Download as doc, pdf, or txt

You might also like

- Introduction To International AccountingDocument7 pagesIntroduction To International AccountinghemantbaidNo ratings yet

- Content Analysis of Textbook From Human Rights Perspective - RukhsanaDocument13 pagesContent Analysis of Textbook From Human Rights Perspective - RukhsanaWaseem Khan67% (3)

- Changes in European Accounting Standard: Swapnil Pacharne: 32 Pintu Rajan: 39 Praful Shettigar: 48Document8 pagesChanges in European Accounting Standard: Swapnil Pacharne: 32 Pintu Rajan: 39 Praful Shettigar: 48praful_shettigarNo ratings yet

- IFRSDocument11 pagesIFRSSagar PanchalNo ratings yet

- Audit Reports On Financial Statements Prepared According To IASB Standards: Empirical Evidence From The European UnionDocument27 pagesAudit Reports On Financial Statements Prepared According To IASB Standards: Empirical Evidence From The European UnionSpytersNo ratings yet

- The Regulatory Framework of AccountingDocument52 pagesThe Regulatory Framework of Accountingssentu100% (1)

- Harmonization and Convergence of StandardsDocument2 pagesHarmonization and Convergence of StandardsSuzette EstiponaNo ratings yet

- Ifrs 3Document140 pagesIfrs 3RakeshkargwalNo ratings yet

- International Financial Reporting Standards: Revised Readiness ToolkitDocument39 pagesInternational Financial Reporting Standards: Revised Readiness ToolkitBASANTA KUMAR SAHUNo ratings yet

- Press Release: International Accounting Standards BoardDocument3 pagesPress Release: International Accounting Standards Boardjgutierrez_edu4213No ratings yet

- International Financial Reporting Standards: Revised Readiness ToolkitDocument40 pagesInternational Financial Reporting Standards: Revised Readiness ToolkitBikaZeeNo ratings yet

- PGC InglesDocument366 pagesPGC InglesNoelia Peirats AymerichNo ratings yet

- EPSAS Progress Report 2019Document9 pagesEPSAS Progress Report 2019Helen ConJotaNo ratings yet

- Chapter 1 - Nature and Regulation of Companies: Review QuestionsDocument19 pagesChapter 1 - Nature and Regulation of Companies: Review QuestionsShek Kwun HeiNo ratings yet

- 2003 PR On ImprovementsDocument6 pages2003 PR On ImprovementsKreshen ShunmugamNo ratings yet

- Assignment: Under Guidance ofDocument13 pagesAssignment: Under Guidance ofRohit PrasadNo ratings yet

- Multinational InfluenceDocument14 pagesMultinational InfluenceVitalie MihailovNo ratings yet

- Objective: Session 01 - International Financial Reporting StandardsDocument18 pagesObjective: Session 01 - International Financial Reporting StandardsVladlenaAlekseenkoNo ratings yet

- Improvement Actions FRANCEDocument17 pagesImprovement Actions FRANCETHE SEZARNo ratings yet

- Lesson 1Document14 pagesLesson 1Alberto HidalgoNo ratings yet

- Ifrs AssignmentDocument13 pagesIfrs Assignmentarijit nathNo ratings yet

- International Financial Reporting Standards A PreDocument10 pagesInternational Financial Reporting Standards A Preadmid aisyahNo ratings yet

- Ias 8Document35 pagesIas 8saif700No ratings yet

- International Accounting Standard - IAS1Document17 pagesInternational Accounting Standard - IAS1khaldoun AlhroubNo ratings yet

- Statement: On The Development and Use of InternationalDocument4 pagesStatement: On The Development and Use of InternationalgdegirolamoNo ratings yet

- Accounting Policies, Changes in Accounting Estimates and ErrorsDocument20 pagesAccounting Policies, Changes in Accounting Estimates and ErrorsJorreyGarciaOplasNo ratings yet

- FUJI Fertilizer: HedgingDocument2 pagesFUJI Fertilizer: HedgingMuhammad Adnan SamiNo ratings yet

- Ypla Academies Financial Handbook GN Nov06Document212 pagesYpla Academies Financial Handbook GN Nov06glonsdale1No ratings yet

- NUWAMANYA PATIENCE-IAS and IFRS-1Document20 pagesNUWAMANYA PATIENCE-IAS and IFRS-1MUSINGUZI IVANNo ratings yet

- COA Circular 2020-001 DTD January 8, 2020 Revised Chart of AccountsDocument2 pagesCOA Circular 2020-001 DTD January 8, 2020 Revised Chart of AccountssssancoberNo ratings yet

- Jurnal BAB 8Document13 pagesJurnal BAB 8Arif NugrohoNo ratings yet

- PRC Colc Tot Esms An3Document59 pagesPRC Colc Tot Esms An3juancsanjoseNo ratings yet

- Consolidated and Separate Financial Statements: International Accounting Standard 27Document41 pagesConsolidated and Separate Financial Statements: International Accounting Standard 27davidwijaya1986No ratings yet

- IAS 8 Accounting Policies - Changes in Accounting Estimates and Errors PDFDocument20 pagesIAS 8 Accounting Policies - Changes in Accounting Estimates and Errors PDFMichelle TanNo ratings yet

- Analysis of The Accounting Systems From Romania and Moldova: AbstractDocument6 pagesAnalysis of The Accounting Systems From Romania and Moldova: AbstractLucia Morosan-DanilaNo ratings yet

- Material PCGE 1-URP Group3Dec19AMBDocument68 pagesMaterial PCGE 1-URP Group3Dec19AMBScribdTranslationsNo ratings yet

- F7FR RQB As - j08Document126 pagesF7FR RQB As - j08Jamilya SNo ratings yet

- 6 Saiful Assets 123Document30 pages6 Saiful Assets 123Zahra RamadhaniNo ratings yet

- Ipsas 6 Consolidated and 3Document36 pagesIpsas 6 Consolidated and 3EmmaNo ratings yet

- Reflection PaperDocument10 pagesReflection PaperhouseoflannisterNo ratings yet

- RBV2013 Conceptual FrameworkDocument32 pagesRBV2013 Conceptual FrameworkhemantbaidNo ratings yet

- E TechnicalDocument6 pagesE Technicalkhurram_66No ratings yet

- Test PDFDocument3 pagesTest PDFYiannisNo ratings yet

- Ias 9Document5 pagesIas 9Giulia TabaraNo ratings yet

- GCA Consultants: Introduction of The EuroDocument34 pagesGCA Consultants: Introduction of The EuroNaeem MalikNo ratings yet

- List of Institute'S Publications Relevant For May, 2011 ExaminationDocument15 pagesList of Institute'S Publications Relevant For May, 2011 ExaminationVineet ShahNo ratings yet

- Annual Report MCADocument69 pagesAnnual Report MCARahul BhanNo ratings yet

- British Accounting StandardsDocument7 pagesBritish Accounting StandardsZeeshanSameenNo ratings yet

- AFADocument26 pagesAFAMAHENDRAN_CHRISTNo ratings yet

- What Is IfrsDocument11 pagesWhat Is IfrsSandy Gill GillNo ratings yet

- A10 Ipsas - 01Document60 pagesA10 Ipsas - 01Marius SteffyNo ratings yet

- Stephen Das A 4022183 Research Proposal-IfRSDocument25 pagesStephen Das A 4022183 Research Proposal-IfRSStephen Das100% (1)

- International Accounting Standards PDFDocument54 pagesInternational Accounting Standards PDFAKINYEMI ADISA KAMORUNo ratings yet

- A Practical Guide To New IFRSs 2011Document27 pagesA Practical Guide To New IFRSs 2011darciechoyNo ratings yet

- International Public Sector Accounting Standards Implementation Road Map for UzbekistanFrom EverandInternational Public Sector Accounting Standards Implementation Road Map for UzbekistanNo ratings yet

- Codification of Statements on Standards for Accounting and Review Services: Numbers 21-24From EverandCodification of Statements on Standards for Accounting and Review Services: Numbers 21-24No ratings yet

- Audit and Accounting Guide: Entities With Oil and Gas Producing Activities, 2018From EverandAudit and Accounting Guide: Entities With Oil and Gas Producing Activities, 2018No ratings yet

- Estimating Value-Added Tax Using a Supply and Use Framework: The ADB National Accounts Statistics Value-Added Tax ModelFrom EverandEstimating Value-Added Tax Using a Supply and Use Framework: The ADB National Accounts Statistics Value-Added Tax ModelNo ratings yet

- Common Bank Interview QuestionsDocument23 pagesCommon Bank Interview Questionssultan erbo0% (1)

- LPG in IndiaDocument14 pagesLPG in Indiasangeetha_sasid2201No ratings yet

- Zamora V QuinanDocument6 pagesZamora V QuinanSocrates Jerome De Guzman100% (1)

- Discipleship in Practice: Assembly Bible Class For TeensDocument17 pagesDiscipleship in Practice: Assembly Bible Class For TeensChristian Believers' Assembly Borivali100% (1)

- Problems 1st PartDocument17 pagesProblems 1st PartMelyssa Ayala0% (1)

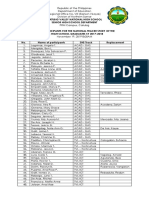

- Catubig Valley National High School Senior High School DepartmentDocument1 pageCatubig Valley National High School Senior High School DepartmentDerickNo ratings yet

- Art. VI Sec. 27 32Document180 pagesArt. VI Sec. 27 32John Henry GramaNo ratings yet

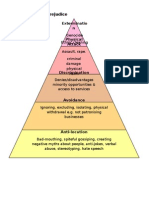

- Allports Scale of PrejudiceDocument1 pageAllports Scale of PrejudicebmckNo ratings yet

- PCVL Nle B2Document5 pagesPCVL Nle B2WEINDLY AYONo ratings yet

- Resident Mammals FIDEC vs. Sec. ReyesDocument4 pagesResident Mammals FIDEC vs. Sec. ReyesDawn Jessa Go0% (1)

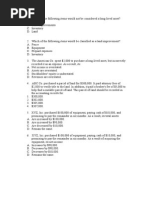

- Depreciation MCQDocument3 pagesDepreciation MCQWalid Mohamed AnwarNo ratings yet

- 019GMA Network Vs Commission On Elections, 734 SCRA 88, G.R. No. 205357, September 2, 2014Document165 pages019GMA Network Vs Commission On Elections, 734 SCRA 88, G.R. No. 205357, September 2, 2014Lu CasNo ratings yet

- In and Then There Were NoneDocument3 pagesIn and Then There Were Noneapi-355592002No ratings yet

- Nicholas Patrick HendrixDocument8 pagesNicholas Patrick HendrixNEWS CENTER MaineNo ratings yet

- Can't We All Just Get Along - Conflict Resolution StrategiesDocument24 pagesCan't We All Just Get Along - Conflict Resolution StrategiesDuy BùiNo ratings yet

- Blaw SoftDocument596 pagesBlaw Softjonathan tanNo ratings yet

- SUPREME COURT REPORTS ANNOTATED VOLUME 626 Case 10Document29 pagesSUPREME COURT REPORTS ANNOTATED VOLUME 626 Case 10Marie Bernadette BartolomeNo ratings yet

- People vs. Ampuan (Rule 117)Document2 pagesPeople vs. Ampuan (Rule 117)merebearooNo ratings yet

- Bishop of Nueva Segovia Vs Provincial BoardDocument1 pageBishop of Nueva Segovia Vs Provincial BoardJan Carlo SanchezNo ratings yet

- CTC - Salary Slip - The Very Basic VersionDocument2 pagesCTC - Salary Slip - The Very Basic VersionAJAY KULKARNI100% (2)

- Texas Certified Lienholders ListDocument62 pagesTexas Certified Lienholders ListJose CeceñaNo ratings yet

- 2 Term Mock Exam: Paper 1 Name: - Total Mark: - /30Document8 pages2 Term Mock Exam: Paper 1 Name: - Total Mark: - /30Training & Development GWCNo ratings yet

- CHC2D1 World War 1Document74 pagesCHC2D1 World War 1Zer0oBtwNo ratings yet

- Understanding Culture, Society, and PoliticsDocument2 pagesUnderstanding Culture, Society, and Politicsria ricciNo ratings yet

- Chapter - 6 Work Energy and PowerDocument34 pagesChapter - 6 Work Energy and PowerNafees FarheenNo ratings yet

- Employee Release, Waiver and Quitclaim With UndertakingDocument2 pagesEmployee Release, Waiver and Quitclaim With UndertakingChristian RoqueNo ratings yet

- MCQ On Finals TaxesDocument7 pagesMCQ On Finals TaxesRandy ManzanoNo ratings yet

- ArtcDocument2 pagesArtcEswar VarmaNo ratings yet

- National Bankruptcy Services The LedgerDocument28 pagesNational Bankruptcy Services The LedgerOxigyneNo ratings yet