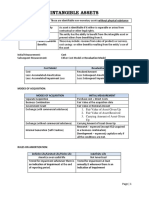

IAS 36 - Summary

IAS 36 - Summary

You might also like

- 2024 Becker CPA Financial (FAR) NotesDocument51 pages2024 Becker CPA Financial (FAR) Notescraigsappletree100% (4)

- Wall Street Mastermind S Investment Banking Technical Interview Cheat SheetDocument2 pagesWall Street Mastermind S Investment Banking Technical Interview Cheat Sheetxandar198No ratings yet

- RAISE Plus WEEKLY PLAN FOR BLENDED LEARNING TleDocument3 pagesRAISE Plus WEEKLY PLAN FOR BLENDED LEARNING TleRomeo jr RamirezNo ratings yet

- The Best Deal GiIlette Could Get - Procter & Gamble's Acquisition of GilletteDocument366 pagesThe Best Deal GiIlette Could Get - Procter & Gamble's Acquisition of Gillettejk kumarNo ratings yet

- Walmart Responsible Sourcing Evaluation Rs / Fcca / GSV: Example ReportDocument16 pagesWalmart Responsible Sourcing Evaluation Rs / Fcca / GSV: Example ReportLia ErizkaNo ratings yet

- Chapter 3 - Tangible Non-Current Asset - Part 1Document29 pagesChapter 3 - Tangible Non-Current Asset - Part 1Nga Phuong NguyenNo ratings yet

- Andp Fiepreciation4p: $ Non-Current AssetsDocument5 pagesAndp Fiepreciation4p: $ Non-Current AssetsShahid MahmudNo ratings yet

- Admin Purposes and To Be Used More Than One PeriodDocument2 pagesAdmin Purposes and To Be Used More Than One PeriodManuel MagadatuNo ratings yet

- U.S. GAAP vs. IFRS: Intangible Assets Other Than Goodwill: Prepared byDocument4 pagesU.S. GAAP vs. IFRS: Intangible Assets Other Than Goodwill: Prepared bySebastian RomoNo ratings yet

- Impairment of Assets (IAS 36)Document16 pagesImpairment of Assets (IAS 36)cynthiama7777No ratings yet

- Summary - IAS 36 by HKDocument3 pagesSummary - IAS 36 by HKaimanraees10No ratings yet

- Topic 3 - IAS 36Document15 pagesTopic 3 - IAS 36antran.31201025723No ratings yet

- CHP 5 Concept and Accounting of DepreciationDocument6 pagesCHP 5 Concept and Accounting of DepreciationAmit KumarNo ratings yet

- Business Strategy Using Financial Statements: Asset Analysis-Long-Lived Asset and DepreciationDocument41 pagesBusiness Strategy Using Financial Statements: Asset Analysis-Long-Lived Asset and DepreciationMeena KhattakNo ratings yet

- FAR Cheat SheetDocument6 pagesFAR Cheat Sheetngan.foldersNo ratings yet

- Chapter 28: Depletion Pfrs/Ifrs 6: Financial Reporting For The Exploration and Evaluation of Mineral ResourcesDocument3 pagesChapter 28: Depletion Pfrs/Ifrs 6: Financial Reporting For The Exploration and Evaluation of Mineral ResourcesKaryl FailmaNo ratings yet

- LU 4 - IAS 40 Investment Property SummaryDocument3 pagesLU 4 - IAS 40 Investment Property Summarycz82h7z84tNo ratings yet

- AFM Chapter 7 Depreciation MergeDocument99 pagesAFM Chapter 7 Depreciation MergeSarah Shahnaz IlmaNo ratings yet

- This Study Resource Was: (Individual Asset)Document6 pagesThis Study Resource Was: (Individual Asset)Febby Grace SabinoNo ratings yet

- IMPAIRMENTS WHITE PAPER v2 PDFDocument33 pagesIMPAIRMENTS WHITE PAPER v2 PDFSrinibasNo ratings yet

- Impairments White PaperDocument35 pagesImpairments White PaperRam PillaiNo ratings yet

- SUMMARY - Intangible AssetsDocument12 pagesSUMMARY - Intangible AssetsKRESLEY LAUDEEN ORTEGANo ratings yet

- Modes of Acquisition: Refer To The FV Hierarchy in Impairment of AssetsDocument4 pagesModes of Acquisition: Refer To The FV Hierarchy in Impairment of AssetsKaryl FailmaNo ratings yet

- Property Plant Equipment PART 1 FINALDocument22 pagesProperty Plant Equipment PART 1 FINALJames R JunioNo ratings yet

- Zrive IB 1Q23 Intro To Valuation Methods Up2Document9 pagesZrive IB 1Q23 Intro To Valuation Methods Up2Luis Soldevilla MorenoNo ratings yet

- FAR 12 - Intangible AssetsDocument5 pagesFAR 12 - Intangible Assetsmrsjeon0501No ratings yet

- Learning Objectives: Impairment of AssetsDocument14 pagesLearning Objectives: Impairment of AssetsBích TrâmNo ratings yet

- 05 Ias 36Document4 pages05 Ias 36Irtiza AbbasNo ratings yet

- Corporate Reporting - MFRS136 - Impairment of Assets - Dayana MasturaDocument26 pagesCorporate Reporting - MFRS136 - Impairment of Assets - Dayana MasturaDayana MasturaNo ratings yet

- AAFR by Sir Nasir Abbas - RemovedDocument559 pagesAAFR by Sir Nasir Abbas - RemovedAbdul BalochNo ratings yet

- Gross Profit Net Profit/ EBIT: Return On Capital EmployesDocument9 pagesGross Profit Net Profit/ EBIT: Return On Capital Employesshekhar371No ratings yet

- 5600/020 Definitions: Eff. From: 01/01/2010 Eff. Until: Topic: Property, Plant & EquipmentDocument2 pages5600/020 Definitions: Eff. From: 01/01/2010 Eff. Until: Topic: Property, Plant & EquipmentBilal ShafiqueNo ratings yet

- Approaches of Valuation - CostDocument7 pagesApproaches of Valuation - CostSanjay PatelNo ratings yet

- Income Taxation Chapter 9Document11 pagesIncome Taxation Chapter 9Kim Patrice NavarraNo ratings yet

- Nas 16Document33 pagesNas 16bhattag283No ratings yet

- Scope: Financial Accounting and Reporting - Property, Plant and Equipment Property, Plant and EquipmentDocument12 pagesScope: Financial Accounting and Reporting - Property, Plant and Equipment Property, Plant and EquipmentEngel QuimsonNo ratings yet

- Handout AP 2301Document13 pagesHandout AP 2301Dyosa MeNo ratings yet

- IND AS 38 - INTANGIBLE ASSETS RevisionDocument10 pagesIND AS 38 - INTANGIBLE ASSETS Revisionnimisha vermaNo ratings yet

- Impairment of Non Current Assets - Ias 36: - Impairment Is A Reduction To The Recoverable Amount of An Asset or ADocument89 pagesImpairment of Non Current Assets - Ias 36: - Impairment Is A Reduction To The Recoverable Amount of An Asset or ATram NguyenNo ratings yet

- Ias 38 - TSVHDocument37 pagesIas 38 - TSVHHồ Đan ThụcNo ratings yet

- FAR210 MFRS116 PPE - Oct23Document28 pagesFAR210 MFRS116 PPE - Oct23Nur Alya DamiaNo ratings yet

- IAS 36 Impairment of Assets: ScopeDocument2 pagesIAS 36 Impairment of Assets: ScopeKazi MahbubNo ratings yet

- Corporate Actions PresentationDocument12 pagesCorporate Actions PresentationSheetal LaddhaNo ratings yet

- Lecture Note of Unit 4: Turnover Turnover TurnoverDocument2 pagesLecture Note of Unit 4: Turnover Turnover Turnoverthinh macNo ratings yet

- Dwnload Full Taxation of Business Entities 2018 Edition 9th Edition Spilker Solutions Manual PDFDocument31 pagesDwnload Full Taxation of Business Entities 2018 Edition 9th Edition Spilker Solutions Manual PDFquemefuloathableilljzf100% (16)

- Chapter 03Document2 pagesChapter 03Patrick Kyle AgraviadorNo ratings yet

- Abusama Impairment of AssetsDocument1 pageAbusama Impairment of AssetsGarp BarrocaNo ratings yet

- Valuation of Shares / Goodwill: Part A: TheoryDocument14 pagesValuation of Shares / Goodwill: Part A: TheoryYatrik DaveNo ratings yet

- Fin544 - Mind Mapping (Chapter 2)Document2 pagesFin544 - Mind Mapping (Chapter 2)nur fatihahNo ratings yet

- 1 Intangible Assets PDFDocument56 pages1 Intangible Assets PDFCatherine RiveraNo ratings yet

- Property, Plant, and Equipment and Intangible Assets: Utilization and ImpairmentDocument53 pagesProperty, Plant, and Equipment and Intangible Assets: Utilization and ImpairmentSara LimNo ratings yet

- Intangible AssetDocument2 pagesIntangible Asset202201538No ratings yet

- Dwnload Full Taxation of Business Entities 5th Edition Spilker Solutions Manual PDFDocument22 pagesDwnload Full Taxation of Business Entities 5th Edition Spilker Solutions Manual PDFquemefuloathableilljzf100% (14)

- Full Download Taxation of Business Entities 5th Edition Spilker Solutions ManualDocument35 pagesFull Download Taxation of Business Entities 5th Edition Spilker Solutions Manualmateorivu100% (39)

- PPE Presentation - 11.22.2020Document21 pagesPPE Presentation - 11.22.2020Makoy BixenmanNo ratings yet

- FAR 007 Summary Notes - Intangible AssetsDocument5 pagesFAR 007 Summary Notes - Intangible AssetsMarynelle Labrador SevillaNo ratings yet

- Balance Sheet: Prepared OnDocument3 pagesBalance Sheet: Prepared OnfiohdiohhodoNo ratings yet

- How Formula Expressed Meaning: Current Assets Current LiabilitiesDocument5 pagesHow Formula Expressed Meaning: Current Assets Current LiabilitiesHemraj VermaNo ratings yet

- Chapter 17 IAS 36 Impairment of AssetsDocument13 pagesChapter 17 IAS 36 Impairment of AssetsKelvin Chu JYNo ratings yet

- Chap09 - Student (Revised)Document36 pagesChap09 - Student (Revised)Fung Yat Kit KeithNo ratings yet

- Fair Value for Financial Reporting: Meeting the New FASB RequirementsFrom EverandFair Value for Financial Reporting: Meeting the New FASB RequirementsNo ratings yet

- Unit 10Document3 pagesUnit 10Husam Nusair100% (1)

- LENCIONI Weekly Tactical Meeting TemplateDocument2 pagesLENCIONI Weekly Tactical Meeting Templatedaniela.schittengruberNo ratings yet

- NMIF T301 Sand Bitumen Mix Laying and Annular - Bottom Plates Installation - Rev 01Document11 pagesNMIF T301 Sand Bitumen Mix Laying and Annular - Bottom Plates Installation - Rev 01Jennifer JavierNo ratings yet

- PB Xii Economics 2023-24Document7 pagesPB Xii Economics 2023-24nhag720207No ratings yet

- Contract of UsufructDocument3 pagesContract of UsufructPatrick Angelo GutierrezNo ratings yet

- Civil Law Bar Questions 06-14Document50 pagesCivil Law Bar Questions 06-14CarmeloNo ratings yet

- MCQ Quantitative TechniquesDocument14 pagesMCQ Quantitative Techniquesajeet sharmaNo ratings yet

- SITXHRM002 Roster Staff Student Guide V1.1 1 .Docx 1 PDFDocument91 pagesSITXHRM002 Roster Staff Student Guide V1.1 1 .Docx 1 PDFNicolas EscobarNo ratings yet

- Sop PurchasingDocument5 pagesSop PurchasingShivam GaurNo ratings yet

- ABSOLUTE AGREEMENT OF SALE DR Kaleem 03-02-2014Document11 pagesABSOLUTE AGREEMENT OF SALE DR Kaleem 03-02-2014new india associatesNo ratings yet

- MTH601-MidTerm-solved MCQ Mega File 2Document14 pagesMTH601-MidTerm-solved MCQ Mega File 2kiranNo ratings yet

- Group 3 MKT330Document28 pagesGroup 3 MKT330MD. MOWDUD HASAN LALON 1632830630No ratings yet

- Cost and Management Accounting Antique and Collectibles ShopDocument6 pagesCost and Management Accounting Antique and Collectibles ShopNaman GuptaNo ratings yet

- Bharti Axa Life Monthly Income Plan +: Toll Free Helpline: 1800-22-6465 WWW - Bluechipindia.co - inDocument6 pagesBharti Axa Life Monthly Income Plan +: Toll Free Helpline: 1800-22-6465 WWW - Bluechipindia.co - inOnline YogeshNo ratings yet

- Theory of Consumption Andtheory of ProductionDocument6 pagesTheory of Consumption Andtheory of ProductionMarinale LabroNo ratings yet

- Dynamic Trader Daily Report: Today's LessonDocument3 pagesDynamic Trader Daily Report: Today's LessonBudi MulyonoNo ratings yet

- Sigmazinc™ 109 HS: Product Data SheetDocument5 pagesSigmazinc™ 109 HS: Product Data SheetinnovativekarthiNo ratings yet

- Business Pitch II - Pitch Deck: LABU 2060 L11BDocument26 pagesBusiness Pitch II - Pitch Deck: LABU 2060 L11BMd. Safiqul IslamNo ratings yet

- Research 1Document1 pageResearch 1api-297189035No ratings yet

- Unit 2 Topic 1 TemplateDocument5 pagesUnit 2 Topic 1 TemplateDev KhatriNo ratings yet

- A Friedman Doctrine-The Social Responsibility of Business Is To Increase Its ProfitsDocument7 pagesA Friedman Doctrine-The Social Responsibility of Business Is To Increase Its ProfitsVarun S UNo ratings yet

- Yokohama Tire Vs Yokohama EUDocument3 pagesYokohama Tire Vs Yokohama EUJohnday MartirezNo ratings yet

- DB Managment Ch4Document15 pagesDB Managment Ch4Juan Manuel Garcia NoguesNo ratings yet

- How We Are Getting Digital????????: Presented By: Dr. Ruchi Jain GargDocument59 pagesHow We Are Getting Digital????????: Presented By: Dr. Ruchi Jain GargDrRuchi GargNo ratings yet

- What To Read To Understand The History of Western Capitalism The EconomistDocument7 pagesWhat To Read To Understand The History of Western Capitalism The EconomistDavid Farias PizarroNo ratings yet

- DLL G6 Q4 WEEK 5 ALL SUBJECTS Mam Inkay PeraltaDocument64 pagesDLL G6 Q4 WEEK 5 ALL SUBJECTS Mam Inkay Peraltaedelberto100% (1)

- Afar 2 Module CH 13Document12 pagesAfar 2 Module CH 13Joyce Anne Mananquil100% (1)

- #169 City Lumber vs. Domingo DigestDocument2 pages#169 City Lumber vs. Domingo DigestNisa Sango OpallaNo ratings yet

Download as pdf or txt

You might also like

- 2024 Becker CPA Financial (FAR) NotesDocument51 pages2024 Becker CPA Financial (FAR) Notescraigsappletree100% (4)

- Wall Street Mastermind S Investment Banking Technical Interview Cheat SheetDocument2 pagesWall Street Mastermind S Investment Banking Technical Interview Cheat Sheetxandar198No ratings yet

- RAISE Plus WEEKLY PLAN FOR BLENDED LEARNING TleDocument3 pagesRAISE Plus WEEKLY PLAN FOR BLENDED LEARNING TleRomeo jr RamirezNo ratings yet

- The Best Deal GiIlette Could Get - Procter & Gamble's Acquisition of GilletteDocument366 pagesThe Best Deal GiIlette Could Get - Procter & Gamble's Acquisition of Gillettejk kumarNo ratings yet

- Walmart Responsible Sourcing Evaluation Rs / Fcca / GSV: Example ReportDocument16 pagesWalmart Responsible Sourcing Evaluation Rs / Fcca / GSV: Example ReportLia ErizkaNo ratings yet

- Chapter 3 - Tangible Non-Current Asset - Part 1Document29 pagesChapter 3 - Tangible Non-Current Asset - Part 1Nga Phuong NguyenNo ratings yet

- Andp Fiepreciation4p: $ Non-Current AssetsDocument5 pagesAndp Fiepreciation4p: $ Non-Current AssetsShahid MahmudNo ratings yet

- Admin Purposes and To Be Used More Than One PeriodDocument2 pagesAdmin Purposes and To Be Used More Than One PeriodManuel MagadatuNo ratings yet

- U.S. GAAP vs. IFRS: Intangible Assets Other Than Goodwill: Prepared byDocument4 pagesU.S. GAAP vs. IFRS: Intangible Assets Other Than Goodwill: Prepared bySebastian RomoNo ratings yet

- Impairment of Assets (IAS 36)Document16 pagesImpairment of Assets (IAS 36)cynthiama7777No ratings yet

- Summary - IAS 36 by HKDocument3 pagesSummary - IAS 36 by HKaimanraees10No ratings yet

- Topic 3 - IAS 36Document15 pagesTopic 3 - IAS 36antran.31201025723No ratings yet

- CHP 5 Concept and Accounting of DepreciationDocument6 pagesCHP 5 Concept and Accounting of DepreciationAmit KumarNo ratings yet

- Business Strategy Using Financial Statements: Asset Analysis-Long-Lived Asset and DepreciationDocument41 pagesBusiness Strategy Using Financial Statements: Asset Analysis-Long-Lived Asset and DepreciationMeena KhattakNo ratings yet

- FAR Cheat SheetDocument6 pagesFAR Cheat Sheetngan.foldersNo ratings yet

- Chapter 28: Depletion Pfrs/Ifrs 6: Financial Reporting For The Exploration and Evaluation of Mineral ResourcesDocument3 pagesChapter 28: Depletion Pfrs/Ifrs 6: Financial Reporting For The Exploration and Evaluation of Mineral ResourcesKaryl FailmaNo ratings yet

- LU 4 - IAS 40 Investment Property SummaryDocument3 pagesLU 4 - IAS 40 Investment Property Summarycz82h7z84tNo ratings yet

- AFM Chapter 7 Depreciation MergeDocument99 pagesAFM Chapter 7 Depreciation MergeSarah Shahnaz IlmaNo ratings yet

- This Study Resource Was: (Individual Asset)Document6 pagesThis Study Resource Was: (Individual Asset)Febby Grace SabinoNo ratings yet

- IMPAIRMENTS WHITE PAPER v2 PDFDocument33 pagesIMPAIRMENTS WHITE PAPER v2 PDFSrinibasNo ratings yet

- Impairments White PaperDocument35 pagesImpairments White PaperRam PillaiNo ratings yet

- SUMMARY - Intangible AssetsDocument12 pagesSUMMARY - Intangible AssetsKRESLEY LAUDEEN ORTEGANo ratings yet

- Modes of Acquisition: Refer To The FV Hierarchy in Impairment of AssetsDocument4 pagesModes of Acquisition: Refer To The FV Hierarchy in Impairment of AssetsKaryl FailmaNo ratings yet

- Property Plant Equipment PART 1 FINALDocument22 pagesProperty Plant Equipment PART 1 FINALJames R JunioNo ratings yet

- Zrive IB 1Q23 Intro To Valuation Methods Up2Document9 pagesZrive IB 1Q23 Intro To Valuation Methods Up2Luis Soldevilla MorenoNo ratings yet

- FAR 12 - Intangible AssetsDocument5 pagesFAR 12 - Intangible Assetsmrsjeon0501No ratings yet

- Learning Objectives: Impairment of AssetsDocument14 pagesLearning Objectives: Impairment of AssetsBích TrâmNo ratings yet

- 05 Ias 36Document4 pages05 Ias 36Irtiza AbbasNo ratings yet

- Corporate Reporting - MFRS136 - Impairment of Assets - Dayana MasturaDocument26 pagesCorporate Reporting - MFRS136 - Impairment of Assets - Dayana MasturaDayana MasturaNo ratings yet

- AAFR by Sir Nasir Abbas - RemovedDocument559 pagesAAFR by Sir Nasir Abbas - RemovedAbdul BalochNo ratings yet

- Gross Profit Net Profit/ EBIT: Return On Capital EmployesDocument9 pagesGross Profit Net Profit/ EBIT: Return On Capital Employesshekhar371No ratings yet

- 5600/020 Definitions: Eff. From: 01/01/2010 Eff. Until: Topic: Property, Plant & EquipmentDocument2 pages5600/020 Definitions: Eff. From: 01/01/2010 Eff. Until: Topic: Property, Plant & EquipmentBilal ShafiqueNo ratings yet

- Approaches of Valuation - CostDocument7 pagesApproaches of Valuation - CostSanjay PatelNo ratings yet

- Income Taxation Chapter 9Document11 pagesIncome Taxation Chapter 9Kim Patrice NavarraNo ratings yet

- Nas 16Document33 pagesNas 16bhattag283No ratings yet

- Scope: Financial Accounting and Reporting - Property, Plant and Equipment Property, Plant and EquipmentDocument12 pagesScope: Financial Accounting and Reporting - Property, Plant and Equipment Property, Plant and EquipmentEngel QuimsonNo ratings yet

- Handout AP 2301Document13 pagesHandout AP 2301Dyosa MeNo ratings yet

- IND AS 38 - INTANGIBLE ASSETS RevisionDocument10 pagesIND AS 38 - INTANGIBLE ASSETS Revisionnimisha vermaNo ratings yet

- Impairment of Non Current Assets - Ias 36: - Impairment Is A Reduction To The Recoverable Amount of An Asset or ADocument89 pagesImpairment of Non Current Assets - Ias 36: - Impairment Is A Reduction To The Recoverable Amount of An Asset or ATram NguyenNo ratings yet

- Ias 38 - TSVHDocument37 pagesIas 38 - TSVHHồ Đan ThụcNo ratings yet

- FAR210 MFRS116 PPE - Oct23Document28 pagesFAR210 MFRS116 PPE - Oct23Nur Alya DamiaNo ratings yet

- IAS 36 Impairment of Assets: ScopeDocument2 pagesIAS 36 Impairment of Assets: ScopeKazi MahbubNo ratings yet

- Corporate Actions PresentationDocument12 pagesCorporate Actions PresentationSheetal LaddhaNo ratings yet

- Lecture Note of Unit 4: Turnover Turnover TurnoverDocument2 pagesLecture Note of Unit 4: Turnover Turnover Turnoverthinh macNo ratings yet

- Dwnload Full Taxation of Business Entities 2018 Edition 9th Edition Spilker Solutions Manual PDFDocument31 pagesDwnload Full Taxation of Business Entities 2018 Edition 9th Edition Spilker Solutions Manual PDFquemefuloathableilljzf100% (16)

- Chapter 03Document2 pagesChapter 03Patrick Kyle AgraviadorNo ratings yet

- Abusama Impairment of AssetsDocument1 pageAbusama Impairment of AssetsGarp BarrocaNo ratings yet

- Valuation of Shares / Goodwill: Part A: TheoryDocument14 pagesValuation of Shares / Goodwill: Part A: TheoryYatrik DaveNo ratings yet

- Fin544 - Mind Mapping (Chapter 2)Document2 pagesFin544 - Mind Mapping (Chapter 2)nur fatihahNo ratings yet

- 1 Intangible Assets PDFDocument56 pages1 Intangible Assets PDFCatherine RiveraNo ratings yet

- Property, Plant, and Equipment and Intangible Assets: Utilization and ImpairmentDocument53 pagesProperty, Plant, and Equipment and Intangible Assets: Utilization and ImpairmentSara LimNo ratings yet

- Intangible AssetDocument2 pagesIntangible Asset202201538No ratings yet

- Dwnload Full Taxation of Business Entities 5th Edition Spilker Solutions Manual PDFDocument22 pagesDwnload Full Taxation of Business Entities 5th Edition Spilker Solutions Manual PDFquemefuloathableilljzf100% (14)

- Full Download Taxation of Business Entities 5th Edition Spilker Solutions ManualDocument35 pagesFull Download Taxation of Business Entities 5th Edition Spilker Solutions Manualmateorivu100% (39)

- PPE Presentation - 11.22.2020Document21 pagesPPE Presentation - 11.22.2020Makoy BixenmanNo ratings yet

- FAR 007 Summary Notes - Intangible AssetsDocument5 pagesFAR 007 Summary Notes - Intangible AssetsMarynelle Labrador SevillaNo ratings yet

- Balance Sheet: Prepared OnDocument3 pagesBalance Sheet: Prepared OnfiohdiohhodoNo ratings yet

- How Formula Expressed Meaning: Current Assets Current LiabilitiesDocument5 pagesHow Formula Expressed Meaning: Current Assets Current LiabilitiesHemraj VermaNo ratings yet

- Chapter 17 IAS 36 Impairment of AssetsDocument13 pagesChapter 17 IAS 36 Impairment of AssetsKelvin Chu JYNo ratings yet

- Chap09 - Student (Revised)Document36 pagesChap09 - Student (Revised)Fung Yat Kit KeithNo ratings yet

- Fair Value for Financial Reporting: Meeting the New FASB RequirementsFrom EverandFair Value for Financial Reporting: Meeting the New FASB RequirementsNo ratings yet

- Unit 10Document3 pagesUnit 10Husam Nusair100% (1)

- LENCIONI Weekly Tactical Meeting TemplateDocument2 pagesLENCIONI Weekly Tactical Meeting Templatedaniela.schittengruberNo ratings yet

- NMIF T301 Sand Bitumen Mix Laying and Annular - Bottom Plates Installation - Rev 01Document11 pagesNMIF T301 Sand Bitumen Mix Laying and Annular - Bottom Plates Installation - Rev 01Jennifer JavierNo ratings yet

- PB Xii Economics 2023-24Document7 pagesPB Xii Economics 2023-24nhag720207No ratings yet

- Contract of UsufructDocument3 pagesContract of UsufructPatrick Angelo GutierrezNo ratings yet

- Civil Law Bar Questions 06-14Document50 pagesCivil Law Bar Questions 06-14CarmeloNo ratings yet

- MCQ Quantitative TechniquesDocument14 pagesMCQ Quantitative Techniquesajeet sharmaNo ratings yet

- SITXHRM002 Roster Staff Student Guide V1.1 1 .Docx 1 PDFDocument91 pagesSITXHRM002 Roster Staff Student Guide V1.1 1 .Docx 1 PDFNicolas EscobarNo ratings yet

- Sop PurchasingDocument5 pagesSop PurchasingShivam GaurNo ratings yet

- ABSOLUTE AGREEMENT OF SALE DR Kaleem 03-02-2014Document11 pagesABSOLUTE AGREEMENT OF SALE DR Kaleem 03-02-2014new india associatesNo ratings yet

- MTH601-MidTerm-solved MCQ Mega File 2Document14 pagesMTH601-MidTerm-solved MCQ Mega File 2kiranNo ratings yet

- Group 3 MKT330Document28 pagesGroup 3 MKT330MD. MOWDUD HASAN LALON 1632830630No ratings yet

- Cost and Management Accounting Antique and Collectibles ShopDocument6 pagesCost and Management Accounting Antique and Collectibles ShopNaman GuptaNo ratings yet

- Bharti Axa Life Monthly Income Plan +: Toll Free Helpline: 1800-22-6465 WWW - Bluechipindia.co - inDocument6 pagesBharti Axa Life Monthly Income Plan +: Toll Free Helpline: 1800-22-6465 WWW - Bluechipindia.co - inOnline YogeshNo ratings yet

- Theory of Consumption Andtheory of ProductionDocument6 pagesTheory of Consumption Andtheory of ProductionMarinale LabroNo ratings yet

- Dynamic Trader Daily Report: Today's LessonDocument3 pagesDynamic Trader Daily Report: Today's LessonBudi MulyonoNo ratings yet

- Sigmazinc™ 109 HS: Product Data SheetDocument5 pagesSigmazinc™ 109 HS: Product Data SheetinnovativekarthiNo ratings yet

- Business Pitch II - Pitch Deck: LABU 2060 L11BDocument26 pagesBusiness Pitch II - Pitch Deck: LABU 2060 L11BMd. Safiqul IslamNo ratings yet

- Research 1Document1 pageResearch 1api-297189035No ratings yet

- Unit 2 Topic 1 TemplateDocument5 pagesUnit 2 Topic 1 TemplateDev KhatriNo ratings yet

- A Friedman Doctrine-The Social Responsibility of Business Is To Increase Its ProfitsDocument7 pagesA Friedman Doctrine-The Social Responsibility of Business Is To Increase Its ProfitsVarun S UNo ratings yet

- Yokohama Tire Vs Yokohama EUDocument3 pagesYokohama Tire Vs Yokohama EUJohnday MartirezNo ratings yet

- DB Managment Ch4Document15 pagesDB Managment Ch4Juan Manuel Garcia NoguesNo ratings yet

- How We Are Getting Digital????????: Presented By: Dr. Ruchi Jain GargDocument59 pagesHow We Are Getting Digital????????: Presented By: Dr. Ruchi Jain GargDrRuchi GargNo ratings yet

- What To Read To Understand The History of Western Capitalism The EconomistDocument7 pagesWhat To Read To Understand The History of Western Capitalism The EconomistDavid Farias PizarroNo ratings yet

- DLL G6 Q4 WEEK 5 ALL SUBJECTS Mam Inkay PeraltaDocument64 pagesDLL G6 Q4 WEEK 5 ALL SUBJECTS Mam Inkay Peraltaedelberto100% (1)

- Afar 2 Module CH 13Document12 pagesAfar 2 Module CH 13Joyce Anne Mananquil100% (1)

- #169 City Lumber vs. Domingo DigestDocument2 pages#169 City Lumber vs. Domingo DigestNisa Sango OpallaNo ratings yet