Download as docx, pdf, or txt

You might also like

- Fiscal Policy - The Basics: A) IntroductionDocument7 pagesFiscal Policy - The Basics: A) IntroductionmalcewanNo ratings yet

- ADB Project CycleDocument5 pagesADB Project CycleElvin CruzNo ratings yet

- Executive Summary ENG2 R (A, J, K)Document9 pagesExecutive Summary ENG2 R (A, J, K)JohnStarksNo ratings yet

- Economics Handout Public Debt: The Debt Stock Net Budget DeficitDocument6 pagesEconomics Handout Public Debt: The Debt Stock Net Budget DeficitOnella GrantNo ratings yet

- Macroeconomics: CHAPTER 1: Introducti On and Measurement IssuesDocument7 pagesMacroeconomics: CHAPTER 1: Introducti On and Measurement IssuesCole WallaceNo ratings yet

- Unit 13 - Economic Fluctuations and Unemployment - 1.0Document35 pagesUnit 13 - Economic Fluctuations and Unemployment - 1.0Georgius Yeremia CandraNo ratings yet

- Economics TermsDocument11 pagesEconomics TermsAhmad Zia JamiliNo ratings yet

- Unit 14 - Unemployment and Fiscal Policy - 1.0Document41 pagesUnit 14 - Unemployment and Fiscal Policy - 1.0Georgius Yeremia CandraNo ratings yet

- Fiscal Policy and Government DebtDocument14 pagesFiscal Policy and Government DebtNick GrzebienikNo ratings yet

- Fiscal PolicyDocument24 pagesFiscal Policyરહીમ હુદ્દાNo ratings yet

- ACCA BT Topic 4 NotesDocument5 pagesACCA BT Topic 4 Notesعمر اعظمNo ratings yet

- Unit 5 Government Expenditure and RevenueDocument45 pagesUnit 5 Government Expenditure and RevenuePump AestheticsNo ratings yet

- R-G 0: Can We Sleep More Soundly?: by Paolo Mauro and Jing ZhouDocument32 pagesR-G 0: Can We Sleep More Soundly?: by Paolo Mauro and Jing ZhoutegelinskyNo ratings yet

- WP 12184Document40 pagesWP 12184Thái Vũ Nguyễn ViếtNo ratings yet

- Week 7 Unit 13Document27 pagesWeek 7 Unit 13livres influentNo ratings yet

- Chapter 11Document9 pagesChapter 11Kotryna RudelytėNo ratings yet

- Chapter - 04 - Deep Dive - DPDocument43 pagesChapter - 04 - Deep Dive - DPDilshansasankayahoo.comNo ratings yet

- Multiplicadores FiscalesDocument15 pagesMultiplicadores FiscalesXhail BalamNo ratings yet

- Fiscal Multipliers: Imf Staff Position NoteDocument15 pagesFiscal Multipliers: Imf Staff Position NotewalshkevinmNo ratings yet

- Gruberch 04Document62 pagesGruberch 04Boy ColdNo ratings yet

- Demand Sided Policy: Spending/g)Document9 pagesDemand Sided Policy: Spending/g)Umesh SharmaNo ratings yet

- Unit 1,2&3Document71 pagesUnit 1,2&3Bhavani venkatesanNo ratings yet

- Mks PFM I Module 1.3 Macro and The Budget Corrections 06.09.2016Document30 pagesMks PFM I Module 1.3 Macro and The Budget Corrections 06.09.2016renalyn alraNo ratings yet

- Working Paper 7 ADocument144 pagesWorking Paper 7 Aziyad786123No ratings yet

- IGCSE 04192024 PracticeDocument7 pagesIGCSE 04192024 PracticeWu JingbiaoNo ratings yet

- Tarea U2.Document7 pagesTarea U2.Amanda CedeñoNo ratings yet

- Intros 5Document25 pagesIntros 5drfendiameenNo ratings yet

- Economics PaperDocument15 pagesEconomics PaperSamad Ashraf MemonNo ratings yet

- IMF Fiscal MonitorDocument42 pagesIMF Fiscal MonitorqonijoNo ratings yet

- Class 12 Macro Economics Chapter 5 - Revision NotesDocument4 pagesClass 12 Macro Economics Chapter 5 - Revision NotesROHIT SHANo ratings yet

- CH 22Document5 pagesCH 22Ahmad AlatasNo ratings yet

- Some Important TopicsDocument5 pagesSome Important TopicsStuti DeopaNo ratings yet

- Ecu - 08606 Lecture 8Document26 pagesEcu - 08606 Lecture 8DanielNo ratings yet

- Fiscal Policy WrittenDocument4 pagesFiscal Policy WrittenKenneth Rae QuirimoNo ratings yet

- Government BudgetDocument2 pagesGovernment BudgetParth NataniNo ratings yet

- Def 1Document4 pagesDef 1Guezil Joy DelfinNo ratings yet

- Reflection PaperDocument5 pagesReflection PaperJoice RuzolNo ratings yet

- Chapter 12 Full EmplymentDocument14 pagesChapter 12 Full Emplymentowais5577No ratings yet

- Econ6049 Economic Analysis, S1 2021: Week 8: Unit 13 - Economic Fluctuations and UnemploymentDocument27 pagesEcon6049 Economic Analysis, S1 2021: Week 8: Unit 13 - Economic Fluctuations and UnemploymentTom WongNo ratings yet

- BED1201Document3 pagesBED1201cyrusNo ratings yet

- Agcapita April 2010Document11 pagesAgcapita April 2010Capita1No ratings yet

- 18e Key Question Answers CH 30Document3 pages18e Key Question Answers CH 30pikachu_latias_latiosNo ratings yet

- Global Debt Monitor - April2020 IIF PDFDocument5 pagesGlobal Debt Monitor - April2020 IIF PDFAndyNo ratings yet

- Backup of Economic Readings SummaryDocument21 pagesBackup of Economic Readings Summarybenicebronzwaer0No ratings yet

- Economic Effects of A Budget DeficitDocument20 pagesEconomic Effects of A Budget DeficitKalu AbuNo ratings yet

- Fiscal PolicyDocument30 pagesFiscal PolicySumana ChatterjeeNo ratings yet

- Govt BudgetDocument38 pagesGovt BudgetRicha GoelNo ratings yet

- Leec 105Document19 pagesLeec 105Pradeep NairNo ratings yet

- ECS2602 NotesDocument30 pagesECS2602 NotesSimphiwe NkosiNo ratings yet

- Govt. Budgeconomy Budget: It Is An Annual Financial Statement of TheDocument8 pagesGovt. Budgeconomy Budget: It Is An Annual Financial Statement of TheTirsha BiswasNo ratings yet

- Questions: Answer: Options Are To Reduce Government Spending, Increase Taxes, or SomeDocument5 pagesQuestions: Answer: Options Are To Reduce Government Spending, Increase Taxes, or Somecourse101No ratings yet

- Pitchford Thesis Current Account DeficitDocument8 pagesPitchford Thesis Current Account DeficitErin Taylor100% (2)

- Macroeconomic Signals - Fiche CalculatriceDocument12 pagesMacroeconomic Signals - Fiche Calculatricebaillon.andreamaria9No ratings yet

- W11 Topic 8.fiscal PolicyDocument20 pagesW11 Topic 8.fiscal Policy刘家亨No ratings yet

- Fiscal PolicyDocument7 pagesFiscal PolicySara de la SernaNo ratings yet

- ¿Qué Hacen Los Déficits Presupuestarios¿ - MankiwDocument26 pages¿Qué Hacen Los Déficits Presupuestarios¿ - Mankiwpandita86No ratings yet

- Chapter 1.4 - GDP ComponentsDocument26 pagesChapter 1.4 - GDP Componentsgon.ugarrizaNo ratings yet

- Government BudgetDocument22 pagesGovernment Budgetsukh singhNo ratings yet

- Economics Study NotesDocument4 pagesEconomics Study NotesjestinaNo ratings yet

- Leec 105Document19 pagesLeec 105pradyu1990No ratings yet

- China and the US Foreign Debt Crisis: Does China Own the USA?From EverandChina and the US Foreign Debt Crisis: Does China Own the USA?No ratings yet

- Careers After COVID-19Document12 pagesCareers After COVID-19Iqbal Pugar RamadhanNo ratings yet

- Compensation Project 1Document10 pagesCompensation Project 1Digital EraNo ratings yet

- Exercise 1 - Chapter 1Document4 pagesExercise 1 - Chapter 1ᴀǫɪʟ Rᴀᴍʟɪ100% (1)

- 2021 Commercial WorkbookDocument146 pages2021 Commercial WorkbookFarhan KhanNo ratings yet

- CLBS Financial Statement 1Document6 pagesCLBS Financial Statement 1Peter Cranzo MeisterNo ratings yet

- Bar QuestionsLAborDocument50 pagesBar QuestionsLAborBasmuthNo ratings yet

- How Government Spends and Accounts For Public Money in ZambiaDocument145 pagesHow Government Spends and Accounts For Public Money in ZambiaMichael MbangwetaNo ratings yet

- AKKU Annual Report 2016Document141 pagesAKKU Annual Report 2016Doli Dui TilfaNo ratings yet

- Module 2, Test 1, Test 3Document9 pagesModule 2, Test 1, Test 3Jigz GuzmanNo ratings yet

- Pertemuan-10 Tata Kelola Sistem InformasiDocument28 pagesPertemuan-10 Tata Kelola Sistem InformasiMela NewpyNo ratings yet

- Adi Setia - Islamic Transactional LawDocument42 pagesAdi Setia - Islamic Transactional LawAmru Khalid SazaliNo ratings yet

- Handbook On The Shadow EconomyDocument542 pagesHandbook On The Shadow Economydiana marinaNo ratings yet

- S - Ch7 - Long Term Objectives and StrategiesDocument31 pagesS - Ch7 - Long Term Objectives and StrategiesYion LekNo ratings yet

- L9 Transforming Existing Markets MGN815Document17 pagesL9 Transforming Existing Markets MGN815Sam RehmanNo ratings yet

- Meaning of Responsibility CenterDocument18 pagesMeaning of Responsibility CenterSuman Preet KaurNo ratings yet

- Economic Relief Package Pdfver.Document130 pagesEconomic Relief Package Pdfver.sanjith saravananNo ratings yet

- Penn Exemption Rev-1220Document2 pagesPenn Exemption Rev-1220jpesNo ratings yet

- Chapter 4 - Audit PlanningDocument43 pagesChapter 4 - Audit PlanningMy DgNo ratings yet

- Law and Economics ProjectDocument12 pagesLaw and Economics ProjectSankalp PatelNo ratings yet

- Services Marketing 6th Edition Zeithaml Test Bank 1Document36 pagesServices Marketing 6th Edition Zeithaml Test Bank 1tarawarnerqxwzkpfbyd100% (25)

- International Relations and Current Affairs: Answer: (D)Document3 pagesInternational Relations and Current Affairs: Answer: (D)Mujahid Ali0% (1)

- Role of Filipino Consumer Culture To Filipino Self and IdentityDocument7 pagesRole of Filipino Consumer Culture To Filipino Self and IdentityMaria Lyn ArandiaNo ratings yet

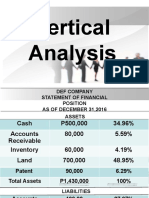

- Vertical AnalysisDocument8 pagesVertical AnalysisHannah Mae BautistaNo ratings yet

- LC & Standby LCDocument8 pagesLC & Standby LCmanith_kim13No ratings yet

- Corruption in Pakistan - Nguyễn Thị Thu Hằng - 425068 - MGT353Document4 pagesCorruption in Pakistan - Nguyễn Thị Thu Hằng - 425068 - MGT353Hằng ThuNo ratings yet

- BFM 3206 Chapter 1Document25 pagesBFM 3206 Chapter 1Mary Anne JamisolaNo ratings yet

- Chapter 2 Page 40 - 68Document29 pagesChapter 2 Page 40 - 68Naveen KumarNo ratings yet

- Notes For Studies DR - PK Singhai Qty Surveying & Costing CE602 5 Valuation LNCTS, Civil Engg. 6 Semester Civil Diploma 29 MARCH 2020Document8 pagesNotes For Studies DR - PK Singhai Qty Surveying & Costing CE602 5 Valuation LNCTS, Civil Engg. 6 Semester Civil Diploma 29 MARCH 2020SNo ratings yet