Download as xlsx, pdf, or txt

You might also like

- Tesco PLC (Group 7)Document23 pagesTesco PLC (Group 7)Jingquan (Adele) ZhaoNo ratings yet

- Balance SheetDocument24 pagesBalance SheetsakshiNo ratings yet

- Femsa VS PepsicoDocument8 pagesFemsa VS PepsicoDanniel MtNo ratings yet

- Income Statement For Group and SegmentsDocument1 pageIncome Statement For Group and Segmentstry6y6hmhbNo ratings yet

- Income Statements For Group and SegmentsDocument5 pagesIncome Statements For Group and SegmentsSaba MasoodNo ratings yet

- TRG FinancialsDocument2 pagesTRG FinancialsArsalanNo ratings yet

- FS NvidiaDocument22 pagesFS NvidiaReza FachrizalNo ratings yet

- Nexo Nature 4Document20 pagesNexo Nature 4Milan SamantarayNo ratings yet

- Income Statements For Group and Segments For The Period From 1 April To 30 JuneDocument7 pagesIncome Statements For Group and Segments For The Period From 1 April To 30 Juneali balochNo ratings yet

- Keerthika Case StudiesDocument9 pagesKeerthika Case StudiesAarti SaxenaNo ratings yet

- Yusuf Bhai Munda Computation 2019-20Document3 pagesYusuf Bhai Munda Computation 2019-20satish devdaNo ratings yet

- Financial Statements 2020Document9 pagesFinancial Statements 2020ADITYA VERMANo ratings yet

- Income Statements For Group and SegmentsDocument9 pagesIncome Statements For Group and SegmentsADITYA VERMANo ratings yet

- Week 3 Activity-1Document2 pagesWeek 3 Activity-1Aliyana SmolderhalderNo ratings yet

- PG FS AnalysisDocument13 pagesPG FS AnalysisReina Nina CamanoNo ratings yet

- Company Info - Print FinancialsDocument1 pageCompany Info - Print Financialsabhey1035ranaNo ratings yet

- Om Prakash Comp Ay 2020-21Document4 pagesOm Prakash Comp Ay 2020-21Soumya SwainNo ratings yet

- Analysis of Finanacial Statements and Interpretation in DetailDocument8 pagesAnalysis of Finanacial Statements and Interpretation in DetailMayuri RawatNo ratings yet

- Profit Budget 2017/18 QTR 1 QTR 2 QTR 3Document6 pagesProfit Budget 2017/18 QTR 1 QTR 2 QTR 3Tatiana Garcia MendozaNo ratings yet

- Invesment AppraisalDocument2 pagesInvesment AppraisalMuhasina MuzyNo ratings yet

- 1 +Data+File+for+Debit+Credit+ConversionDocument1,779 pages1 +Data+File+for+Debit+Credit+Conversionprakash chandra jain & company.No ratings yet

- Form Nl-1-B-Ra Periodic DisclosuresDocument1 pageForm Nl-1-B-Ra Periodic DisclosuresNilesh DawandeNo ratings yet

- Itr-3 Coi - F.Y 2021-22 - Ayush BhosleDocument6 pagesItr-3 Coi - F.Y 2021-22 - Ayush Bhosledarshil thakkerNo ratings yet

- Sandeep Sharma Computation 23-24Document2 pagesSandeep Sharma Computation 23-24mentoraxis1No ratings yet

- Group Wise StatementDocument60 pagesGroup Wise Statementnibha0705No ratings yet

- Comp 22 23Document2 pagesComp 22 23mexop31426No ratings yet

- اكسل شيت رائع في التحليل الماليDocument144 pagesاكسل شيت رائع في التحليل الماليNabil SharafaldinNo ratings yet

- NVDA DCFDocument7 pagesNVDA DCFSahand LaliNo ratings yet

- Old SachemeDocument2 pagesOld Sachemerinkuaws9696.2No ratings yet

- Profit and Loss Account Expenses IncomeDocument10 pagesProfit and Loss Account Expenses IncomeAnkit AggarwalNo ratings yet

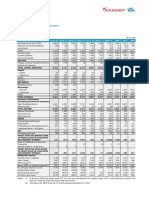

- TCS Q4'24 Financial ResultsDocument11 pagesTCS Q4'24 Financial ResultsLavanya MaheshwariNo ratings yet

- AttachmentDocument4 pagesAttachmentLikhithVulapuNo ratings yet

- Inbamfi Equity CaseDocument19 pagesInbamfi Equity CaseBinsentcaragNo ratings yet

- Quice Foods Industries LTDDocument4 pagesQuice Foods Industries LTDOsama RiazNo ratings yet

- Interpretation of Results: 1. Multiple Regression ForDocument5 pagesInterpretation of Results: 1. Multiple Regression ForATUL KUMARNo ratings yet

- Fathom Example Import FileDocument4 pagesFathom Example Import FileSaravananNo ratings yet

- Financial Statement Q2-2018Document13 pagesFinancial Statement Q2-2018Bharath Simha ReddyNo ratings yet

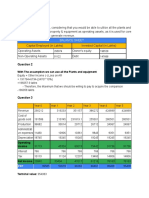

- Balance Sheet: With The Assumption We Can Use All The Plants and EquipmentDocument4 pagesBalance Sheet: With The Assumption We Can Use All The Plants and EquipmentPriadarshini Subramanyam DM21B093No ratings yet

- Company Name: Orion Pharma LTDDocument18 pagesCompany Name: Orion Pharma LTDMehenaj Sultana BithyNo ratings yet

- Jet AirwaysDocument4 pagesJet Airwayssmith dabreoNo ratings yet

- 2016 Nestle ExtratedDocument7 pages2016 Nestle ExtratednesanNo ratings yet

- Provision For Fringe Benefit Tax Provision For Fradulent EncashmentDocument20 pagesProvision For Fringe Benefit Tax Provision For Fradulent EncashmentSwapnil GadewarNo ratings yet

- 1q23 QuarterlyseriesDocument21 pages1q23 Quarterlyseriesmana manaNo ratings yet

- Itr GVX 2018-19Document5 pagesItr GVX 2018-19akhil kwatraNo ratings yet

- Payslip APR 900546Document1 pagePayslip APR 900546jyprakash17No ratings yet

- ComputationDocument3 pagesComputationsaurabh240386No ratings yet

- Historical Data BoeingDocument90 pagesHistorical Data BoeingRohit BhangaleNo ratings yet

- Waterfall Ob Des. '21Document63 pagesWaterfall Ob Des. '21Feni PerdanaNo ratings yet

- Nations Trust Bank PLC and Its Subsidiaries: Company Number PQ 118Document19 pagesNations Trust Bank PLC and Its Subsidiaries: Company Number PQ 118haffaNo ratings yet

- Hotel Maharaja - Subham Anil Gade 26012023Document12 pagesHotel Maharaja - Subham Anil Gade 26012023Nikhil PawaseNo ratings yet

- Power Cement Limited: Jun/2017 Cash Flows From Operating ActivitiesDocument24 pagesPower Cement Limited: Jun/2017 Cash Flows From Operating ActivitiesUsama malikNo ratings yet

- Sunway Berhad Comparative Income StatementDocument16 pagesSunway Berhad Comparative Income StatementYaesnavy ParamesvaranNo ratings yet

- Financial at A GlanceDocument1 pageFinancial at A GlancesaeedNo ratings yet

- Section B Group 4 Assignment BNL StoresDocument3 pagesSection B Group 4 Assignment BNL StoresMohit VermaNo ratings yet

- 1st Challenge 11-1Document4 pages1st Challenge 11-1SergiiNo ratings yet

- UBL Annual Report 2018-129Document1 pageUBL Annual Report 2018-129IFRS LabNo ratings yet

- Equity Research Report: Market Movers Trading CoDocument4 pagesEquity Research Report: Market Movers Trading CoNayan PatelNo ratings yet

- MARKET ESTIMATES FOR Sep, 2008 Results To Be Announced TodayDocument2 pagesMARKET ESTIMATES FOR Sep, 2008 Results To Be Announced TodaydidwaniasNo ratings yet

- The Hanuman Estates Limited: Adjutments ForDocument1 pageThe Hanuman Estates Limited: Adjutments Forravibhartia1978No ratings yet