Download as pdf or txt

You might also like

- Standard - Featured Artist AgreementDocument4 pagesStandard - Featured Artist Agreementsilvia grassiNo ratings yet

- Safety Integrity Level Selection: Systematic Methods Including Layer of Protection AnalysisDocument2 pagesSafety Integrity Level Selection: Systematic Methods Including Layer of Protection AnalysiswalidNo ratings yet

- Top 100 Aerospace Companies by Revenue 2018 PDFDocument8 pagesTop 100 Aerospace Companies by Revenue 2018 PDFNinerMike MysNo ratings yet

- Building Materials - Multiple Tailwinds For A Cheerful New Year - HSIE-202301050653325279381Document104 pagesBuilding Materials - Multiple Tailwinds For A Cheerful New Year - HSIE-202301050653325279381Varun MalikNo ratings yet

- Proforwarding PitchDocument14 pagesProforwarding PitchAb JaNo ratings yet

- Hindalco: Performance HighlightsDocument14 pagesHindalco: Performance HighlightsAngel BrokingNo ratings yet

- Cap Sim Round 7Document17 pagesCap Sim Round 7Prashant NarulaNo ratings yet

- Anderson Energy Announces 2010 Second Quarter Results: HighlightsDocument37 pagesAnderson Energy Announces 2010 Second Quarter Results: Highlightsikehenderson4879No ratings yet

- BA 545 Case StudyDocument3 pagesBA 545 Case Studytiffany reavesNo ratings yet

- Cement - Sector Update - 05 Apr 22Document17 pagesCement - Sector Update - 05 Apr 22shubh13septemberNo ratings yet

- NMDC LTD: Metals & Mining Sector Outlook - PositiveDocument5 pagesNMDC LTD: Metals & Mining Sector Outlook - Positivemtnit07No ratings yet

- Round: 0 Dec. 31, 2016: Selected Financial StatisticsDocument13 pagesRound: 0 Dec. 31, 2016: Selected Financial StatisticsHimanshu KriplaniNo ratings yet

- AMR 3Q EPS Preview: Back On TrackDocument10 pagesAMR 3Q EPS Preview: Back On TrackAshokNo ratings yet

- Sterlite, 1Q FY 2014Document13 pagesSterlite, 1Q FY 2014Angel BrokingNo ratings yet

- MRF 2Q Sy 2013Document12 pagesMRF 2Q Sy 2013Angel BrokingNo ratings yet

- Ambuja Cements: NeutralDocument8 pagesAmbuja Cements: Neutral张迪No ratings yet

- Cap Sim Round 5 ExcelDocument22 pagesCap Sim Round 5 ExcelPrashant NarulaNo ratings yet

- TAG Initiating Coverage - 20111003 CasimirDocument17 pagesTAG Initiating Coverage - 20111003 CasimirmpgervetNo ratings yet

- Assignment - Session 8Document20 pagesAssignment - Session 8Aditya JandialNo ratings yet

- WEEK 10, 14 March 2021: CapesizeDocument13 pagesWEEK 10, 14 March 2021: CapesizeVGNo ratings yet

- For CII: ApplicationDocument4 pagesFor CII: ApplicationVISHALNo ratings yet

- TiO2 FinancialDocument15 pagesTiO2 Financialbhagvandodiya88% (8)

- Metorex Int Dec07Document12 pagesMetorex Int Dec07Take OneNo ratings yet

- Year Geico Dividend Per Share in $ Total Dividend To Berkshire Hathaway in $ MillionDocument8 pagesYear Geico Dividend Per Share in $ Total Dividend To Berkshire Hathaway in $ MillionIshan KakkarNo ratings yet

- Hindalcosnapshot31 Aug 09Document1 pageHindalcosnapshot31 Aug 09Sunil KajariaNo ratings yet

- Round: 1 Dec. 31, 2021: Selected Financial StatisticsDocument15 pagesRound: 1 Dec. 31, 2021: Selected Financial StatisticsParas DhamaNo ratings yet

- Tesla DCF Valuation by Ihor MedvidDocument105 pagesTesla DCF Valuation by Ihor Medvidpriyanshu14No ratings yet

- JSW Steel: Performance HighlightsDocument13 pagesJSW Steel: Performance HighlightsAngel BrokingNo ratings yet

- ICICI Securities Update On Metals Q4FY24 Preview Non Ferrous PlayersDocument8 pagesICICI Securities Update On Metals Q4FY24 Preview Non Ferrous Playersmanitjainm21No ratings yet

- B&K On Jindal Saw - 60% UPSIDEDocument3 pagesB&K On Jindal Saw - 60% UPSIDEmailtoyadavshwetaNo ratings yet

- Sterlite Industries Result UpdatedDocument12 pagesSterlite Industries Result UpdatedAngel BrokingNo ratings yet

- ACACIA-Results For The 3 Months Ended 31 March 2019 - FINAL (1) - 1Document22 pagesACACIA-Results For The 3 Months Ended 31 March 2019 - FINAL (1) - 1Baraka LetaraNo ratings yet

- Results Continue To Demonstrate Stability of Portfolio and Provide Opportunities For High Quality GrowthDocument35 pagesResults Continue To Demonstrate Stability of Portfolio and Provide Opportunities For High Quality GrowthJavier Montecinos MalebranNo ratings yet

- Comparable Companies - U.S.-Based Steel Manufacturer Companies With FY16 Projected Revenue Between $1 Billion and $20 BillionDocument2 pagesComparable Companies - U.S.-Based Steel Manufacturer Companies With FY16 Projected Revenue Between $1 Billion and $20 Billion/jncjdncjdnNo ratings yet

- Discounted Cash Flow Analysis - Steel Dynamics Inc. (Unlevered DCF)Document4 pagesDiscounted Cash Flow Analysis - Steel Dynamics Inc. (Unlevered DCF)Moni DahalNo ratings yet

- 23 12 11 Yanzhou Coal NomuraDocument14 pages23 12 11 Yanzhou Coal NomuraMichael BauermNo ratings yet

- Round: 2 Dec. 31, 2022: Selected Financial StatisticsDocument15 pagesRound: 2 Dec. 31, 2022: Selected Financial StatisticsAshesh DasNo ratings yet

- Courier C136952 R1 TEK0 CA2Document14 pagesCourier C136952 R1 TEK0 CA2shivam kumarNo ratings yet

- Supreme Industries: Near-Term Lower Margins With Inventory Loss Upgrade To BuyDocument6 pagesSupreme Industries: Near-Term Lower Margins With Inventory Loss Upgrade To BuygirishrajsNo ratings yet

- Analysis: MRF Limited: Reader's QueryDocument20 pagesAnalysis: MRF Limited: Reader's Querysubrato KrNo ratings yet

- Cap Sim Round 1 ExcelDocument17 pagesCap Sim Round 1 ExcelPrashant NarulaNo ratings yet

- Total Income ($ / Year) : Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7Document9 pagesTotal Income ($ / Year) : Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7MANSINo ratings yet

- Cap Sim Round 6 ExcelDocument17 pagesCap Sim Round 6 ExcelPrashant NarulaNo ratings yet

- GSPL, 11th February, 2013Document10 pagesGSPL, 11th February, 2013Angel BrokingNo ratings yet

- APC 3Q EPS Preview: Smooth Sailing in 3Q But 2019 Guidance Could Be The HighlightDocument10 pagesAPC 3Q EPS Preview: Smooth Sailing in 3Q But 2019 Guidance Could Be The HighlightAshokNo ratings yet

- CpasimCourier Round 0Document14 pagesCpasimCourier Round 0AjitNo ratings yet

- Remesas BancosDocument8 pagesRemesas BancosANGELINE VARGASNo ratings yet

- Sagar Cement LTD - 23 January 2021Document11 pagesSagar Cement LTD - 23 January 2021nakilNo ratings yet

- GAIL 2QF12 Result ReviewDocument6 pagesGAIL 2QF12 Result ReviewdikshitmittalNo ratings yet

- Sarin Technologies: SingaporeDocument8 pagesSarin Technologies: SingaporephuawlNo ratings yet

- Round: 5 Dec. 31, 2024: Selected Financial StatisticsDocument15 pagesRound: 5 Dec. 31, 2024: Selected Financial StatisticsYadandla AdityaNo ratings yet

- Round: 4 Dec. 31, 2023: Selected Financial StatisticsDocument15 pagesRound: 4 Dec. 31, 2023: Selected Financial StatisticsUjjawal MittalNo ratings yet

- This Spreadsheet Supports Analysis of The Case, "Coleco Industries Inc." (Case 60)Document6 pagesThis Spreadsheet Supports Analysis of The Case, "Coleco Industries Inc." (Case 60)kashanr82No ratings yet

- Titan Company by Anuj GuptaDocument25 pagesTitan Company by Anuj GuptaHIMANSHU RAWATNo ratings yet

- Performance Highlights: AccumulateDocument12 pagesPerformance Highlights: AccumulateAngel BrokingNo ratings yet

- Fischer Price ToysDocument11 pagesFischer Price ToysAvijit BanerjeeNo ratings yet

- Market Report Week 31Document18 pagesMarket Report Week 31Mai PhamNo ratings yet

- Industry Note: Equity ResearchDocument16 pagesIndustry Note: Equity ResearchForexliveNo ratings yet

- Seanergy Maritime Reports Financial Results For The Third Quarter and Nine Months Ended September 30, 2023 and Declares Dividend of $0.025 Per ShareDocument10 pagesSeanergy Maritime Reports Financial Results For The Third Quarter and Nine Months Ended September 30, 2023 and Declares Dividend of $0.025 Per ShareKevin ParkerNo ratings yet

- Capstone Round 3 CourierDocument15 pagesCapstone Round 3 CourierKitarpNo ratings yet

- Modern Glass CharacterizationFrom EverandModern Glass CharacterizationMario AffatigatoNo ratings yet

- Motilal Oswal Monthly Update On Healthcare Sector Weak SeasonalityDocument24 pagesMotilal Oswal Monthly Update On Healthcare Sector Weak SeasonalitymisfitmedicoNo ratings yet

- Centrum Flash Note On Sugar Industry Sugar Production This YearDocument3 pagesCentrum Flash Note On Sugar Industry Sugar Production This YearmisfitmedicoNo ratings yet

- Vilas TranscriptDocument18 pagesVilas TranscriptmisfitmedicoNo ratings yet

- HDFC Securities Results ReviewDocument5 pagesHDFC Securities Results ReviewmisfitmedicoNo ratings yet

- Sushil Finance Initiating Coverage On Eveready Industries IndiaDocument15 pagesSushil Finance Initiating Coverage On Eveready Industries IndiamisfitmedicoNo ratings yet

- HDFC Securities Results Review On QSR - Demand PangsDocument6 pagesHDFC Securities Results Review On QSR - Demand PangsmisfitmedicoNo ratings yet

- In The Matter of Dealing in Illiquid Stock Options On The BSEDocument3 pagesIn The Matter of Dealing in Illiquid Stock Options On The BSEmisfitmedicoNo ratings yet

- Antique Daily 18-JAn-24Document23 pagesAntique Daily 18-JAn-24misfitmedicoNo ratings yet

- Kotak Daily 18-Jan-24Document45 pagesKotak Daily 18-Jan-24misfitmedicoNo ratings yet

- Maharashtra SeamlessDocument19 pagesMaharashtra SeamlessmisfitmedicoNo ratings yet

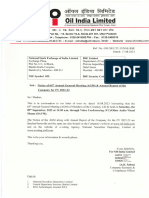

- Oil India - ARDocument403 pagesOil India - ARmisfitmedicoNo ratings yet

- Raymonds LTDDocument18 pagesRaymonds LTDmisfitmedicoNo ratings yet

- Authum Infra - PPTDocument191 pagesAuthum Infra - PPTmisfitmedicoNo ratings yet

- Holiday - 2024Document9 pagesHoliday - 2024misfitmedicoNo ratings yet

- Board Secretariat: Presentation and Audio of Conference Call Held On October 23, 2023Document6 pagesBoard Secretariat: Presentation and Audio of Conference Call Held On October 23, 2023misfitmedicoNo ratings yet

- Mannapuram FinanceDocument459 pagesMannapuram FinancemisfitmedicoNo ratings yet

- Oil India - TRDocument31 pagesOil India - TRmisfitmedicoNo ratings yet

- Economic Survey (2012-2013)Document297 pagesEconomic Survey (2012-2013)misfitmedico100% (1)

- NMDCDocument15 pagesNMDCmisfitmedicoNo ratings yet

- Adani TDocument14 pagesAdani TmisfitmedicoNo ratings yet

- Investor Presentation (Shalby Hospitals)Document42 pagesInvestor Presentation (Shalby Hospitals)misfitmedicoNo ratings yet

- ONGCDocument40 pagesONGCmisfitmedicoNo ratings yet

- Xat 2016 OfficialDocument29 pagesXat 2016 OfficialmisfitmedicoNo ratings yet

- CS50Document2 pagesCS50misfitmedicoNo ratings yet

- Quality Inspection Assurance System - : Supplier ManagementDocument2 pagesQuality Inspection Assurance System - : Supplier ManagementMURALIDHRA100% (1)

- Celpip Writing SampleDocument2 pagesCelpip Writing SampleManinder KaurNo ratings yet

- Chapter 6 Production Activity Control - Powerpoint PPT PresentationDocument17 pagesChapter 6 Production Activity Control - Powerpoint PPT PresentationsivaNo ratings yet

- CMD & Cmir V1Document45 pagesCMD & Cmir V1tmaha87No ratings yet

- Practice Sums 2Document3 pagesPractice Sums 2Vedant JoshiNo ratings yet

- F2 Mha Mock 3Document12 pagesF2 Mha Mock 3Annas SaeedNo ratings yet

- AnalysisDocument11 pagesAnalysis9463684355No ratings yet

- PDDocument15 pagesPDvikas jaimanNo ratings yet

- Activity Sheets in Fundamentals of Accountanc4Document8 pagesActivity Sheets in Fundamentals of Accountanc4Irish NicolasNo ratings yet

- Supply Chain Management - Quiz 2 - 2020 v1Document7 pagesSupply Chain Management - Quiz 2 - 2020 v1Raj BafnaNo ratings yet

- People Express Airlines: Rise and Decline: Group 1Document9 pagesPeople Express Airlines: Rise and Decline: Group 1ssagr123No ratings yet

- Lecture 07Document24 pagesLecture 07A RaufNo ratings yet

- Contoh Company Profile StartupDocument15 pagesContoh Company Profile StartupDavid RamadhanNo ratings yet

- Introduction To Gemini TTG199v6Document30 pagesIntroduction To Gemini TTG199v6acticall21No ratings yet

- Audit Test Solution by CA Harshad Jaju SirDocument13 pagesAudit Test Solution by CA Harshad Jaju SirHetal BeraNo ratings yet

- Kpi Scorecard TemplateDocument2 pagesKpi Scorecard TemplatePersonalia HC JBSPNo ratings yet

- 104 2022 220 EyDocument30 pages104 2022 220 EyJason BramwellNo ratings yet

- Corrective Action and Preventive Actions and Its Importance in Quality Management System: A ReviewDocument6 pagesCorrective Action and Preventive Actions and Its Importance in Quality Management System: A ReviewsachinNo ratings yet

- 04.theories of SupplyDocument10 pages04.theories of SupplyMd Shah AlamNo ratings yet

- OUbs042114 PrinciplesofManagementDocument138 pagesOUbs042114 PrinciplesofManagementMaria CristinaNo ratings yet

- Self-Assessment Check - Plan Training SessionDocument4 pagesSelf-Assessment Check - Plan Training SessionMaidy CervantesNo ratings yet

- EN 16646 Maintenance Within Physical Asset ManagementDocument8 pagesEN 16646 Maintenance Within Physical Asset ManagementoperacionesNo ratings yet

- RBB Syllabus Open Level5 Cash 5030Document3 pagesRBB Syllabus Open Level5 Cash 5030alxaNo ratings yet

- 5568 Digit UniliverDocument30 pages5568 Digit UniliverAhsinNo ratings yet

- Communicating For ServiceDocument12 pagesCommunicating For ServiceSuper PBNo ratings yet

- Optimum: Operating ManualDocument50 pagesOptimum: Operating ManualPolina OmgNo ratings yet

- Apple Company Leadership Change - Edited 1 .EditedDocument13 pagesApple Company Leadership Change - Edited 1 .EditedFun Toosh345No ratings yet

- Assignment On Strategic Planning of Bashundhara GroupDocument12 pagesAssignment On Strategic Planning of Bashundhara GroupSamiraNo ratings yet