Cibil Market Report

Cibil Market Report

You might also like

- IB Economics Coursebook 3ed Test Your Understanding AnswersDocument26 pagesIB Economics Coursebook 3ed Test Your Understanding AnswersIzyan LiraniNo ratings yet

- Issues in Pakistan EconomyDocument4 pagesIssues in Pakistan EconomyMuhammad Waqas100% (3)

- Assignment From Lecture 3Document5 pagesAssignment From Lecture 3J. NawreenNo ratings yet

- Cmi Report April 2023Document25 pagesCmi Report April 2023Pankaj MaryeNo ratings yet

- CMI - India 2023Document29 pagesCMI - India 2023Vignesh RaghunathanNo ratings yet

- JS-MCB 29feb24Document3 pagesJS-MCB 29feb24Rizwan IqbalNo ratings yet

- Lemon Tree Hotels.Document9 pagesLemon Tree Hotels.Anonymous brpVlaVBNo ratings yet

- Slower Growth Stubborn Inflation: APRIL 3, 2023Document20 pagesSlower Growth Stubborn Inflation: APRIL 3, 2023Tomas SuaresNo ratings yet

- Oil & Gas POV GLOBALDocument8 pagesOil & Gas POV GLOBALGustavo AgudeloNo ratings yet

- Maceef FS202212Document10 pagesMaceef FS202212Guan JooNo ratings yet

- NZ Consumer Confidence JuneDocument4 pagesNZ Consumer Confidence JuneTim MooreNo ratings yet

- Scaling New Horizons: Key Performance IndicatorsDocument1 pageScaling New Horizons: Key Performance IndicatorsPapu SahooNo ratings yet

- Accomplished RCA: KYC Quality ReportDocument1 pageAccomplished RCA: KYC Quality ReportHan Htun OoNo ratings yet

- Pick of The Day (Short Term Delivery Call) - Va Tech Wabag LTD - 08-11-2023Document3 pagesPick of The Day (Short Term Delivery Call) - Va Tech Wabag LTD - 08-11-2023Anurag SanodiaNo ratings yet

- IDirect JKTyres ShubhNivesh May24Document4 pagesIDirect JKTyres ShubhNivesh May24Krunal PatelNo ratings yet

- ASAL Business Coursebook Answers PDF 15Document10 pagesASAL Business Coursebook Answers PDF 15HanNo ratings yet

- Retail Lending: in A Post Covid WorldDocument24 pagesRetail Lending: in A Post Covid WorldAbhishek JaiswalNo ratings yet

- Karen Ward IsfwDocument13 pagesKaren Ward IsfwLEE JEFFNo ratings yet

- Cement - 3QFY24 Earnings To Decline by 25%QoQDocument4 pagesCement - 3QFY24 Earnings To Decline by 25%QoQmuhammadghufran1No ratings yet

- Q3 - 2023 - Investor PresentationDocument37 pagesQ3 - 2023 - Investor PresentationMo LaNo ratings yet

- Cloudpt TP 0.79 by RHBDocument13 pagesCloudpt TP 0.79 by RHBNabil JazliNo ratings yet

- IDirect IDFCBank Q4FY23Document6 pagesIDirect IDFCBank Q4FY23Silambarasan AshokkumarNo ratings yet

- Fino Payments Bank Q3FY22 Investor PresentationDocument53 pagesFino Payments Bank Q3FY22 Investor Presentationg_sivakumarNo ratings yet

- Houlihan Lokey - Travel-&-Hospitality-Update - q3-2023Document17 pagesHoulihan Lokey - Travel-&-Hospitality-Update - q3-2023Antonius VincentNo ratings yet

- Seniors Housing Annual Review 2023-24-10752 KFDocument16 pagesSeniors Housing Annual Review 2023-24-10752 KFashwini atNo ratings yet

- Business Guardian (New Delhi) - May 23, 2023Document8 pagesBusiness Guardian (New Delhi) - May 23, 2023Camilo BenavidesNo ratings yet

- Industry - : SnapshotDocument14 pagesIndustry - : SnapshotBích DiệuNo ratings yet

- Motilal Nifty Next 50 Fund - 31MAY2024Document1 pageMotilal Nifty Next 50 Fund - 31MAY2024Krishnanand GaurNo ratings yet

- IIFL - Powermech Projects - Company Update - 20230118-1Document9 pagesIIFL - Powermech Projects - Company Update - 20230118-1Dhittbanda GamingNo ratings yet

- Axis Fixed Term Plan Series 102 1133 Days Direct High Yearly Dividend PayoutDocument1 pageAxis Fixed Term Plan Series 102 1133 Days Direct High Yearly Dividend PayoutChankyaNo ratings yet

- Morningstarreport20190906084844 PDFDocument1 pageMorningstarreport20190906084844 PDFChankyaNo ratings yet

- Axis Fixed Term Plan Series 102 1133 Days Regular High Yearly Dividend PayoutDocument1 pageAxis Fixed Term Plan Series 102 1133 Days Regular High Yearly Dividend PayoutChankyaNo ratings yet

- LGS Dom Review 23rd Sep'23Document12 pagesLGS Dom Review 23rd Sep'23Abhijit SahaNo ratings yet

- Capt SUBRA ZIA Conference - Post Pandemic ChallengesDocument24 pagesCapt SUBRA ZIA Conference - Post Pandemic ChallengesJohn HoangNo ratings yet

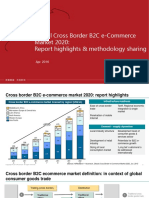

- Global Cross Border B2C E-Commerce Market 2020: Report Highlights & Methodology SharingDocument9 pagesGlobal Cross Border B2C E-Commerce Market 2020: Report Highlights & Methodology Sharingngungo12345678No ratings yet

- Morning Star Report 20190906084839Document1 pageMorning Star Report 20190906084839ChankyaNo ratings yet

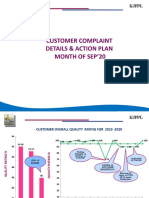

- Customer Complaint Sep'20Document23 pagesCustomer Complaint Sep'20SQA HOSURNo ratings yet

- Birla Insurance Individual Maximiser Fund December 2023Document1 pageBirla Insurance Individual Maximiser Fund December 2023sharmaoriginalNo ratings yet

- Morning Star Report 20190906084927Document1 pageMorning Star Report 20190906084927ChankyaNo ratings yet

- IDirect JMFinancial StockTalesDocument12 pagesIDirect JMFinancial StockTalesPorus Saranjit SinghNo ratings yet

- Morning Star Report 20190906084925Document1 pageMorning Star Report 20190906084925ChankyaNo ratings yet

- Of The Day (Short Term Delivery Call) - PI Industries LTDDocument3 pagesOf The Day (Short Term Delivery Call) - PI Industries LTDdeepaksinghbishtNo ratings yet

- Industry Dashboard Nov23Document114 pagesIndustry Dashboard Nov23Vignesh RaghunathanNo ratings yet

- ICRA Analytics Mutual Fund Screener - Q4FY23Document44 pagesICRA Analytics Mutual Fund Screener - Q4FY23Tshering SherpaNo ratings yet

- India Sectoral - Credit - Deployment - For - March - 2024Document7 pagesIndia Sectoral - Credit - Deployment - For - March - 2024purveshparekhNo ratings yet

- PGIM India Money Market FundDocument1 pagePGIM India Money Market FundYogi173No ratings yet

- Morningstarreport20221024033734 Canara Robeco SmallDocument1 pageMorningstarreport20221024033734 Canara Robeco SmallNiaz Abdul KarimNo ratings yet

- SuprajitDocument5 pagesSuprajitabhimanyugodara007No ratings yet

- 1Q - FY2023 Quarterly Results Briefing - 1Document18 pages1Q - FY2023 Quarterly Results Briefing - 1RidtwanNo ratings yet

- Morning Star Report 20190915054829Document1 pageMorning Star Report 20190915054829ChankyaNo ratings yet

- Autos: Super Tax To Suppress Earnings During 4QFY22Document3 pagesAutos: Super Tax To Suppress Earnings During 4QFY22Khalid Abbas ChaudhryNo ratings yet

- Sanchay Public Deposit FormDocument6 pagesSanchay Public Deposit Formmanoj barokaNo ratings yet

- Mutual Fund ScreenerDocument41 pagesMutual Fund ScreenerSantoshNo ratings yet

- QMR October 2023 - December 2023Document51 pagesQMR October 2023 - December 2023Debt Market GeekNo ratings yet

- Adani Ports Investor Presentation - London NDR PDFDocument31 pagesAdani Ports Investor Presentation - London NDR PDFHarsh GuptaNo ratings yet

- Annual MSP Performance Report Jan Dec 2021 Final CleanDocument22 pagesAnnual MSP Performance Report Jan Dec 2021 Final CleanKian Andrei EngayNo ratings yet

- External Debt Development and Management: Presentations On IndiaDocument22 pagesExternal Debt Development and Management: Presentations On IndiaYasser KhanNo ratings yet

- Zomato LTD.: Investment RationaleDocument10 pagesZomato LTD.: Investment RationaleSumundra RathNo ratings yet

- Morning Star Report 20190916052149Document1 pageMorning Star Report 20190916052149ChankyaNo ratings yet

- Morning Star Report 20190916052137Document1 pageMorning Star Report 20190916052137ChankyaNo ratings yet

- FMR Oct 2023Document39 pagesFMR Oct 2023Qamber RazaNo ratings yet

- Morning Star Report 20190916052116Document1 pageMorning Star Report 20190916052116ChankyaNo ratings yet

- Investment Pricing Methods: A Guide for Accounting and Financial ProfessionalsFrom EverandInvestment Pricing Methods: A Guide for Accounting and Financial ProfessionalsNo ratings yet

- Job and Batch Costing 2Document3 pagesJob and Batch Costing 2TAFARA MUKARAKATENo ratings yet

- Genesis' Trial Balance Reflected The FollowingDocument1 pageGenesis' Trial Balance Reflected The FollowingQueen ValleNo ratings yet

- Entrepreneurship and Small Business NotesDocument225 pagesEntrepreneurship and Small Business NotesSatish Kumar RanjanNo ratings yet

- GeM Bidding 4842619Document30 pagesGeM Bidding 4842619Deepak JainNo ratings yet

- Operating/Safety Instructions Consignes de Fonctionnement/sécurité Instrucciones de Funcionamiento y SeguridadDocument40 pagesOperating/Safety Instructions Consignes de Fonctionnement/sécurité Instrucciones de Funcionamiento y Seguridadangel jose trinidadNo ratings yet

- List EP COR PDFDocument3 pagesList EP COR PDFCesarNo ratings yet

- Full Download Introduction To Emergency Management 1st Edition Lindell Solutions ManualDocument36 pagesFull Download Introduction To Emergency Management 1st Edition Lindell Solutions Manualbeveridgetamera1544100% (41)

- Taxation 101 Basic Principles in Philippine Taxation by JR Lopez GonzalesDocument8 pagesTaxation 101 Basic Principles in Philippine Taxation by JR Lopez Gonzalesjrgon_zales92% (25)

- The Holts of Alamance County - Textiles HistoryDocument4 pagesThe Holts of Alamance County - Textiles HistoryemilyNo ratings yet

- 74-Article Text-279-2-10-20210614Document8 pages74-Article Text-279-2-10-20210614Tâm NguyễnNo ratings yet

- Instrukcja Obslugi ADLER AD 7302Document60 pagesInstrukcja Obslugi ADLER AD 7302kosay52130No ratings yet

- Chapter-9 Imperfect CompetitionDocument23 pagesChapter-9 Imperfect Competitiongr8_amaraNo ratings yet

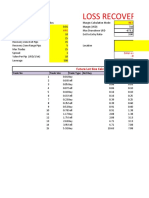

- Loss Recovery Trader CalculatorDocument31 pagesLoss Recovery Trader CalculatorMuhammad Rizki Amin100% (1)

- SafetyDocument25 pagesSafetyflorencedago08No ratings yet

- Jam 2023Document35 pagesJam 2023iamphilospher1No ratings yet

- Atlas Copco: Compressed Air FiltersDocument50 pagesAtlas Copco: Compressed Air FiltersAlonso GomezNo ratings yet

- A Guided Book of Engineering EconomicsDocument54 pagesA Guided Book of Engineering EconomicsmusaNo ratings yet

- Tata Green Batteries Online Warranty ManualDocument5 pagesTata Green Batteries Online Warranty ManualManoj Kumar NayakNo ratings yet

- 05 AC212 Lecture 5-Marginal Costing and Absorption Costing PDFDocument22 pages05 AC212 Lecture 5-Marginal Costing and Absorption Costing PDFsengpisalNo ratings yet

- OSLeak Repair Clamp FlysheetDocument2 pagesOSLeak Repair Clamp FlysheetTT0% (1)

- Mapping RR Non Staff 2024 NewDocument146 pagesMapping RR Non Staff 2024 NewpalasgedoNo ratings yet

- Brother LK3 Instruction ManualDocument16 pagesBrother LK3 Instruction ManualJeremy IdkNo ratings yet

- JAIBB Comparative Syllabus PDFDocument8 pagesJAIBB Comparative Syllabus PDFshahaneauez alamNo ratings yet

- Armitron WarrantyDocument1 pageArmitron Warrantyb2basicsNo ratings yet

- Ardi Said, IGN Anom Maruto, Sri Andayani, Program Studi Administrasi Bisnis-Universitas 17 Agustus 1945 SurabayaDocument17 pagesArdi Said, IGN Anom Maruto, Sri Andayani, Program Studi Administrasi Bisnis-Universitas 17 Agustus 1945 SurabayaNaning Panggrahito Lagilagi D'bieterzNo ratings yet

- @canotes - Final Customs Question Bank May, Nov 20 by ICAI PDFDocument111 pages@canotes - Final Customs Question Bank May, Nov 20 by ICAI PDFPraneelNo ratings yet

- Session 2 - Basics of DemandDocument13 pagesSession 2 - Basics of DemandSayan GangulyNo ratings yet

Download as pdf or txt

You might also like

- IB Economics Coursebook 3ed Test Your Understanding AnswersDocument26 pagesIB Economics Coursebook 3ed Test Your Understanding AnswersIzyan LiraniNo ratings yet

- Issues in Pakistan EconomyDocument4 pagesIssues in Pakistan EconomyMuhammad Waqas100% (3)

- Assignment From Lecture 3Document5 pagesAssignment From Lecture 3J. NawreenNo ratings yet

- Cmi Report April 2023Document25 pagesCmi Report April 2023Pankaj MaryeNo ratings yet

- CMI - India 2023Document29 pagesCMI - India 2023Vignesh RaghunathanNo ratings yet

- JS-MCB 29feb24Document3 pagesJS-MCB 29feb24Rizwan IqbalNo ratings yet

- Lemon Tree Hotels.Document9 pagesLemon Tree Hotels.Anonymous brpVlaVBNo ratings yet

- Slower Growth Stubborn Inflation: APRIL 3, 2023Document20 pagesSlower Growth Stubborn Inflation: APRIL 3, 2023Tomas SuaresNo ratings yet

- Oil & Gas POV GLOBALDocument8 pagesOil & Gas POV GLOBALGustavo AgudeloNo ratings yet

- Maceef FS202212Document10 pagesMaceef FS202212Guan JooNo ratings yet

- NZ Consumer Confidence JuneDocument4 pagesNZ Consumer Confidence JuneTim MooreNo ratings yet

- Scaling New Horizons: Key Performance IndicatorsDocument1 pageScaling New Horizons: Key Performance IndicatorsPapu SahooNo ratings yet

- Accomplished RCA: KYC Quality ReportDocument1 pageAccomplished RCA: KYC Quality ReportHan Htun OoNo ratings yet

- Pick of The Day (Short Term Delivery Call) - Va Tech Wabag LTD - 08-11-2023Document3 pagesPick of The Day (Short Term Delivery Call) - Va Tech Wabag LTD - 08-11-2023Anurag SanodiaNo ratings yet

- IDirect JKTyres ShubhNivesh May24Document4 pagesIDirect JKTyres ShubhNivesh May24Krunal PatelNo ratings yet

- ASAL Business Coursebook Answers PDF 15Document10 pagesASAL Business Coursebook Answers PDF 15HanNo ratings yet

- Retail Lending: in A Post Covid WorldDocument24 pagesRetail Lending: in A Post Covid WorldAbhishek JaiswalNo ratings yet

- Karen Ward IsfwDocument13 pagesKaren Ward IsfwLEE JEFFNo ratings yet

- Cement - 3QFY24 Earnings To Decline by 25%QoQDocument4 pagesCement - 3QFY24 Earnings To Decline by 25%QoQmuhammadghufran1No ratings yet

- Q3 - 2023 - Investor PresentationDocument37 pagesQ3 - 2023 - Investor PresentationMo LaNo ratings yet

- Cloudpt TP 0.79 by RHBDocument13 pagesCloudpt TP 0.79 by RHBNabil JazliNo ratings yet

- IDirect IDFCBank Q4FY23Document6 pagesIDirect IDFCBank Q4FY23Silambarasan AshokkumarNo ratings yet

- Fino Payments Bank Q3FY22 Investor PresentationDocument53 pagesFino Payments Bank Q3FY22 Investor Presentationg_sivakumarNo ratings yet

- Houlihan Lokey - Travel-&-Hospitality-Update - q3-2023Document17 pagesHoulihan Lokey - Travel-&-Hospitality-Update - q3-2023Antonius VincentNo ratings yet

- Seniors Housing Annual Review 2023-24-10752 KFDocument16 pagesSeniors Housing Annual Review 2023-24-10752 KFashwini atNo ratings yet

- Business Guardian (New Delhi) - May 23, 2023Document8 pagesBusiness Guardian (New Delhi) - May 23, 2023Camilo BenavidesNo ratings yet

- Industry - : SnapshotDocument14 pagesIndustry - : SnapshotBích DiệuNo ratings yet

- Motilal Nifty Next 50 Fund - 31MAY2024Document1 pageMotilal Nifty Next 50 Fund - 31MAY2024Krishnanand GaurNo ratings yet

- IIFL - Powermech Projects - Company Update - 20230118-1Document9 pagesIIFL - Powermech Projects - Company Update - 20230118-1Dhittbanda GamingNo ratings yet

- Axis Fixed Term Plan Series 102 1133 Days Direct High Yearly Dividend PayoutDocument1 pageAxis Fixed Term Plan Series 102 1133 Days Direct High Yearly Dividend PayoutChankyaNo ratings yet

- Morningstarreport20190906084844 PDFDocument1 pageMorningstarreport20190906084844 PDFChankyaNo ratings yet

- Axis Fixed Term Plan Series 102 1133 Days Regular High Yearly Dividend PayoutDocument1 pageAxis Fixed Term Plan Series 102 1133 Days Regular High Yearly Dividend PayoutChankyaNo ratings yet

- LGS Dom Review 23rd Sep'23Document12 pagesLGS Dom Review 23rd Sep'23Abhijit SahaNo ratings yet

- Capt SUBRA ZIA Conference - Post Pandemic ChallengesDocument24 pagesCapt SUBRA ZIA Conference - Post Pandemic ChallengesJohn HoangNo ratings yet

- Global Cross Border B2C E-Commerce Market 2020: Report Highlights & Methodology SharingDocument9 pagesGlobal Cross Border B2C E-Commerce Market 2020: Report Highlights & Methodology Sharingngungo12345678No ratings yet

- Morning Star Report 20190906084839Document1 pageMorning Star Report 20190906084839ChankyaNo ratings yet

- Customer Complaint Sep'20Document23 pagesCustomer Complaint Sep'20SQA HOSURNo ratings yet

- Birla Insurance Individual Maximiser Fund December 2023Document1 pageBirla Insurance Individual Maximiser Fund December 2023sharmaoriginalNo ratings yet

- Morning Star Report 20190906084927Document1 pageMorning Star Report 20190906084927ChankyaNo ratings yet

- IDirect JMFinancial StockTalesDocument12 pagesIDirect JMFinancial StockTalesPorus Saranjit SinghNo ratings yet

- Morning Star Report 20190906084925Document1 pageMorning Star Report 20190906084925ChankyaNo ratings yet

- Of The Day (Short Term Delivery Call) - PI Industries LTDDocument3 pagesOf The Day (Short Term Delivery Call) - PI Industries LTDdeepaksinghbishtNo ratings yet

- Industry Dashboard Nov23Document114 pagesIndustry Dashboard Nov23Vignesh RaghunathanNo ratings yet

- ICRA Analytics Mutual Fund Screener - Q4FY23Document44 pagesICRA Analytics Mutual Fund Screener - Q4FY23Tshering SherpaNo ratings yet

- India Sectoral - Credit - Deployment - For - March - 2024Document7 pagesIndia Sectoral - Credit - Deployment - For - March - 2024purveshparekhNo ratings yet

- PGIM India Money Market FundDocument1 pagePGIM India Money Market FundYogi173No ratings yet

- Morningstarreport20221024033734 Canara Robeco SmallDocument1 pageMorningstarreport20221024033734 Canara Robeco SmallNiaz Abdul KarimNo ratings yet

- SuprajitDocument5 pagesSuprajitabhimanyugodara007No ratings yet

- 1Q - FY2023 Quarterly Results Briefing - 1Document18 pages1Q - FY2023 Quarterly Results Briefing - 1RidtwanNo ratings yet

- Morning Star Report 20190915054829Document1 pageMorning Star Report 20190915054829ChankyaNo ratings yet

- Autos: Super Tax To Suppress Earnings During 4QFY22Document3 pagesAutos: Super Tax To Suppress Earnings During 4QFY22Khalid Abbas ChaudhryNo ratings yet

- Sanchay Public Deposit FormDocument6 pagesSanchay Public Deposit Formmanoj barokaNo ratings yet

- Mutual Fund ScreenerDocument41 pagesMutual Fund ScreenerSantoshNo ratings yet

- QMR October 2023 - December 2023Document51 pagesQMR October 2023 - December 2023Debt Market GeekNo ratings yet

- Adani Ports Investor Presentation - London NDR PDFDocument31 pagesAdani Ports Investor Presentation - London NDR PDFHarsh GuptaNo ratings yet

- Annual MSP Performance Report Jan Dec 2021 Final CleanDocument22 pagesAnnual MSP Performance Report Jan Dec 2021 Final CleanKian Andrei EngayNo ratings yet

- External Debt Development and Management: Presentations On IndiaDocument22 pagesExternal Debt Development and Management: Presentations On IndiaYasser KhanNo ratings yet

- Zomato LTD.: Investment RationaleDocument10 pagesZomato LTD.: Investment RationaleSumundra RathNo ratings yet

- Morning Star Report 20190916052149Document1 pageMorning Star Report 20190916052149ChankyaNo ratings yet

- Morning Star Report 20190916052137Document1 pageMorning Star Report 20190916052137ChankyaNo ratings yet

- FMR Oct 2023Document39 pagesFMR Oct 2023Qamber RazaNo ratings yet

- Morning Star Report 20190916052116Document1 pageMorning Star Report 20190916052116ChankyaNo ratings yet

- Investment Pricing Methods: A Guide for Accounting and Financial ProfessionalsFrom EverandInvestment Pricing Methods: A Guide for Accounting and Financial ProfessionalsNo ratings yet

- Job and Batch Costing 2Document3 pagesJob and Batch Costing 2TAFARA MUKARAKATENo ratings yet

- Genesis' Trial Balance Reflected The FollowingDocument1 pageGenesis' Trial Balance Reflected The FollowingQueen ValleNo ratings yet

- Entrepreneurship and Small Business NotesDocument225 pagesEntrepreneurship and Small Business NotesSatish Kumar RanjanNo ratings yet

- GeM Bidding 4842619Document30 pagesGeM Bidding 4842619Deepak JainNo ratings yet

- Operating/Safety Instructions Consignes de Fonctionnement/sécurité Instrucciones de Funcionamiento y SeguridadDocument40 pagesOperating/Safety Instructions Consignes de Fonctionnement/sécurité Instrucciones de Funcionamiento y Seguridadangel jose trinidadNo ratings yet

- List EP COR PDFDocument3 pagesList EP COR PDFCesarNo ratings yet

- Full Download Introduction To Emergency Management 1st Edition Lindell Solutions ManualDocument36 pagesFull Download Introduction To Emergency Management 1st Edition Lindell Solutions Manualbeveridgetamera1544100% (41)

- Taxation 101 Basic Principles in Philippine Taxation by JR Lopez GonzalesDocument8 pagesTaxation 101 Basic Principles in Philippine Taxation by JR Lopez Gonzalesjrgon_zales92% (25)

- The Holts of Alamance County - Textiles HistoryDocument4 pagesThe Holts of Alamance County - Textiles HistoryemilyNo ratings yet

- 74-Article Text-279-2-10-20210614Document8 pages74-Article Text-279-2-10-20210614Tâm NguyễnNo ratings yet

- Instrukcja Obslugi ADLER AD 7302Document60 pagesInstrukcja Obslugi ADLER AD 7302kosay52130No ratings yet

- Chapter-9 Imperfect CompetitionDocument23 pagesChapter-9 Imperfect Competitiongr8_amaraNo ratings yet

- Loss Recovery Trader CalculatorDocument31 pagesLoss Recovery Trader CalculatorMuhammad Rizki Amin100% (1)

- SafetyDocument25 pagesSafetyflorencedago08No ratings yet

- Jam 2023Document35 pagesJam 2023iamphilospher1No ratings yet

- Atlas Copco: Compressed Air FiltersDocument50 pagesAtlas Copco: Compressed Air FiltersAlonso GomezNo ratings yet

- A Guided Book of Engineering EconomicsDocument54 pagesA Guided Book of Engineering EconomicsmusaNo ratings yet

- Tata Green Batteries Online Warranty ManualDocument5 pagesTata Green Batteries Online Warranty ManualManoj Kumar NayakNo ratings yet

- 05 AC212 Lecture 5-Marginal Costing and Absorption Costing PDFDocument22 pages05 AC212 Lecture 5-Marginal Costing and Absorption Costing PDFsengpisalNo ratings yet

- OSLeak Repair Clamp FlysheetDocument2 pagesOSLeak Repair Clamp FlysheetTT0% (1)

- Mapping RR Non Staff 2024 NewDocument146 pagesMapping RR Non Staff 2024 NewpalasgedoNo ratings yet

- Brother LK3 Instruction ManualDocument16 pagesBrother LK3 Instruction ManualJeremy IdkNo ratings yet

- JAIBB Comparative Syllabus PDFDocument8 pagesJAIBB Comparative Syllabus PDFshahaneauez alamNo ratings yet

- Armitron WarrantyDocument1 pageArmitron Warrantyb2basicsNo ratings yet

- Ardi Said, IGN Anom Maruto, Sri Andayani, Program Studi Administrasi Bisnis-Universitas 17 Agustus 1945 SurabayaDocument17 pagesArdi Said, IGN Anom Maruto, Sri Andayani, Program Studi Administrasi Bisnis-Universitas 17 Agustus 1945 SurabayaNaning Panggrahito Lagilagi D'bieterzNo ratings yet

- @canotes - Final Customs Question Bank May, Nov 20 by ICAI PDFDocument111 pages@canotes - Final Customs Question Bank May, Nov 20 by ICAI PDFPraneelNo ratings yet

- Session 2 - Basics of DemandDocument13 pagesSession 2 - Basics of DemandSayan GangulyNo ratings yet