratings yet

- Twelve Steps Program PaperDocument5 pagesTwelve Steps Program Paperrobertobuezo2No ratings yet

- Baker HughesDocument92 pagesBaker HughesItalo Venegas100% (1)

- The Elephant Vanishes AnalysisDocument3 pagesThe Elephant Vanishes AnalysisDavid100% (1)

- External & Internal Communication: Standard Operating ProcedureDocument12 pagesExternal & Internal Communication: Standard Operating ProcedureAby FNo ratings yet

- Chapter 6 FeminismDocument20 pagesChapter 6 FeminismatelierimkellerNo ratings yet

- If The World Was Ending - JP SaxeDocument2 pagesIf The World Was Ending - JP SaxejobvandekampNo ratings yet

- List of Technical Agencies (TA) Empanelled Under SFURTI SchemeDocument10 pagesList of Technical Agencies (TA) Empanelled Under SFURTI SchemeRa ManNo ratings yet

- Syllabus: SPED 120 Introduction To Special EducationDocument15 pagesSyllabus: SPED 120 Introduction To Special EducationMaridel Mugot-DuranNo ratings yet

- The Silk Road: ¿What Is It?Document2 pagesThe Silk Road: ¿What Is It?Harold Stiven HERNANDEZ RAYONo ratings yet

- God Sees The Truth But WaitsDocument2 pagesGod Sees The Truth But WaitsrowenaNo ratings yet

- Chapter 4 Operation of Travel AgentDocument26 pagesChapter 4 Operation of Travel AgentJanella LlamasNo ratings yet

- 34 Chap - Module 5 - Direct MarketingDocument7 pages34 Chap - Module 5 - Direct MarketingraisehellNo ratings yet

- CDL Manual PDFDocument140 pagesCDL Manual PDFmarceloNo ratings yet

- Hermeneia 17 2016 Small-1Document291 pagesHermeneia 17 2016 Small-1Fanel SuteuNo ratings yet

- NTJD CURRICULUM CHECKLIST SHIFTEES 115, 116, 117, 118 VSN 3 0Document41 pagesNTJD CURRICULUM CHECKLIST SHIFTEES 115, 116, 117, 118 VSN 3 0Jappy AlonNo ratings yet

- ISFIF Programme Schedule - 08 12 2017Document31 pagesISFIF Programme Schedule - 08 12 2017Saurav DashNo ratings yet

- Entrepreneurial Journey of Richard BransonDocument7 pagesEntrepreneurial Journey of Richard Bransondolly saggarNo ratings yet

- People v. Manalo y CabisuelasDocument7 pagesPeople v. Manalo y CabisuelasdingNo ratings yet

- Synechron Corporate Apartments GuidelinesDocument4 pagesSynechron Corporate Apartments GuidelinesSree KrithNo ratings yet

- FinMod 2022-2023 Tutorial Exercise + Answers Week 6Document39 pagesFinMod 2022-2023 Tutorial Exercise + Answers Week 6jjpasemperNo ratings yet

- Paint Booth Calculator AdvancedDocument1 pagePaint Booth Calculator AdvancedSwastik AutomotiveNo ratings yet

- Moeller Consumer Units and The 17 Edition Wiring RegulationsDocument12 pagesMoeller Consumer Units and The 17 Edition Wiring RegulationsArvensisdesignNo ratings yet

- PMI Agile Certified Practitioner (PMI-ACP) HandbookDocument55 pagesPMI Agile Certified Practitioner (PMI-ACP) HandbookmicheledevasconcelosNo ratings yet

- Private International LawDocument16 pagesPrivate International LawMelvin PernezNo ratings yet

- Looking Beyond: Give Him Your Best A Deeper Exposure Global Newswatch Dare 4 MoreDocument20 pagesLooking Beyond: Give Him Your Best A Deeper Exposure Global Newswatch Dare 4 Morejimesh7825No ratings yet

- Narrative 1Document6 pagesNarrative 1Babiejoy Beltran AceloNo ratings yet