Download as pdf or txt

You might also like

- Ewhore 2Document29 pagesEwhore 2Camilo lopez100% (1)

- VN CB Vietnam Consumer Retail 2019Document32 pagesVN CB Vietnam Consumer Retail 2019Huy Võ QuangNo ratings yet

- Svo PP 2016 PDFDocument344 pagesSvo PP 2016 PDFkcchan7No ratings yet

- Thailand e Conomy Sea 2023 ReportDocument14 pagesThailand e Conomy Sea 2023 ReportMitsu BùiNo ratings yet

- Vietnam e Conomy Sea 2023 ReportDocument14 pagesVietnam e Conomy Sea 2023 ReportMitsu BùiNo ratings yet

- Vietnam e Conomy Sea 2023 Report Share by WorldLine TechnologyDocument14 pagesVietnam e Conomy Sea 2023 Report Share by WorldLine Technologyvan.vn0912No ratings yet

- Singapore e Conomy Sea 2023 ReportDocument6 pagesSingapore e Conomy Sea 2023 ReportMitsu BùiNo ratings yet

- Indonesia e Conomy Sea 2023 ReportDocument14 pagesIndonesia e Conomy Sea 2023 ReportDonyNo ratings yet

- Industry - Brochure - E-CommerceDocument9 pagesIndustry - Brochure - E-CommerceANo ratings yet

- FinTech Futures Industry Survey v1Document15 pagesFinTech Futures Industry Survey v1SORY TOURENo ratings yet

- IOH - Rakernas KADIN - Perkembangan Dan Masa Depan Talenta Digital Di IndonesiaDocument15 pagesIOH - Rakernas KADIN - Perkembangan Dan Masa Depan Talenta Digital Di IndonesiaKarang SuragabayaNo ratings yet

- China E-Commerce Platforms: Who Will Make Money in Lower-Tier Cities?Document54 pagesChina E-Commerce Platforms: Who Will Make Money in Lower-Tier Cities?Brandon TanNo ratings yet

- Startup Report 2018 PDFDocument35 pagesStartup Report 2018 PDFbenyhartoNo ratings yet

- Q1 2023 Trend ReportDocument27 pagesQ1 2023 Trend ReportBinh LongNo ratings yet

- Economie Numerique 4Document168 pagesEconomie Numerique 4Biggest JunjunNo ratings yet

- It Sector ReportDocument25 pagesIt Sector ReportAryan BhageriaNo ratings yet

- Thematic - Film Exhibition Industry - Outlook - Nov 2022Document16 pagesThematic - Film Exhibition Industry - Outlook - Nov 2022Saurabh SinghNo ratings yet

- JLL 2022 Year End ReportDocument16 pagesJLL 2022 Year End Reportabhish1984No ratings yet

- The Indian Media & Entertainment Industry 2019: Trends & Analysis - Past, Present & FutureDocument63 pagesThe Indian Media & Entertainment Industry 2019: Trends & Analysis - Past, Present & FutureSharvari ShankarNo ratings yet

- Zalando SE - CMD 2021 - Financial Deep DiveDocument16 pagesZalando SE - CMD 2021 - Financial Deep DivehaoNo ratings yet

- Ecommerce Industry AnalysisDocument14 pagesEcommerce Industry AnalysisJANARTHAN SANKARANNo ratings yet

- Study Id72509 Fmcg-In-VietnamDocument55 pagesStudy Id72509 Fmcg-In-VietnamThanh Luân Lê NguyễnNo ratings yet

- Acb - HSCDocument10 pagesAcb - HSCSeoNaYoungNo ratings yet

- Project Indium Discussion Material - VFDocument11 pagesProject Indium Discussion Material - VFApoorva ChandraNo ratings yet

- Ecommerce Is Growing Faster Than Ever Before: An Extract From The Statista Digital Economy Compass 2021Document41 pagesEcommerce Is Growing Faster Than Ever Before: An Extract From The Statista Digital Economy Compass 2021Jose A MijaresNo ratings yet

- Nielsen+Local+Audience+Insights+Report+ January+2023Document26 pagesNielsen+Local+Audience+Insights+Report+ January+2023nobelaungNo ratings yet

- RR Immediate Reform Agenda Imf and BeyondDocument122 pagesRR Immediate Reform Agenda Imf and BeyondSidra GhafoorNo ratings yet

- Accenture-Unlocking-Digital-Value-South Africa-Telecoms-Sector PDFDocument26 pagesAccenture-Unlocking-Digital-Value-South Africa-Telecoms-Sector PDFadityaNo ratings yet

- Vietnam Retailed 2019-Fix PDFDocument27 pagesVietnam Retailed 2019-Fix PDFXuan Khoa NguyenNo ratings yet

- The Customer Data Platform ReportDocument28 pagesThe Customer Data Platform ReportCommon UserNo ratings yet

- Demand AnalysisDocument8 pagesDemand AnalysisHagad, Angelica BA 2ANo ratings yet

- Primed For A Smooth Drive: SpeakersDocument15 pagesPrimed For A Smooth Drive: SpeakersJohn RegalNo ratings yet

- 2C2P-IDC-InfoBrief AP241267IB Final SmallDocument17 pages2C2P-IDC-InfoBrief AP241267IB Final Smalljefcheung19No ratings yet

- Africa Day Presentation VDefDocument30 pagesAfrica Day Presentation VDefBernard BiboumNo ratings yet

- PWC H1 2020 Global Crypto M&A Fundraising Report Oct 2020 PDFDocument26 pagesPWC H1 2020 Global Crypto M&A Fundraising Report Oct 2020 PDFForkLogNo ratings yet

- Unlocking Vietnam'S Fintech: Growth PotentialDocument31 pagesUnlocking Vietnam'S Fintech: Growth PotentialGia Han LeNo ratings yet

- Report E-Conomy SEA 2018 by Google Temasek 121418 CPSLJLQDocument32 pagesReport E-Conomy SEA 2018 by Google Temasek 121418 CPSLJLQPatricia OoiNo ratings yet

- 2022 SaaS Performance Reporting BenchmarksDocument24 pages2022 SaaS Performance Reporting BenchmarksDương Thị Lệ QuyênNo ratings yet

- MEM June 2020 - PPT - 2Document21 pagesMEM June 2020 - PPT - 2Kyaw SithuNo ratings yet

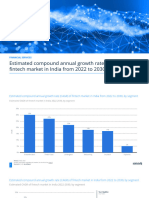

- Statistic - Id1372816 - Estimated Cagr of Fintech Market in India 2022 2030 by SegmentDocument8 pagesStatistic - Id1372816 - Estimated Cagr of Fintech Market in India 2022 2030 by SegmentGuilherme LustosaNo ratings yet

- Riding India's Digital Super-Cycle Saurabh Tripathi - Panel PresentationDocument13 pagesRiding India's Digital Super-Cycle Saurabh Tripathi - Panel Presentationgupta_pankajkr5626No ratings yet

- E Tailing Market - Clubfactory GMV - Ajio GMV - Redseer ConsultingDocument10 pagesE Tailing Market - Clubfactory GMV - Ajio GMV - Redseer ConsultingredseerNo ratings yet

- AC IR Deck August 2018 27 Slides VF PDFDocument27 pagesAC IR Deck August 2018 27 Slides VF PDFjohn lerry loberioNo ratings yet

- GroupM X Facebook Rural Day Whitepaper Report Shared by WorldLineDocument35 pagesGroupM X Facebook Rural Day Whitepaper Report Shared by WorldLineNhật LinhNo ratings yet

- GroupM X Facebook Rural Day Whitepaper Report Apr 15Document37 pagesGroupM X Facebook Rural Day Whitepaper Report Apr 15Trần Quốc CườngNo ratings yet

- E Commerce Research April 2023Document11 pagesE Commerce Research April 2023Hussain Bin Ali100% (1)

- 2023 Pss Overviewreport1 CareeraspirationsDocument29 pages2023 Pss Overviewreport1 CareeraspirationsarunNo ratings yet

- Fintech Emerging Don of Financial ServicesDocument23 pagesFintech Emerging Don of Financial Servicesavinash singhNo ratings yet

- PWC Global Crypto M A and Fundraising Report April 2020Document28 pagesPWC Global Crypto M A and Fundraising Report April 2020ForkLogNo ratings yet

- Annual Report 202021Document128 pagesAnnual Report 202021fddNo ratings yet

- FiinGroup Vietnam Consumer Finance Factsheet 2023Document16 pagesFiinGroup Vietnam Consumer Finance Factsheet 2023bondinginvestmentNo ratings yet

- PMAR Report 2021Document60 pagesPMAR Report 2021Parmvir SinghNo ratings yet

- PWC Vietnam Outlook enDocument10 pagesPWC Vietnam Outlook enPham Thi Phuong Anh (K16 HCM)No ratings yet

- PWC Vietnam Outlook enDocument10 pagesPWC Vietnam Outlook enQuynh VoNo ratings yet

- 2021 Impact of Change Forecast Highlights: COVID-19 Recovery and Impact On Future UtilizationDocument17 pages2021 Impact of Change Forecast Highlights: COVID-19 Recovery and Impact On Future UtilizationwahidNo ratings yet

- Indian Healthcare Industry To Surpass USD 130 BN by FY24Document5 pagesIndian Healthcare Industry To Surpass USD 130 BN by FY24Neelaj MaityNo ratings yet

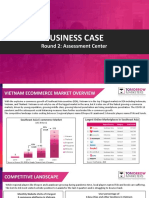

- Business Case: Round 2: Assessment CenterDocument9 pagesBusiness Case: Round 2: Assessment CenterMy Nguyen Thi Tra VOCFNo ratings yet

- DSInnovate Startup Report 2022Document79 pagesDSInnovate Startup Report 2022rudyjabbar23No ratings yet

- Delhi NCR: Industrial Q2 2020Document2 pagesDelhi NCR: Industrial Q2 2020Shivam SharmaNo ratings yet

- Edelweiss Focused Equity Fund - PresentationDocument47 pagesEdelweiss Focused Equity Fund - PresentationSudhir GotaNo ratings yet

- GovTech Maturity Index: The State of Public Sector Digital TransformationFrom EverandGovTech Maturity Index: The State of Public Sector Digital TransformationNo ratings yet

- Managing the Development of Digital Marketplaces in AsiaFrom EverandManaging the Development of Digital Marketplaces in AsiaNo ratings yet

- The Impact of New Nigerian Petroleum Industry Bill PIB 2021 On Government andDocument39 pagesThe Impact of New Nigerian Petroleum Industry Bill PIB 2021 On Government andIbrahim SalahudinNo ratings yet

- Investment in AssociateDocument2 pagesInvestment in AssociatebluemajaNo ratings yet

- UCCC & SPBCBA & SDHG College of BCA & IT, Surat M.C.Q. Question Bank of Macro Economics (English Medium)Document11 pagesUCCC & SPBCBA & SDHG College of BCA & IT, Surat M.C.Q. Question Bank of Macro Economics (English Medium)Parth RanaNo ratings yet

- ControlingDocument19 pagesControlingAhmad SanusiNo ratings yet

- Match The Two Parts of The SentencesDocument4 pagesMatch The Two Parts of The SentencesSorina MariaNo ratings yet

- FAC4863 NFA4863 Exam Paper 1 RequiredDocument3 pagesFAC4863 NFA4863 Exam Paper 1 RequiredNosipho NyathiNo ratings yet

- Trademark Info Corp PDFDocument1 pageTrademark Info Corp PDFHoward KnopfNo ratings yet

- Corporate BondDocument14 pagesCorporate BondRavi WadherNo ratings yet

- How To Save Money: To Use This For More Than One Time?"Document2 pagesHow To Save Money: To Use This For More Than One Time?"Han O100% (1)

- Treasury Management: Transmittal LetterDocument56 pagesTreasury Management: Transmittal Lettermashael abanmiNo ratings yet

- Codification Annex ING Format Descriptions Strategic v1.0 - tcm162-110480Document24 pagesCodification Annex ING Format Descriptions Strategic v1.0 - tcm162-110480rahul_agrawal165No ratings yet

- NON-ToD Bill PreviewDocument2 pagesNON-ToD Bill PreviewNaveen Kumar Singh78% (18)

- 06192023-Gateway Regency Studios-20e11Document4 pages06192023-Gateway Regency Studios-20e11joone M. gutierrezNo ratings yet

- Damodaram Sanjivayya National Law University Visakhapatnam, A.P., IndiaDocument32 pagesDamodaram Sanjivayya National Law University Visakhapatnam, A.P., IndiaKaushik NanduriNo ratings yet

- Modular POF Test2 QuestionDocument2 pagesModular POF Test2 QuestionMs TanNo ratings yet

- InteretrustDocument21 pagesInteretrustConstantin WellsNo ratings yet

- Open Economy MacroeconomicsDocument31 pagesOpen Economy MacroeconomicsMuhammadNo ratings yet

- Adv Acc Sol Manual 2008Document190 pagesAdv Acc Sol Manual 2008Khey Soniga RollanNo ratings yet

- Basic Business Finance AbmDocument26 pagesBasic Business Finance AbmK-Cube Morong100% (2)

- SAP Period End Closing ActivitiesDocument4 pagesSAP Period End Closing ActivitiessivasivasapNo ratings yet

- VXV DY23 LCD 47 C QGDocument2 pagesVXV DY23 LCD 47 C QGhp34thNo ratings yet

- Small Course About Bank and Cards LuciDocument5 pagesSmall Course About Bank and Cards LuciDougNo ratings yet

- Identifying and Analyzing Business TransactionsDocument2 pagesIdentifying and Analyzing Business TransactionsMardy DahuyagNo ratings yet

- Ccris BNM BookletDocument11 pagesCcris BNM BookletMuhamad AzmirNo ratings yet

- BoB - MITC - A4 Booklet - Ver 5.0 - 25JAN23 NewDocument8 pagesBoB - MITC - A4 Booklet - Ver 5.0 - 25JAN23 NewThakur KdNo ratings yet

- Assignment 1Document13 pagesAssignment 1Elin EkströmNo ratings yet

- Lju JK BlankDocument5 pagesLju JK Blankakun.gabut324No ratings yet

- Chapt 05Document12 pagesChapt 05Richa KothariNo ratings yet