Download as pdf or txt

You might also like

- Acctg I State Test Review Packet - KEYDocument13 pagesAcctg I State Test Review Packet - KEYMr. Intel0% (1)

- Calculate The Balance of The Account, Greg Failla, CapitalDocument1 pageCalculate The Balance of The Account, Greg Failla, CapitalJaida Castillo0% (2)

- Latihan UTS AKUNDocument32 pagesLatihan UTS AKUNchittamahayantiNo ratings yet

- Lecture 2Document36 pagesLecture 2Aram NawaisehNo ratings yet

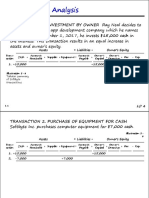

- Transaction Analysis: Transaction 1. Investment by Owner Ray Neal Decides ToDocument31 pagesTransaction Analysis: Transaction 1. Investment by Owner Ray Neal Decides ToSophia LocreNo ratings yet

- 6 - Business Transactions and Their AnalysisDocument23 pages6 - Business Transactions and Their AnalysisJarred FranciscoNo ratings yet

- CH 01 Fin. Acc - Lec 02 EditedDocument16 pagesCH 01 Fin. Acc - Lec 02 Editednumber oneNo ratings yet

- Chapter 1 - Accounting Equation - CorporationDocument37 pagesChapter 1 - Accounting Equation - CorporationadriamNo ratings yet

- Chapter 1 (Mathematical)Document18 pagesChapter 1 (Mathematical)Sabbir HossainNo ratings yet

- Tutorial - Session W1 - SolutionsDocument15 pagesTutorial - Session W1 - SolutionslizaNo ratings yet

- Week+1 Accounting+Equation+-+Solutions PDFDocument15 pagesWeek+1 Accounting+Equation+-+Solutions PDFAli Zain ParharNo ratings yet

- Accounting ExercisesDocument17 pagesAccounting ExercisesKarenNo ratings yet

- Assignment 1Document14 pagesAssignment 1azimlitamellaNo ratings yet

- JW1.chp01-Net Income.2440126966-Julian Lukman SimbolonDocument3 pagesJW1.chp01-Net Income.2440126966-Julian Lukman SimbolonJulian Lukman SimbolonNo ratings yet

- ID 193120001 Final Assignment.Document64 pagesID 193120001 Final Assignment.CSE 1033Naymur RahmanNo ratings yet

- Rule of Debit and Credit (2023)Document26 pagesRule of Debit and Credit (2023)TEE Yu Yang TEENo ratings yet

- Principles of Accounting Lecture 2Document11 pagesPrinciples of Accounting Lecture 2Masum HossainNo ratings yet

- Chapter 1 Sample ProblemsDocument4 pagesChapter 1 Sample ProblemsMesbaul RatulNo ratings yet

- ACCT 207 CHAPTER 3 - No - Video PDFDocument56 pagesACCT 207 CHAPTER 3 - No - Video PDFRoxy BobadillaNo ratings yet

- Tuga 2 Pengantar Akuntansi 1Document25 pagesTuga 2 Pengantar Akuntansi 1Akbar MansyNo ratings yet

- 1.3 - Ch01 Practice MathDocument2 pages1.3 - Ch01 Practice MatharjunaidbdNo ratings yet

- Course Code: Course Title: Submitted To Sahana Kabir Department of Business AdministratorDocument11 pagesCourse Code: Course Title: Submitted To Sahana Kabir Department of Business AdministratorSaif UR RahmanNo ratings yet

- Chapter 2 Basic Accounting Equation BAE and Integrated Financial Reporting WorksheetDocument4 pagesChapter 2 Basic Accounting Equation BAE and Integrated Financial Reporting Worksheetdeon.contactNo ratings yet

- LF BC Corpo Correspondances CorrigéDocument4 pagesLF BC Corpo Correspondances Corrigévive la FranceNo ratings yet

- Show The Effect of The Following Transactions On The Accounting EquationDocument2 pagesShow The Effect of The Following Transactions On The Accounting EquationKhadra HassanNo ratings yet

- Fundamantels of Accounting PresentationDocument24 pagesFundamantels of Accounting PresentationAmy TabaconNo ratings yet

- FSA Financial Mechanism ExcelDocument11 pagesFSA Financial Mechanism ExcelDaniela AriasNo ratings yet

- Accounting Equation WorksheetDocument2 pagesAccounting Equation WorksheetMelu Jean MayoresNo ratings yet

- IIMK - FA - SectionB - Assignment 4Document4 pagesIIMK - FA - SectionB - Assignment 4Jay PatelNo ratings yet

- Tutorial Answer Topic 2 AA015 2122Document3 pagesTutorial Answer Topic 2 AA015 2122Nadia FarhanaNo ratings yet

- Lecture03 FSDocument17 pagesLecture03 FS錢永健No ratings yet

- Assignment 1 (ACT 201)Document4 pagesAssignment 1 (ACT 201)Jihadul IslamNo ratings yet

- HE 2 Questions - Updated-1Document6 pagesHE 2 Questions - Updated-1halelz69No ratings yet

- Studies in Accounting 3Document19 pagesStudies in Accounting 3amirrashad141No ratings yet

- Tugas Accounting 1 With NotesDocument14 pagesTugas Accounting 1 With Notesvico lorenzoNo ratings yet

- Transaction AssignmentDocument2 pagesTransaction AssignmentAbdullah - Al - Safoan 211-15-14629No ratings yet

- Tugas 1 Tabular AnalyzeDocument3 pagesTugas 1 Tabular Analyzealfonsus.wardhana220No ratings yet

- Assignment on Transactions Analysis using the Accounting Equation Due June 5Document34 pagesAssignment on Transactions Analysis using the Accounting Equation Due June 5R.M. CommunityNo ratings yet

- Ap10 1 23Document13 pagesAp10 1 23hieuluu.31221023224No ratings yet

- Fundametals of Acct I CH 1-5Document382 pagesFundametals of Acct I CH 1-5Zerihun GetachewNo ratings yet

- An Sa CT IonDocument2 pagesAn Sa CT IonCharisa BenjaminNo ratings yet

- Ch1 - Exercises SolutionsDocument3 pagesCh1 - Exercises SolutionsReem AbanmiNo ratings yet

- Company Accounting Equation For The Month Ended . AssetsDocument6 pagesCompany Accounting Equation For The Month Ended . AssetsChau ThuNo ratings yet

- Homework 1 and Its SolutionsDocument5 pagesHomework 1 and Its SolutionsBassam AlyeserNo ratings yet

- Financial StatementsDocument13 pagesFinancial Statementspriskilapangaila13No ratings yet

- Department of Computer Science and Engineering: Green University of BangladeshDocument3 pagesDepartment of Computer Science and Engineering: Green University of BangladeshAminul IslamNo ratings yet

- NLKTDocument15 pagesNLKTYến Hoàng HảiNo ratings yet

- Nguyễn Minh Nhật KNC03 31221024307 P1.2LO 45Document4 pagesNguyễn Minh Nhật KNC03 31221024307 P1.2LO 45Bảo KhangNo ratings yet

- Chapter 1 IblDocument13 pagesChapter 1 IblDing DongNo ratings yet

- Course 2 Recording in Journals & Posting in Ledgers22Document1 pageCourse 2 Recording in Journals & Posting in Ledgers22scrbdthowaway271023No ratings yet

- P1-2A Lecture Matarial 1 (Slide 1 Er)Document3 pagesP1-2A Lecture Matarial 1 (Slide 1 Er)Movie Magazine100% (1)

- FA Chap 1Document9 pagesFA Chap 1Bảo TrânNo ratings yet

- Worksheet 1 DR CRDocument5 pagesWorksheet 1 DR CRMc Clent CervantesNo ratings yet

- Name of The Business: Egreen Shop Nature of Business: Online Grossary ShopDocument7 pagesName of The Business: Egreen Shop Nature of Business: Online Grossary ShopShakil AhsanNo ratings yet

- Chapter 1 Exercises 2Document7 pagesChapter 1 Exercises 2thtram03No ratings yet

- Income Statement: IVAN IZO Law OfficeDocument4 pagesIncome Statement: IVAN IZO Law OfficeClaudio AbinenoNo ratings yet

- New Rev Financial Acc1Document22 pagesNew Rev Financial Acc1ahmedfaiyaz917No ratings yet

- Accounting Equation - George LittlechildDocument2 pagesAccounting Equation - George LittlechildIshanNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Interim Test 2021 10 21Document3 pagesInterim Test 2021 10 21Giulia BarthaNo ratings yet

- MTP 2Document5 pagesMTP 2Arpit GuptaNo ratings yet

- FAR 2 Final Mock SolutionDocument11 pagesFAR 2 Final Mock SolutionsheldonjabrazaNo ratings yet

- Main Exam 2014-Sol-1Document7 pagesMain Exam 2014-Sol-1Diego AguirreNo ratings yet

- Acc 201 CH 9Document7 pagesAcc 201 CH 9Trickster TwelveNo ratings yet

- Capita Budgeting QuestionsDocument5 pagesCapita Budgeting QuestionsSULEIMANNo ratings yet

- Nism CH 10Document13 pagesNism CH 10Darshan JainNo ratings yet

- Other Receivables and PayablesDocument6 pagesOther Receivables and PayablesZaara AshfaqNo ratings yet

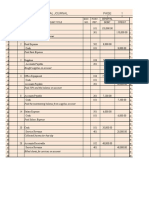

- Date Account Titles and Explanation P.R. Debit Credit: General JournalDocument48 pagesDate Account Titles and Explanation P.R. Debit Credit: General JournalHồng LamNo ratings yet

- 74607bos60479 FND cp2 U2Document111 pages74607bos60479 FND cp2 U2adityatiwari122006No ratings yet

- Tsla 20230331 GenDocument38 pagesTsla 20230331 Gendiego escuin claramonteNo ratings yet

- Quiz 1 - Intacc 2Document9 pagesQuiz 1 - Intacc 2Usagi TsukkiNo ratings yet

- SYLLBS2023Document6 pagesSYLLBS2023AMBenedicto - MCCNo ratings yet

- Corporate FinanceDocument4 pagesCorporate FinancejosemusiNo ratings yet

- Tutorial 3 QDocument2 pagesTutorial 3 QBraham Rahul Ram JamnadasNo ratings yet

- Cyient DLM Limited RHPDocument375 pagesCyient DLM Limited RHPRahul MehtaNo ratings yet

- Case 4 Matapang's Repair BusinessDocument13 pagesCase 4 Matapang's Repair BusinessCobie VillenaNo ratings yet

- XIJI May 2014 (English)Document1 pageXIJI May 2014 (English)Mochamad BhadawiNo ratings yet

- Stock Market Thesis TopicsDocument7 pagesStock Market Thesis Topicsggzgpeikd100% (1)

- Manjunatha TVDocument10 pagesManjunatha TVShilpa RNo ratings yet

- AFAR-13 (Joint Arrangements)Document6 pagesAFAR-13 (Joint Arrangements)MABI ESPENIDONo ratings yet

- BIEF Major Choice Finance 1920191203104134Document20 pagesBIEF Major Choice Finance 1920191203104134GiorgioNo ratings yet

- Practice Problems Introduction To Financial AccountingDocument18 pagesPractice Problems Introduction To Financial AccountingLuciferNo ratings yet

- Tutorial Letter 501/3/2022: General Financial ReportingDocument277 pagesTutorial Letter 501/3/2022: General Financial ReportingMelissaNo ratings yet

- Lesson 3Document29 pagesLesson 3Anh MinhNo ratings yet

- Energy SPDR Fact SheetDocument4 pagesEnergy SPDR Fact Sheetjbyjw5g6jhNo ratings yet

- BOEING 7e7Document5 pagesBOEING 7e7EVA Rental AdminNo ratings yet

- CASH Module Q N ADocument20 pagesCASH Module Q N AAndrea Gwen ArapocNo ratings yet

- Cbleacpu 01Document10 pagesCbleacpu 01Udaya RakavanNo ratings yet