RIL Company Analysis - MARICO

RIL Company Analysis - MARICO

You might also like

- Textbook Promoting Successful Transition To Adulthood For Students With Disabilities 1St Edition Robert L Morgan Ebook All Chapter PDFDocument53 pagesTextbook Promoting Successful Transition To Adulthood For Students With Disabilities 1St Edition Robert L Morgan Ebook All Chapter PDFvicki.vaught30780% (5)

- Boeing 737 Nef Program and Procedures Manual Rev 4Document36 pagesBoeing 737 Nef Program and Procedures Manual Rev 4Adrian100% (2)

- Chapter 5 - Vision and Mission AnalysisDocument40 pagesChapter 5 - Vision and Mission AnalysisNero Sha100% (5)

- NitinolDocument20 pagesNitinolTamara PricilaNo ratings yet

- Sequence of Operation of FahuDocument1 pageSequence of Operation of FahuahmedNo ratings yet

- Measurement of Line Impedances and Mutual Coupling of Parallel LinesDocument8 pagesMeasurement of Line Impedances and Mutual Coupling of Parallel LinesKhandai SeenananNo ratings yet

- Final Report of SIPDocument56 pagesFinal Report of SIPRahul Parashar100% (1)

- FMCG May 2023Document32 pagesFMCG May 2023Sangeethasruthi SNo ratings yet

- FMCG - August - 2023Document32 pagesFMCG - August - 2023Barshali DasNo ratings yet

- FMCG December 2023Document32 pagesFMCG December 2023pimewip969No ratings yet

- Almost-There 2 PDFDocument32 pagesAlmost-There 2 PDFPaul StriderNo ratings yet

- CFA Institute Research Challenge Hosted in CFA Society Bangladesh Team Name: Last In, First OutDocument32 pagesCFA Institute Research Challenge Hosted in CFA Society Bangladesh Team Name: Last In, First OutPaul StriderNo ratings yet

- Almost There PDFDocument32 pagesAlmost There PDFPaul StriderNo ratings yet

- Vishruti Khandelwal PGDM - 1. 2019-1705-0001-0033Document17 pagesVishruti Khandelwal PGDM - 1. 2019-1705-0001-0033Vishruti KhandelwalNo ratings yet

- FMCG IbefDocument32 pagesFMCG IbefjeetNo ratings yet

- Bajaj-Consumer-Care-Limited 827 CompanyUpdate PDFDocument11 pagesBajaj-Consumer-Care-Limited 827 CompanyUpdate PDFhamsNo ratings yet

- Term Paper On Marico Bangladesh Ltd.Document35 pagesTerm Paper On Marico Bangladesh Ltd.simeen srabaniNo ratings yet

- FMCG - Sector ReportDocument10 pagesFMCG - Sector ReportRajendra BhoirNo ratings yet

- Dabur India LTD.: Equity Research ReportDocument40 pagesDabur India LTD.: Equity Research ReportshakeDNo ratings yet

- Marketing Challenges On Siri Food ProductsDocument81 pagesMarketing Challenges On Siri Food ProductsShrivatsa JoshiNo ratings yet

- Castrol India LTD: November 06, 2018Document17 pagesCastrol India LTD: November 06, 2018Yash AgarwalNo ratings yet

- Nestle Equity Research ReportDocument7 pagesNestle Equity Research Reportyadhu krishnaNo ratings yet

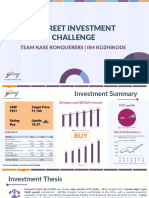

- R-Street Investment Challenge: Team Kase Konquerers - Iim KozhikodeDocument12 pagesR-Street Investment Challenge: Team Kase Konquerers - Iim KozhikodeApoorva JainNo ratings yet

- Group 3 - Praj IndustriesDocument9 pagesGroup 3 - Praj IndustriesAayushi ChandwaniNo ratings yet

- B3 - Equity Research ReportDocument9 pagesB3 - Equity Research ReportAayushi ChandwaniNo ratings yet

- Britannia Industries LimitedDocument8 pagesBritannia Industries Limitedvedantpatnaik.privNo ratings yet

- Pidilite CompanyDocument6 pagesPidilite Companykhalsa.taranjitNo ratings yet

- Company Analysis - Britannia Industries Ltd. (Jayraj Agrawal)Document3 pagesCompany Analysis - Britannia Industries Ltd. (Jayraj Agrawal)JAYRAJ AGRAWALNo ratings yet

- Sanitary MKT ReportDocument38 pagesSanitary MKT ReportsanjnuNo ratings yet

- Research Report - Cupid LTDDocument8 pagesResearch Report - Cupid LTDNeetu LatwalNo ratings yet

- DhairyaShah 26 DDocument22 pagesDhairyaShah 26 DDHAIRYA09No ratings yet

- IDirect Zomato IPOReviewDocument13 pagesIDirect Zomato IPOReviewSnehashree SahooNo ratings yet

- Edible Oils in VietnamDocument10 pagesEdible Oils in VietnamNguyen Ly Thanh LuongNo ratings yet

- IDirect GSKConsumer ICDocument26 pagesIDirect GSKConsumer ICChaitanya JagarlapudiNo ratings yet

- Prudential - Digital Marketing ProposalDocument39 pagesPrudential - Digital Marketing ProposalUYÊN NGUYỄN THỊ PHƯƠNGNo ratings yet

- The Scope For GI Based Branding in Agricultural Products An OverviewDocument2 pagesThe Scope For GI Based Branding in Agricultural Products An OverviewEditor IJTSRDNo ratings yet

- Saurabh Ghare - To Study Fundamental Analysis of Fast-Moving Consumer Goods Sector and Comparitive Study of HUL ITCDocument46 pagesSaurabh Ghare - To Study Fundamental Analysis of Fast-Moving Consumer Goods Sector and Comparitive Study of HUL ITCKRITARTH SINGHNo ratings yet

- Bajaj AllianzDocument99 pagesBajaj AllianzYASH PRAJAPATINo ratings yet

- Marketing Management: (Document Subtitle)Document21 pagesMarketing Management: (Document Subtitle)aseni herathNo ratings yet

- MOSL AGIC - Highlights From The ConferenceDocument74 pagesMOSL AGIC - Highlights From The ConferenceqwertixNo ratings yet

- BCG Analysis-Report: Prepared By: Sanya Nauharia Sankara Narayanan Nikhil Jha Jay Saxena Jayant Choudhary Manju DhindwalDocument9 pagesBCG Analysis-Report: Prepared By: Sanya Nauharia Sankara Narayanan Nikhil Jha Jay Saxena Jayant Choudhary Manju DhindwalJay SaxenaNo ratings yet

- Glenmark Pharmaceuticals Limited - Investor Presentation - Q3 FY24Document19 pagesGlenmark Pharmaceuticals Limited - Investor Presentation - Q3 FY24SHREYA NAIRNo ratings yet

- Godrej Consumer Products LTD.: Analyst Meet TakeawaysDocument6 pagesGodrej Consumer Products LTD.: Analyst Meet TakeawaysArti SalaskarNo ratings yet

- FMCGDocument32 pagesFMCGMayur ChavanNo ratings yet

- Fast Moving Consumer Goods (FMCG) : Industry AnalysisDocument17 pagesFast Moving Consumer Goods (FMCG) : Industry AnalysisPriya AggarwalNo ratings yet

- DairyDocument12 pagesDairyHimanshu SoniNo ratings yet

- Adani Wilmar IPO Note Angel OneDocument7 pagesAdani Wilmar IPO Note Angel OneRevant SatiNo ratings yet

- Dabur India: Outperformance ContinuesDocument14 pagesDabur India: Outperformance ContinuesVishakha RathodNo ratings yet

- Marico Ltd.Document16 pagesMarico Ltd.Mitali ParekhNo ratings yet

- Bajaj Consumer Care Conf Call Transcript 3Q2023Document20 pagesBajaj Consumer Care Conf Call Transcript 3Q2023PradeepNo ratings yet

- Nguyensyquochung - 1097 - 20717 - GROUP 2 - PRUDENTIAL - DIGITIAL MARKETING PLAN PROPOSALDocument39 pagesNguyensyquochung - 1097 - 20717 - GROUP 2 - PRUDENTIAL - DIGITIAL MARKETING PLAN PROPOSALMỹ Tú VõNo ratings yet

- 0.-DTTC BTN Ban-Chinh 15.1Document26 pages0.-DTTC BTN Ban-Chinh 15.1Nhi Tran Vo HoangNo ratings yet

- Ism 2022Document7 pagesIsm 2022Galib NayimNo ratings yet

- ITC Limited Equity Research ReportDocument31 pagesITC Limited Equity Research ReportMithun SanjayNo ratings yet

- 536248112021255dabur India Limited - 20210806Document5 pages536248112021255dabur India Limited - 20210806Michelle CastelinoNo ratings yet

- Analysis of BritanniaDocument12 pagesAnalysis of BritanniaPra RoopNo ratings yet

- Orner Ffice: Weathering Industry Challenges Through Product Innovation and Distribution ReachDocument10 pagesOrner Ffice: Weathering Industry Challenges Through Product Innovation and Distribution Reachprabirkumarghosh02No ratings yet

- Market Value Ratios: Annual Report Analysis of Godrej Consumer ProductsDocument14 pagesMarket Value Ratios: Annual Report Analysis of Godrej Consumer ProductsAmit RanjanNo ratings yet

- Motilal Oswal Sees 2% UPSIDE in Pidilite Industries Broad BasedDocument12 pagesMotilal Oswal Sees 2% UPSIDE in Pidilite Industries Broad BasedArvindRajVTNo ratings yet

- VinamilkDocument7 pagesVinamilkTrần Lê Phương ThảoNo ratings yet

- Hikal LTD: Crop Protection Propels Growth But Margins MissDocument10 pagesHikal LTD: Crop Protection Propels Growth But Margins MissRakesh KumarNo ratings yet

- Fundamental Analysis of The FMCG IndustryDocument58 pagesFundamental Analysis of The FMCG Industryavinash singhNo ratings yet

- FMCG Report July 2018Document32 pagesFMCG Report July 2018Anshuman UpadhyayNo ratings yet

- Dabur Buy ICICIDirect 20200731 PDFDocument9 pagesDabur Buy ICICIDirect 20200731 PDFHitendra PanchalNo ratings yet

- Resilient Q1 Performance Amid Challenges: Hindustan Unilever LTDDocument8 pagesResilient Q1 Performance Amid Challenges: Hindustan Unilever LTDUTSAVNo ratings yet

- Consumer Newsletter - June 2021Document23 pagesConsumer Newsletter - June 2021binoy_jariwalaNo ratings yet

- EMBA Day2Document24 pagesEMBA Day2Abdullah Mohammed ArifNo ratings yet

- AscentWorship - 1C - WaterDocument28 pagesAscentWorship - 1C - WaterAbdullah Mohammed ArifNo ratings yet

- Navana Pharmaceuticals Limited IPO Analytics EnglishDocument4 pagesNavana Pharmaceuticals Limited IPO Analytics EnglishAbdullah Mohammed ArifNo ratings yet

- AscentWorship - 1D - WuduDocument44 pagesAscentWorship - 1D - WuduAbdullah Mohammed ArifNo ratings yet

- AscentWorship - 1B - Introduction To Author TextDocument25 pagesAscentWorship - 1B - Introduction To Author TextAbdullah Mohammed ArifNo ratings yet

- Foundations of Religion and Guidance - 07 - Roots of Islamic TheologyDocument7 pagesFoundations of Religion and Guidance - 07 - Roots of Islamic TheologyAbdullah Mohammed ArifNo ratings yet

- AscentWorship - 1A - Introduction To Fiqh Imam Abu HanifaDocument56 pagesAscentWorship - 1A - Introduction To Fiqh Imam Abu HanifaAbdullah Mohammed ArifNo ratings yet

- Foundations of Religion and Guidance - 06 - The MadhhabsDocument4 pagesFoundations of Religion and Guidance - 06 - The MadhhabsAbdullah Mohammed ArifNo ratings yet

- Foundations of Religion and Guidance - 04 - Transmission of The QuranDocument10 pagesFoundations of Religion and Guidance - 04 - Transmission of The QuranAbdullah Mohammed ArifNo ratings yet

- Efficient Securities MarketDocument19 pagesEfficient Securities MarketAnnisa MuktiNo ratings yet

- COPYRIGHTSDocument16 pagesCOPYRIGHTSMaui IbabaoNo ratings yet

- Regional Trial Court: Motion To Quash Search WarrantDocument3 pagesRegional Trial Court: Motion To Quash Search WarrantPaulo VillarinNo ratings yet

- Assure RMS PDFDocument2 pagesAssure RMS PDFDesi EryonNo ratings yet

- Data Cleansing Process For Master DataDocument4 pagesData Cleansing Process For Master DataAjay Kumar KhattarNo ratings yet

- Pilz PNOZ Sigma PDFDocument16 pagesPilz PNOZ Sigma PDFCristopher Entena100% (1)

- Definition, Nature & Development of Tort Law-1Document40 pagesDefinition, Nature & Development of Tort Law-1Dhinesh Vijayaraj100% (1)

- Amendment of Information, Formal Vs SubstantialDocument2 pagesAmendment of Information, Formal Vs SubstantialNikkoCataquiz100% (3)

- M01e1-Introduction of Optometrists & Opticians Act 2007 PresentationDocument45 pagesM01e1-Introduction of Optometrists & Opticians Act 2007 Presentationsytwins100% (1)

- Succession DigestDocument407 pagesSuccession DigestToni Gabrielle Ang EspinaNo ratings yet

- Cambridge O Level: Business Studies 7115/21Document21 pagesCambridge O Level: Business Studies 7115/21mariejocalouNo ratings yet

- The 2020 Lithium-Ion Battery Guide - The Easy DIY Guide To Building Your Own Battery Packs (Lithium Ion Battery Book Book 1)Document101 pagesThe 2020 Lithium-Ion Battery Guide - The Easy DIY Guide To Building Your Own Battery Packs (Lithium Ion Battery Book Book 1)Hangar Graus75% (4)

- TV Ole 2020Document1 pageTV Ole 2020david floresNo ratings yet

- A Profect Report On Star Claytech Pvt. LTDDocument44 pagesA Profect Report On Star Claytech Pvt. LTDraj danichaNo ratings yet

- Artikel Sardi SantosaDocument18 pagesArtikel Sardi SantosaSardi Santosa NastahNo ratings yet

- Niengo Outsep North Papua 5 - 06 - 07rev2Document20 pagesNiengo Outsep North Papua 5 - 06 - 07rev2Prince DenhaagNo ratings yet

- Solar Charge Controller User Manual: I Functional CharacteristicsDocument5 pagesSolar Charge Controller User Manual: I Functional CharacteristicsAmer WarrakNo ratings yet

- Assignment 2-Groundwater MovementDocument2 pagesAssignment 2-Groundwater MovementPhước LêNo ratings yet

- The Leverage Effect Uncovering The True Nature of VolatilityDocument68 pagesThe Leverage Effect Uncovering The True Nature of VolatilityVlad StNo ratings yet

- Company Profile - V2Document4 pagesCompany Profile - V2bhuvaneshelango2209No ratings yet

- Analysis and Interpretation of Data Research PaperDocument4 pagesAnalysis and Interpretation of Data Research Paperefdkhd4eNo ratings yet

- Ace3 Unit8 TestDocument3 pagesAce3 Unit8 Testnatacha100% (3)

- Gyrator - Wikipedia PDFDocument44 pagesGyrator - Wikipedia PDFRishabh MishraNo ratings yet

Download as pdf or txt

You might also like

- Textbook Promoting Successful Transition To Adulthood For Students With Disabilities 1St Edition Robert L Morgan Ebook All Chapter PDFDocument53 pagesTextbook Promoting Successful Transition To Adulthood For Students With Disabilities 1St Edition Robert L Morgan Ebook All Chapter PDFvicki.vaught30780% (5)

- Boeing 737 Nef Program and Procedures Manual Rev 4Document36 pagesBoeing 737 Nef Program and Procedures Manual Rev 4Adrian100% (2)

- Chapter 5 - Vision and Mission AnalysisDocument40 pagesChapter 5 - Vision and Mission AnalysisNero Sha100% (5)

- NitinolDocument20 pagesNitinolTamara PricilaNo ratings yet

- Sequence of Operation of FahuDocument1 pageSequence of Operation of FahuahmedNo ratings yet

- Measurement of Line Impedances and Mutual Coupling of Parallel LinesDocument8 pagesMeasurement of Line Impedances and Mutual Coupling of Parallel LinesKhandai SeenananNo ratings yet

- Final Report of SIPDocument56 pagesFinal Report of SIPRahul Parashar100% (1)

- FMCG May 2023Document32 pagesFMCG May 2023Sangeethasruthi SNo ratings yet

- FMCG - August - 2023Document32 pagesFMCG - August - 2023Barshali DasNo ratings yet

- FMCG December 2023Document32 pagesFMCG December 2023pimewip969No ratings yet

- Almost-There 2 PDFDocument32 pagesAlmost-There 2 PDFPaul StriderNo ratings yet

- CFA Institute Research Challenge Hosted in CFA Society Bangladesh Team Name: Last In, First OutDocument32 pagesCFA Institute Research Challenge Hosted in CFA Society Bangladesh Team Name: Last In, First OutPaul StriderNo ratings yet

- Almost There PDFDocument32 pagesAlmost There PDFPaul StriderNo ratings yet

- Vishruti Khandelwal PGDM - 1. 2019-1705-0001-0033Document17 pagesVishruti Khandelwal PGDM - 1. 2019-1705-0001-0033Vishruti KhandelwalNo ratings yet

- FMCG IbefDocument32 pagesFMCG IbefjeetNo ratings yet

- Bajaj-Consumer-Care-Limited 827 CompanyUpdate PDFDocument11 pagesBajaj-Consumer-Care-Limited 827 CompanyUpdate PDFhamsNo ratings yet

- Term Paper On Marico Bangladesh Ltd.Document35 pagesTerm Paper On Marico Bangladesh Ltd.simeen srabaniNo ratings yet

- FMCG - Sector ReportDocument10 pagesFMCG - Sector ReportRajendra BhoirNo ratings yet

- Dabur India LTD.: Equity Research ReportDocument40 pagesDabur India LTD.: Equity Research ReportshakeDNo ratings yet

- Marketing Challenges On Siri Food ProductsDocument81 pagesMarketing Challenges On Siri Food ProductsShrivatsa JoshiNo ratings yet

- Castrol India LTD: November 06, 2018Document17 pagesCastrol India LTD: November 06, 2018Yash AgarwalNo ratings yet

- Nestle Equity Research ReportDocument7 pagesNestle Equity Research Reportyadhu krishnaNo ratings yet

- R-Street Investment Challenge: Team Kase Konquerers - Iim KozhikodeDocument12 pagesR-Street Investment Challenge: Team Kase Konquerers - Iim KozhikodeApoorva JainNo ratings yet

- Group 3 - Praj IndustriesDocument9 pagesGroup 3 - Praj IndustriesAayushi ChandwaniNo ratings yet

- B3 - Equity Research ReportDocument9 pagesB3 - Equity Research ReportAayushi ChandwaniNo ratings yet

- Britannia Industries LimitedDocument8 pagesBritannia Industries Limitedvedantpatnaik.privNo ratings yet

- Pidilite CompanyDocument6 pagesPidilite Companykhalsa.taranjitNo ratings yet

- Company Analysis - Britannia Industries Ltd. (Jayraj Agrawal)Document3 pagesCompany Analysis - Britannia Industries Ltd. (Jayraj Agrawal)JAYRAJ AGRAWALNo ratings yet

- Sanitary MKT ReportDocument38 pagesSanitary MKT ReportsanjnuNo ratings yet

- Research Report - Cupid LTDDocument8 pagesResearch Report - Cupid LTDNeetu LatwalNo ratings yet

- DhairyaShah 26 DDocument22 pagesDhairyaShah 26 DDHAIRYA09No ratings yet

- IDirect Zomato IPOReviewDocument13 pagesIDirect Zomato IPOReviewSnehashree SahooNo ratings yet

- Edible Oils in VietnamDocument10 pagesEdible Oils in VietnamNguyen Ly Thanh LuongNo ratings yet

- IDirect GSKConsumer ICDocument26 pagesIDirect GSKConsumer ICChaitanya JagarlapudiNo ratings yet

- Prudential - Digital Marketing ProposalDocument39 pagesPrudential - Digital Marketing ProposalUYÊN NGUYỄN THỊ PHƯƠNGNo ratings yet

- The Scope For GI Based Branding in Agricultural Products An OverviewDocument2 pagesThe Scope For GI Based Branding in Agricultural Products An OverviewEditor IJTSRDNo ratings yet

- Saurabh Ghare - To Study Fundamental Analysis of Fast-Moving Consumer Goods Sector and Comparitive Study of HUL ITCDocument46 pagesSaurabh Ghare - To Study Fundamental Analysis of Fast-Moving Consumer Goods Sector and Comparitive Study of HUL ITCKRITARTH SINGHNo ratings yet

- Bajaj AllianzDocument99 pagesBajaj AllianzYASH PRAJAPATINo ratings yet

- Marketing Management: (Document Subtitle)Document21 pagesMarketing Management: (Document Subtitle)aseni herathNo ratings yet

- MOSL AGIC - Highlights From The ConferenceDocument74 pagesMOSL AGIC - Highlights From The ConferenceqwertixNo ratings yet

- BCG Analysis-Report: Prepared By: Sanya Nauharia Sankara Narayanan Nikhil Jha Jay Saxena Jayant Choudhary Manju DhindwalDocument9 pagesBCG Analysis-Report: Prepared By: Sanya Nauharia Sankara Narayanan Nikhil Jha Jay Saxena Jayant Choudhary Manju DhindwalJay SaxenaNo ratings yet

- Glenmark Pharmaceuticals Limited - Investor Presentation - Q3 FY24Document19 pagesGlenmark Pharmaceuticals Limited - Investor Presentation - Q3 FY24SHREYA NAIRNo ratings yet

- Godrej Consumer Products LTD.: Analyst Meet TakeawaysDocument6 pagesGodrej Consumer Products LTD.: Analyst Meet TakeawaysArti SalaskarNo ratings yet

- FMCGDocument32 pagesFMCGMayur ChavanNo ratings yet

- Fast Moving Consumer Goods (FMCG) : Industry AnalysisDocument17 pagesFast Moving Consumer Goods (FMCG) : Industry AnalysisPriya AggarwalNo ratings yet

- DairyDocument12 pagesDairyHimanshu SoniNo ratings yet

- Adani Wilmar IPO Note Angel OneDocument7 pagesAdani Wilmar IPO Note Angel OneRevant SatiNo ratings yet

- Dabur India: Outperformance ContinuesDocument14 pagesDabur India: Outperformance ContinuesVishakha RathodNo ratings yet

- Marico Ltd.Document16 pagesMarico Ltd.Mitali ParekhNo ratings yet

- Bajaj Consumer Care Conf Call Transcript 3Q2023Document20 pagesBajaj Consumer Care Conf Call Transcript 3Q2023PradeepNo ratings yet

- Nguyensyquochung - 1097 - 20717 - GROUP 2 - PRUDENTIAL - DIGITIAL MARKETING PLAN PROPOSALDocument39 pagesNguyensyquochung - 1097 - 20717 - GROUP 2 - PRUDENTIAL - DIGITIAL MARKETING PLAN PROPOSALMỹ Tú VõNo ratings yet

- 0.-DTTC BTN Ban-Chinh 15.1Document26 pages0.-DTTC BTN Ban-Chinh 15.1Nhi Tran Vo HoangNo ratings yet

- Ism 2022Document7 pagesIsm 2022Galib NayimNo ratings yet

- ITC Limited Equity Research ReportDocument31 pagesITC Limited Equity Research ReportMithun SanjayNo ratings yet

- 536248112021255dabur India Limited - 20210806Document5 pages536248112021255dabur India Limited - 20210806Michelle CastelinoNo ratings yet

- Analysis of BritanniaDocument12 pagesAnalysis of BritanniaPra RoopNo ratings yet

- Orner Ffice: Weathering Industry Challenges Through Product Innovation and Distribution ReachDocument10 pagesOrner Ffice: Weathering Industry Challenges Through Product Innovation and Distribution Reachprabirkumarghosh02No ratings yet

- Market Value Ratios: Annual Report Analysis of Godrej Consumer ProductsDocument14 pagesMarket Value Ratios: Annual Report Analysis of Godrej Consumer ProductsAmit RanjanNo ratings yet

- Motilal Oswal Sees 2% UPSIDE in Pidilite Industries Broad BasedDocument12 pagesMotilal Oswal Sees 2% UPSIDE in Pidilite Industries Broad BasedArvindRajVTNo ratings yet

- VinamilkDocument7 pagesVinamilkTrần Lê Phương ThảoNo ratings yet

- Hikal LTD: Crop Protection Propels Growth But Margins MissDocument10 pagesHikal LTD: Crop Protection Propels Growth But Margins MissRakesh KumarNo ratings yet

- Fundamental Analysis of The FMCG IndustryDocument58 pagesFundamental Analysis of The FMCG Industryavinash singhNo ratings yet

- FMCG Report July 2018Document32 pagesFMCG Report July 2018Anshuman UpadhyayNo ratings yet

- Dabur Buy ICICIDirect 20200731 PDFDocument9 pagesDabur Buy ICICIDirect 20200731 PDFHitendra PanchalNo ratings yet

- Resilient Q1 Performance Amid Challenges: Hindustan Unilever LTDDocument8 pagesResilient Q1 Performance Amid Challenges: Hindustan Unilever LTDUTSAVNo ratings yet

- Consumer Newsletter - June 2021Document23 pagesConsumer Newsletter - June 2021binoy_jariwalaNo ratings yet

- EMBA Day2Document24 pagesEMBA Day2Abdullah Mohammed ArifNo ratings yet

- AscentWorship - 1C - WaterDocument28 pagesAscentWorship - 1C - WaterAbdullah Mohammed ArifNo ratings yet

- Navana Pharmaceuticals Limited IPO Analytics EnglishDocument4 pagesNavana Pharmaceuticals Limited IPO Analytics EnglishAbdullah Mohammed ArifNo ratings yet

- AscentWorship - 1D - WuduDocument44 pagesAscentWorship - 1D - WuduAbdullah Mohammed ArifNo ratings yet

- AscentWorship - 1B - Introduction To Author TextDocument25 pagesAscentWorship - 1B - Introduction To Author TextAbdullah Mohammed ArifNo ratings yet

- Foundations of Religion and Guidance - 07 - Roots of Islamic TheologyDocument7 pagesFoundations of Religion and Guidance - 07 - Roots of Islamic TheologyAbdullah Mohammed ArifNo ratings yet

- AscentWorship - 1A - Introduction To Fiqh Imam Abu HanifaDocument56 pagesAscentWorship - 1A - Introduction To Fiqh Imam Abu HanifaAbdullah Mohammed ArifNo ratings yet

- Foundations of Religion and Guidance - 06 - The MadhhabsDocument4 pagesFoundations of Religion and Guidance - 06 - The MadhhabsAbdullah Mohammed ArifNo ratings yet

- Foundations of Religion and Guidance - 04 - Transmission of The QuranDocument10 pagesFoundations of Religion and Guidance - 04 - Transmission of The QuranAbdullah Mohammed ArifNo ratings yet

- Efficient Securities MarketDocument19 pagesEfficient Securities MarketAnnisa MuktiNo ratings yet

- COPYRIGHTSDocument16 pagesCOPYRIGHTSMaui IbabaoNo ratings yet

- Regional Trial Court: Motion To Quash Search WarrantDocument3 pagesRegional Trial Court: Motion To Quash Search WarrantPaulo VillarinNo ratings yet

- Assure RMS PDFDocument2 pagesAssure RMS PDFDesi EryonNo ratings yet

- Data Cleansing Process For Master DataDocument4 pagesData Cleansing Process For Master DataAjay Kumar KhattarNo ratings yet

- Pilz PNOZ Sigma PDFDocument16 pagesPilz PNOZ Sigma PDFCristopher Entena100% (1)

- Definition, Nature & Development of Tort Law-1Document40 pagesDefinition, Nature & Development of Tort Law-1Dhinesh Vijayaraj100% (1)

- Amendment of Information, Formal Vs SubstantialDocument2 pagesAmendment of Information, Formal Vs SubstantialNikkoCataquiz100% (3)

- M01e1-Introduction of Optometrists & Opticians Act 2007 PresentationDocument45 pagesM01e1-Introduction of Optometrists & Opticians Act 2007 Presentationsytwins100% (1)

- Succession DigestDocument407 pagesSuccession DigestToni Gabrielle Ang EspinaNo ratings yet

- Cambridge O Level: Business Studies 7115/21Document21 pagesCambridge O Level: Business Studies 7115/21mariejocalouNo ratings yet

- The 2020 Lithium-Ion Battery Guide - The Easy DIY Guide To Building Your Own Battery Packs (Lithium Ion Battery Book Book 1)Document101 pagesThe 2020 Lithium-Ion Battery Guide - The Easy DIY Guide To Building Your Own Battery Packs (Lithium Ion Battery Book Book 1)Hangar Graus75% (4)

- TV Ole 2020Document1 pageTV Ole 2020david floresNo ratings yet

- A Profect Report On Star Claytech Pvt. LTDDocument44 pagesA Profect Report On Star Claytech Pvt. LTDraj danichaNo ratings yet

- Artikel Sardi SantosaDocument18 pagesArtikel Sardi SantosaSardi Santosa NastahNo ratings yet

- Niengo Outsep North Papua 5 - 06 - 07rev2Document20 pagesNiengo Outsep North Papua 5 - 06 - 07rev2Prince DenhaagNo ratings yet

- Solar Charge Controller User Manual: I Functional CharacteristicsDocument5 pagesSolar Charge Controller User Manual: I Functional CharacteristicsAmer WarrakNo ratings yet

- Assignment 2-Groundwater MovementDocument2 pagesAssignment 2-Groundwater MovementPhước LêNo ratings yet

- The Leverage Effect Uncovering The True Nature of VolatilityDocument68 pagesThe Leverage Effect Uncovering The True Nature of VolatilityVlad StNo ratings yet

- Company Profile - V2Document4 pagesCompany Profile - V2bhuvaneshelango2209No ratings yet

- Analysis and Interpretation of Data Research PaperDocument4 pagesAnalysis and Interpretation of Data Research Paperefdkhd4eNo ratings yet

- Ace3 Unit8 TestDocument3 pagesAce3 Unit8 Testnatacha100% (3)

- Gyrator - Wikipedia PDFDocument44 pagesGyrator - Wikipedia PDFRishabh MishraNo ratings yet