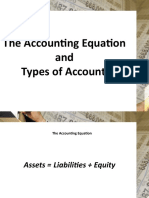

Abm 1-W6.M2.T1.L1

Abm 1-W6.M2.T1.L1

You might also like

- Fabm1 Module 7Document26 pagesFabm1 Module 7Randy Magbudhi100% (10)

- Accounting Basics Part 1Document33 pagesAccounting Basics Part 1Vinny Hungwe100% (1)

- Accounting Basics, Part 1: Accrual, Double-Entry Accounting, Debits & Credits, Chart of Accounts Journals And, LedgerDocument147 pagesAccounting Basics, Part 1: Accrual, Double-Entry Accounting, Debits & Credits, Chart of Accounts Journals And, LedgerThe Three Queens100% (1)

- Accounting BasicsDocument147 pagesAccounting BasicsAnnie Berja GucabanNo ratings yet

- BOOKKEEPING BasicsDocument100 pagesBOOKKEEPING BasicsIan Pol Fiesta100% (1)

- Abm Abm Abm AbmDocument27 pagesAbm Abm Abm AbmNoaj Palon100% (1)

- BSBA 1 Topic 4 2022 For The StudentsDocument4 pagesBSBA 1 Topic 4 2022 For The StudentsshanehermoginoNo ratings yet

- Unit 2: General Concepts and Principles of AccountingDocument12 pagesUnit 2: General Concepts and Principles of AccountingChen HaoNo ratings yet

- W3 Las Fabm1-Catherine-Pascual PDFDocument8 pagesW3 Las Fabm1-Catherine-Pascual PDFSynd WpNo ratings yet

- Local Media8011400976913649007Document16 pagesLocal Media8011400976913649007Ivan dela CruzNo ratings yet

- Chapter 2 Fundamentals of Accounting Module PDFDocument12 pagesChapter 2 Fundamentals of Accounting Module PDFCyrille Kaye TorrecampoNo ratings yet

- Chapter 3 - The Accounting Equation FinalDocument22 pagesChapter 3 - The Accounting Equation FinalEowyn DianaNo ratings yet

- Accounting - Self Study Guide For Staff of Micro Finance InstitutionsDocument9 pagesAccounting - Self Study Guide For Staff of Micro Finance Institutionsஆக்ஞா கிருஷ்ணா ஷர்மாNo ratings yet

- Module 3Document47 pagesModule 3Harrold HarryNo ratings yet

- Lesson 3 - AccountsDocument13 pagesLesson 3 - AccountsJeyem AscueNo ratings yet

- Types of Major Accounts PDFDocument14 pagesTypes of Major Accounts PDFDennis LacsonNo ratings yet

- Accounting 1 (SHS) - Week 6 - Accounting EquationDocument31 pagesAccounting 1 (SHS) - Week 6 - Accounting EquationAustin Capal Dela CruzNo ratings yet

- Accounting For Non-Accountant HandoutDocument26 pagesAccounting For Non-Accountant HandoutROMMUEL TOLENTINONo ratings yet

- Fundamentals of Accountancy, Business and Management 1: Learning Activity SheetDocument11 pagesFundamentals of Accountancy, Business and Management 1: Learning Activity SheetMarlyn LotivioNo ratings yet

- Learning Module 5 FarDocument11 pagesLearning Module 5 FarAira AbigailNo ratings yet

- Learning Module 5 FarDocument10 pagesLearning Module 5 FarAngelica SamboNo ratings yet

- Las 5 2S2QW4Document4 pagesLas 5 2S2QW4Luis UrsusNo ratings yet

- Fabm1 Grade-11 QTR1 Module4 Week-4Document6 pagesFabm1 Grade-11 QTR1 Module4 Week-4John anthony CasucoNo ratings yet

- Ass 2Document4 pagesAss 2CARMINA SANCHEZNo ratings yet

- ISR 111 - Chapter 6 MaterialsDocument14 pagesISR 111 - Chapter 6 MaterialsTrisha Nicole FajardoNo ratings yet

- Acctg. Ed 1 - Unit2 Module 4Document13 pagesAcctg. Ed 1 - Unit2 Module 4Angel Justine BernardoNo ratings yet

- EntrepreneurshipHandout Week 5Document6 pagesEntrepreneurshipHandout Week 5Pio GuiretNo ratings yet

- Economy ProfitDocument18 pagesEconomy ProfitVenkata Naresh KachhalaNo ratings yet

- Chapter 11 Bookkeeping EntrepDocument37 pagesChapter 11 Bookkeeping EntrepJacel GadonNo ratings yet

- Financial Acctg Reporting 1 Chapter 10Document18 pagesFinancial Acctg Reporting 1 Chapter 10Charise Jane ZullaNo ratings yet

- Elements of Financial Statements: AssetsDocument39 pagesElements of Financial Statements: AssetsEdna MingNo ratings yet

- Accounting Module 4 PDFDocument9 pagesAccounting Module 4 PDFMaria CristinaNo ratings yet

- Fundamentals of Accountancy, Business and Management 1Document25 pagesFundamentals of Accountancy, Business and Management 1Worship Songs / Choreo / LyricsNo ratings yet

- ChapterDocument47 pagesChapteralfyomar79No ratings yet

- Financial Accounting: PGP-1 June 2010Document29 pagesFinancial Accounting: PGP-1 June 2010Sukeerth ThodimaladinneNo ratings yet

- Accounting and FinanceDocument51 pagesAccounting and FinanceVIGNESH MBANo ratings yet

- 1 BSA WORKBOOK PS ServiceDocument37 pages1 BSA WORKBOOK PS ServiceFelicity ZodiacalNo ratings yet

- Q2Mod4TVEGrade10Entrep-BaesDacanayTalavera 1150BNAHS 250FBHS-CommonDocument10 pagesQ2Mod4TVEGrade10Entrep-BaesDacanayTalavera 1150BNAHS 250FBHS-CommonYato CreNo ratings yet

- Fabm2 - Summative Test 1Document2 pagesFabm2 - Summative Test 1Kyla AcyatanNo ratings yet

- Business ModelDocument29 pagesBusiness ModelTirsolito SalvadorNo ratings yet

- Accountancy: Shaheen Falcons Pu CollegeDocument13 pagesAccountancy: Shaheen Falcons Pu CollegeMohammed RayyanNo ratings yet

- Prepratory Material - AFMDocument39 pagesPrepratory Material - AFMRUTHVIK NETHANo ratings yet

- Module 001: Review of The Basic Accounting Concepts and PrinciplesDocument18 pagesModule 001: Review of The Basic Accounting Concepts and PrinciplesHo Ming LamNo ratings yet

- Accounting C2 Lesson 2 PDFDocument6 pagesAccounting C2 Lesson 2 PDFJake ShimNo ratings yet

- Chapter 4 Accounting Information SystemDocument3 pagesChapter 4 Accounting Information SystemFlordeliza HalogNo ratings yet

- Shs Fabm2 q3 Weeks 1 2 2ndreading Egs EditedfinalDocument20 pagesShs Fabm2 q3 Weeks 1 2 2ndreading Egs EditedfinalKrize Colene dela CruzNo ratings yet

- Exam Revision - 9 & 10 SolDocument7 pagesExam Revision - 9 & 10 SolNguyễn Minh ĐứcNo ratings yet

- Double Entry BookkeepingDocument23 pagesDouble Entry BookkeepingAhrian BenaNo ratings yet

- Part B: Computerised AccountingDocument6 pagesPart B: Computerised AccountingSonakshi JainNo ratings yet

- Why Do We Care About Revenue Recognition?: 15.514 2003 Session 4Document14 pagesWhy Do We Care About Revenue Recognition?: 15.514 2003 Session 4Veli NgwenyaNo ratings yet

- Basic Accounting For IT Part IIDocument4 pagesBasic Accounting For IT Part IImailbag6100% (1)

- Exam Revision - Chapter 9 10Document7 pagesExam Revision - Chapter 9 10Vũ Thị NgoanNo ratings yet

- Lec 4 NotesDocument14 pagesLec 4 NotesAhmed AltohamyNo ratings yet

- Financial Statements and Business DecisionsDocument37 pagesFinancial Statements and Business DecisionsHARMAN SINGHNo ratings yet

- 22 - AE - 111 - Module - 3 - Recording - Business - TransactionsDocument23 pages22 - AE - 111 - Module - 3 - Recording - Business - TransactionsEnrica BalladaresNo ratings yet

- Tutorial 1 - SsDocument3 pagesTutorial 1 - SsChigoziem OnyekawaNo ratings yet

- Basic AccountingDocument32 pagesBasic AccountinghectorbaladingNo ratings yet

- Supplementary 1 - Financial StatementsDocument21 pagesSupplementary 1 - Financial StatementsQuốc Khánh100% (1)

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- Payment HistoryDocument1 pagePayment HistoryRam KumarNo ratings yet

- Accounting 101 - Cash and Cash EquivalentsDocument2 pagesAccounting 101 - Cash and Cash EquivalentsNoah HNo ratings yet

- Consultancy Services For Technical Support Unit & Related Services Under BMWSS Project Technical ProposalDocument5 pagesConsultancy Services For Technical Support Unit & Related Services Under BMWSS Project Technical ProposalKohana RaggsNo ratings yet

- TC-20190629-0033 Tomy AdityaramaDocument1 pageTC-20190629-0033 Tomy AdityaramatommmmmmyNo ratings yet

- Consumer S Behaviour Regarding Cashless Payments During The Covid-19 PandemicDocument13 pagesConsumer S Behaviour Regarding Cashless Payments During The Covid-19 PandemicAesthetica MoonNo ratings yet

- Lecture 10 Cash and Internal Controls - NUS ACC1002 2020 SpringDocument24 pagesLecture 10 Cash and Internal Controls - NUS ACC1002 2020 SpringZenyuiNo ratings yet

- Financial Accounting Solution ch14Document23 pagesFinancial Accounting Solution ch14hw cNo ratings yet

- User Manual Oracle Banking Digital Experience Corporate Cash ManagementDocument36 pagesUser Manual Oracle Banking Digital Experience Corporate Cash ManagementpatienceNo ratings yet

- Basic Concepts of Guest Accounting - PT 2Document36 pagesBasic Concepts of Guest Accounting - PT 2Leonardo FloresNo ratings yet

- Co DLP English Grade 5 Q1Document5 pagesCo DLP English Grade 5 Q1cindymiranda810No ratings yet

- GABI@211Document22 pagesGABI@211princeaugust558No ratings yet

- Qdoc - Tips Internship Report On MCBDocument50 pagesQdoc - Tips Internship Report On MCBRaza AliNo ratings yet

- Sta Clara - Summary Part 1Document49 pagesSta Clara - Summary Part 1Carms St ClaireNo ratings yet

- Week 4 5 ULOb Lets Analyze Activity 1 SolutionDocument2 pagesWeek 4 5 ULOb Lets Analyze Activity 1 Solutionemem resuentoNo ratings yet

- Adnan AskariDocument72 pagesAdnan AskariFaisal AwanNo ratings yet

- Cash Management in SBI Effect On Their Customers .Docx (3) - 1 (3) (Repaired)Document75 pagesCash Management in SBI Effect On Their Customers .Docx (3) - 1 (3) (Repaired)anas khanNo ratings yet

- AIF Benchmarking - FAQsDocument10 pagesAIF Benchmarking - FAQsHarishNo ratings yet

- Audit of Cash and Marketable SecuritiesDocument21 pagesAudit of Cash and Marketable Securitiesዝምታ ተሻለNo ratings yet

- Act 110 Activity 4 (Answe Sheet - Dimalawang)Document2 pagesAct 110 Activity 4 (Answe Sheet - Dimalawang)Norkan DimalawangNo ratings yet

- Financial Management Class Part 2-KasetsartDocument66 pagesFinancial Management Class Part 2-KasetsartKong KrcNo ratings yet

- Chapter 11 Statement of Cash FlowsDocument4 pagesChapter 11 Statement of Cash FlowsEllen MaskariñoNo ratings yet

- Retail Teller Oracle FLEXCUBE Universal Banking Release 11.3.1.0.0EU (April) (2012) Oracle Part Number E51534-01Document45 pagesRetail Teller Oracle FLEXCUBE Universal Banking Release 11.3.1.0.0EU (April) (2012) Oracle Part Number E51534-01Omar AlgaddarNo ratings yet

- Assessmentscashmanagement DashanDocument16 pagesAssessmentscashmanagement Dashanhasenabdi30No ratings yet

- Demonetisation in IndiaDocument23 pagesDemonetisation in IndiaNITISH BHARDWAJNo ratings yet

- Error Correction Problem 1: Lord Gen A. Rilloraza, CPADocument5 pagesError Correction Problem 1: Lord Gen A. Rilloraza, CPAMae-shane SagayoNo ratings yet

- NPO Accounting Basis Tool V3Document39 pagesNPO Accounting Basis Tool V3Ipang NoyoNo ratings yet

- AIS615Document7 pagesAIS615Khamila NajwaNo ratings yet

- Bank Account Management - Cash PoolDocument10 pagesBank Account Management - Cash PoolDillip Kumar mallickNo ratings yet

- Teller - Transaction: Concept-Since The TELLER Application Will Be One and There Will Be Different Types of TransactionsDocument5 pagesTeller - Transaction: Concept-Since The TELLER Application Will Be One and There Will Be Different Types of TransactionsKamran MallickNo ratings yet

- Solved Discovered An Error in Computing A Commission Received Cash FromDocument1 pageSolved Discovered An Error in Computing A Commission Received Cash FromAnbu jaromiaNo ratings yet

Download as pdf or txt

You might also like

- Fabm1 Module 7Document26 pagesFabm1 Module 7Randy Magbudhi100% (10)

- Accounting Basics Part 1Document33 pagesAccounting Basics Part 1Vinny Hungwe100% (1)

- Accounting Basics, Part 1: Accrual, Double-Entry Accounting, Debits & Credits, Chart of Accounts Journals And, LedgerDocument147 pagesAccounting Basics, Part 1: Accrual, Double-Entry Accounting, Debits & Credits, Chart of Accounts Journals And, LedgerThe Three Queens100% (1)

- Accounting BasicsDocument147 pagesAccounting BasicsAnnie Berja GucabanNo ratings yet

- BOOKKEEPING BasicsDocument100 pagesBOOKKEEPING BasicsIan Pol Fiesta100% (1)

- Abm Abm Abm AbmDocument27 pagesAbm Abm Abm AbmNoaj Palon100% (1)

- BSBA 1 Topic 4 2022 For The StudentsDocument4 pagesBSBA 1 Topic 4 2022 For The StudentsshanehermoginoNo ratings yet

- Unit 2: General Concepts and Principles of AccountingDocument12 pagesUnit 2: General Concepts and Principles of AccountingChen HaoNo ratings yet

- W3 Las Fabm1-Catherine-Pascual PDFDocument8 pagesW3 Las Fabm1-Catherine-Pascual PDFSynd WpNo ratings yet

- Local Media8011400976913649007Document16 pagesLocal Media8011400976913649007Ivan dela CruzNo ratings yet

- Chapter 2 Fundamentals of Accounting Module PDFDocument12 pagesChapter 2 Fundamentals of Accounting Module PDFCyrille Kaye TorrecampoNo ratings yet

- Chapter 3 - The Accounting Equation FinalDocument22 pagesChapter 3 - The Accounting Equation FinalEowyn DianaNo ratings yet

- Accounting - Self Study Guide For Staff of Micro Finance InstitutionsDocument9 pagesAccounting - Self Study Guide For Staff of Micro Finance Institutionsஆக்ஞா கிருஷ்ணா ஷர்மாNo ratings yet

- Module 3Document47 pagesModule 3Harrold HarryNo ratings yet

- Lesson 3 - AccountsDocument13 pagesLesson 3 - AccountsJeyem AscueNo ratings yet

- Types of Major Accounts PDFDocument14 pagesTypes of Major Accounts PDFDennis LacsonNo ratings yet

- Accounting 1 (SHS) - Week 6 - Accounting EquationDocument31 pagesAccounting 1 (SHS) - Week 6 - Accounting EquationAustin Capal Dela CruzNo ratings yet

- Accounting For Non-Accountant HandoutDocument26 pagesAccounting For Non-Accountant HandoutROMMUEL TOLENTINONo ratings yet

- Fundamentals of Accountancy, Business and Management 1: Learning Activity SheetDocument11 pagesFundamentals of Accountancy, Business and Management 1: Learning Activity SheetMarlyn LotivioNo ratings yet

- Learning Module 5 FarDocument11 pagesLearning Module 5 FarAira AbigailNo ratings yet

- Learning Module 5 FarDocument10 pagesLearning Module 5 FarAngelica SamboNo ratings yet

- Las 5 2S2QW4Document4 pagesLas 5 2S2QW4Luis UrsusNo ratings yet

- Fabm1 Grade-11 QTR1 Module4 Week-4Document6 pagesFabm1 Grade-11 QTR1 Module4 Week-4John anthony CasucoNo ratings yet

- Ass 2Document4 pagesAss 2CARMINA SANCHEZNo ratings yet

- ISR 111 - Chapter 6 MaterialsDocument14 pagesISR 111 - Chapter 6 MaterialsTrisha Nicole FajardoNo ratings yet

- Acctg. Ed 1 - Unit2 Module 4Document13 pagesAcctg. Ed 1 - Unit2 Module 4Angel Justine BernardoNo ratings yet

- EntrepreneurshipHandout Week 5Document6 pagesEntrepreneurshipHandout Week 5Pio GuiretNo ratings yet

- Economy ProfitDocument18 pagesEconomy ProfitVenkata Naresh KachhalaNo ratings yet

- Chapter 11 Bookkeeping EntrepDocument37 pagesChapter 11 Bookkeeping EntrepJacel GadonNo ratings yet

- Financial Acctg Reporting 1 Chapter 10Document18 pagesFinancial Acctg Reporting 1 Chapter 10Charise Jane ZullaNo ratings yet

- Elements of Financial Statements: AssetsDocument39 pagesElements of Financial Statements: AssetsEdna MingNo ratings yet

- Accounting Module 4 PDFDocument9 pagesAccounting Module 4 PDFMaria CristinaNo ratings yet

- Fundamentals of Accountancy, Business and Management 1Document25 pagesFundamentals of Accountancy, Business and Management 1Worship Songs / Choreo / LyricsNo ratings yet

- ChapterDocument47 pagesChapteralfyomar79No ratings yet

- Financial Accounting: PGP-1 June 2010Document29 pagesFinancial Accounting: PGP-1 June 2010Sukeerth ThodimaladinneNo ratings yet

- Accounting and FinanceDocument51 pagesAccounting and FinanceVIGNESH MBANo ratings yet

- 1 BSA WORKBOOK PS ServiceDocument37 pages1 BSA WORKBOOK PS ServiceFelicity ZodiacalNo ratings yet

- Q2Mod4TVEGrade10Entrep-BaesDacanayTalavera 1150BNAHS 250FBHS-CommonDocument10 pagesQ2Mod4TVEGrade10Entrep-BaesDacanayTalavera 1150BNAHS 250FBHS-CommonYato CreNo ratings yet

- Fabm2 - Summative Test 1Document2 pagesFabm2 - Summative Test 1Kyla AcyatanNo ratings yet

- Business ModelDocument29 pagesBusiness ModelTirsolito SalvadorNo ratings yet

- Accountancy: Shaheen Falcons Pu CollegeDocument13 pagesAccountancy: Shaheen Falcons Pu CollegeMohammed RayyanNo ratings yet

- Prepratory Material - AFMDocument39 pagesPrepratory Material - AFMRUTHVIK NETHANo ratings yet

- Module 001: Review of The Basic Accounting Concepts and PrinciplesDocument18 pagesModule 001: Review of The Basic Accounting Concepts and PrinciplesHo Ming LamNo ratings yet

- Accounting C2 Lesson 2 PDFDocument6 pagesAccounting C2 Lesson 2 PDFJake ShimNo ratings yet

- Chapter 4 Accounting Information SystemDocument3 pagesChapter 4 Accounting Information SystemFlordeliza HalogNo ratings yet

- Shs Fabm2 q3 Weeks 1 2 2ndreading Egs EditedfinalDocument20 pagesShs Fabm2 q3 Weeks 1 2 2ndreading Egs EditedfinalKrize Colene dela CruzNo ratings yet

- Exam Revision - 9 & 10 SolDocument7 pagesExam Revision - 9 & 10 SolNguyễn Minh ĐứcNo ratings yet

- Double Entry BookkeepingDocument23 pagesDouble Entry BookkeepingAhrian BenaNo ratings yet

- Part B: Computerised AccountingDocument6 pagesPart B: Computerised AccountingSonakshi JainNo ratings yet

- Why Do We Care About Revenue Recognition?: 15.514 2003 Session 4Document14 pagesWhy Do We Care About Revenue Recognition?: 15.514 2003 Session 4Veli NgwenyaNo ratings yet

- Basic Accounting For IT Part IIDocument4 pagesBasic Accounting For IT Part IImailbag6100% (1)

- Exam Revision - Chapter 9 10Document7 pagesExam Revision - Chapter 9 10Vũ Thị NgoanNo ratings yet

- Lec 4 NotesDocument14 pagesLec 4 NotesAhmed AltohamyNo ratings yet

- Financial Statements and Business DecisionsDocument37 pagesFinancial Statements and Business DecisionsHARMAN SINGHNo ratings yet

- 22 - AE - 111 - Module - 3 - Recording - Business - TransactionsDocument23 pages22 - AE - 111 - Module - 3 - Recording - Business - TransactionsEnrica BalladaresNo ratings yet

- Tutorial 1 - SsDocument3 pagesTutorial 1 - SsChigoziem OnyekawaNo ratings yet

- Basic AccountingDocument32 pagesBasic AccountinghectorbaladingNo ratings yet

- Supplementary 1 - Financial StatementsDocument21 pagesSupplementary 1 - Financial StatementsQuốc Khánh100% (1)

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- Payment HistoryDocument1 pagePayment HistoryRam KumarNo ratings yet

- Accounting 101 - Cash and Cash EquivalentsDocument2 pagesAccounting 101 - Cash and Cash EquivalentsNoah HNo ratings yet

- Consultancy Services For Technical Support Unit & Related Services Under BMWSS Project Technical ProposalDocument5 pagesConsultancy Services For Technical Support Unit & Related Services Under BMWSS Project Technical ProposalKohana RaggsNo ratings yet

- TC-20190629-0033 Tomy AdityaramaDocument1 pageTC-20190629-0033 Tomy AdityaramatommmmmmyNo ratings yet

- Consumer S Behaviour Regarding Cashless Payments During The Covid-19 PandemicDocument13 pagesConsumer S Behaviour Regarding Cashless Payments During The Covid-19 PandemicAesthetica MoonNo ratings yet

- Lecture 10 Cash and Internal Controls - NUS ACC1002 2020 SpringDocument24 pagesLecture 10 Cash and Internal Controls - NUS ACC1002 2020 SpringZenyuiNo ratings yet

- Financial Accounting Solution ch14Document23 pagesFinancial Accounting Solution ch14hw cNo ratings yet

- User Manual Oracle Banking Digital Experience Corporate Cash ManagementDocument36 pagesUser Manual Oracle Banking Digital Experience Corporate Cash ManagementpatienceNo ratings yet

- Basic Concepts of Guest Accounting - PT 2Document36 pagesBasic Concepts of Guest Accounting - PT 2Leonardo FloresNo ratings yet

- Co DLP English Grade 5 Q1Document5 pagesCo DLP English Grade 5 Q1cindymiranda810No ratings yet

- GABI@211Document22 pagesGABI@211princeaugust558No ratings yet

- Qdoc - Tips Internship Report On MCBDocument50 pagesQdoc - Tips Internship Report On MCBRaza AliNo ratings yet

- Sta Clara - Summary Part 1Document49 pagesSta Clara - Summary Part 1Carms St ClaireNo ratings yet

- Week 4 5 ULOb Lets Analyze Activity 1 SolutionDocument2 pagesWeek 4 5 ULOb Lets Analyze Activity 1 Solutionemem resuentoNo ratings yet

- Adnan AskariDocument72 pagesAdnan AskariFaisal AwanNo ratings yet

- Cash Management in SBI Effect On Their Customers .Docx (3) - 1 (3) (Repaired)Document75 pagesCash Management in SBI Effect On Their Customers .Docx (3) - 1 (3) (Repaired)anas khanNo ratings yet

- AIF Benchmarking - FAQsDocument10 pagesAIF Benchmarking - FAQsHarishNo ratings yet

- Audit of Cash and Marketable SecuritiesDocument21 pagesAudit of Cash and Marketable Securitiesዝምታ ተሻለNo ratings yet

- Act 110 Activity 4 (Answe Sheet - Dimalawang)Document2 pagesAct 110 Activity 4 (Answe Sheet - Dimalawang)Norkan DimalawangNo ratings yet

- Financial Management Class Part 2-KasetsartDocument66 pagesFinancial Management Class Part 2-KasetsartKong KrcNo ratings yet

- Chapter 11 Statement of Cash FlowsDocument4 pagesChapter 11 Statement of Cash FlowsEllen MaskariñoNo ratings yet

- Retail Teller Oracle FLEXCUBE Universal Banking Release 11.3.1.0.0EU (April) (2012) Oracle Part Number E51534-01Document45 pagesRetail Teller Oracle FLEXCUBE Universal Banking Release 11.3.1.0.0EU (April) (2012) Oracle Part Number E51534-01Omar AlgaddarNo ratings yet

- Assessmentscashmanagement DashanDocument16 pagesAssessmentscashmanagement Dashanhasenabdi30No ratings yet

- Demonetisation in IndiaDocument23 pagesDemonetisation in IndiaNITISH BHARDWAJNo ratings yet

- Error Correction Problem 1: Lord Gen A. Rilloraza, CPADocument5 pagesError Correction Problem 1: Lord Gen A. Rilloraza, CPAMae-shane SagayoNo ratings yet

- NPO Accounting Basis Tool V3Document39 pagesNPO Accounting Basis Tool V3Ipang NoyoNo ratings yet

- AIS615Document7 pagesAIS615Khamila NajwaNo ratings yet

- Bank Account Management - Cash PoolDocument10 pagesBank Account Management - Cash PoolDillip Kumar mallickNo ratings yet

- Teller - Transaction: Concept-Since The TELLER Application Will Be One and There Will Be Different Types of TransactionsDocument5 pagesTeller - Transaction: Concept-Since The TELLER Application Will Be One and There Will Be Different Types of TransactionsKamran MallickNo ratings yet

- Solved Discovered An Error in Computing A Commission Received Cash FromDocument1 pageSolved Discovered An Error in Computing A Commission Received Cash FromAnbu jaromiaNo ratings yet