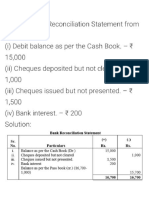

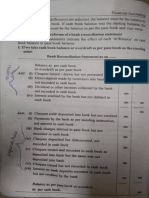

Unit-Iii Bank Reconciliation Statement Debit (+) Credit (-) Credit (-) Debit (+)

Unit-Iii Bank Reconciliation Statement Debit (+) Credit (-) Credit (-) Debit (+)

You might also like

- Auditing Concept Problems Cash and Cash EquivalentDocument7 pagesAuditing Concept Problems Cash and Cash EquivalentJoanah TayamenNo ratings yet

- Introduction To Investment BankingDocument37 pagesIntroduction To Investment BankingVaidyanathan RavichandranNo ratings yet

- Cash and Cash EquivalentDocument32 pagesCash and Cash EquivalentArbie D. DecimioNo ratings yet

- Reviewer Intacc 1n2Document58 pagesReviewer Intacc 1n2John100% (1)

- FarDocument8 pagesFarnivea gumayagay71% (7)

- Practical - Bank Reconciliation StatementDocument5 pagesPractical - Bank Reconciliation StatementUniversal SoldierNo ratings yet

- BRS ProblemsDocument28 pagesBRS ProblemsKutbuddin JawadwalaNo ratings yet

- Prepare Bank Reconciliation Statement From The Following: (I) Debit Balance As Per The Cash BookDocument10 pagesPrepare Bank Reconciliation Statement From The Following: (I) Debit Balance As Per The Cash BookPragya ShuklaNo ratings yet

- Chapter 9 - Bank Reconciliation StatementDocument15 pagesChapter 9 - Bank Reconciliation StatementSaurabh GohanNo ratings yet

- Bank Reconciliation StatementDocument33 pagesBank Reconciliation StatementMd TahirNo ratings yet

- BRS PDFDocument8 pagesBRS PDFAnshumanNo ratings yet

- CA Foundation June 23 BRS Problem - CTC ClassesDocument2 pagesCA Foundation June 23 BRS Problem - CTC ClassesMohit SharmaNo ratings yet

- Bank Reconcilaition Statement Problems PDF 1 4 PDFDocument4 pagesBank Reconcilaition Statement Problems PDF 1 4 PDFHakim JanNo ratings yet

- BRS 2Document2 pagesBRS 2Aarnav SharmaNo ratings yet

- BRS WorksheetDocument8 pagesBRS WorksheetMayank VermaNo ratings yet

- Bank ReconciliationDocument6 pagesBank Reconciliationnaih marchessaNo ratings yet

- Bank Reconciliation Statement: Gravity 4 CaDocument13 pagesBank Reconciliation Statement: Gravity 4 CaAmit ChaudhryNo ratings yet

- Bank Re-Conciliation QuesDocument3 pagesBank Re-Conciliation QuesGarima GarimaNo ratings yet

- Accounts RTP CA Foundation May 2020Document31 pagesAccounts RTP CA Foundation May 2020YashNo ratings yet

- Account Past Questions Compilation (2009june - 2022 June)Document319 pagesAccount Past Questions Compilation (2009june - 2022 June)Arjun AdhikariNo ratings yet

- Quiz 1Document3 pagesQuiz 1Carmi FeceroNo ratings yet

- Cash and Cash Equivalent Tutorial PDFDocument3 pagesCash and Cash Equivalent Tutorial PDFClara San MiguelNo ratings yet

- Additional Illustrations-13Document5 pagesAdditional Illustrations-13Deepak YadavNo ratings yet

- Unit 8 Bank Reconciliation StatementDocument7 pagesUnit 8 Bank Reconciliation StatementUrja JoshiNo ratings yet

- Bank Reconciliation - SolutionsDocument6 pagesBank Reconciliation - SolutionsNIAZ HUSSAIN100% (1)

- P01. Cash and Cash Equivalents AnswersDocument8 pagesP01. Cash and Cash Equivalents AnswersIosif DzhugasviliNo ratings yet

- Balance: Financial AccountingDocument6 pagesBalance: Financial AccountingravinraghzNo ratings yet

- Paper - 1: Principles & Practice of Accounting Questions True and FalseDocument31 pagesPaper - 1: Principles & Practice of Accounting Questions True and FalseUnknown 1No ratings yet

- FAR 0 Bank Recon and Proof of Cash Drill ProblemsDocument6 pagesFAR 0 Bank Recon and Proof of Cash Drill Problemsyeeaahh56No ratings yet

- AP - Quiz 01 (UCP)Document8 pagesAP - Quiz 01 (UCP)CrestinaNo ratings yet

- 4.CA Foundation Test 4Document6 pages4.CA Foundation Test 4Nived Narayan PNo ratings yet

- Assignment BRSDocument2 pagesAssignment BRSveydantsharma42No ratings yet

- MOD 01 - Cash and Cash EquivalentsDocument3 pagesMOD 01 - Cash and Cash EquivalentsIrish VargasNo ratings yet

- FAR103 - FAR - 203 (A) - Cash and Cash EquivalentsDocument3 pagesFAR103 - FAR - 203 (A) - Cash and Cash EquivalentsDan Andrei BongoNo ratings yet

- Adobe Scan 05 Jan 2024Document2 pagesAdobe Scan 05 Jan 2024Harshit GargNo ratings yet

- Cce Board WorkDocument3 pagesCce Board WorkNicole VinaraoNo ratings yet

- Assessment Task 1-1Document10 pagesAssessment Task 1-1hahahahaNo ratings yet

- Bank Reconciliation StatementDocument3 pagesBank Reconciliation StatementKritika HarlalkaNo ratings yet

- Financial AssetsDocument127 pagesFinancial Assetscherry blossomNo ratings yet

- Tsgrewal BRSDocument11 pagesTsgrewal BRSDhruvNo ratings yet

- Cash Cash Equivalent Bank ReconDocument4 pagesCash Cash Equivalent Bank Reconmavie arellanoNo ratings yet

- Mock Prelim - Intermediate AcctDocument9 pagesMock Prelim - Intermediate AcctNikki LabialNo ratings yet

- Bank Reconciliation StatementDocument12 pagesBank Reconciliation StatementBhuvan PrajapatiNo ratings yet

- FAR - CASH ProbDocument2 pagesFAR - CASH Prob2216391No ratings yet

- AACONAPPS2 Quiz No. 01 - Audit of Cash Problem Questions (2022)Document4 pagesAACONAPPS2 Quiz No. 01 - Audit of Cash Problem Questions (2022)Dawson Dela CruzNo ratings yet

- Cash and Cash Equivalents Quizzer 1Document5 pagesCash and Cash Equivalents Quizzer 1yna kyleneNo ratings yet

- Cash and Cash EquivalentsDocument3 pagesCash and Cash EquivalentsBeat KarbNo ratings yet

- Submitted To: Submitted byDocument33 pagesSubmitted To: Submitted byaanaughtyNo ratings yet

- CCE Bank Recon DISCUSSION EXERCISESDocument2 pagesCCE Bank Recon DISCUSSION EXERCISESGlance Piscasio CruzNo ratings yet

- Cash and Cash EquivalentsDocument3 pagesCash and Cash EquivalentsShiela Mae SangidNo ratings yet

- ACCTG 102 Practice Sets Quizzes ExamsDocument25 pagesACCTG 102 Practice Sets Quizzes ExamsheythereitsclaireNo ratings yet

- CashDocument6 pagesCashrosemariesollegue888No ratings yet

- FINANCIAL ACCOUNTING - Cash To Receivables Problems and SolutionsDocument8 pagesFINANCIAL ACCOUNTING - Cash To Receivables Problems and Solutionsstan iKONNo ratings yet

- Paper - 1: Principles & Practice of Accounting Questions True and FalseDocument32 pagesPaper - 1: Principles & Practice of Accounting Questions True and FalseShaindra SinghNo ratings yet

- Proof+of+Cash ProblemsDocument2 pagesProof+of+Cash ProblemshelaihjsNo ratings yet

- Proof of Cash ProblemsDocument2 pagesProof of Cash ProblemsSamantha Marie Arevalo100% (1)

- BA3 M KIT Chapter 16Document4 pagesBA3 M KIT Chapter 16Nivneth PeirisNo ratings yet

- Bank Reconciliation StatementDocument4 pagesBank Reconciliation StatementProttasha AsifNo ratings yet

- Bank Reconciliation Statement August 17Document10 pagesBank Reconciliation Statement August 17NO NAMENo ratings yet

- FM Quiz Set ADocument3 pagesFM Quiz Set AShaira Mae TomasNo ratings yet

- BCom Second Year Assignments PDFDocument2 pagesBCom Second Year Assignments PDFKotaiah Avula75% (8)

- AGNPO The Budget ProcessDocument57 pagesAGNPO The Budget ProcessJassyNo ratings yet

- CC Two-Wheeler-LoansDocument29 pagesCC Two-Wheeler-LoansRight ClickNo ratings yet

- MSME Definition by RBIDocument8 pagesMSME Definition by RBIRahul YadavNo ratings yet

- A Study On Brand Awareness of Financial Products With Special Reference To Agile Capital ServicesDocument71 pagesA Study On Brand Awareness of Financial Products With Special Reference To Agile Capital Servicesjassi nishadNo ratings yet

- VOPAK Jaarverslag2010 PDFDocument180 pagesVOPAK Jaarverslag2010 PDFJasper Laarmans Teixeira de MattosNo ratings yet

- Match Each Annual Report Section With Its Description Annual ReportDocument1 pageMatch Each Annual Report Section With Its Description Annual ReportLet's Talk With HassanNo ratings yet

- 10 - Borrowing Costs PS 12edDocument15 pages10 - Borrowing Costs PS 12edbusiness docNo ratings yet

- Notes LAW OF TAXATIONDocument266 pagesNotes LAW OF TAXATIONsadia zaahirNo ratings yet

- Infographic Bank Issue Fin360Document1 pageInfographic Bank Issue Fin360NUR SYAFIQAH DAYANA MOHD SUFFIANNo ratings yet

- Absorption CostingDocument32 pagesAbsorption Costingsknco50% (2)

- Research Report Bajaj Finance LTDDocument8 pagesResearch Report Bajaj Finance LTDvivekNo ratings yet

- Apr 2023Document1 pageApr 2023saurabhjaNo ratings yet

- Oman Oil Balance SheetDocument27 pagesOman Oil Balance Sheeta.hasan670100% (1)

- Accounts Mock Test May 2019Document18 pagesAccounts Mock Test May 2019poojitha reddyNo ratings yet

- Vol 5-1 and 2..akram Khan..Performance Auditing For Islamic Banks..DpDocument15 pagesVol 5-1 and 2..akram Khan..Performance Auditing For Islamic Banks..Dpbabak1897No ratings yet

- QuizDocument4 pagesQuizPraveer BoseNo ratings yet

- Chapter 10Document26 pagesChapter 10Minh Ánh NguyênNo ratings yet

- Accounting 21 Financial Accounting and Reporting Part 1Document5 pagesAccounting 21 Financial Accounting and Reporting Part 1Faith BariasNo ratings yet

- MBFS Unit 1Document48 pagesMBFS Unit 1pearlksrNo ratings yet

- Securities Laws in IndiaDocument19 pagesSecurities Laws in IndiaBhawna Pamnani100% (1)

- Risk Management For MBA StudentsDocument28 pagesRisk Management For MBA StudentsMuneeb Sada50% (2)

- AOi XTIANDocument4 pagesAOi XTIANArste GimoNo ratings yet

- Risk & Return: Chapte RDocument52 pagesRisk & Return: Chapte RMohammad Salim HossainNo ratings yet

- Trade Indicator Handbook FINAL 2013Document138 pagesTrade Indicator Handbook FINAL 2013Santiago.VRNo ratings yet

- Tax Chapter 3 SummaryDocument4 pagesTax Chapter 3 SummaryishaNo ratings yet

- Roosevelt DEcision of Bank HolidayDocument12 pagesRoosevelt DEcision of Bank HolidaySheetal ChauhanNo ratings yet

- CF Industries Presentation May 2016Document23 pagesCF Industries Presentation May 2016red cornerNo ratings yet

- 6 Enano-Bote v. Alvarez, G.R. No. 223572, (November 10, 2020)Document13 pages6 Enano-Bote v. Alvarez, G.R. No. 223572, (November 10, 2020)Marlito Joshua AmistosoNo ratings yet

Download as docx, pdf, or txt

You might also like

- Auditing Concept Problems Cash and Cash EquivalentDocument7 pagesAuditing Concept Problems Cash and Cash EquivalentJoanah TayamenNo ratings yet

- Introduction To Investment BankingDocument37 pagesIntroduction To Investment BankingVaidyanathan RavichandranNo ratings yet

- Cash and Cash EquivalentDocument32 pagesCash and Cash EquivalentArbie D. DecimioNo ratings yet

- Reviewer Intacc 1n2Document58 pagesReviewer Intacc 1n2John100% (1)

- FarDocument8 pagesFarnivea gumayagay71% (7)

- Practical - Bank Reconciliation StatementDocument5 pagesPractical - Bank Reconciliation StatementUniversal SoldierNo ratings yet

- BRS ProblemsDocument28 pagesBRS ProblemsKutbuddin JawadwalaNo ratings yet

- Prepare Bank Reconciliation Statement From The Following: (I) Debit Balance As Per The Cash BookDocument10 pagesPrepare Bank Reconciliation Statement From The Following: (I) Debit Balance As Per The Cash BookPragya ShuklaNo ratings yet

- Chapter 9 - Bank Reconciliation StatementDocument15 pagesChapter 9 - Bank Reconciliation StatementSaurabh GohanNo ratings yet

- Bank Reconciliation StatementDocument33 pagesBank Reconciliation StatementMd TahirNo ratings yet

- BRS PDFDocument8 pagesBRS PDFAnshumanNo ratings yet

- CA Foundation June 23 BRS Problem - CTC ClassesDocument2 pagesCA Foundation June 23 BRS Problem - CTC ClassesMohit SharmaNo ratings yet

- Bank Reconcilaition Statement Problems PDF 1 4 PDFDocument4 pagesBank Reconcilaition Statement Problems PDF 1 4 PDFHakim JanNo ratings yet

- BRS 2Document2 pagesBRS 2Aarnav SharmaNo ratings yet

- BRS WorksheetDocument8 pagesBRS WorksheetMayank VermaNo ratings yet

- Bank ReconciliationDocument6 pagesBank Reconciliationnaih marchessaNo ratings yet

- Bank Reconciliation Statement: Gravity 4 CaDocument13 pagesBank Reconciliation Statement: Gravity 4 CaAmit ChaudhryNo ratings yet

- Bank Re-Conciliation QuesDocument3 pagesBank Re-Conciliation QuesGarima GarimaNo ratings yet

- Accounts RTP CA Foundation May 2020Document31 pagesAccounts RTP CA Foundation May 2020YashNo ratings yet

- Account Past Questions Compilation (2009june - 2022 June)Document319 pagesAccount Past Questions Compilation (2009june - 2022 June)Arjun AdhikariNo ratings yet

- Quiz 1Document3 pagesQuiz 1Carmi FeceroNo ratings yet

- Cash and Cash Equivalent Tutorial PDFDocument3 pagesCash and Cash Equivalent Tutorial PDFClara San MiguelNo ratings yet

- Additional Illustrations-13Document5 pagesAdditional Illustrations-13Deepak YadavNo ratings yet

- Unit 8 Bank Reconciliation StatementDocument7 pagesUnit 8 Bank Reconciliation StatementUrja JoshiNo ratings yet

- Bank Reconciliation - SolutionsDocument6 pagesBank Reconciliation - SolutionsNIAZ HUSSAIN100% (1)

- P01. Cash and Cash Equivalents AnswersDocument8 pagesP01. Cash and Cash Equivalents AnswersIosif DzhugasviliNo ratings yet

- Balance: Financial AccountingDocument6 pagesBalance: Financial AccountingravinraghzNo ratings yet

- Paper - 1: Principles & Practice of Accounting Questions True and FalseDocument31 pagesPaper - 1: Principles & Practice of Accounting Questions True and FalseUnknown 1No ratings yet

- FAR 0 Bank Recon and Proof of Cash Drill ProblemsDocument6 pagesFAR 0 Bank Recon and Proof of Cash Drill Problemsyeeaahh56No ratings yet

- AP - Quiz 01 (UCP)Document8 pagesAP - Quiz 01 (UCP)CrestinaNo ratings yet

- 4.CA Foundation Test 4Document6 pages4.CA Foundation Test 4Nived Narayan PNo ratings yet

- Assignment BRSDocument2 pagesAssignment BRSveydantsharma42No ratings yet

- MOD 01 - Cash and Cash EquivalentsDocument3 pagesMOD 01 - Cash and Cash EquivalentsIrish VargasNo ratings yet

- FAR103 - FAR - 203 (A) - Cash and Cash EquivalentsDocument3 pagesFAR103 - FAR - 203 (A) - Cash and Cash EquivalentsDan Andrei BongoNo ratings yet

- Adobe Scan 05 Jan 2024Document2 pagesAdobe Scan 05 Jan 2024Harshit GargNo ratings yet

- Cce Board WorkDocument3 pagesCce Board WorkNicole VinaraoNo ratings yet

- Assessment Task 1-1Document10 pagesAssessment Task 1-1hahahahaNo ratings yet

- Bank Reconciliation StatementDocument3 pagesBank Reconciliation StatementKritika HarlalkaNo ratings yet

- Financial AssetsDocument127 pagesFinancial Assetscherry blossomNo ratings yet

- Tsgrewal BRSDocument11 pagesTsgrewal BRSDhruvNo ratings yet

- Cash Cash Equivalent Bank ReconDocument4 pagesCash Cash Equivalent Bank Reconmavie arellanoNo ratings yet

- Mock Prelim - Intermediate AcctDocument9 pagesMock Prelim - Intermediate AcctNikki LabialNo ratings yet

- Bank Reconciliation StatementDocument12 pagesBank Reconciliation StatementBhuvan PrajapatiNo ratings yet

- FAR - CASH ProbDocument2 pagesFAR - CASH Prob2216391No ratings yet

- AACONAPPS2 Quiz No. 01 - Audit of Cash Problem Questions (2022)Document4 pagesAACONAPPS2 Quiz No. 01 - Audit of Cash Problem Questions (2022)Dawson Dela CruzNo ratings yet

- Cash and Cash Equivalents Quizzer 1Document5 pagesCash and Cash Equivalents Quizzer 1yna kyleneNo ratings yet

- Cash and Cash EquivalentsDocument3 pagesCash and Cash EquivalentsBeat KarbNo ratings yet

- Submitted To: Submitted byDocument33 pagesSubmitted To: Submitted byaanaughtyNo ratings yet

- CCE Bank Recon DISCUSSION EXERCISESDocument2 pagesCCE Bank Recon DISCUSSION EXERCISESGlance Piscasio CruzNo ratings yet

- Cash and Cash EquivalentsDocument3 pagesCash and Cash EquivalentsShiela Mae SangidNo ratings yet

- ACCTG 102 Practice Sets Quizzes ExamsDocument25 pagesACCTG 102 Practice Sets Quizzes ExamsheythereitsclaireNo ratings yet

- CashDocument6 pagesCashrosemariesollegue888No ratings yet

- FINANCIAL ACCOUNTING - Cash To Receivables Problems and SolutionsDocument8 pagesFINANCIAL ACCOUNTING - Cash To Receivables Problems and Solutionsstan iKONNo ratings yet

- Paper - 1: Principles & Practice of Accounting Questions True and FalseDocument32 pagesPaper - 1: Principles & Practice of Accounting Questions True and FalseShaindra SinghNo ratings yet

- Proof+of+Cash ProblemsDocument2 pagesProof+of+Cash ProblemshelaihjsNo ratings yet

- Proof of Cash ProblemsDocument2 pagesProof of Cash ProblemsSamantha Marie Arevalo100% (1)

- BA3 M KIT Chapter 16Document4 pagesBA3 M KIT Chapter 16Nivneth PeirisNo ratings yet

- Bank Reconciliation StatementDocument4 pagesBank Reconciliation StatementProttasha AsifNo ratings yet

- Bank Reconciliation Statement August 17Document10 pagesBank Reconciliation Statement August 17NO NAMENo ratings yet

- FM Quiz Set ADocument3 pagesFM Quiz Set AShaira Mae TomasNo ratings yet

- BCom Second Year Assignments PDFDocument2 pagesBCom Second Year Assignments PDFKotaiah Avula75% (8)

- AGNPO The Budget ProcessDocument57 pagesAGNPO The Budget ProcessJassyNo ratings yet

- CC Two-Wheeler-LoansDocument29 pagesCC Two-Wheeler-LoansRight ClickNo ratings yet

- MSME Definition by RBIDocument8 pagesMSME Definition by RBIRahul YadavNo ratings yet

- A Study On Brand Awareness of Financial Products With Special Reference To Agile Capital ServicesDocument71 pagesA Study On Brand Awareness of Financial Products With Special Reference To Agile Capital Servicesjassi nishadNo ratings yet

- VOPAK Jaarverslag2010 PDFDocument180 pagesVOPAK Jaarverslag2010 PDFJasper Laarmans Teixeira de MattosNo ratings yet

- Match Each Annual Report Section With Its Description Annual ReportDocument1 pageMatch Each Annual Report Section With Its Description Annual ReportLet's Talk With HassanNo ratings yet

- 10 - Borrowing Costs PS 12edDocument15 pages10 - Borrowing Costs PS 12edbusiness docNo ratings yet

- Notes LAW OF TAXATIONDocument266 pagesNotes LAW OF TAXATIONsadia zaahirNo ratings yet

- Infographic Bank Issue Fin360Document1 pageInfographic Bank Issue Fin360NUR SYAFIQAH DAYANA MOHD SUFFIANNo ratings yet

- Absorption CostingDocument32 pagesAbsorption Costingsknco50% (2)

- Research Report Bajaj Finance LTDDocument8 pagesResearch Report Bajaj Finance LTDvivekNo ratings yet

- Apr 2023Document1 pageApr 2023saurabhjaNo ratings yet

- Oman Oil Balance SheetDocument27 pagesOman Oil Balance Sheeta.hasan670100% (1)

- Accounts Mock Test May 2019Document18 pagesAccounts Mock Test May 2019poojitha reddyNo ratings yet

- Vol 5-1 and 2..akram Khan..Performance Auditing For Islamic Banks..DpDocument15 pagesVol 5-1 and 2..akram Khan..Performance Auditing For Islamic Banks..Dpbabak1897No ratings yet

- QuizDocument4 pagesQuizPraveer BoseNo ratings yet

- Chapter 10Document26 pagesChapter 10Minh Ánh NguyênNo ratings yet

- Accounting 21 Financial Accounting and Reporting Part 1Document5 pagesAccounting 21 Financial Accounting and Reporting Part 1Faith BariasNo ratings yet

- MBFS Unit 1Document48 pagesMBFS Unit 1pearlksrNo ratings yet

- Securities Laws in IndiaDocument19 pagesSecurities Laws in IndiaBhawna Pamnani100% (1)

- Risk Management For MBA StudentsDocument28 pagesRisk Management For MBA StudentsMuneeb Sada50% (2)

- AOi XTIANDocument4 pagesAOi XTIANArste GimoNo ratings yet

- Risk & Return: Chapte RDocument52 pagesRisk & Return: Chapte RMohammad Salim HossainNo ratings yet

- Trade Indicator Handbook FINAL 2013Document138 pagesTrade Indicator Handbook FINAL 2013Santiago.VRNo ratings yet

- Tax Chapter 3 SummaryDocument4 pagesTax Chapter 3 SummaryishaNo ratings yet

- Roosevelt DEcision of Bank HolidayDocument12 pagesRoosevelt DEcision of Bank HolidaySheetal ChauhanNo ratings yet

- CF Industries Presentation May 2016Document23 pagesCF Industries Presentation May 2016red cornerNo ratings yet

- 6 Enano-Bote v. Alvarez, G.R. No. 223572, (November 10, 2020)Document13 pages6 Enano-Bote v. Alvarez, G.R. No. 223572, (November 10, 2020)Marlito Joshua AmistosoNo ratings yet