Download as pdf or txt

You might also like

- Inspector general’s letterDocument18 pagesInspector general’s letterKatie AnthonyNo ratings yet

- Complaint at Law FILEDDocument12 pagesComplaint at Law FILEDRobert GarciaNo ratings yet

- 2024.05.02 CTBA Understanding and Addressing Chicago's Pension Funding Crisis FinalDocument17 pages2024.05.02 CTBA Understanding and Addressing Chicago's Pension Funding Crisis FinalAnn DwyerNo ratings yet

- Stadium Announcement Press ReleaseDocument4 pagesStadium Announcement Press ReleaseAnn DwyerNo ratings yet

- Tax Sale Class Action LawsuitDocument36 pagesTax Sale Class Action LawsuitAnn DwyerNo ratings yet

- SOS Modernization Report v2Document51 pagesSOS Modernization Report v2Robert GarciaNo ratings yet

- Bring Chicago Home DecisionDocument12 pagesBring Chicago Home DecisionKelly BauerNo ratings yet

- Bring Chicago Home DecisionDocument12 pagesBring Chicago Home DecisionKelly BauerNo ratings yet

- 2024 CH 01108Document44 pages2024 CH 01108Ann DwyerNo ratings yet

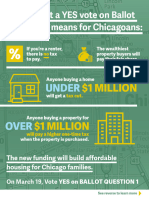

- BCHI24023 Explainer Infographic FINAL FPODocument2 pagesBCHI24023 Explainer Infographic FINAL FPORobert GarciaNo ratings yet

- NASCAR Chicago ReportDocument6 pagesNASCAR Chicago ReportCrains Chicago BusinessNo ratings yet

- Ryan Field Impact Independent Economic Impact Study September 14 2023Document99 pagesRyan Field Impact Independent Economic Impact Study September 14 2023Ann DwyerNo ratings yet

- Lawsuit Against NUDocument14 pagesLawsuit Against NUAnonymous 6f8RIS6No ratings yet

- Final Report On Chicago Park District Lifeguard Matter.11.2Document43 pagesFinal Report On Chicago Park District Lifeguard Matter.11.2Crains Chicago Business0% (1)

- 23-cv-1636 ComplaintDocument17 pages23-cv-1636 ComplaintAnn DwyerNo ratings yet

- Lawsuit Against TribuneDocument21 pagesLawsuit Against TribuneRobert GarciaNo ratings yet

- Ricketts - Insurance Is PlaintiffDocument24 pagesRicketts - Insurance Is PlaintiffAnn DwyerNo ratings yet

- Reforming Mass Transit Governance in The Chicago RegionDocument14 pagesReforming Mass Transit Governance in The Chicago RegionCrains Chicago BusinessNo ratings yet

- Lollapalooza 2022 Economic Impact ReportDocument16 pagesLollapalooza 2022 Economic Impact ReportRobert GarciaNo ratings yet

- US V McClain, Pramaggiore, Hooker & DohertyDocument7 pagesUS V McClain, Pramaggiore, Hooker & DohertyCrains Chicago BusinessNo ratings yet

- Evanston V MonsantoDocument39 pagesEvanston V MonsantoMarcus GilmerNo ratings yet

- Wolf Point SuitDocument37 pagesWolf Point SuitTodd J. BehmeNo ratings yet

- Civil Action Cover Sheet - Case Initiation (12/01/20) CCL 0520 in The Circuit Court of Cook County, Illinois County Department, Law DivisionDocument21 pagesCivil Action Cover Sheet - Case Initiation (12/01/20) CCL 0520 in The Circuit Court of Cook County, Illinois County Department, Law DivisionAnn DwyerNo ratings yet

- Lawsuit Against HUDDocument51 pagesLawsuit Against HUDAnonymous 6f8RIS6No ratings yet

- Usa V BicherDocument9 pagesUsa V BicherGMG EditorialNo ratings yet

- Grubhub ComplaintDocument120 pagesGrubhub ComplaintAnonymous 6f8RIS6No ratings yet

- Lightfoot SpeechDocument30 pagesLightfoot SpeechRobert GarciaNo ratings yet

- 2022 People of The State of V People of The State of Letter Correspond 1681Document12 pages2022 People of The State of V People of The State of Letter Correspond 1681Ann DwyerNo ratings yet

- Pramaggiore AppealDocument86 pagesPramaggiore AppealAnonymous 6f8RIS6100% (1)

- Walker v. Agpawa 2021 IL 127206 (Opinion)Document12 pagesWalker v. Agpawa 2021 IL 127206 (Opinion)Adam HarringtonNo ratings yet

- (LaSalle Initiative) 0Document4 pages(LaSalle Initiative) 0Ann DwyerNo ratings yet

- Metropolitan Pier & Exposition Authority FRI For Lakesider CenterDocument18 pagesMetropolitan Pier & Exposition Authority FRI For Lakesider CenterMarcus GilmerNo ratings yet

- United States Court of Appeals: For The Seventh CircuitDocument17 pagesUnited States Court of Appeals: For The Seventh CircuitAnonymous 6f8RIS6No ratings yet

- Chicago Cook County State's Attorney's Office 2021 ReportDocument4 pagesChicago Cook County State's Attorney's Office 2021 ReportAdam HarringtonNo ratings yet

- Zoning Requirements in We Will Chicago PlanDocument2 pagesZoning Requirements in We Will Chicago PlanAnn DwyerNo ratings yet

- Cook County Board of Review v. Illinois Property Tax Appeal Board, 2023 IL App (1st) 210799-UDocument13 pagesCook County Board of Review v. Illinois Property Tax Appeal Board, 2023 IL App (1st) 210799-UAnn DwyerNo ratings yet

- McDonalds RulingDocument10 pagesMcDonalds RulingAnonymous 6f8RIS6No ratings yet

- Bell V Pappas DismissDocument25 pagesBell V Pappas DismissRobert GarciaNo ratings yet

- Emil Jones ChargesDocument6 pagesEmil Jones ChargesMarcus GilmerNo ratings yet

- FOTP Responds To Bears Stadium Presentation Release-FDocument2 pagesFOTP Responds To Bears Stadium Presentation Release-FAnn Dwyer100% (1)

- Heitman SuitDocument11 pagesHeitman SuitAnonymous 6f8RIS6No ratings yet

- Prairie Grove Flag Protest ResponseDocument3 pagesPrairie Grove Flag Protest ResponseAdam HarringtonNo ratings yet

- Lifeway LawsuitDocument17 pagesLifeway LawsuitAnonymous 6f8RIS6No ratings yet

- Fitzgerald ComplaintDocument52 pagesFitzgerald ComplaintAnonymous 6f8RIS6No ratings yet

- 30.plDocument54 pages30.plRobert GarciaNo ratings yet

- Dakotah Earley LawsuitDocument13 pagesDakotah Earley LawsuitTodd Feurer100% (1)

- Ews Release: Riverside Police Arrest Man For DUI, DUI Drugs Cannabis and CocaineDocument2 pagesEws Release: Riverside Police Arrest Man For DUI, DUI Drugs Cannabis and Cocaineapi-243850372No ratings yet

- Clerk Letter To AssessorDocument2 pagesClerk Letter To AssessorCrains Chicago BusinessNo ratings yet

- Walgreens Whistleblower LawsuitDocument20 pagesWalgreens Whistleblower LawsuitRobert GarciaNo ratings yet

- Oh Legislative Committees Letter Regarding Il Ceja AnalysisDocument4 pagesOh Legislative Committees Letter Regarding Il Ceja AnalysisAnn DwyerNo ratings yet

- Santiago ProfferDocument126 pagesSantiago ProfferAnn Dwyer100% (1)

- Ricketts - Insurance Is DefendantDocument11 pagesRicketts - Insurance Is DefendantAnn DwyerNo ratings yet

- Lightfoot Speech 12/20/21Document15 pagesLightfoot Speech 12/20/21Crains Chicago BusinessNo ratings yet

- DeFunis Is Moot - The Issue Is NotDocument13 pagesDeFunis Is Moot - The Issue Is NotjoshNo ratings yet

- Burke FilingDocument42 pagesBurke FilingAnonymous 6f8RIS6100% (1)

- SLC ReportDocument649 pagesSLC ReportAnn DwyerNo ratings yet

- Gaming BoardDocument3 pagesGaming BoardAnn DwyerNo ratings yet

- 1123 Special Pension BriefingDocument17 pages1123 Special Pension BriefingAnn DwyerNo ratings yet

- Donagher IndictmentDocument23 pagesDonagher IndictmentCarina McMillinNo ratings yet

- Complaint-State Fairgrounds-FinalDocument13 pagesComplaint-State Fairgrounds-FinalCassidyNo ratings yet

- MWRD ComplaintDocument21 pagesMWRD ComplaintjroneillNo ratings yet

- Caldero IndictmentDocument20 pagesCaldero IndictmentShannon McCarthy AntinoriNo ratings yet

- Lifeway LawsuitDocument17 pagesLifeway LawsuitAnonymous 6f8RIS6No ratings yet

- Village Practice LawsuitDocument66 pagesVillage Practice LawsuitAnonymous 6f8RIS6No ratings yet

- Pilots LawsuitDocument33 pagesPilots LawsuitAnonymous 6f8RIS6No ratings yet

- Inside Inclusion 2022 ReportDocument41 pagesInside Inclusion 2022 ReportAnonymous 6f8RIS6No ratings yet

- Real Estate SuitDocument58 pagesReal Estate SuitAnonymous 6f8RIS6100% (2)

- Assault WeaponsDocument95 pagesAssault WeaponsAnonymous 6f8RIS6100% (1)

- Burke FilingDocument42 pagesBurke FilingAnonymous 6f8RIS6100% (1)

- 2024 Chicago Budget ForecastDocument55 pages2024 Chicago Budget ForecastAnonymous 6f8RIS6No ratings yet

- Pramaggiore AppealDocument86 pagesPramaggiore AppealAnonymous 6f8RIS6100% (1)

- Fitzgerald ComplaintDocument52 pagesFitzgerald ComplaintAnonymous 6f8RIS6No ratings yet

- 401 N Wabash RulingDocument16 pages401 N Wabash RulingAnonymous 6f8RIS6No ratings yet

- Opioid ComplaintDocument190 pagesOpioid ComplaintAnonymous 6f8RIS6No ratings yet

- COVID ReportDocument23 pagesCOVID ReportAnonymous 6f8RIS6No ratings yet

- McDonalds RulingDocument10 pagesMcDonalds RulingAnonymous 6f8RIS6No ratings yet

- Brief On Chicago Greyhound TerminalDocument11 pagesBrief On Chicago Greyhound TerminalAnonymous 6f8RIS6No ratings yet

- Wintrust AnswerDocument23 pagesWintrust AnswerAnonymous 6f8RIS6No ratings yet

- AT&T Illinois Deferred Prosecution AgreementDocument36 pagesAT&T Illinois Deferred Prosecution AgreementAnonymous 6f8RIS60% (1)

- United States Court of Appeals: For The Seventh CircuitDocument44 pagesUnited States Court of Appeals: For The Seventh CircuitAnonymous 6f8RIS6No ratings yet

- United States Court of Appeals: For The Seventh CircuitDocument17 pagesUnited States Court of Appeals: For The Seventh CircuitAnonymous 6f8RIS6No ratings yet

- Beau Wrigley ComplaintDocument10 pagesBeau Wrigley ComplaintAnonymous 6f8RIS6No ratings yet

- JDoe - Alden Complaint W ExhibitsDocument57 pagesJDoe - Alden Complaint W ExhibitsAnonymous 6f8RIS6No ratings yet

- Regional Science and Urban Economics: William Larson, Anthony Yezer, Weihua ZhaoDocument18 pagesRegional Science and Urban Economics: William Larson, Anthony Yezer, Weihua ZhaoAnonymous 6f8RIS6No ratings yet

- Advocate Aurora Antitrust LawsuitDocument76 pagesAdvocate Aurora Antitrust LawsuitAnonymous 6f8RIS6No ratings yet

- Doe 1, Et Al.Document24 pagesDoe 1, Et Al.Anonymous 6f8RIS6No ratings yet

- Cubs LawsuitDocument19 pagesCubs LawsuitTodd FeurerNo ratings yet

- HamptonDocument2 pagesHamptonAnonymous 6f8RIS6No ratings yet

- College LawsuitDocument61 pagesCollege LawsuitAnonymous 6f8RIS6No ratings yet

- In The Court of The Circuit Court of Cook County, Illinois County Department, Chancery DivisionDocument69 pagesIn The Court of The Circuit Court of Cook County, Illinois County Department, Chancery DivisionAnonymous 6f8RIS6No ratings yet