Atty. Recuenco - 2022 Chair's Cases in Taxation Law 09022022 (Final)

Atty. Recuenco - 2022 Chair's Cases in Taxation Law 09022022 (Final)

You might also like

- National Budget 2024 - EnglishDocument68 pagesNational Budget 2024 - EnglishAdaderana Online100% (1)

- Contoh Report Latihan IndustriDocument63 pagesContoh Report Latihan IndustriHafizah A. Aziz100% (1)

- Financial Management 16th Edition Chapter 7Document32 pagesFinancial Management 16th Edition Chapter 7drcoolzNo ratings yet

- Assignments in RemediesDocument22 pagesAssignments in RemediesJoAnne Yaptinchay ClaudioNo ratings yet

- I. Courts Case Digests: Tax Updates SeminarDocument9 pagesI. Courts Case Digests: Tax Updates SeminarJennilyn TugelidaNo ratings yet

- Contex vs. CIR, GR No. 151135, 2 July 2004Document8 pagesContex vs. CIR, GR No. 151135, 2 July 2004Christopher ArellanoNo ratings yet

- Tax Digest 20-28Document21 pagesTax Digest 20-28Marc ChicanoNo ratings yet

- Case List: Value Added TaxDocument7 pagesCase List: Value Added TaxAnne Marieline BuenaventuraNo ratings yet

- CONTEX V CIRDocument11 pagesCONTEX V CIRYoo Si JinNo ratings yet

- Facts:: PILMICO-MAURI FOODS CORP. v. CIR,, GR No. 175651, 2016-09-14Document9 pagesFacts:: PILMICO-MAURI FOODS CORP. v. CIR,, GR No. 175651, 2016-09-14Andrew M. AcederaNo ratings yet

- Tax Updates by Atty. LumberaDocument67 pagesTax Updates by Atty. Lumberacupido88No ratings yet

- Taxation Pre-Bar Review 2019 (With Notes)Document15 pagesTaxation Pre-Bar Review 2019 (With Notes)Reynaldo Fajardo YuNo ratings yet

- CASE DOCTRINES - 2020 Jurisprudence Updates (SC and CTA Cases)Document12 pagesCASE DOCTRINES - 2020 Jurisprudence Updates (SC and CTA Cases)Carlota VillaromanNo ratings yet

- XX. CIR vs. Fitness by Design, IncDocument11 pagesXX. CIR vs. Fitness by Design, IncStef OcsalevNo ratings yet

- Tax Law Review Syllabus Part 2Document20 pagesTax Law Review Syllabus Part 2chaynagirlNo ratings yet

- G.R. No. 152609 - Commissioner of Internal Revenue v. American Express International, IncDocument25 pagesG.R. No. 152609 - Commissioner of Internal Revenue v. American Express International, Incjd1.alphaaceNo ratings yet

- Preweek Taxation Law 2017 PDFDocument48 pagesPreweek Taxation Law 2017 PDFAnonymous kiom0L1FqsNo ratings yet

- 49 Insights July 2022Document41 pages49 Insights July 2022Rheneir MoraNo ratings yet

- China Banking Corporation Vs - Cir GR NO. 172509Document12 pagesChina Banking Corporation Vs - Cir GR NO. 172509Lyka Dennese SalazarNo ratings yet

- Allowable DeductionsDocument118 pagesAllowable DeductionsPrincess Hazel GriñoNo ratings yet

- Second Division: Decision DecisionDocument9 pagesSecond Division: Decision DecisionAndrew LastrolloNo ratings yet

- UDocument53 pagesUvmanalo16No ratings yet

- 2023 Omnibus Notes - Part 2 - Taxation Law LawDocument18 pages2023 Omnibus Notes - Part 2 - Taxation Law LawAPRIL BETONIONo ratings yet

- Summary of Significant CTA Decisions (February 2011)Document2 pagesSummary of Significant CTA Decisions (February 2011)ShaneBeriñaImperialNo ratings yet

- G.R. No. 173425Document15 pagesG.R. No. 173425ayleenNo ratings yet

- LIFEBLOODDocument47 pagesLIFEBLOODBREL GOSIMATNo ratings yet

- Tax LawDocument32 pagesTax Lawgilbert213No ratings yet

- Tax AmnestyDocument3 pagesTax Amnestyapi-236234542No ratings yet

- Exception On The Non Delgation of The PowerDocument14 pagesException On The Non Delgation of The PowerRomero MelandriaNo ratings yet

- Taxation Law Updates by Atty. OrtegaDocument21 pagesTaxation Law Updates by Atty. Ortegavillanueva9guapster9100% (1)

- GR No. 173425 Full CaseDocument24 pagesGR No. 173425 Full CaseRene ValentosNo ratings yet

- Case DigestDocument5 pagesCase DigestGabriel Jhick SaliwanNo ratings yet

- Tax Rev VAT CasesDocument196 pagesTax Rev VAT CasesJake MacTavishNo ratings yet

- Fort Bonifacio Development Corporation V CIRDocument26 pagesFort Bonifacio Development Corporation V CIRDean Lozarie0% (1)

- Commissioner of G.R. No. 163345 Internal Revenue,: Chairperson, - Versus - CHICO-NAZARIODocument70 pagesCommissioner of G.R. No. 163345 Internal Revenue,: Chairperson, - Versus - CHICO-NAZARIOmaeNo ratings yet

- Republic Vs GST Philippines, Inc GR # 190870, October 17, 2013Document5 pagesRepublic Vs GST Philippines, Inc GR # 190870, October 17, 2013leslansanganNo ratings yet

- Digest (1986 To 2016)Document151 pagesDigest (1986 To 2016)Jerwin DaveNo ratings yet

- Tax Case DigestDocument11 pagesTax Case DigestPrincess Caroline Nichole IbarraNo ratings yet

- Contex Corp. v. Commissioner of InternalDocument9 pagesContex Corp. v. Commissioner of InternalCamshtNo ratings yet

- 2012 ITAD - BIR - Ruling - No. - 092 1220210505 11 1ig3ujmDocument4 pages2012 ITAD - BIR - Ruling - No. - 092 1220210505 11 1ig3ujmrian.lee.b.tiangcoNo ratings yet

- Bir Ruling (Da - (C-228) 589-09)Document3 pagesBir Ruling (Da - (C-228) 589-09)Stacy Liong BloggerAccountNo ratings yet

- 49 Insights June 2022V2Document24 pages49 Insights June 2022V2Rheneir MoraNo ratings yet

- Tax 2 Syllabus 2020 PDFDocument9 pagesTax 2 Syllabus 2020 PDFroy rebosuraNo ratings yet

- CASE-DIGEST-Pasia-Taxation-Law (Edited)Document10 pagesCASE-DIGEST-Pasia-Taxation-Law (Edited)Pamela Gutierrez PasiaNo ratings yet

- Tax Updates by Atty. LumberaDocument68 pagesTax Updates by Atty. Lumberaavery03No ratings yet

- (G.R. No. 151135. July 2, 2004) Contex Corporation, Petitioner, vs. Hon. Commissioner of Internal Revenue, Respondent. Decision Quisumbing, J.Document5 pages(G.R. No. 151135. July 2, 2004) Contex Corporation, Petitioner, vs. Hon. Commissioner of Internal Revenue, Respondent. Decision Quisumbing, J.Charisa BelistaNo ratings yet

- Updates and Critical Areas in TaxationDocument327 pagesUpdates and Critical Areas in TaxationMark MagnoNo ratings yet

- BPI Vs CIR, 473 SCRA 205, Oct. 17, 2005Document8 pagesBPI Vs CIR, 473 SCRA 205, Oct. 17, 2005katentom-1No ratings yet

- D. Excise TaxDocument8 pagesD. Excise TaxReymar Pan-oyNo ratings yet

- GSTR 9 GSTR 9C 1700889649Document33 pagesGSTR 9 GSTR 9C 1700889649Jayant JoshiNo ratings yet

- Tax Digest VATDocument5 pagesTax Digest VATJose Mari Angelo DionioNo ratings yet

- CHINA BANK v. CIRDocument8 pagesCHINA BANK v. CIRMuhammadIshahaqBinBenjaminNo ratings yet

- Dr. Jeannie P. LimDocument38 pagesDr. Jeannie P. LimSHeena MaRie ErAsmoNo ratings yet

- PWC News Alert 24 December 2020 Cbic Issues Notifications Amending Key ProvisionsDocument4 pagesPWC News Alert 24 December 2020 Cbic Issues Notifications Amending Key Provisionsjsncitycentralmall12No ratings yet

- G.R. No. 193301 Mindanao II v. CIRDocument35 pagesG.R. No. 193301 Mindanao II v. CIRWretz MusniNo ratings yet

- C.2 - Diaz v. Secretary of FinanceDocument15 pagesC.2 - Diaz v. Secretary of FinanceKristine Irish GeronaNo ratings yet

- CIR Vs American ExpressDocument10 pagesCIR Vs American ExpressM A J esty FalconNo ratings yet

- Tmap - Updates (August September 2017) PDFDocument12 pagesTmap - Updates (August September 2017) PDFAko Si Paula MonghitNo ratings yet

- Contex Corporation Vs CirDocument7 pagesContex Corporation Vs Cirdyajee1986No ratings yet

- CIR vs. American Express InternationalDocument30 pagesCIR vs. American Express InternationalMonikkaNo ratings yet

- Mindanao II Geothermal Partnership Vs CIRDocument17 pagesMindanao II Geothermal Partnership Vs CIRLen Sor LuNo ratings yet

- Taxation in Ghana: a Fiscal Policy Tool for Development: 75 Years ResearchFrom EverandTaxation in Ghana: a Fiscal Policy Tool for Development: 75 Years ResearchRating: 5 out of 5 stars5/5 (1)

- Atty. Juanico - Chair's Cases in Criminal LawDocument116 pagesAtty. Juanico - Chair's Cases in Criminal LawErick Paul de VeraNo ratings yet

- Acknowledgement ReceiptDocument1 pageAcknowledgement ReceiptErick Paul de VeraNo ratings yet

- Landbank Intro CocDocument1 pageLandbank Intro CocErick Paul de VeraNo ratings yet

- Transmittal LetterDocument1 pageTransmittal LetterErick Paul de VeraNo ratings yet

- Choose Wisely: A Reflection Paper On The Influence of A GroupDocument2 pagesChoose Wisely: A Reflection Paper On The Influence of A GroupErick Paul de VeraNo ratings yet

- Final Term Paper Sa Ancient.Document10 pagesFinal Term Paper Sa Ancient.Erick Paul de VeraNo ratings yet

- Working Paper 5 - Hong Kong Air Cargo - Final (v4)Document31 pagesWorking Paper 5 - Hong Kong Air Cargo - Final (v4)Aniketh Roy ChoudhuriNo ratings yet

- CA Resale CertificateDocument1 pageCA Resale Certificateali razaNo ratings yet

- INDIA First Insurance Private Limited 80D DEC 2016Document1 pageINDIA First Insurance Private Limited 80D DEC 2016rushikesh28No ratings yet

- G.R. No. 149110 - National Power Corporation v. City of CabanatuanDocument24 pagesG.R. No. 149110 - National Power Corporation v. City of CabanatuanCamille CruzNo ratings yet

- Itc SWOT and PESTLEDocument6 pagesItc SWOT and PESTLESurya SenNo ratings yet

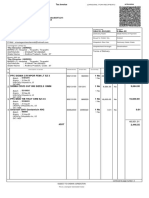

- Inv 2433Document8 pagesInv 2433adarsh pagidiNo ratings yet

- CTA Course Information and RegulationsDocument49 pagesCTA Course Information and Regulationshassan1989No ratings yet

- Jaya Garment Sukses MakmurDocument6 pagesJaya Garment Sukses MakmurgalihpadmasanaNo ratings yet

- UnauditedDocument30 pagesUnauditedSanjay KumarNo ratings yet

- 2023-03-06T00-04 Transaction #5900353713415811-12253031Document1 page2023-03-06T00-04 Transaction #5900353713415811-12253031Melnic IonNo ratings yet

- Dynasty Trusts A Legitimate and Powerful Estate Planning Tool or An Economic Threat To The Realm and To The State of CaliforniaDocument15 pagesDynasty Trusts A Legitimate and Powerful Estate Planning Tool or An Economic Threat To The Realm and To The State of CaliforniaChristopher S. ArmstrongNo ratings yet

- Part Ii PDFDocument212 pagesPart Ii PDFJocagonjcNo ratings yet

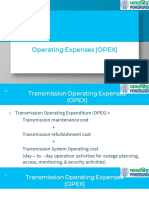

- Operating Expenses (OPEX)Document9 pagesOperating Expenses (OPEX)ASH TVNo ratings yet

- Itr2 2019 PR4Document134 pagesItr2 2019 PR4Dhruv ChitkaraNo ratings yet

- Moc 2Document13 pagesMoc 2pryaparagNo ratings yet

- 2015-01-25 CapTrade Gulf Airlines Subsidies ReportDocument217 pages2015-01-25 CapTrade Gulf Airlines Subsidies ReportcaptradeNo ratings yet

- Future Generali India FinalDocument99 pagesFuture Generali India Finalsuryakantshrotriya67% (3)

- Formalities For Setting Up A Small Business EnterpriseDocument8 pagesFormalities For Setting Up A Small Business EnterpriseMisba Khan0% (1)

- FABM2 Q2 FinalsDocument3 pagesFABM2 Q2 FinalsZeus Malicdem100% (1)

- CIA 3 Company Law FinalDocument7 pagesCIA 3 Company Law FinalANAND GEO 1850508No ratings yet

- The Impact of Capital Structure On The Performance of Microfinance InstitutionsDocument17 pagesThe Impact of Capital Structure On The Performance of Microfinance InstitutionsMuhammadAzharFarooqNo ratings yet

- 4 - Marquez - Hagonoy Market Vs MunicipalityDocument4 pages4 - Marquez - Hagonoy Market Vs Municipalityeverlyyy0% (1)

- Malaysians Seen Curbing Spending As Living Costs SurgeDocument30 pagesMalaysians Seen Curbing Spending As Living Costs SurgeLavanya TheviNo ratings yet

- 18 Tan V Del Rosario 237 SCRA 324 (1994) - DigestDocument15 pages18 Tan V Del Rosario 237 SCRA 324 (1994) - DigestKeith BalbinNo ratings yet

- NIRC Sec 141-151Document9 pagesNIRC Sec 141-151Euxine AlbisNo ratings yet

- BPCL Indemnity BondDocument2 pagesBPCL Indemnity Bondmilind kenjaleNo ratings yet

- CIR v. de La SalleDocument3 pagesCIR v. de La SalleGabriel AdoraNo ratings yet

Download as pdf or txt

You might also like

- National Budget 2024 - EnglishDocument68 pagesNational Budget 2024 - EnglishAdaderana Online100% (1)

- Contoh Report Latihan IndustriDocument63 pagesContoh Report Latihan IndustriHafizah A. Aziz100% (1)

- Financial Management 16th Edition Chapter 7Document32 pagesFinancial Management 16th Edition Chapter 7drcoolzNo ratings yet

- Assignments in RemediesDocument22 pagesAssignments in RemediesJoAnne Yaptinchay ClaudioNo ratings yet

- I. Courts Case Digests: Tax Updates SeminarDocument9 pagesI. Courts Case Digests: Tax Updates SeminarJennilyn TugelidaNo ratings yet

- Contex vs. CIR, GR No. 151135, 2 July 2004Document8 pagesContex vs. CIR, GR No. 151135, 2 July 2004Christopher ArellanoNo ratings yet

- Tax Digest 20-28Document21 pagesTax Digest 20-28Marc ChicanoNo ratings yet

- Case List: Value Added TaxDocument7 pagesCase List: Value Added TaxAnne Marieline BuenaventuraNo ratings yet

- CONTEX V CIRDocument11 pagesCONTEX V CIRYoo Si JinNo ratings yet

- Facts:: PILMICO-MAURI FOODS CORP. v. CIR,, GR No. 175651, 2016-09-14Document9 pagesFacts:: PILMICO-MAURI FOODS CORP. v. CIR,, GR No. 175651, 2016-09-14Andrew M. AcederaNo ratings yet

- Tax Updates by Atty. LumberaDocument67 pagesTax Updates by Atty. Lumberacupido88No ratings yet

- Taxation Pre-Bar Review 2019 (With Notes)Document15 pagesTaxation Pre-Bar Review 2019 (With Notes)Reynaldo Fajardo YuNo ratings yet

- CASE DOCTRINES - 2020 Jurisprudence Updates (SC and CTA Cases)Document12 pagesCASE DOCTRINES - 2020 Jurisprudence Updates (SC and CTA Cases)Carlota VillaromanNo ratings yet

- XX. CIR vs. Fitness by Design, IncDocument11 pagesXX. CIR vs. Fitness by Design, IncStef OcsalevNo ratings yet

- Tax Law Review Syllabus Part 2Document20 pagesTax Law Review Syllabus Part 2chaynagirlNo ratings yet

- G.R. No. 152609 - Commissioner of Internal Revenue v. American Express International, IncDocument25 pagesG.R. No. 152609 - Commissioner of Internal Revenue v. American Express International, Incjd1.alphaaceNo ratings yet

- Preweek Taxation Law 2017 PDFDocument48 pagesPreweek Taxation Law 2017 PDFAnonymous kiom0L1FqsNo ratings yet

- 49 Insights July 2022Document41 pages49 Insights July 2022Rheneir MoraNo ratings yet

- China Banking Corporation Vs - Cir GR NO. 172509Document12 pagesChina Banking Corporation Vs - Cir GR NO. 172509Lyka Dennese SalazarNo ratings yet

- Allowable DeductionsDocument118 pagesAllowable DeductionsPrincess Hazel GriñoNo ratings yet

- Second Division: Decision DecisionDocument9 pagesSecond Division: Decision DecisionAndrew LastrolloNo ratings yet

- UDocument53 pagesUvmanalo16No ratings yet

- 2023 Omnibus Notes - Part 2 - Taxation Law LawDocument18 pages2023 Omnibus Notes - Part 2 - Taxation Law LawAPRIL BETONIONo ratings yet

- Summary of Significant CTA Decisions (February 2011)Document2 pagesSummary of Significant CTA Decisions (February 2011)ShaneBeriñaImperialNo ratings yet

- G.R. No. 173425Document15 pagesG.R. No. 173425ayleenNo ratings yet

- LIFEBLOODDocument47 pagesLIFEBLOODBREL GOSIMATNo ratings yet

- Tax LawDocument32 pagesTax Lawgilbert213No ratings yet

- Tax AmnestyDocument3 pagesTax Amnestyapi-236234542No ratings yet

- Exception On The Non Delgation of The PowerDocument14 pagesException On The Non Delgation of The PowerRomero MelandriaNo ratings yet

- Taxation Law Updates by Atty. OrtegaDocument21 pagesTaxation Law Updates by Atty. Ortegavillanueva9guapster9100% (1)

- GR No. 173425 Full CaseDocument24 pagesGR No. 173425 Full CaseRene ValentosNo ratings yet

- Case DigestDocument5 pagesCase DigestGabriel Jhick SaliwanNo ratings yet

- Tax Rev VAT CasesDocument196 pagesTax Rev VAT CasesJake MacTavishNo ratings yet

- Fort Bonifacio Development Corporation V CIRDocument26 pagesFort Bonifacio Development Corporation V CIRDean Lozarie0% (1)

- Commissioner of G.R. No. 163345 Internal Revenue,: Chairperson, - Versus - CHICO-NAZARIODocument70 pagesCommissioner of G.R. No. 163345 Internal Revenue,: Chairperson, - Versus - CHICO-NAZARIOmaeNo ratings yet

- Republic Vs GST Philippines, Inc GR # 190870, October 17, 2013Document5 pagesRepublic Vs GST Philippines, Inc GR # 190870, October 17, 2013leslansanganNo ratings yet

- Digest (1986 To 2016)Document151 pagesDigest (1986 To 2016)Jerwin DaveNo ratings yet

- Tax Case DigestDocument11 pagesTax Case DigestPrincess Caroline Nichole IbarraNo ratings yet

- Contex Corp. v. Commissioner of InternalDocument9 pagesContex Corp. v. Commissioner of InternalCamshtNo ratings yet

- 2012 ITAD - BIR - Ruling - No. - 092 1220210505 11 1ig3ujmDocument4 pages2012 ITAD - BIR - Ruling - No. - 092 1220210505 11 1ig3ujmrian.lee.b.tiangcoNo ratings yet

- Bir Ruling (Da - (C-228) 589-09)Document3 pagesBir Ruling (Da - (C-228) 589-09)Stacy Liong BloggerAccountNo ratings yet

- 49 Insights June 2022V2Document24 pages49 Insights June 2022V2Rheneir MoraNo ratings yet

- Tax 2 Syllabus 2020 PDFDocument9 pagesTax 2 Syllabus 2020 PDFroy rebosuraNo ratings yet

- CASE-DIGEST-Pasia-Taxation-Law (Edited)Document10 pagesCASE-DIGEST-Pasia-Taxation-Law (Edited)Pamela Gutierrez PasiaNo ratings yet

- Tax Updates by Atty. LumberaDocument68 pagesTax Updates by Atty. Lumberaavery03No ratings yet

- (G.R. No. 151135. July 2, 2004) Contex Corporation, Petitioner, vs. Hon. Commissioner of Internal Revenue, Respondent. Decision Quisumbing, J.Document5 pages(G.R. No. 151135. July 2, 2004) Contex Corporation, Petitioner, vs. Hon. Commissioner of Internal Revenue, Respondent. Decision Quisumbing, J.Charisa BelistaNo ratings yet

- Updates and Critical Areas in TaxationDocument327 pagesUpdates and Critical Areas in TaxationMark MagnoNo ratings yet

- BPI Vs CIR, 473 SCRA 205, Oct. 17, 2005Document8 pagesBPI Vs CIR, 473 SCRA 205, Oct. 17, 2005katentom-1No ratings yet

- D. Excise TaxDocument8 pagesD. Excise TaxReymar Pan-oyNo ratings yet

- GSTR 9 GSTR 9C 1700889649Document33 pagesGSTR 9 GSTR 9C 1700889649Jayant JoshiNo ratings yet

- Tax Digest VATDocument5 pagesTax Digest VATJose Mari Angelo DionioNo ratings yet

- CHINA BANK v. CIRDocument8 pagesCHINA BANK v. CIRMuhammadIshahaqBinBenjaminNo ratings yet

- Dr. Jeannie P. LimDocument38 pagesDr. Jeannie P. LimSHeena MaRie ErAsmoNo ratings yet

- PWC News Alert 24 December 2020 Cbic Issues Notifications Amending Key ProvisionsDocument4 pagesPWC News Alert 24 December 2020 Cbic Issues Notifications Amending Key Provisionsjsncitycentralmall12No ratings yet

- G.R. No. 193301 Mindanao II v. CIRDocument35 pagesG.R. No. 193301 Mindanao II v. CIRWretz MusniNo ratings yet

- C.2 - Diaz v. Secretary of FinanceDocument15 pagesC.2 - Diaz v. Secretary of FinanceKristine Irish GeronaNo ratings yet

- CIR Vs American ExpressDocument10 pagesCIR Vs American ExpressM A J esty FalconNo ratings yet

- Tmap - Updates (August September 2017) PDFDocument12 pagesTmap - Updates (August September 2017) PDFAko Si Paula MonghitNo ratings yet

- Contex Corporation Vs CirDocument7 pagesContex Corporation Vs Cirdyajee1986No ratings yet

- CIR vs. American Express InternationalDocument30 pagesCIR vs. American Express InternationalMonikkaNo ratings yet

- Mindanao II Geothermal Partnership Vs CIRDocument17 pagesMindanao II Geothermal Partnership Vs CIRLen Sor LuNo ratings yet

- Taxation in Ghana: a Fiscal Policy Tool for Development: 75 Years ResearchFrom EverandTaxation in Ghana: a Fiscal Policy Tool for Development: 75 Years ResearchRating: 5 out of 5 stars5/5 (1)

- Atty. Juanico - Chair's Cases in Criminal LawDocument116 pagesAtty. Juanico - Chair's Cases in Criminal LawErick Paul de VeraNo ratings yet

- Acknowledgement ReceiptDocument1 pageAcknowledgement ReceiptErick Paul de VeraNo ratings yet

- Landbank Intro CocDocument1 pageLandbank Intro CocErick Paul de VeraNo ratings yet

- Transmittal LetterDocument1 pageTransmittal LetterErick Paul de VeraNo ratings yet

- Choose Wisely: A Reflection Paper On The Influence of A GroupDocument2 pagesChoose Wisely: A Reflection Paper On The Influence of A GroupErick Paul de VeraNo ratings yet

- Final Term Paper Sa Ancient.Document10 pagesFinal Term Paper Sa Ancient.Erick Paul de VeraNo ratings yet

- Working Paper 5 - Hong Kong Air Cargo - Final (v4)Document31 pagesWorking Paper 5 - Hong Kong Air Cargo - Final (v4)Aniketh Roy ChoudhuriNo ratings yet

- CA Resale CertificateDocument1 pageCA Resale Certificateali razaNo ratings yet

- INDIA First Insurance Private Limited 80D DEC 2016Document1 pageINDIA First Insurance Private Limited 80D DEC 2016rushikesh28No ratings yet

- G.R. No. 149110 - National Power Corporation v. City of CabanatuanDocument24 pagesG.R. No. 149110 - National Power Corporation v. City of CabanatuanCamille CruzNo ratings yet

- Itc SWOT and PESTLEDocument6 pagesItc SWOT and PESTLESurya SenNo ratings yet

- Inv 2433Document8 pagesInv 2433adarsh pagidiNo ratings yet

- CTA Course Information and RegulationsDocument49 pagesCTA Course Information and Regulationshassan1989No ratings yet

- Jaya Garment Sukses MakmurDocument6 pagesJaya Garment Sukses MakmurgalihpadmasanaNo ratings yet

- UnauditedDocument30 pagesUnauditedSanjay KumarNo ratings yet

- 2023-03-06T00-04 Transaction #5900353713415811-12253031Document1 page2023-03-06T00-04 Transaction #5900353713415811-12253031Melnic IonNo ratings yet

- Dynasty Trusts A Legitimate and Powerful Estate Planning Tool or An Economic Threat To The Realm and To The State of CaliforniaDocument15 pagesDynasty Trusts A Legitimate and Powerful Estate Planning Tool or An Economic Threat To The Realm and To The State of CaliforniaChristopher S. ArmstrongNo ratings yet

- Part Ii PDFDocument212 pagesPart Ii PDFJocagonjcNo ratings yet

- Operating Expenses (OPEX)Document9 pagesOperating Expenses (OPEX)ASH TVNo ratings yet

- Itr2 2019 PR4Document134 pagesItr2 2019 PR4Dhruv ChitkaraNo ratings yet

- Moc 2Document13 pagesMoc 2pryaparagNo ratings yet

- 2015-01-25 CapTrade Gulf Airlines Subsidies ReportDocument217 pages2015-01-25 CapTrade Gulf Airlines Subsidies ReportcaptradeNo ratings yet

- Future Generali India FinalDocument99 pagesFuture Generali India Finalsuryakantshrotriya67% (3)

- Formalities For Setting Up A Small Business EnterpriseDocument8 pagesFormalities For Setting Up A Small Business EnterpriseMisba Khan0% (1)

- FABM2 Q2 FinalsDocument3 pagesFABM2 Q2 FinalsZeus Malicdem100% (1)

- CIA 3 Company Law FinalDocument7 pagesCIA 3 Company Law FinalANAND GEO 1850508No ratings yet

- The Impact of Capital Structure On The Performance of Microfinance InstitutionsDocument17 pagesThe Impact of Capital Structure On The Performance of Microfinance InstitutionsMuhammadAzharFarooqNo ratings yet

- 4 - Marquez - Hagonoy Market Vs MunicipalityDocument4 pages4 - Marquez - Hagonoy Market Vs Municipalityeverlyyy0% (1)

- Malaysians Seen Curbing Spending As Living Costs SurgeDocument30 pagesMalaysians Seen Curbing Spending As Living Costs SurgeLavanya TheviNo ratings yet

- 18 Tan V Del Rosario 237 SCRA 324 (1994) - DigestDocument15 pages18 Tan V Del Rosario 237 SCRA 324 (1994) - DigestKeith BalbinNo ratings yet

- NIRC Sec 141-151Document9 pagesNIRC Sec 141-151Euxine AlbisNo ratings yet

- BPCL Indemnity BondDocument2 pagesBPCL Indemnity Bondmilind kenjaleNo ratings yet

- CIR v. de La SalleDocument3 pagesCIR v. de La SalleGabriel AdoraNo ratings yet