Download as docx, pdf, or txt

You might also like

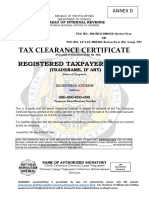

- Annex DDocument1 pageAnnex DIdan Aguirre67% (3)

- Market Impact Model - Nicolo G. Torre, Ph.D. Mark J. Ferrari, Ph.D.Document48 pagesMarket Impact Model - Nicolo G. Torre, Ph.D. Mark J. Ferrari, Ph.D.SylvainNo ratings yet

- AFP Awards and DecorationsDocument106 pagesAFP Awards and DecorationsAtty Rester John NonatoNo ratings yet

- Bir 363-14Document5 pagesBir 363-14msdivergentNo ratings yet

- Powerpoint Presentation For TRAIN LAWDocument29 pagesPowerpoint Presentation For TRAIN LAWEd Armand Ventolero100% (2)

- BIR Ruling DA - VAT-021 121-10Document3 pagesBIR Ruling DA - VAT-021 121-10Jemila Paula Diala100% (1)

- Cost and ManagementDocument310 pagesCost and ManagementWaleed Noman100% (1)

- Art 1828 - 1867 DigestsDocument8 pagesArt 1828 - 1867 Digestsnina armadaNo ratings yet

- BIR RULING NO. 278-13: Noritake Porcelana MFG., IncDocument3 pagesBIR RULING NO. 278-13: Noritake Porcelana MFG., IncJoyceMendozaNo ratings yet

- Authoritative Guide On Real Estate Transfer TaxesDocument37 pagesAuthoritative Guide On Real Estate Transfer TaxesJames ReyesNo ratings yet

- Question As Emailed To Us On 24 Oct 2020 by Safique SardarDocument4 pagesQuestion As Emailed To Us On 24 Oct 2020 by Safique SardarSk Asif AliNo ratings yet

- Running Head: DEAL OF DOZER 1Document5 pagesRunning Head: DEAL OF DOZER 1Ayesha TanvirNo ratings yet

- PRSN / VVK / Rad Indirect Taxes Dept. - HQDocument107 pagesPRSN / VVK / Rad Indirect Taxes Dept. - HQprabhu85No ratings yet

- 2009 ArDocument88 pages2009 ArCuntNo ratings yet

- Characteristic of Vat-Business TaxationDocument8 pagesCharacteristic of Vat-Business TaxationAthena LouiseNo ratings yet

- Application For Remittance of Royalty Fee (App-V53)Document4 pagesApplication For Remittance of Royalty Fee (App-V53)Soniya KhuramNo ratings yet

- CGT Tomanda AntokDocument1 pageCGT Tomanda AntokNvision PresentNo ratings yet

- RR 05-09 (Sale of RP)Document7 pagesRR 05-09 (Sale of RP)joefieNo ratings yet

- MTF Tax Journal July 2021Document27 pagesMTF Tax Journal July 2021Earle EdraNo ratings yet

- Bureau of Internal Revenue Quezon City March 2, 2011: Republic of The Philippines Department of FinanceDocument3 pagesBureau of Internal Revenue Quezon City March 2, 2011: Republic of The Philippines Department of FinanceBret MonsantoNo ratings yet

- Bir Ruling Da (Vat 050) 282 09Document3 pagesBir Ruling Da (Vat 050) 282 09doraemoanNo ratings yet

- How To Compute DSTDocument6 pagesHow To Compute DSTShayne AgustinNo ratings yet

- Eqp - PO - No - IIC-EPO-2023-0404 - ABDULLAH MUHAMMAD AL-MEER GENERAL CONTRACTING EST.Document2 pagesEqp - PO - No - IIC-EPO-2023-0404 - ABDULLAH MUHAMMAD AL-MEER GENERAL CONTRACTING EST.Dhanu NikkuNo ratings yet

- Steps of Land TransferDocument6 pagesSteps of Land TransferKeith LlaveNo ratings yet

- Guideline in The Transfer of Titles of Real PropertyDocument4 pagesGuideline in The Transfer of Titles of Real PropertyLeolaida AragonNo ratings yet

- Taxation WorkshopDocument83 pagesTaxation WorkshopLaw_Portal100% (1)

- 7333-1998-Bir Ruling No. 029-98 PDFDocument3 pages7333-1998-Bir Ruling No. 029-98 PDFjeffreyNo ratings yet

- Karvy Stock Broking LTDDocument2 pagesKarvy Stock Broking LTDMayank KumarNo ratings yet

- Lowe Ruling (BIR Ruling (DA - (C-283) 705-09)Document3 pagesLowe Ruling (BIR Ruling (DA - (C-283) 705-09)Kriszan ManiponNo ratings yet

- Bir RulingDocument4 pagesBir Rulingdranreb ursabiaNo ratings yet

- Tradewise Tax PNL ReportDocument47 pagesTradewise Tax PNL ReportSamir KumarNo ratings yet

- RFQ - M40 Milton Tactical Boots PDFDocument19 pagesRFQ - M40 Milton Tactical Boots PDFSkhumbuzo Macinga0% (1)

- RR 04-08 (Sale of RP)Document7 pagesRR 04-08 (Sale of RP)joefieNo ratings yet

- 1st Semester Transfer Taxation Module 5 Estate Tax Credit and Administrative ProvisionDocument5 pages1st Semester Transfer Taxation Module 5 Estate Tax Credit and Administrative ProvisionJames ScoldNo ratings yet

- Tenant AdvisoryDocument1 pageTenant AdvisoryJanetNo ratings yet

- Other Percentage TaxDocument58 pagesOther Percentage TaxApple AppleNo ratings yet

- Purchase of Real PropertyDocument5 pagesPurchase of Real PropertyBogart D AkitaNo ratings yet

- 5701-1991-Conveyance of The Real Property by The20210505-12-1o05w8wDocument2 pages5701-1991-Conveyance of The Real Property by The20210505-12-1o05w8wCarlo AlfonsoNo ratings yet

- BIR - REIT Tax RegulationsDocument23 pagesBIR - REIT Tax RegulationsDianne ArpasNo ratings yet

- SG ITAD Ruling No. 019-03Document4 pagesSG ITAD Ruling No. 019-03Paul Angelo TombocNo ratings yet

- Bir 2306Document6 pagesBir 2306RodnieGubatonNo ratings yet

- Salient Features of TRAIN LawDocument11 pagesSalient Features of TRAIN LawTiffany TuñacaoNo ratings yet

- Exhibit C - RegFeesDocument3 pagesExhibit C - RegFeesRonald Henry Montoya CubasNo ratings yet

- Item No Description Make Part No Country of Origin Unit Price in OMR QTY UOM Total Price in OMRDocument2 pagesItem No Description Make Part No Country of Origin Unit Price in OMR QTY UOM Total Price in OMRMohammad MudassarNo ratings yet

- Income Taxes For Individuals CA5109 Income Taxation Prepared By: Joseph Angelo B. OgrimenDocument18 pagesIncome Taxes For Individuals CA5109 Income Taxation Prepared By: Joseph Angelo B. Ogrimenlayla scotNo ratings yet

- Pa Tax Brief - November 2019Document10 pagesPa Tax Brief - November 2019Teresita TibayanNo ratings yet

- TOR VillaJosefina Final Re Bid2018Document23 pagesTOR VillaJosefina Final Re Bid2018Riezza Angelie Serrano ZuluetaNo ratings yet

- Rmo 15-2003Document68 pagesRmo 15-2003rodrigoNo ratings yet

- Articles About VAT Zero-RatingDocument8 pagesArticles About VAT Zero-RatingkmoNo ratings yet

- KBT Proposal SheetDocument14 pagesKBT Proposal SheetSouvik BakshiNo ratings yet

- Kepco vs. CirDocument2 pagesKepco vs. CirCaroline A. LegaspinoNo ratings yet

- 2008-BIR Ruling (DA - C-182 559-08)Document8 pages2008-BIR Ruling (DA - C-182 559-08)Jay MirandaNo ratings yet

- Guide When Buying Real Estate in The PhilippinesDocument1 pageGuide When Buying Real Estate in The PhilippinesER O'PlaneNo ratings yet

- Value Added TaxDocument44 pagesValue Added TaxDa Yani ChristeeneNo ratings yet

- Quotation: Customer Code: 10009469 Information VAT Number - 300055945410003Document2 pagesQuotation: Customer Code: 10009469 Information VAT Number - 300055945410003Marcial Jr. MilitanteNo ratings yet

- Direct Taxes Training Material HNL 15032023Document27 pagesDirect Taxes Training Material HNL 15032023fa6No ratings yet

- BIR Ruling No. 340-11 - E-BooksDocument5 pagesBIR Ruling No. 340-11 - E-BooksCkey ArNo ratings yet

- 20 Panasonic Communications vs. CIRDocument10 pages20 Panasonic Communications vs. CIRJohn BernalNo ratings yet

- 2012 ITAD - BIR - Ruling - No. - 092 1220210505 11 1ig3ujmDocument4 pages2012 ITAD - BIR - Ruling - No. - 092 1220210505 11 1ig3ujmrian.lee.b.tiangcoNo ratings yet

- Income Tax ChangesDocument30 pagesIncome Tax ChangesColors of LifeNo ratings yet

- BIR Ruling No. 015-12Document5 pagesBIR Ruling No. 015-12nikkaremullaNo ratings yet

- Rmo 1981Document228 pagesRmo 1981Mary graceNo ratings yet

- Crypto Taxation in USA: A Comprehensive Guide to Navigating Digital Assets and TaxationFrom EverandCrypto Taxation in USA: A Comprehensive Guide to Navigating Digital Assets and TaxationNo ratings yet

- How to Do a 1031 Exchange of Real Estate: Using a 1031 Qualified Intermediary (Qi) 2Nd EditionFrom EverandHow to Do a 1031 Exchange of Real Estate: Using a 1031 Qualified Intermediary (Qi) 2Nd EditionNo ratings yet

- RTC Courts ContactDocument317 pagesRTC Courts ContactAtty Rester John NonatoNo ratings yet

- WillexampleDocument7 pagesWillexampleAtty Rester John NonatoNo ratings yet

- BIR Ruling 419-07Document1 pageBIR Ruling 419-07Atty Rester John NonatoNo ratings yet

- Breach of TrustDocument4 pagesBreach of TrustAtty Rester John NonatoNo ratings yet

- DAO30Document24 pagesDAO30Atty Rester John NonatoNo ratings yet

- Checklist To Lift Order of Revocation-1Document5 pagesChecklist To Lift Order of Revocation-1Atty Rester John NonatoNo ratings yet

- Topic Insurance LawDocument28 pagesTopic Insurance LawAtty Rester John NonatoNo ratings yet

- Power Supply AgreementDocument11 pagesPower Supply AgreementAtty Rester John NonatoNo ratings yet

- 2009IPPDocument4 pages2009IPPAtty Rester John NonatoNo ratings yet

- Topic Bouncing Checks LawDocument29 pagesTopic Bouncing Checks LawAtty Rester John NonatoNo ratings yet

- 2009 RulingsDocument525 pages2009 RulingsAtty Rester John NonatoNo ratings yet

- Topic CorpGovernanceDocument65 pagesTopic CorpGovernanceAtty Rester John NonatoNo ratings yet

- Topic Dissolution and Winding UpDocument24 pagesTopic Dissolution and Winding UpAtty Rester John NonatoNo ratings yet

- Topic PartnershipDocument36 pagesTopic PartnershipAtty Rester John NonatoNo ratings yet

- Amnesty Tax Payment Form: Kawanihan NG Rentas InternasDocument1 pageAmnesty Tax Payment Form: Kawanihan NG Rentas InternasAtty Rester John NonatoNo ratings yet

- Application For Relief From Double Taxation: (Name of Contracting State)Document2 pagesApplication For Relief From Double Taxation: (Name of Contracting State)Atty Rester John NonatoNo ratings yet

- BIR Form No 0901Document2 pagesBIR Form No 0901Atty Rester John NonatoNo ratings yet

- BIR Violations ChecklistDocument1 pageBIR Violations ChecklistAtty Rester John NonatoNo ratings yet

- Malaysia Regional Area StudyDocument28 pagesMalaysia Regional Area StudyAtty Rester John NonatoNo ratings yet

- South China Sea Arbitration DecisionDocument23 pagesSouth China Sea Arbitration DecisionAtty Rester John NonatoNo ratings yet

- Chapter 1 - True or False Part 2Document3 pagesChapter 1 - True or False Part 2Chloe Gabriel Evangeline ChaseNo ratings yet

- Residence PermitDocument19 pagesResidence PermitAras KarlıdağNo ratings yet

- Notice and Declaration of Bank)Document3 pagesNotice and Declaration of Bank)sspikes100% (3)

- Types of Debentures: Redeemable and Irredeemable (Perpetual) DebenturesDocument3 pagesTypes of Debentures: Redeemable and Irredeemable (Perpetual) DebentureshumanNo ratings yet

- ALM Policy of HFCDocument13 pagesALM Policy of HFCSrinivasan IyerNo ratings yet

- Shareholders EquityDocument11 pagesShareholders EquityJasmine ActaNo ratings yet

- The Psychology of Money-9dbc86Document25 pagesThe Psychology of Money-9dbc86Shakti Tandon100% (5)

- USAA Nasdaq-100 Index Fund - USNQX - 4Q 2022Document2 pagesUSAA Nasdaq-100 Index Fund - USNQX - 4Q 2022ag rNo ratings yet

- Your Magic NumberDocument59 pagesYour Magic NumberGregNo ratings yet

- Abuse of Double Taxation Avoidance Agreement by Treaty PART-IDocument31 pagesAbuse of Double Taxation Avoidance Agreement by Treaty PART-IPJ 123No ratings yet

- InvoicehdDocument1 pageInvoicehdKiran RockNo ratings yet

- M. M. Rahman Co.: Statement of Financial PositionDocument5 pagesM. M. Rahman Co.: Statement of Financial PositionAsiful IslamNo ratings yet

- Moot ProblemDocument12 pagesMoot ProblemAchin JanaNo ratings yet

- Zimbabwe Stock Exchange Pricelist: The Complete List of ZSE Indices Can Be Obtained From The ZSE Website: WWW - Zse.co - ZWDocument1 pageZimbabwe Stock Exchange Pricelist: The Complete List of ZSE Indices Can Be Obtained From The ZSE Website: WWW - Zse.co - ZWBen GanzwaNo ratings yet

- Payroll Processing Term PaperDocument20 pagesPayroll Processing Term Papermanpreet_singh991No ratings yet

- DRAFT First Semester 2023 2024 Examination Timetable NewDocument16 pagesDRAFT First Semester 2023 2024 Examination Timetable NewpalngnenchikaNo ratings yet

- IBC Notes PDFDocument46 pagesIBC Notes PDFbhioNo ratings yet

- Lease Accounting LessorDocument13 pagesLease Accounting LessorIts meh SushiNo ratings yet

- Chapter 6: Risk and Return: Prof. Dr. Tamer Mohamed ShahwanDocument24 pagesChapter 6: Risk and Return: Prof. Dr. Tamer Mohamed ShahwanDalia ElarabyNo ratings yet

- Chapter 4Document10 pagesChapter 4Seid KassawNo ratings yet

- Scan 14 Jun 2021Document5 pagesScan 14 Jun 2021Regina ZuluNo ratings yet

- Discounted Cash Flow AnalysisDocument13 pagesDiscounted Cash Flow AnalysisJack Jacinto67% (3)

- An Internship Report On General Banking Operation of EXIM Bank LimitedDocument64 pagesAn Internship Report On General Banking Operation of EXIM Bank LimitedNafiz FahimNo ratings yet

- Ethical Practices of Financial Services OrganisationsDocument20 pagesEthical Practices of Financial Services OrganisationsKrutika Likhite100% (1)

- Functions of Integrated TreasuryDocument2 pagesFunctions of Integrated TreasuryBhavin Patel.0% (1)

- APC Ch10solDocument9 pagesAPC Ch10solAzul Lacson100% (2)

- Apollo Medicine InvoiceNov 8 2022-19-03Document1 pageApollo Medicine InvoiceNov 8 2022-19-03Rajesh GandhiNo ratings yet