ACCM01B - Module 3

ACCM01B - Module 3

You might also like

- Instant Download Alters and Schiff Essential Concepts For Healthy Living Ebook PDF PDF FREEDocument9 pagesInstant Download Alters and Schiff Essential Concepts For Healthy Living Ebook PDF PDF FREEsam.hirt19698% (56)

- Wek 5 HomeworkDocument5 pagesWek 5 HomeworkJobarteh FofanaNo ratings yet

- Understanding Financial Statements (Review and Analysis of Straub's Book)From EverandUnderstanding Financial Statements (Review and Analysis of Straub's Book)Rating: 5 out of 5 stars5/5 (5)

- Final PPT InfosysDocument29 pagesFinal PPT Infosysyashthefriend89% (9)

- Budgetary PlanningDocument51 pagesBudgetary Planningmehnaz kNo ratings yet

- Chapter 6Document13 pagesChapter 6yana kiutNo ratings yet

- Cost and Management Accounting IIDocument9 pagesCost and Management Accounting IIarefayne wodajoNo ratings yet

- U02 Budget Methodolgies and Budget PreparationDocument26 pagesU02 Budget Methodolgies and Budget PreparationIslam AhmedNo ratings yet

- Budget FinalDocument32 pagesBudget FinalFaiza KhalilNo ratings yet

- Original 1436552353 VICTORIA ProjectDocument12 pagesOriginal 1436552353 VICTORIA ProjectShashank SharanNo ratings yet

- Chapter Two The Master BudgetDocument49 pagesChapter Two The Master BudgetGutu Usma'ilNo ratings yet

- Midterm Topic 4.1 - Notes - Sales Budgets and Production BudgetsDocument2 pagesMidterm Topic 4.1 - Notes - Sales Budgets and Production BudgetslanoyjessicaellahNo ratings yet

- Budgeting For Profit and Control - StuDocument42 pagesBudgeting For Profit and Control - StuAlexis Kaye DayagNo ratings yet

- Financial Planning and BudgetingDocument45 pagesFinancial Planning and BudgetingRafael BensigNo ratings yet

- Financial Management, Lecture 5 & 6Document27 pagesFinancial Management, Lecture 5 & 6Muhammad ImranNo ratings yet

- 2019 CIA P3 SIV 2A 1 BudgetingDocument133 pages2019 CIA P3 SIV 2A 1 BudgetingMarieJoiaNo ratings yet

- Planning and Budgetng.: Course: Introduction To FinancialDocument38 pagesPlanning and Budgetng.: Course: Introduction To FinancialMichaelNo ratings yet

- Chapter 08Document18 pagesChapter 08hana_kimi_91No ratings yet

- Master BudgetDocument6 pagesMaster BudgetPacir QubeNo ratings yet

- Report No. 6 Batoy Khey Heart N. Matano Naffy BDocument35 pagesReport No. 6 Batoy Khey Heart N. Matano Naffy BCamille EscoteNo ratings yet

- 4 - BF - For STUDENTSDocument47 pages4 - BF - For STUDENTSPhill SamonteNo ratings yet

- Profit Planning and BudgetingDocument53 pagesProfit Planning and BudgetingBhey PayumoNo ratings yet

- Profit PlanningDocument5 pagesProfit PlanningChaudhry Umair YounisNo ratings yet

- Spontaneous FundsDocument5 pagesSpontaneous FundsTobelaNcube100% (2)

- Horngrens Financial and Managerial Accounting The Managerial Chapters 4Th Edition Nobles Solutions Manual Download PDF 2024Document133 pagesHorngrens Financial and Managerial Accounting The Managerial Chapters 4Th Edition Nobles Solutions Manual Download PDF 2024thomas.casey387100% (21)

- CHAPTER 3 Financial PlanningDocument7 pagesCHAPTER 3 Financial Planningflorabel parana0% (1)

- CC C C: Y$Y # Yyy Yy YyDocument5 pagesCC C C: Y$Y # Yyy Yy YyNurul 'AinNo ratings yet

- Class 9 - Managerial AccountingDocument12 pagesClass 9 - Managerial AccountingcarlaNo ratings yet

- Chapter 10Document13 pagesChapter 10Shane Melody G. GetonzoNo ratings yet

- Profit Planning-1Document39 pagesProfit Planning-1yaxyesahal123No ratings yet

- Master Budgeting OutlineDocument14 pagesMaster Budgeting OutlineGina Mantos GocotanoNo ratings yet

- CH7 BudgetingDocument51 pagesCH7 BudgetingYMNo ratings yet

- National BudgetDocument27 pagesNational BudgetMAGEZI DAVIDNo ratings yet

- BudgetDocument14 pagesBudgetKomal Shujaat100% (8)

- FM Chapter 10-1Document14 pagesFM Chapter 10-1Shane Melody G. GetonzoNo ratings yet

- UNIT-3 Financial Planning and ForecastingDocument33 pagesUNIT-3 Financial Planning and ForecastingAssfaw KebedeNo ratings yet

- Chapter Two Budgeting Types of BudgetDocument7 pagesChapter Two Budgeting Types of BudgetAnfield FaithfulNo ratings yet

- Financial Management Chapter 10Document14 pagesFinancial Management Chapter 10Shane Melody G. GetonzoNo ratings yet

- Moduel 4Document11 pagesModuel 4sarojkumardasbsetNo ratings yet

- Review 20Document4 pagesReview 20StubadubNo ratings yet

- Illustrative Problem On Master BudgetingDocument13 pagesIllustrative Problem On Master BudgetingSumendra Shrestha84% (19)

- Principles of Finance Chapter08 金融学原理Document75 pagesPrinciples of Finance Chapter08 金融学原理Lim Mei SuokNo ratings yet

- Chapter 3 BCDocument42 pagesChapter 3 BCAN NesNo ratings yet

- Budget: Definition, Classification and Types of BudgetsDocument15 pagesBudget: Definition, Classification and Types of BudgetsAnderson GuzmanNo ratings yet

- Chapter 13 To 15Document13 pagesChapter 13 To 15Cherry Mae GecoNo ratings yet

- Blue Jay Private LimitedDocument2 pagesBlue Jay Private LimitedanuNo ratings yet

- Budget Matterial For The Students NewDocument10 pagesBudget Matterial For The Students NewheysemNo ratings yet

- ACCT 504 Final Exam AnswersDocument5 pagesACCT 504 Final Exam Answerssusanperry50% (2)

- Chapter 5-Financial Forecasting, Corporate Planning and BudgetingDocument64 pagesChapter 5-Financial Forecasting, Corporate Planning and BudgetingJanadine Grace De LeonNo ratings yet

- Ch.13 Managing Small Business FinanceDocument5 pagesCh.13 Managing Small Business FinanceBaesick MoviesNo ratings yet

- Mas 10 Flexible and Static BudgetDocument18 pagesMas 10 Flexible and Static BudgetJean Fajardo BadilloNo ratings yet

- Additional Funds Needed MasDocument22 pagesAdditional Funds Needed MasWilmer Mateo Bernardo100% (1)

- Unit - 4 Marginal Costing: DefinitionDocument5 pagesUnit - 4 Marginal Costing: DefinitionThigilpandi07 YTNo ratings yet

- Actual Activities of A Firm.: Answers To Study Questions For Chapter 8Document4 pagesActual Activities of A Firm.: Answers To Study Questions For Chapter 8Louie De La TorreNo ratings yet

- Case 123Document5 pagesCase 123jhanzabNo ratings yet

- ACCT 504 MART Perfect EducationDocument62 pagesACCT 504 MART Perfect EducationdavidwarneNo ratings yet

- Chapter 5: Financial Forecasting, Corporate Planning, and Budgeting Corporate PlanningDocument6 pagesChapter 5: Financial Forecasting, Corporate Planning, and Budgeting Corporate PlanningAdoree RamosNo ratings yet

- Financial Planning Tool and ConceptDocument125 pagesFinancial Planning Tool and ConceptKareen Tapia PublicoNo ratings yet

- Scribd DownloadDocument20 pagesScribd DownloadQuite VairaNo ratings yet

- Teaching Notes CH03 Financial ForecastingDocument7 pagesTeaching Notes CH03 Financial ForecastingMai PhamNo ratings yet

- Chapter 4Document3 pagesChapter 4Ak AlNo ratings yet

- Brochure - Final - 13092019 22 PDFDocument2 pagesBrochure - Final - 13092019 22 PDFCHARINo ratings yet

- Cover Letter For Any Job Position SampleDocument4 pagesCover Letter For Any Job Position Sampleasbbrfsmd100% (1)

- Textbook Ebook Introduction To Management Accounting Global Edition 17Th Edition Charles Horngren All Chapter PDFDocument43 pagesTextbook Ebook Introduction To Management Accounting Global Edition 17Th Edition Charles Horngren All Chapter PDFkim.reyes855100% (9)

- ECON130 Tutorial 04Document5 pagesECON130 Tutorial 04Tino Palala TenariNo ratings yet

- Why Soft-Skills Simulation: Makes A Hard Case For Sales TrainingDocument13 pagesWhy Soft-Skills Simulation: Makes A Hard Case For Sales TrainingShreyaNo ratings yet

- Chapter 16 AuditingDocument29 pagesChapter 16 AuditingMisshtaCNo ratings yet

- Jawaban UAS EnglishDocument2 pagesJawaban UAS EnglishAulia FitriyaniNo ratings yet

- Bus Admin New Feeschedule 2020 2021Document3 pagesBus Admin New Feeschedule 2020 2021Ajith PNo ratings yet

- ECON7850Document2 pagesECON7850t tNo ratings yet

- Design Qualification TemplateDocument5 pagesDesign Qualification Templateavinash peddintiNo ratings yet

- SMAW-Basics DEMODocument24 pagesSMAW-Basics DEMOKentDemeterioNo ratings yet

- Midterm 2 BootcampDocument33 pagesMidterm 2 Bootcampmaged famNo ratings yet

- UNLEASH X Unit4 HR Technology Market Report 2023 - FINALDocument9 pagesUNLEASH X Unit4 HR Technology Market Report 2023 - FINALSophia RusconiNo ratings yet

- Business PlanDocument14 pagesBusiness PlanJayson JandocNo ratings yet

- Macsec Feature Parameter Description: SingleranDocument20 pagesMacsec Feature Parameter Description: SingleranAlina Ali MalikNo ratings yet

- Horizon 2035 Downtown PlanDocument210 pagesHorizon 2035 Downtown PlanconfluencescribdNo ratings yet

- 5 - Intraday Pattern Practice SessionDocument12 pages5 - Intraday Pattern Practice SessioncollegetradingexchangeNo ratings yet

- GlobeScan SIGWATCH Future of Business NGO Collaboration Summary Report May2023Document5 pagesGlobeScan SIGWATCH Future of Business NGO Collaboration Summary Report May2023ComunicarSe-ArchivoNo ratings yet

- 7 ElevenDocument16 pages7 ElevenRena Mae Lava MuycoNo ratings yet

- A Project Report On Winning The Strikers: Shagun SharmaDocument59 pagesA Project Report On Winning The Strikers: Shagun SharmaharshNo ratings yet

- AIandwork WweDocument41 pagesAIandwork WweTaylan ŞahinNo ratings yet

- Assessing The Role of Master Plans in City Development: Reform Measures and ApproachesDocument19 pagesAssessing The Role of Master Plans in City Development: Reform Measures and Approachesshreya jaiswalNo ratings yet

- Level - 3 - Unit - 3 Workbook Sample CEFR B1+Document8 pagesLevel - 3 - Unit - 3 Workbook Sample CEFR B1+karyee limNo ratings yet

- Project Report Mukesh DeshmukhDocument13 pagesProject Report Mukesh Deshmukharju gaikwadNo ratings yet

- FINA2320 - ABC - 2023 - Tutorial 1Document5 pagesFINA2320 - ABC - 2023 - Tutorial 1Aaron WongNo ratings yet

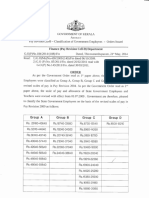

- GO (P) No 184-2014 - (188) - Fin Dated 21-05-2014Document2 pagesGO (P) No 184-2014 - (188) - Fin Dated 21-05-2014Sarath SNo ratings yet

- Sindh Building Control Authority Public Notice: Maple HomesDocument2 pagesSindh Building Control Authority Public Notice: Maple HomesKhalid MehboobNo ratings yet

Download as docx, pdf, or txt

You might also like

- Instant Download Alters and Schiff Essential Concepts For Healthy Living Ebook PDF PDF FREEDocument9 pagesInstant Download Alters and Schiff Essential Concepts For Healthy Living Ebook PDF PDF FREEsam.hirt19698% (56)

- Wek 5 HomeworkDocument5 pagesWek 5 HomeworkJobarteh FofanaNo ratings yet

- Understanding Financial Statements (Review and Analysis of Straub's Book)From EverandUnderstanding Financial Statements (Review and Analysis of Straub's Book)Rating: 5 out of 5 stars5/5 (5)

- Final PPT InfosysDocument29 pagesFinal PPT Infosysyashthefriend89% (9)

- Budgetary PlanningDocument51 pagesBudgetary Planningmehnaz kNo ratings yet

- Chapter 6Document13 pagesChapter 6yana kiutNo ratings yet

- Cost and Management Accounting IIDocument9 pagesCost and Management Accounting IIarefayne wodajoNo ratings yet

- U02 Budget Methodolgies and Budget PreparationDocument26 pagesU02 Budget Methodolgies and Budget PreparationIslam AhmedNo ratings yet

- Budget FinalDocument32 pagesBudget FinalFaiza KhalilNo ratings yet

- Original 1436552353 VICTORIA ProjectDocument12 pagesOriginal 1436552353 VICTORIA ProjectShashank SharanNo ratings yet

- Chapter Two The Master BudgetDocument49 pagesChapter Two The Master BudgetGutu Usma'ilNo ratings yet

- Midterm Topic 4.1 - Notes - Sales Budgets and Production BudgetsDocument2 pagesMidterm Topic 4.1 - Notes - Sales Budgets and Production BudgetslanoyjessicaellahNo ratings yet

- Budgeting For Profit and Control - StuDocument42 pagesBudgeting For Profit and Control - StuAlexis Kaye DayagNo ratings yet

- Financial Planning and BudgetingDocument45 pagesFinancial Planning and BudgetingRafael BensigNo ratings yet

- Financial Management, Lecture 5 & 6Document27 pagesFinancial Management, Lecture 5 & 6Muhammad ImranNo ratings yet

- 2019 CIA P3 SIV 2A 1 BudgetingDocument133 pages2019 CIA P3 SIV 2A 1 BudgetingMarieJoiaNo ratings yet

- Planning and Budgetng.: Course: Introduction To FinancialDocument38 pagesPlanning and Budgetng.: Course: Introduction To FinancialMichaelNo ratings yet

- Chapter 08Document18 pagesChapter 08hana_kimi_91No ratings yet

- Master BudgetDocument6 pagesMaster BudgetPacir QubeNo ratings yet

- Report No. 6 Batoy Khey Heart N. Matano Naffy BDocument35 pagesReport No. 6 Batoy Khey Heart N. Matano Naffy BCamille EscoteNo ratings yet

- 4 - BF - For STUDENTSDocument47 pages4 - BF - For STUDENTSPhill SamonteNo ratings yet

- Profit Planning and BudgetingDocument53 pagesProfit Planning and BudgetingBhey PayumoNo ratings yet

- Profit PlanningDocument5 pagesProfit PlanningChaudhry Umair YounisNo ratings yet

- Spontaneous FundsDocument5 pagesSpontaneous FundsTobelaNcube100% (2)

- Horngrens Financial and Managerial Accounting The Managerial Chapters 4Th Edition Nobles Solutions Manual Download PDF 2024Document133 pagesHorngrens Financial and Managerial Accounting The Managerial Chapters 4Th Edition Nobles Solutions Manual Download PDF 2024thomas.casey387100% (21)

- CHAPTER 3 Financial PlanningDocument7 pagesCHAPTER 3 Financial Planningflorabel parana0% (1)

- CC C C: Y$Y # Yyy Yy YyDocument5 pagesCC C C: Y$Y # Yyy Yy YyNurul 'AinNo ratings yet

- Class 9 - Managerial AccountingDocument12 pagesClass 9 - Managerial AccountingcarlaNo ratings yet

- Chapter 10Document13 pagesChapter 10Shane Melody G. GetonzoNo ratings yet

- Profit Planning-1Document39 pagesProfit Planning-1yaxyesahal123No ratings yet

- Master Budgeting OutlineDocument14 pagesMaster Budgeting OutlineGina Mantos GocotanoNo ratings yet

- CH7 BudgetingDocument51 pagesCH7 BudgetingYMNo ratings yet

- National BudgetDocument27 pagesNational BudgetMAGEZI DAVIDNo ratings yet

- BudgetDocument14 pagesBudgetKomal Shujaat100% (8)

- FM Chapter 10-1Document14 pagesFM Chapter 10-1Shane Melody G. GetonzoNo ratings yet

- UNIT-3 Financial Planning and ForecastingDocument33 pagesUNIT-3 Financial Planning and ForecastingAssfaw KebedeNo ratings yet

- Chapter Two Budgeting Types of BudgetDocument7 pagesChapter Two Budgeting Types of BudgetAnfield FaithfulNo ratings yet

- Financial Management Chapter 10Document14 pagesFinancial Management Chapter 10Shane Melody G. GetonzoNo ratings yet

- Moduel 4Document11 pagesModuel 4sarojkumardasbsetNo ratings yet

- Review 20Document4 pagesReview 20StubadubNo ratings yet

- Illustrative Problem On Master BudgetingDocument13 pagesIllustrative Problem On Master BudgetingSumendra Shrestha84% (19)

- Principles of Finance Chapter08 金融学原理Document75 pagesPrinciples of Finance Chapter08 金融学原理Lim Mei SuokNo ratings yet

- Chapter 3 BCDocument42 pagesChapter 3 BCAN NesNo ratings yet

- Budget: Definition, Classification and Types of BudgetsDocument15 pagesBudget: Definition, Classification and Types of BudgetsAnderson GuzmanNo ratings yet

- Chapter 13 To 15Document13 pagesChapter 13 To 15Cherry Mae GecoNo ratings yet

- Blue Jay Private LimitedDocument2 pagesBlue Jay Private LimitedanuNo ratings yet

- Budget Matterial For The Students NewDocument10 pagesBudget Matterial For The Students NewheysemNo ratings yet

- ACCT 504 Final Exam AnswersDocument5 pagesACCT 504 Final Exam Answerssusanperry50% (2)

- Chapter 5-Financial Forecasting, Corporate Planning and BudgetingDocument64 pagesChapter 5-Financial Forecasting, Corporate Planning and BudgetingJanadine Grace De LeonNo ratings yet

- Ch.13 Managing Small Business FinanceDocument5 pagesCh.13 Managing Small Business FinanceBaesick MoviesNo ratings yet

- Mas 10 Flexible and Static BudgetDocument18 pagesMas 10 Flexible and Static BudgetJean Fajardo BadilloNo ratings yet

- Additional Funds Needed MasDocument22 pagesAdditional Funds Needed MasWilmer Mateo Bernardo100% (1)

- Unit - 4 Marginal Costing: DefinitionDocument5 pagesUnit - 4 Marginal Costing: DefinitionThigilpandi07 YTNo ratings yet

- Actual Activities of A Firm.: Answers To Study Questions For Chapter 8Document4 pagesActual Activities of A Firm.: Answers To Study Questions For Chapter 8Louie De La TorreNo ratings yet

- Case 123Document5 pagesCase 123jhanzabNo ratings yet

- ACCT 504 MART Perfect EducationDocument62 pagesACCT 504 MART Perfect EducationdavidwarneNo ratings yet

- Chapter 5: Financial Forecasting, Corporate Planning, and Budgeting Corporate PlanningDocument6 pagesChapter 5: Financial Forecasting, Corporate Planning, and Budgeting Corporate PlanningAdoree RamosNo ratings yet

- Financial Planning Tool and ConceptDocument125 pagesFinancial Planning Tool and ConceptKareen Tapia PublicoNo ratings yet

- Scribd DownloadDocument20 pagesScribd DownloadQuite VairaNo ratings yet

- Teaching Notes CH03 Financial ForecastingDocument7 pagesTeaching Notes CH03 Financial ForecastingMai PhamNo ratings yet

- Chapter 4Document3 pagesChapter 4Ak AlNo ratings yet

- Brochure - Final - 13092019 22 PDFDocument2 pagesBrochure - Final - 13092019 22 PDFCHARINo ratings yet

- Cover Letter For Any Job Position SampleDocument4 pagesCover Letter For Any Job Position Sampleasbbrfsmd100% (1)

- Textbook Ebook Introduction To Management Accounting Global Edition 17Th Edition Charles Horngren All Chapter PDFDocument43 pagesTextbook Ebook Introduction To Management Accounting Global Edition 17Th Edition Charles Horngren All Chapter PDFkim.reyes855100% (9)

- ECON130 Tutorial 04Document5 pagesECON130 Tutorial 04Tino Palala TenariNo ratings yet

- Why Soft-Skills Simulation: Makes A Hard Case For Sales TrainingDocument13 pagesWhy Soft-Skills Simulation: Makes A Hard Case For Sales TrainingShreyaNo ratings yet

- Chapter 16 AuditingDocument29 pagesChapter 16 AuditingMisshtaCNo ratings yet

- Jawaban UAS EnglishDocument2 pagesJawaban UAS EnglishAulia FitriyaniNo ratings yet

- Bus Admin New Feeschedule 2020 2021Document3 pagesBus Admin New Feeschedule 2020 2021Ajith PNo ratings yet

- ECON7850Document2 pagesECON7850t tNo ratings yet

- Design Qualification TemplateDocument5 pagesDesign Qualification Templateavinash peddintiNo ratings yet

- SMAW-Basics DEMODocument24 pagesSMAW-Basics DEMOKentDemeterioNo ratings yet

- Midterm 2 BootcampDocument33 pagesMidterm 2 Bootcampmaged famNo ratings yet

- UNLEASH X Unit4 HR Technology Market Report 2023 - FINALDocument9 pagesUNLEASH X Unit4 HR Technology Market Report 2023 - FINALSophia RusconiNo ratings yet

- Business PlanDocument14 pagesBusiness PlanJayson JandocNo ratings yet

- Macsec Feature Parameter Description: SingleranDocument20 pagesMacsec Feature Parameter Description: SingleranAlina Ali MalikNo ratings yet

- Horizon 2035 Downtown PlanDocument210 pagesHorizon 2035 Downtown PlanconfluencescribdNo ratings yet

- 5 - Intraday Pattern Practice SessionDocument12 pages5 - Intraday Pattern Practice SessioncollegetradingexchangeNo ratings yet

- GlobeScan SIGWATCH Future of Business NGO Collaboration Summary Report May2023Document5 pagesGlobeScan SIGWATCH Future of Business NGO Collaboration Summary Report May2023ComunicarSe-ArchivoNo ratings yet

- 7 ElevenDocument16 pages7 ElevenRena Mae Lava MuycoNo ratings yet

- A Project Report On Winning The Strikers: Shagun SharmaDocument59 pagesA Project Report On Winning The Strikers: Shagun SharmaharshNo ratings yet

- AIandwork WweDocument41 pagesAIandwork WweTaylan ŞahinNo ratings yet

- Assessing The Role of Master Plans in City Development: Reform Measures and ApproachesDocument19 pagesAssessing The Role of Master Plans in City Development: Reform Measures and Approachesshreya jaiswalNo ratings yet

- Level - 3 - Unit - 3 Workbook Sample CEFR B1+Document8 pagesLevel - 3 - Unit - 3 Workbook Sample CEFR B1+karyee limNo ratings yet

- Project Report Mukesh DeshmukhDocument13 pagesProject Report Mukesh Deshmukharju gaikwadNo ratings yet

- FINA2320 - ABC - 2023 - Tutorial 1Document5 pagesFINA2320 - ABC - 2023 - Tutorial 1Aaron WongNo ratings yet

- GO (P) No 184-2014 - (188) - Fin Dated 21-05-2014Document2 pagesGO (P) No 184-2014 - (188) - Fin Dated 21-05-2014Sarath SNo ratings yet

- Sindh Building Control Authority Public Notice: Maple HomesDocument2 pagesSindh Building Control Authority Public Notice: Maple HomesKhalid MehboobNo ratings yet