Download as pdf or txt

You might also like

- PDFDocument2 pagesPDFLIMNo ratings yet

- Marginal Costing & Absorption CostingDocument56 pagesMarginal Costing & Absorption CostingHoàng Phương ThảoNo ratings yet

- Local Voice - Winter 2019Document32 pagesLocal Voice - Winter 2019MoveUP, the Movement of United ProfessionalsNo ratings yet

- Banking DictionaryDocument188 pagesBanking DictionaryRanjan Shetty100% (1)

- Absorption and Variable Costing ReviewDocument13 pagesAbsorption and Variable Costing ReviewRodelLabor100% (1)

- Topic 7 - Absorption & Marginal CostingDocument8 pagesTopic 7 - Absorption & Marginal CostingMuhammad Alif100% (5)

- 1491820614costing by CA Jitender Singh (Overhead, Labour, Material, Marginal, Ratio, Machine Hour RateDocument311 pages1491820614costing by CA Jitender Singh (Overhead, Labour, Material, Marginal, Ratio, Machine Hour RateRam IyerNo ratings yet

- Module 4 Absorption and Variable Costing NotesDocument3 pagesModule 4 Absorption and Variable Costing NotesMadielyn Santarin Miranda100% (3)

- Chapter 1-Over ViewDocument39 pagesChapter 1-Over ViewMalcolmNo ratings yet

- DAC 5013-Week 03Document60 pagesDAC 5013-Week 03Dilshan J. NiranjanNo ratings yet

- Week 67 and 9 Absorption Costing Vs Marginal Costing Costing MethodDocument31 pagesWeek 67 and 9 Absorption Costing Vs Marginal Costing Costing MethodMai LyNo ratings yet

- Absorption and Variable Costing: Types of Product Costing MethodDocument2 pagesAbsorption and Variable Costing: Types of Product Costing MethodKuya ANo ratings yet

- Cost & MGT II CH 1Document13 pagesCost & MGT II CH 1fikruhope533No ratings yet

- Review Session 01 MA Topics 1-6 BeforeDocument32 pagesReview Session 01 MA Topics 1-6 BeforemisalNo ratings yet

- Review Session 01 MA Topics 1-6 AfterDocument32 pagesReview Session 01 MA Topics 1-6 AftermisalNo ratings yet

- Marginal and Absorption CostingDocument8 pagesMarginal and Absorption CostingEniola OgunmonaNo ratings yet

- Costman Variable CostingDocument2 pagesCostman Variable CostingJeremi BernardoNo ratings yet

- Absorption and Marginal CostingDocument19 pagesAbsorption and Marginal CostingsadikzeenatNo ratings yet

- Chapter 10 - Marginal and Absorption CostingDocument8 pagesChapter 10 - Marginal and Absorption CostingkundiarshdeepNo ratings yet

- 03 MAS - Var. & Absorption CostingDocument6 pages03 MAS - Var. & Absorption CostingManwol JangNo ratings yet

- 3MA 03 Absortion and Variable CostingDocument3 pages3MA 03 Absortion and Variable CostingAbigail Regondola BonitaNo ratings yet

- Chapter 7Document4 pagesChapter 7Mixx MineNo ratings yet

- CH 1 CM Cost-Volume-Profit Analysis, Absorption, and Variable CostingDocument15 pagesCH 1 CM Cost-Volume-Profit Analysis, Absorption, and Variable CostingOROM VINE100% (5)

- Mas-03: Absorption & Variable CostingDocument4 pagesMas-03: Absorption & Variable CostingClint AbenojaNo ratings yet

- 9Document16 pages9Asal IslamNo ratings yet

- Absorption and Variable CostingDocument5 pagesAbsorption and Variable CostingKIM RAGANo ratings yet

- Presentation - Chapter3 & 9Document49 pagesPresentation - Chapter3 & 9rajeshaisdu009No ratings yet

- Absorption Costing Vs Variable CostingDocument20 pagesAbsorption Costing Vs Variable CostingMa. Alene MagdaraogNo ratings yet

- Absorption Costing & Variable CostingDocument20 pagesAbsorption Costing & Variable Costingsaidkhatib368No ratings yet

- Chapter 4 Income Measurement and ReportingDocument13 pagesChapter 4 Income Measurement and ReportingOmisha KhatiwadaNo ratings yet

- Variable Costing CRDocument21 pagesVariable Costing CRMary Rose GonzalesNo ratings yet

- Marginal Costing TYBAFDocument13 pagesMarginal Costing TYBAFAkash BugadeNo ratings yet

- Marginal and Absorption CostingDocument21 pagesMarginal and Absorption Costingkelvin mboyaNo ratings yet

- Lecture 4 - 5 17102022 032709am 07032023 090715pm 17102023 015148pmDocument41 pagesLecture 4 - 5 17102022 032709am 07032023 090715pm 17102023 015148pmmurtaza haiderNo ratings yet

- Session-16-17-18-CVP AnalysisDocument78 pagesSession-16-17-18-CVP Analysis020Abhisek KhadangaNo ratings yet

- IWB Chapter 5 - Marginal and Absorption CostingDocument28 pagesIWB Chapter 5 - Marginal and Absorption Costingjulioruiz891No ratings yet

- 04 Variable and Absorption CostingDocument8 pages04 Variable and Absorption CostingJunZon VelascoNo ratings yet

- Absorption and Marginal CostingDocument25 pagesAbsorption and Marginal CostingMehwish ziadNo ratings yet

- F2 Marginal Costing & Contribution TheoryDocument7 pagesF2 Marginal Costing & Contribution TheoryCourage KanyonganiseNo ratings yet

- Absorption CostingDocument34 pagesAbsorption Costinggaurav pandeyNo ratings yet

- Contribution Approach 2Document16 pagesContribution Approach 2kualler80% (5)

- ACT121 - Topic 5Document5 pagesACT121 - Topic 5Juan FrivaldoNo ratings yet

- ACCTG 42 Module 3Document5 pagesACCTG 42 Module 3Hazel Grace PaguiaNo ratings yet

- Activity Based CostingDocument28 pagesActivity Based CostingApril TorresNo ratings yet

- Absorption Costing For STDocument6 pagesAbsorption Costing For STDEREJENo ratings yet

- Marginal Costing & Decision MakingDocument8 pagesMarginal Costing & Decision MakingPraneeth KNo ratings yet

- Niti MarginalDocument19 pagesNiti MarginalNitichandra IngleNo ratings yet

- Chapter 2 Marginal CostingDocument21 pagesChapter 2 Marginal CostingLan Nhi NguyenNo ratings yet

- Variable Costing: A Tool For Management: © 2010 The Mcgraw-Hill Companies, IncDocument29 pagesVariable Costing: A Tool For Management: © 2010 The Mcgraw-Hill Companies, IncTurbo TechNo ratings yet

- Week 5 NotesDocument9 pagesWeek 5 NotescalebNo ratings yet

- CHAPTER 3-4 CacDocument7 pagesCHAPTER 3-4 CacCARLA MEDRANONo ratings yet

- M3 Variable Costing As Management ToolDocument6 pagesM3 Variable Costing As Management Toolwingsenigma 00No ratings yet

- Marginal & Absorption CostingDocument12 pagesMarginal & Absorption CostingMayal Sheikh100% (1)

- MAS 04 Absorption CostingDocument6 pagesMAS 04 Absorption CostingJoelyn Grace MontajesNo ratings yet

- Variable CostingDocument7 pagesVariable CostingRainie LopezNo ratings yet

- SIM - Variable and Absorption Costing - 0Document5 pagesSIM - Variable and Absorption Costing - 0lilienesieraNo ratings yet

- Absorption CostingDocument10 pagesAbsorption Costingberyl_hst100% (1)

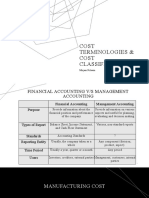

- Cost Terminologies & Cost Classification: Mirjam NilssonDocument13 pagesCost Terminologies & Cost Classification: Mirjam NilssonHitesh JainNo ratings yet

- Absorption and Variable CostingDocument3 pagesAbsorption and Variable CostingDhona Mae FidelNo ratings yet

- Cost Terms, Concepts and Classification Session 2 2018 For UploadingDocument19 pagesCost Terms, Concepts and Classification Session 2 2018 For UploadingSohaib ArifNo ratings yet

- Variable Costing & Segment Reporting-FINALDocument29 pagesVariable Costing & Segment Reporting-FINALTin Bernadette DominicoNo ratings yet

- 006 Camist Ch04 Amndd Hs PP 79-102 Branded BW RP SecDocument25 pages006 Camist Ch04 Amndd Hs PP 79-102 Branded BW RP SecMd Salahuddin HowladerNo ratings yet

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageFrom EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageRating: 5 out of 5 stars5/5 (1)

- Ch14 - Organisational Culture - UpdatedDocument27 pagesCh14 - Organisational Culture - UpdatedrbnbalachandranNo ratings yet

- Chapter 3 - Consumer Behaviour and ChoiceDocument61 pagesChapter 3 - Consumer Behaviour and ChoicerbnbalachandranNo ratings yet

- Ch04 - Workplace Emotions, Attitudes and Stress - UpdatedDocument40 pagesCh04 - Workplace Emotions, Attitudes and Stress - UpdatedrbnbalachandranNo ratings yet

- Chapter 8 Human Resource ManagementDocument36 pagesChapter 8 Human Resource ManagementrbnbalachandranNo ratings yet

- STD Costing Variance Analysis - StudentDocument28 pagesSTD Costing Variance Analysis - StudentrbnbalachandranNo ratings yet

- Budget For Planning - StudentDocument20 pagesBudget For Planning - StudentrbnbalachandranNo ratings yet

- Igcse Accounting Control Accounts - Questions AnswersDocument24 pagesIgcse Accounting Control Accounts - Questions AnswersOmar WaheedNo ratings yet

- Bank Reconciliation ProcessDocument6 pagesBank Reconciliation ProcessbluephoeNo ratings yet

- 2.caro For Company AuditDocument43 pages2.caro For Company AuditchariNo ratings yet

- Annex I MSN012024-1Document5 pagesAnnex I MSN012024-1moashi chandraNo ratings yet

- Merger ReportDocument9 pagesMerger ReportArisha KhanNo ratings yet

- Commerce: Research Paper Significance of The Indian Gold Loan MarketDocument2 pagesCommerce: Research Paper Significance of The Indian Gold Loan Marketjaymin2303No ratings yet

- UBS Market Internal Dynamic Model - Deep-Dive Models 101 102Document67 pagesUBS Market Internal Dynamic Model - Deep-Dive Models 101 102David YANGNo ratings yet

- MEDINA - Homework 1 (Midterm) No. 8Document3 pagesMEDINA - Homework 1 (Midterm) No. 8Von Andrei MedinaNo ratings yet

- Turmoil in The Financial Institutions ofDocument63 pagesTurmoil in The Financial Institutions ofMohammad Adnan RummanNo ratings yet

- HHH1Document24 pagesHHH1Sitan Kumar SahooNo ratings yet

- Syllabus G11 FABMoneDocument5 pagesSyllabus G11 FABMoneMJ TobiasNo ratings yet

- Basel Committee On Banking Supervision Reforms - Basel IIIDocument1 pageBasel Committee On Banking Supervision Reforms - Basel IIISunlight FoundationNo ratings yet

- Create Your Own Promissory NotesDocument2 pagesCreate Your Own Promissory NotesvalytenNo ratings yet

- Law Relating To Banking May 2015Document5 pagesLaw Relating To Banking May 2015Basilio MaliwangaNo ratings yet

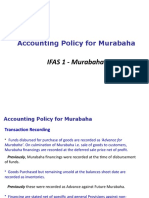

- Murabaha AccountingDocument15 pagesMurabaha AccountingShakeel IqbalNo ratings yet

- Chapter 16 - Corporate GovernanceDocument34 pagesChapter 16 - Corporate Governancekarryl barnuevoNo ratings yet

- The Difference Between FASB and IASB Conceptual Framework 18 AIS 013Document4 pagesThe Difference Between FASB and IASB Conceptual Framework 18 AIS 013Mazharul IslamNo ratings yet

- Derivatives and TranslationDocument3 pagesDerivatives and TranslationVienna Corrine Q. AbucejoNo ratings yet

- Daily Fund Report-PCSO Daily Report PDFDocument2 pagesDaily Fund Report-PCSO Daily Report PDFFranz Thelen Lozano CariñoNo ratings yet

- RDInstallmentReport13 11 2019Document1 pageRDInstallmentReport13 11 2019Archana AwasthiNo ratings yet

- 909Document2 pages909Kashif SiddiquiNo ratings yet

- Prof.: Impact of Mobile Banking (M-Banking) On Banking SectorDocument81 pagesProf.: Impact of Mobile Banking (M-Banking) On Banking Sectorilmuhammad619No ratings yet

- Accounting For Consolidation at Acquisition: 2238 Financial Reporting - 2021/2022 T1Document25 pagesAccounting For Consolidation at Acquisition: 2238 Financial Reporting - 2021/2022 T1Tommaso SpositoNo ratings yet

- PPT On Raghunandan MoneyDocument17 pagesPPT On Raghunandan MoneyAmarkantNo ratings yet

- LEVERAGE Online Problem SheetDocument6 pagesLEVERAGE Online Problem SheetSoumendra RoyNo ratings yet

- An Analysis of Public Sector Banks PerfoDocument14 pagesAn Analysis of Public Sector Banks PerfoMurali Balaji M CNo ratings yet

- Reconciliation TemplateDocument1 pageReconciliation TemplateSyed AmrohviNo ratings yet