Download as pdf or txt

You might also like

- Greenwald Earnings Power Value EPV Lecture SlidesDocument43 pagesGreenwald Earnings Power Value EPV Lecture SlidesOld School Value100% (13)

- Energy Policy: SciencedirectDocument11 pagesEnergy Policy: Sciencedirectdiyah100% (1)

- Steel Industry in Indi1Document24 pagesSteel Industry in Indi1Vatsal JainNo ratings yet

- 2015 Energy BalanceDocument133 pages2015 Energy BalanceIndunil WarnasooriyaNo ratings yet

- Trimegah Coal - Hello Old Economy, I'm BackDocument46 pagesTrimegah Coal - Hello Old Economy, I'm BackRizki Jauhari IndraNo ratings yet

- 2023.04.28 Press Release - ICSG Copper Market Forecast 2023-2024Document2 pages2023.04.28 Press Release - ICSG Copper Market Forecast 2023-2024Pedro Jose Cardenas PyastolovNo ratings yet

- World Bank View On Commodity Prices 02 13Document4 pagesWorld Bank View On Commodity Prices 02 13nafa nuksanNo ratings yet

- Demand Forecast of Fertilizer in PakistanDocument10 pagesDemand Forecast of Fertilizer in PakistanmadihashkhNo ratings yet

- CostCurves PDFDocument63 pagesCostCurves PDFashikhmd4467No ratings yet

- EIU Natural GasDocument6 pagesEIU Natural GashikaridamashiiNo ratings yet

- EM Chapter 1 Introduction August 06 2023Document84 pagesEM Chapter 1 Introduction August 06 2023Shubham kumarNo ratings yet

- Development and Opportunities in China's Natural Gas MarketDocument23 pagesDevelopment and Opportunities in China's Natural Gas MarketAlok GiriNo ratings yet

- KTrade 2023 Strategy Report - Where To Invest in 2023Document51 pagesKTrade 2023 Strategy Report - Where To Invest in 2023Amir MarwatNo ratings yet

- Resources and Energy Quarterly December 2023 Forecast DataDocument38 pagesResources and Energy Quarterly December 2023 Forecast Datak60.2112153075No ratings yet

- Plantation: MaintainDocument4 pagesPlantation: MaintainirfanaffiqNo ratings yet

- Vale's 3Q23 Production and Sales ReportDocument7 pagesVale's 3Q23 Production and Sales ReportSoniwell SoniwellNo ratings yet

- Waras Budi Santosa, Head of Monetization Division Oil & Gas, SKK MigasDocument16 pagesWaras Budi Santosa, Head of Monetization Division Oil & Gas, SKK MigasShah Reza DwiputraNo ratings yet

- Prices of Fuels Purchased by Manufacturing Industry in Great Britain (P/KWH)Document11 pagesPrices of Fuels Purchased by Manufacturing Industry in Great Britain (P/KWH)Eng Bile LastroNo ratings yet

- Valuation Challenges in Stranded Asset Scenarios - A Risk Discourse of Evidence From The UKDocument19 pagesValuation Challenges in Stranded Asset Scenarios - A Risk Discourse of Evidence From The UKUyen HoangNo ratings yet

- 2018 Paper 3 - InsertDocument4 pages2018 Paper 3 - Insertgeetapt2No ratings yet

- Content Handbook of Energy and Economic Statistics of Indonesia 2019Document109 pagesContent Handbook of Energy and Economic Statistics of Indonesia 2019Jasa JahitNo ratings yet

- Accepted Manuscript: 10.1016/j.jngse.2017.05.013Document27 pagesAccepted Manuscript: 10.1016/j.jngse.2017.05.013João Paulo NevesNo ratings yet

- TD Economics: Weekly Commodity Price ReportDocument6 pagesTD Economics: Weekly Commodity Price ReportInternational Business TimesNo ratings yet

- Content Handbook of Energy and Economic Statistics of Indonesia 2020Document111 pagesContent Handbook of Energy and Economic Statistics of Indonesia 2020Fabiola Marella PardedeNo ratings yet

- Weekly Commodity Price ReportDocument6 pagesWeekly Commodity Price ReportInternational Business TimesNo ratings yet

- Content Handbook of Energy and Economic Statistics of Indonesia 2018 Final Edition PDFDocument107 pagesContent Handbook of Energy and Economic Statistics of Indonesia 2018 Final Edition PDFAnwaruddin SalehNo ratings yet

- Content Handbook of Energy and Economic Statistics of Indonesia 2018 Final Edition PDFDocument107 pagesContent Handbook of Energy and Economic Statistics of Indonesia 2018 Final Edition PDFIreg TraxNo ratings yet

- HEESI 2019-Portrait PDFDocument141 pagesHEESI 2019-Portrait PDFnanda citraNo ratings yet

- BHP Operational Review For The Year Ended 30 June 2022Document19 pagesBHP Operational Review For The Year Ended 30 June 2022NoNo ratings yet

- Commodities Outlook 2024 IntesaDocument36 pagesCommodities Outlook 2024 IntesajeanmarcpuechNo ratings yet

- Cfbc'-A Preferred Generation Technology For India: by - S. C.Pal & S. S. ChopadeDocument24 pagesCfbc'-A Preferred Generation Technology For India: by - S. C.Pal & S. S. ChopadePrudhvi RajNo ratings yet

- Outlook 1H.2022 - Ha - EngDocument13 pagesOutlook 1H.2022 - Ha - EngHa TrinhNo ratings yet

- BNIS Short Notes: Under-Appreciated Gold AssetDocument4 pagesBNIS Short Notes: Under-Appreciated Gold AssetfirmanNo ratings yet

- Coal India Limited: Corporate PresentationDocument14 pagesCoal India Limited: Corporate PresentationPraveen KumarNo ratings yet

- OM-HP Project Report Group3Document3 pagesOM-HP Project Report Group3Ninaad MadrasNo ratings yet

- 2012 A Review of Performance Appraisals of Nigerian Federal Government-Owned RefineriesDocument7 pages2012 A Review of Performance Appraisals of Nigerian Federal Government-Owned RefineriesvietnampetrochemicalNo ratings yet

- Nomura - Oil & Gas, Chemicals 30 Sept 2010Document21 pagesNomura - Oil & Gas, Chemicals 30 Sept 2010ppt46No ratings yet

- Global Coal Risk AssessmentDocument76 pagesGlobal Coal Risk AssessmentEnergiemediaNo ratings yet

- PAT Target Achievement: Strategies and Practices: EEC Conference 31 August, 2015Document23 pagesPAT Target Achievement: Strategies and Practices: EEC Conference 31 August, 2015Gaurav SinghNo ratings yet

- Appendix 2 GMU PVC Decarb 2050Document18 pagesAppendix 2 GMU PVC Decarb 2050Abby LaingNo ratings yet

- BCCL Project ReportDocument42 pagesBCCL Project ReportChandan Kumar Singh100% (1)

- Seaborne Trade and Tonne-Mile Tables - March 2024Document22 pagesSeaborne Trade and Tonne-Mile Tables - March 2024ssshewale1988No ratings yet

- ADMR - Laporan Informasi Dan Fakta Material - 31257144 - EnglishDocument5 pagesADMR - Laporan Informasi Dan Fakta Material - 31257144 - Englishrakhimbjb78No ratings yet

- Climate Change (POLIGON)Document16 pagesClimate Change (POLIGON)Nurdayanti SNo ratings yet

- Final Dynamic EnergyDocument398 pagesFinal Dynamic EnergyAsad ShahNo ratings yet

- Presentation To Institutional Investors On Non-Deal Roadshow at USA 01042017Document14 pagesPresentation To Institutional Investors On Non-Deal Roadshow at USA 01042017Yadav JiNo ratings yet

- Nail - ModifiedDocument28 pagesNail - ModifiedFekadie TesfaNo ratings yet

- 1.energy ScenarioDocument50 pages1.energy ScenarioHemanth Kumar MahanthiNo ratings yet

- 2023 12 21 Monthly Press ReleaseDocument2 pages2023 12 21 Monthly Press ReleasechaxaimNo ratings yet

- 2 67 1637046254 Ijmperddec20217Document12 pages2 67 1637046254 Ijmperddec20217TJPRC PublicationsNo ratings yet

- The Nickel Market: I. Historical PricesDocument4 pagesThe Nickel Market: I. Historical PricesTuan AnhNo ratings yet

- Do Oil Prices Drive Food Prices? A Natural Experiment: Fernando Avalos BIS Office of The Americas 21 March 2013Document28 pagesDo Oil Prices Drive Food Prices? A Natural Experiment: Fernando Avalos BIS Office of The Americas 21 March 2013FranJim FjdNo ratings yet

- Exchanges Can Be Far-Reaching, Not Just For The British Economy But For The Global Economy TooDocument8 pagesExchanges Can Be Far-Reaching, Not Just For The British Economy But For The Global Economy TooTabish IqbalNo ratings yet

- Daily News 2012 11 13Document5 pagesDaily News 2012 11 13te_gantengNo ratings yet

- Energy in Italy IllahDocument31 pagesEnergy in Italy Illahfatoumatacanada96No ratings yet

- Power Plus - I DirectDocument9 pagesPower Plus - I DirectpasamvNo ratings yet

- Working Paper CilDocument20 pagesWorking Paper Cilsravan kumar garaNo ratings yet

- Project Profile On The Establishment of Nails Producing PlantDocument28 pagesProject Profile On The Establishment of Nails Producing PlantAwetahegn HagosNo ratings yet

- Modeling and Forecasting Electricity Loads and Prices: A Statistical ApproachFrom EverandModeling and Forecasting Electricity Loads and Prices: A Statistical ApproachNo ratings yet

- Ashmore Weekly Commentary 5 Jan 2024Document3 pagesAshmore Weekly Commentary 5 Jan 2024bagus.dpbri6741No ratings yet

- Aia Financial: Indonesia Syariah Small-Mid Cap FundDocument19 pagesAia Financial: Indonesia Syariah Small-Mid Cap Fundbagus.dpbri6741No ratings yet

- AISA 13 June 2012Document3 pagesAISA 13 June 2012bagus.dpbri6741No ratings yet

- Pt. Tritama Niaga BerjayaDocument1 pagePt. Tritama Niaga BerjayaJuli AntoNo ratings yet

- 04 04Rpt Funding Request SummaryDocument8 pages04 04Rpt Funding Request SummarySri Maharani AndaNo ratings yet

- (Mirae Asset Sekuritas Indonesia) Trend Focus - Expecting Another Exciting Dividend Season in 2023 PDFDocument15 pages(Mirae Asset Sekuritas Indonesia) Trend Focus - Expecting Another Exciting Dividend Season in 2023 PDFAstro HolicNo ratings yet

- PROFIL SINGKAT PERUSAHAAN Yang Isinya Meliputi:: Tugas IiDocument8 pagesPROFIL SINGKAT PERUSAHAAN Yang Isinya Meliputi:: Tugas Iisupaijho watiNo ratings yet

- Kode TK KPJ Nomor Identitas Nama LengkapDocument10 pagesKode TK KPJ Nomor Identitas Nama LengkapNoval AhmadNo ratings yet

- SOADocument165 pagesSOAFachru RozyNo ratings yet

- Reversals in Emerging Market-Will Momentum Strategy Be Profitable in Indonesia's Stock Market? (Agista Saraswati) PDFDocument47 pagesReversals in Emerging Market-Will Momentum Strategy Be Profitable in Indonesia's Stock Market? (Agista Saraswati) PDFAgista Rully SaraswatiNo ratings yet

- 57121-Article Text-177864-1-10-20221011Document10 pages57121-Article Text-177864-1-10-20221011EstefaniaNo ratings yet

- SAHAM Rekap Index - 1Document8 pagesSAHAM Rekap Index - 1Muhammad ZamröniNo ratings yet

- New AgainDocument6 pagesNew AgainRahmatNo ratings yet

- Contact Information (Responses)Document9 pagesContact Information (Responses)Muhammad Faris GymnastiarNo ratings yet

- Adoc - Pub - Tanggal Kode Kode Nama Donatur Kode Uraian JumlahDocument345 pagesAdoc - Pub - Tanggal Kode Kode Nama Donatur Kode Uraian Jumlahdjoko santosoNo ratings yet

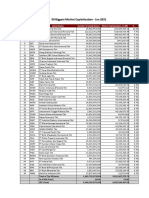

- 50 Biggest Market Capitalization - Feb 2022Document1 page50 Biggest Market Capitalization - Feb 2022Rizky Nugroho SantosNo ratings yet

- Daftar Saham Consumer Non-CyclicalsDocument6 pagesDaftar Saham Consumer Non-CyclicalsChatrine VioletNo ratings yet

- UntitledDocument24 pagesUntitledRiza OktoriyandiaNo ratings yet

- Emerging Markets Review: James Foye, Aljo Ša Valentinčič TDocument15 pagesEmerging Markets Review: James Foye, Aljo Ša Valentinčič TDessy ParamitaNo ratings yet

- IDX Statistic 2021Q2Document216 pagesIDX Statistic 2021Q2LisaNo ratings yet

- Islamic Economy - Philosophical Foundations and The Experience of IndonesiaDocument51 pagesIslamic Economy - Philosophical Foundations and The Experience of IndonesiaTaufik HussinNo ratings yet

- Daftar Saham - Consumer Non-Cyclicals - 20240210Document36 pagesDaftar Saham - Consumer Non-Cyclicals - 20240210Widia TriNo ratings yet

- BOLT - Annual Report - 2018Document162 pagesBOLT - Annual Report - 2018DiLaNo ratings yet

- Annual Report BISIDocument89 pagesAnnual Report BISIstanley.antonia7No ratings yet

- 328-Article Text-655-2-10-20230530Document10 pages328-Article Text-655-2-10-20230530WISNU SUKMANEGARANo ratings yet

- WIKA Annual Report 2008 RevisiDocument241 pagesWIKA Annual Report 2008 RevisioviNo ratings yet

- Financial Report13 PDFDocument148 pagesFinancial Report13 PDFsyahrir83No ratings yet

- Transaction StatusDocument9 pagesTransaction StatusStevanita PermatasariNo ratings yet

- 50 Biggest Market Capitalization - Jan 2021Document1 page50 Biggest Market Capitalization - Jan 2021Aditya WidiyadiNo ratings yet

- Ar Elnusa 2020Document698 pagesAr Elnusa 2020gd sutawijayaNo ratings yet

- Bank BTPN Syaria Annual Report 2021329 Wc000000002953795789Document492 pagesBank BTPN Syaria Annual Report 2021329 Wc000000002953795789dio dioNo ratings yet

- HTTPSWWW Idx Co Idmedia4865idx-Annual-Statistics-2018 PDFDocument210 pagesHTTPSWWW Idx Co Idmedia4865idx-Annual-Statistics-2018 PDFKarinakarennNo ratings yet

- RMD Ef 0489 - 19Document1 pageRMD Ef 0489 - 19Steven BayuNo ratings yet