Download as pdf or txt

You might also like

- Bit CoinDocument7 pagesBit CoinYoga Prima Nanda0% (2)

- Role of RBI in Economic and Social Development PDFDocument88 pagesRole of RBI in Economic and Social Development PDFKaruna LadeNo ratings yet

- Untitled13 PDFDocument22 pagesUntitled13 PDFErsin TukenmezNo ratings yet

- Notes - IfM - MergedDocument210 pagesNotes - IfM - MergedNeerajNo ratings yet

- Chapter 1-IBF IntroductionDocument61 pagesChapter 1-IBF IntroductionHay JirenyaaNo ratings yet

- Ifm Module 1Document9 pagesIfm Module 1Ramya GowdaNo ratings yet

- Importance of International EconomicDocument3 pagesImportance of International Economicrajdeep singh100% (1)

- International Financial Management: The Outlook of The World Through Domestic MarketsDocument49 pagesInternational Financial Management: The Outlook of The World Through Domestic MarketsSuryansh IvaturiNo ratings yet

- Afu 08504 - International Finance - Introduction and The ImsDocument18 pagesAfu 08504 - International Finance - Introduction and The ImsAbdulkarim Hamisi KufakunogaNo ratings yet

- Research Project ReportDocument55 pagesResearch Project ReportharryNo ratings yet

- Chapter OneDocument8 pagesChapter OneMan SanchoNo ratings yet

- International FinanceDocument15 pagesInternational FinanceManuel Andres OrtizNo ratings yet

- CH 1 - Scope of International FinanceDocument7 pagesCH 1 - Scope of International Financepritesh_baidya269100% (3)

- Final Assignment Forex MarketDocument6 pagesFinal Assignment Forex MarketUrvish Tushar DalalNo ratings yet

- Nternational Economics and Asis of International Rade: Presented byDocument26 pagesNternational Economics and Asis of International Rade: Presented byShriya ShinNo ratings yet

- If - Mba 4Document72 pagesIf - Mba 4mansisharma8301No ratings yet

- International Monetary and Financial Systems - Chapter-4 MbsDocument62 pagesInternational Monetary and Financial Systems - Chapter-4 MbsArjun MishraNo ratings yet

- Ifm NotesDocument70 pagesIfm Notessridhara.ramkarthik173No ratings yet

- Report Module ContemporaryDocument8 pagesReport Module ContemporaryEarl Lord Vincent OlivaNo ratings yet

- TCQT EssayDocument11 pagesTCQT EssayThư TrầnNo ratings yet

- International FinanceDocument2 pagesInternational FinanceMansi PatwaNo ratings yet

- Importance of International FinanceDocument4 pagesImportance of International FinanceNandini Jagan29% (7)

- Interational Marketing HardDocument11 pagesInterational Marketing HardKrutika ManeNo ratings yet

- International Financial Management: UNIT I: An Overview, Theoretical Developments. International FinancialDocument45 pagesInternational Financial Management: UNIT I: An Overview, Theoretical Developments. International FinancialADESH BAJPAINo ratings yet

- International FinanceDocument18 pagesInternational FinanceMaría Fernanda LeónNo ratings yet

- Additional-Learning-Material GFEBDocument6 pagesAdditional-Learning-Material GFEBcharlenealvarez59No ratings yet

- Afu 08504 - International Finance - Introduction and The ImsDocument18 pagesAfu 08504 - International Finance - Introduction and The ImsAbdulkarim Hamisi KufakunogaNo ratings yet

- International Economic Integration and Institution WRDocument10 pagesInternational Economic Integration and Institution WRYvonne LlamadaNo ratings yet

- Presentation On International Financial ManagementDocument17 pagesPresentation On International Financial ManagementSukruth SNo ratings yet

- International Financial Markets-Chapter 8Document12 pagesInternational Financial Markets-Chapter 8Marlou AbejuelaNo ratings yet

- Winter 2017 BBA Semester 6 BBA603: Role of International Financial InstitutionsDocument10 pagesWinter 2017 BBA Semester 6 BBA603: Role of International Financial InstitutionsSujal SNo ratings yet

- International FinanceDocument48 pagesInternational FinanceAizik Lessik AreveNo ratings yet

- Module 1 IfmDocument17 pagesModule 1 IfmAYISHA BEEVI UNo ratings yet

- FM 3103 Unit I PendingDocument35 pagesFM 3103 Unit I PendingKumardeep SinghaNo ratings yet

- Introduction to International EconomicsDocument2 pagesIntroduction to International Economicsiyakaremyee70No ratings yet

- Global EconomyDocument4 pagesGlobal EconomyKarinaNo ratings yet

- International Financial Management Unit - IDocument15 pagesInternational Financial Management Unit - IBHRAMARBAR SAHANINo ratings yet

- IRL 3109 - Lecture 6 (2020-12-10)Document26 pagesIRL 3109 - Lecture 6 (2020-12-10)nolissaNo ratings yet

- IFM1Document12 pagesIFM1Shaan MahendraNo ratings yet

- Chapter 1Document20 pagesChapter 1Jubayer 3DNo ratings yet

- Fundamentals of International FinanceDocument11 pagesFundamentals of International FinanceChirag KotianNo ratings yet

- Economic SystemDocument7 pagesEconomic SystemHabib ur RehmanNo ratings yet

- Unit I &II and Others AlsoDocument41 pagesUnit I &II and Others AlsoRaj VermaNo ratings yet

- I.E Week 1Document16 pagesI.E Week 1CHRISTINE JOY MACAYANo ratings yet

- International Finance - Hons NotesDocument30 pagesInternational Finance - Hons NotesafeeftalhapcNo ratings yet

- 1 - Reading 1 International Finance ImportanceDocument3 pages1 - Reading 1 International Finance ImportanceLina RamosNo ratings yet

- International Financial Management Notes Unit-1Document15 pagesInternational Financial Management Notes Unit-1Geetha aptdcNo ratings yet

- INTERNATIONAL FINANCE NotesDocument8 pagesINTERNATIONAL FINANCE Notesanon_879418278No ratings yet

- TMIF Chapter ThreeDocument40 pagesTMIF Chapter ThreeYibeltal AssefaNo ratings yet

- Uluslararasi Fi̇nans 1Document18 pagesUluslararasi Fi̇nans 1rhkrktNo ratings yet

- International FinanceDocument2 pagesInternational FinanceElyas SaadNo ratings yet

- Intl FinanceDocument10 pagesIntl FinanceMAYNo ratings yet

- 01 Global Financial System: 1.1 International InstitutionsDocument25 pages01 Global Financial System: 1.1 International Institutionsapi-26524819No ratings yet

- IFM M.Com NotesDocument36 pagesIFM M.Com NotesViraja GuruNo ratings yet

- International FinanceDocument36 pagesInternational FinanceHetal bariaNo ratings yet

- What Is The Relevance of IMF, World Bank, and General Agreement On Tariffs and Trade (GATT) To The Global Economy?Document4 pagesWhat Is The Relevance of IMF, World Bank, and General Agreement On Tariffs and Trade (GATT) To The Global Economy?ElmaNo ratings yet

- International Finance: Lecture# 3 and 4Document4 pagesInternational Finance: Lecture# 3 and 4bakhtawar soniaNo ratings yet

- International Finance and Its ImportanceDocument7 pagesInternational Finance and Its ImportancePrasanjit BiswasNo ratings yet

- Topic 4 - Gonzales & MicolobDocument11 pagesTopic 4 - Gonzales & MicolobHaries Vi MicolobNo ratings yet

- International Eco and Policy Assignment Question 1Document10 pagesInternational Eco and Policy Assignment Question 1Deepak Singh Bisht100% (1)

- Chapter 1 Globalization and Multinational FirmDocument30 pagesChapter 1 Globalization and Multinational FirmIrnes ImamovicNo ratings yet

- MF Module 4Document50 pagesMF Module 4Gouri K MakatiNo ratings yet

- Dynamics of ValueDocument8 pagesDynamics of ValueHardik GoriNo ratings yet

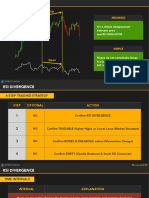

- RSI DivergenceDocument18 pagesRSI DivergencevuhuyhnvnNo ratings yet

- Chapter 4Document5 pagesChapter 4Angelica PagaduanNo ratings yet

- Chapter 01Document2 pagesChapter 01badunktuaNo ratings yet

- Atanasov and Nenovsky Money-And-Prices-In-The-18th-19th-Centuries-Bulgarian-Historiography Bulgarian Historical Review 2019Document33 pagesAtanasov and Nenovsky Money-And-Prices-In-The-18th-19th-Centuries-Bulgarian-Historiography Bulgarian Historical Review 2019Hristiyan AtanasovNo ratings yet

- HSBC CHINA Black SampleDocument1 pageHSBC CHINA Black SamplejinnahcorporationsNo ratings yet

- Unit - Problem Mejia Pablo1Document2 pagesUnit - Problem Mejia Pablo1CM LanceNo ratings yet

- Moller Expert Report 28ss 29 28mtm 29 2c 1 6 2014Document43 pagesMoller Expert Report 28ss 29 28mtm 29 2c 1 6 2014api-310287335100% (1)

- Capsule For Sbi Po Mainsrrbrbi Assistant UpdatedDocument55 pagesCapsule For Sbi Po Mainsrrbrbi Assistant Updatedcrazy about readingNo ratings yet

- Hughes - Crony CapitalismDocument7 pagesHughes - Crony CapitalismAntonio JoséNo ratings yet

- InvoiceDocument1 pageInvoiceVignesh KumarNo ratings yet

- Credit TransactionDocument22 pagesCredit TransactionAnalynNo ratings yet

- ACCO 20053 Lecture Notes 2 - Imprest System and Petty Cash FundDocument7 pagesACCO 20053 Lecture Notes 2 - Imprest System and Petty Cash FundVincent Luigil AlceraNo ratings yet

- Payment Registration SlipDocument1 pagePayment Registration SlipDaniel Kyeyune MuwangaNo ratings yet

- Madhu Chaudhary ReportDocument36 pagesMadhu Chaudhary ReportMadhu ChyNo ratings yet

- Please Do Not Write On This Examination FormDocument8 pagesPlease Do Not Write On This Examination Formzaidashraf007No ratings yet

- What Are The Functions of BanksDocument15 pagesWhat Are The Functions of BanksppperfectNo ratings yet

- Consumer S Behaviour Regarding Cashless Payments During The Covid-19 PandemicDocument13 pagesConsumer S Behaviour Regarding Cashless Payments During The Covid-19 PandemicAesthetica MoonNo ratings yet

- Account Statement For Account Number0674001500113444: Branch DetailsDocument3 pagesAccount Statement For Account Number0674001500113444: Branch DetailsVed sinhaNo ratings yet

- TransactionCodes FIORIDocument94 pagesTransactionCodes FIORIMounir ZakiNo ratings yet

- ECON138 Syllabus W23Document9 pagesECON138 Syllabus W23bmora018No ratings yet

- International Payment: Edward G. HinkelmanDocument23 pagesInternational Payment: Edward G. HinkelmanQuỳnh PhươngNo ratings yet

- HSBC Vietnam PaymentDocument2 pagesHSBC Vietnam PaymentcuongNo ratings yet

- Survey and Thought of Financial Management and EduDocument4 pagesSurvey and Thought of Financial Management and EduDENMARKNo ratings yet

- EFIN542 U09 T01 PowerPointDocument26 pagesEFIN542 U09 T01 PowerPointcustomsgyanNo ratings yet

- ArdancertDocument14 pagesArdancertclube de inteligência e desenvolvimento coletivoNo ratings yet