Download as xlsx, pdf, or txt

You might also like

- Introduction To Islamic Fintech - Mufti Faraz AdamDocument165 pagesIntroduction To Islamic Fintech - Mufti Faraz AdamAini Khairiyah SharakalNo ratings yet

- Tronica CityDocument10 pagesTronica CitysahildoraNo ratings yet

- Product Planning, Branding & Packaging - Assignment FinalDocument31 pagesProduct Planning, Branding & Packaging - Assignment FinalDgl100% (2)

- Sensitivity Analysis: Capital CostDocument4 pagesSensitivity Analysis: Capital CostZaini AhNo ratings yet

- Options Greeks CalculatorDocument6 pagesOptions Greeks CalculatoranbuNo ratings yet

- BKM9e EOC Ch27Document4 pagesBKM9e EOC Ch27Cardoso PenhaNo ratings yet

- 5.1 Holding Period ReturnDocument48 pages5.1 Holding Period ReturnSrilekha BasavojuNo ratings yet

- Revisi ValidDocument12 pagesRevisi ValidirfanNo ratings yet

- Optimal Portfolio DataDocument3 pagesOptimal Portfolio Datanga vuNo ratings yet

- Risk Hedging: Investment Analysis and Portfolio ManagementDocument16 pagesRisk Hedging: Investment Analysis and Portfolio ManagementPhuong Anh NguyenNo ratings yet

- FM300 Exam 2022 Section B Q2Document4 pagesFM300 Exam 2022 Section B Q2包金叶No ratings yet

- Shares 10 Discreet Return 15% Continuous Compounding Return 13.98%Document6 pagesShares 10 Discreet Return 15% Continuous Compounding Return 13.98%Khushboo RajNo ratings yet

- Sample Question 1: TimestampDocument9 pagesSample Question 1: Timestampsaurabh kumarNo ratings yet

- Risk Aversion ExampleDocument10 pagesRisk Aversion ExampleShashwat DeshmukhNo ratings yet

- Portofoliu DividendeDocument7 pagesPortofoliu DividendeLucian LadicNo ratings yet

- Modern Portfolio TheoryDocument7 pagesModern Portfolio TheoryTEcHEduNo ratings yet

- Attribute Coeffs S.E. Wald Z P-ValueDocument8 pagesAttribute Coeffs S.E. Wald Z P-Valuesarthak mendirattaNo ratings yet

- Raroc NewDocument2 pagesRaroc NewAtiaTahiraNo ratings yet

- FO-003 Uncertainty Estimate - 1621923638Document2 pagesFO-003 Uncertainty Estimate - 1621923638swapon kumar shillNo ratings yet

- Distâ1Document19 pagesDistâ1Nastase DamianNo ratings yet

- Profit Loss CalculatorDocument8 pagesProfit Loss Calculator'Izzad AfifNo ratings yet

- Convertable Bond: (Option Adjusted Spread)Document6 pagesConvertable Bond: (Option Adjusted Spread)Taychang WangNo ratings yet

- Excel BookDocument6 pagesExcel Bookmoneesh 99No ratings yet

- Quality Engineering Report IIIDocument3 pagesQuality Engineering Report IIIKurtNo ratings yet

- Ch. 6: Beta Estimation and The Cost of EquityDocument2 pagesCh. 6: Beta Estimation and The Cost of EquitymallikaNo ratings yet

- FM09-CH 06Document2 pagesFM09-CH 06Mukul KadyanNo ratings yet

- Options Greeks CalculatorDocument6 pagesOptions Greeks CalculatorpraschNo ratings yet

- Resistencias SMD WIN-1524917Document4 pagesResistencias SMD WIN-1524917Ignacio Barriga NuñezNo ratings yet

- Credit Risk ClassDocument17 pagesCredit Risk ClassSAI GANESH M S 2127321No ratings yet

- Planilha de Calculo RAIN CRANE WalterDocument5 pagesPlanilha de Calculo RAIN CRANE WalterThiagoNo ratings yet

- ReportDocument4 pagesReportLâm Bá ĐạtNo ratings yet

- Probablity of 'C' or Less DefectsDocument4 pagesProbablity of 'C' or Less DefectsChaitanya BhujadeNo ratings yet

- Head Loss Vs Vloumatric FL Ow RateDocument3 pagesHead Loss Vs Vloumatric FL Ow RateAli Al- HayraniNo ratings yet

- GY462 Lec04 Leverage RiskCalculationsDocument2 pagesGY462 Lec04 Leverage RiskCalculationszhou maggieNo ratings yet

- CIA III-calculationDocument9 pagesCIA III-calculationVAISHALI HASIJA 1923584No ratings yet

- Portfolio Assignment: InstructionsDocument9 pagesPortfolio Assignment: InstructionsAntariksh ShahwalNo ratings yet

- Portafolio CARLOSDocument20 pagesPortafolio CARLOSKJ ZapataNo ratings yet

- 01Document14 pages01NarinderNo ratings yet

- Post HocDocument3 pagesPost HocTania DesceyNo ratings yet

- Stack Up Analysis 18 20Document2 pagesStack Up Analysis 18 20Amirac MNo ratings yet

- Problem 15 Problem 16: Investments, by Bodie, Kane, and Marcus, 9th Edition Spreadsheet Templates MAIN MENU - Chapter 18Document4 pagesProblem 15 Problem 16: Investments, by Bodie, Kane, and Marcus, 9th Edition Spreadsheet Templates MAIN MENU - Chapter 18Bona Christanto SiahaanNo ratings yet

- Marriott Cost of CapitalDocument3 pagesMarriott Cost of Capitalanmolsaini01No ratings yet

- PNL Ustt2022Document2 pagesPNL Ustt2022nerdvanacolNo ratings yet

- Assignment 1 SolutionDocument8 pagesAssignment 1 SolutionDanial HemaniNo ratings yet

- Statistics Report: Output Filename: Fe Dec 13, 2018Document3 pagesStatistics Report: Output Filename: Fe Dec 13, 2018nurafniNo ratings yet

- Portfolio Performance PresentationDocument9 pagesPortfolio Performance Presentationharshwardhan.singh202No ratings yet

- Corporate Risk EstimatesDocument21 pagesCorporate Risk EstimatesRahul sardanaNo ratings yet

- Problem 8,10,12,145Document10 pagesProblem 8,10,12,145Ariel ZamoraNo ratings yet

- 3% PRI Final SheetDocument3 pages3% PRI Final SheetAmit KumarNo ratings yet

- Indexing Techniques For Cubic Materials - Limbaga, Laguna, Heramis, Silas, JabienDocument24 pagesIndexing Techniques For Cubic Materials - Limbaga, Laguna, Heramis, Silas, JabienEDISON LIMBAGANo ratings yet

- Fofport 1Document8 pagesFofport 1AliceNo ratings yet

- FM09-CH 05Document4 pagesFM09-CH 05Mukul KadyanNo ratings yet

- Strategy Research: Input ParametersDocument233 pagesStrategy Research: Input Parametersapi-26370089No ratings yet

- Assignment 1Document2 pagesAssignment 1SwapnilNo ratings yet

- Blue Bus485 FinalDocument13 pagesBlue Bus485 FinalTamzid Ahmed AnikNo ratings yet

- Chapter 1 - Investment SettingDocument6 pagesChapter 1 - Investment SettingMayang SrssnrtNo ratings yet

- PrincipalsandRatings - 5.2.2021 Part 5Document9 pagesPrincipalsandRatings - 5.2.2021 Part 5mitchellhockinNo ratings yet

- Chapter 5: Risk and Return: Portfolio Theory and Assets Pricing ModelsDocument3 pagesChapter 5: Risk and Return: Portfolio Theory and Assets Pricing ModelsMukul KadyanNo ratings yet

- LD & SharpeDocument2 pagesLD & SharpedeeldoNo ratings yet

- Sample Size & Portfolio in ConstructionDocument7 pagesSample Size & Portfolio in ConstructionArshad HussainNo ratings yet

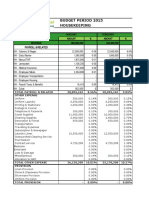

- File Budget 2015 HKDocument10 pagesFile Budget 2015 HKAvip HidayatNo ratings yet

- Calibre Agujas y CanulasDocument3 pagesCalibre Agujas y CanulasCarolina Reis PenedoNo ratings yet

- 3.13 Pirovano v. Dela Rama Steamship Co., 96 P 335Document19 pages3.13 Pirovano v. Dela Rama Steamship Co., 96 P 335Sam ConcepcionNo ratings yet

- Pan American Silver: MODEL:3700 10th Edition (ISO13709) LA SIZE:3x4-16S QTY: 2Document6 pagesPan American Silver: MODEL:3700 10th Edition (ISO13709) LA SIZE:3x4-16S QTY: 2wilsonNo ratings yet

- Assessment Task 2Document4 pagesAssessment Task 2Christian N MagsinoNo ratings yet

- Causes and Effects of Delays in Construction of Medium Scale Drinking Water Supply Projects in Sri LankaDocument10 pagesCauses and Effects of Delays in Construction of Medium Scale Drinking Water Supply Projects in Sri LankaHanaNo ratings yet

- Full Name: Example 1 No Summary Statement and Education Listed After ExperienceDocument3 pagesFull Name: Example 1 No Summary Statement and Education Listed After ExperienceGarimaBhandariNo ratings yet

- Paper No. BCH 5.2) - Financial ManagementDocument5 pagesPaper No. BCH 5.2) - Financial ManagementMary CharlesNo ratings yet

- 7ps of MarketingDocument58 pages7ps of MarketingRaquel Sibal RodriguezNo ratings yet

- Bank Deposit Slip-Askari-800Document1 pageBank Deposit Slip-Askari-800RK DanishNo ratings yet

- Amir CVDocument1 pageAmir CVAmir ToumaNo ratings yet

- Effect of Logistics Performance On The Store's Image and Consumers' SatisfactionDocument4 pagesEffect of Logistics Performance On The Store's Image and Consumers' SatisfactionInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Revisi Soal Pas Genap Bahasa Inggris Kelas Xii 2324Document7 pagesRevisi Soal Pas Genap Bahasa Inggris Kelas Xii 2324Syahrul RamadhanNo ratings yet

- Abdur Rehman Rehan-Ul-Haque - Admission Confirmation Payment PlanDocument2 pagesAbdur Rehman Rehan-Ul-Haque - Admission Confirmation Payment PlanAbdur RehmanNo ratings yet

- 313 PCDRDocument3 pages313 PCDRkahwai ngNo ratings yet

- Life Sciences OpX Consulting - OpX Begins Here Article ChemEng0307Document4 pagesLife Sciences OpX Consulting - OpX Begins Here Article ChemEng0307Sandu LicaNo ratings yet

- Kratos October 2020Document13 pagesKratos October 2020flateric74@yandex.ruNo ratings yet

- Fastener EurAsia Magazine 74Document100 pagesFastener EurAsia Magazine 74Varun KumarNo ratings yet

- Marketing Mod 1 Summary (MBA Sem 4)Document5 pagesMarketing Mod 1 Summary (MBA Sem 4)Jayanti PandeNo ratings yet

- Rent To Own Student Activity PDFDocument3 pagesRent To Own Student Activity PDFScott MartzNo ratings yet

- 1.0 Executive Summary: Abdm3313 EntrepreneurshipDocument17 pages1.0 Executive Summary: Abdm3313 EntrepreneurshipisqmaNo ratings yet

- Guideline For Petronas RegistrationDocument36 pagesGuideline For Petronas RegistrationHabib Mukmin100% (1)

- FSA Tutorial 1Document2 pagesFSA Tutorial 1KHOO TAT SHERN DEXTONNo ratings yet

- Return and Refund PolicyDocument4 pagesReturn and Refund PolicyChishty Shai NomaniNo ratings yet

- IBM-UNIT 3 NotesDocument37 pagesIBM-UNIT 3 Notesabhishek singhNo ratings yet

- Study On Consumer Perception and Attitude TowardsDocument48 pagesStudy On Consumer Perception and Attitude Towardsgaurav gargNo ratings yet

- Project 2-Embezzlement of FundsDocument6 pagesProject 2-Embezzlement of FundsabhiramNo ratings yet

- Report Writing@@@Document15 pagesReport Writing@@@satya narayanaNo ratings yet

- GJCPP5643 H: Income Tax Department Govt. of IndiaDocument1 pageGJCPP5643 H: Income Tax Department Govt. of Indiaswathi100% (1)