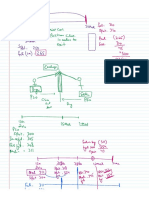

Consolidation Basics Solution

Consolidation Basics Solution

You might also like

- AKL Kel 8 - P5-1 P5-4 P5-8 - Eka NisrinaDocument8 pagesAKL Kel 8 - P5-1 P5-4 P5-8 - Eka NisrinaNur Ayu Mariya67% (3)

- Problems and Solutions Chapter 1 Advanced Accounting PDFDocument6 pagesProblems and Solutions Chapter 1 Advanced Accounting PDFMeera Khalil44% (9)

- Far410 - SS - Feb 2022Document9 pagesFar410 - SS - Feb 2022AFIZA JASMANNo ratings yet

- Summer Training ReportDocument11 pagesSummer Training ReportEncore GamingNo ratings yet

- Study Hub SECTION CDocument10 pagesStudy Hub SECTION Cgetcultured69No ratings yet

- Problem 1. The Balance Sheet of PX and SV Corporations at Year End 2007 AreDocument17 pagesProblem 1. The Balance Sheet of PX and SV Corporations at Year End 2007 AreMark Angelo BustosNo ratings yet

- Practice 6 Consolidated Statement One Year After AcquisitionDocument10 pagesPractice 6 Consolidated Statement One Year After AcquisitionGloria Lisa SusiloNo ratings yet

- Issued & Paid Up Capital: 14 Schedual of Fixed AssetsDocument6 pagesIssued & Paid Up Capital: 14 Schedual of Fixed AssetsShoukat KhaliqNo ratings yet

- Extra Session 3 (14 Oct 2022) Spreadsheet (CH 4)Document4 pagesExtra Session 3 (14 Oct 2022) Spreadsheet (CH 4)georgius gabrielNo ratings yet

- Book 1Document2 pagesBook 1Eman RehanNo ratings yet

- Consolidation (Study Hub)Document4 pagesConsolidation (Study Hub)HammadNo ratings yet

- Entry For The AcquisitionDocument5 pagesEntry For The AcquisitionEnalem OtsuepmeNo ratings yet

- Questionn 3-Dec 2018Document4 pagesQuestionn 3-Dec 2018GIROLYDIA EDDYNo ratings yet

- Exercise 5.3 (A)Document10 pagesExercise 5.3 (A)Stephanie XieNo ratings yet

- Problem 1 1. Record The Transactions To Account The Investment. P Corporation's BooksDocument2 pagesProblem 1 1. Record The Transactions To Account The Investment. P Corporation's BooksArtisanNo ratings yet

- FAR610 Consolidated Cashflow Past Semester FinalexamDocument18 pagesFAR610 Consolidated Cashflow Past Semester FinalexamANIS SYAKIRAH ADHWA MAHDILLAHNo ratings yet

- FR CH22 2023-24Document31 pagesFR CH22 2023-24ekambonga2No ratings yet

- Chap 13 - ProblemsDocument5 pagesChap 13 - ProblemsBuenaventura, Lara Jane T.No ratings yet

- Practice 2AssetAcquisitionDocument11 pagesPractice 2AssetAcquisitionEllen KokaliNo ratings yet

- Problem 3.1 - Financial Accounting With IFRS 4th Edition - UELDocument7 pagesProblem 3.1 - Financial Accounting With IFRS 4th Edition - UELChristyNo ratings yet

- Answer 4 - Excel For Diff. Acctg.Document42 pagesAnswer 4 - Excel For Diff. Acctg.Rheu ReyesNo ratings yet

- Practice 6 Consolidated Statement One Year After AcquisitionDocument12 pagesPractice 6 Consolidated Statement One Year After AcquisitionMario KaunangNo ratings yet

- S Man1 2008-2Document9 pagesS Man1 2008-2ExequielCamisaCrusperoNo ratings yet

- S1 SDocument7 pagesS1 SROHIT PANDEYNo ratings yet

- 5532 $FDocument1 page5532 $FSarahNo ratings yet

- Adv Acc 2 Sol Man 2008 BaysaDocument8 pagesAdv Acc 2 Sol Man 2008 BaysaNorman DelirioNo ratings yet

- Chapter 14 Business CombinationDocument5 pagesChapter 14 Business CombinationAshNor Randy0% (1)

- Preacquisition IncomeDocument39 pagesPreacquisition IncomeSentra SainsNo ratings yet

- B326 MTA REVISION Summer 2019 - Third UpdateDocument27 pagesB326 MTA REVISION Summer 2019 - Third UpdatemjlNo ratings yet

- Handout 1 Adjusting Entries Adjusted Trial Balance Financial Statements Answer KeyDocument3 pagesHandout 1 Adjusting Entries Adjusted Trial Balance Financial Statements Answer KeyKris Dela CruzNo ratings yet

- Conso FSDocument60 pagesConso FSAldrinNo ratings yet

- Chapter 4Document6 pagesChapter 4HelloWorldNowNo ratings yet

- Business Combination - EM Sample ProblemDocument32 pagesBusiness Combination - EM Sample ProblemJohn Stephen PendonNo ratings yet

- Tut 3Document5 pagesTut 3Đào Huyền Trang 4KT-20ACNNo ratings yet

- Profit and Loss Account For The Year Ended 31.03.2005: Expenditure Amt (RS.) Income Amt (RS.)Document2 pagesProfit and Loss Account For The Year Ended 31.03.2005: Expenditure Amt (RS.) Income Amt (RS.)Nayan NagdaNo ratings yet

- OLC Chap 5Document6 pagesOLC Chap 5Isha SinghNo ratings yet

- Working PaperDocument1 pageWorking PaperVina Rahma AuliyaNo ratings yet

- ACC132 MQ2 SolutionDocument4 pagesACC132 MQ2 SolutionRodNo ratings yet

- Consolidation and Equity Accounting - ExampleDocument12 pagesConsolidation and Equity Accounting - ExampleRobert lincolnNo ratings yet

- Cochin Marine FoodsDocument6 pagesCochin Marine Foodsmehtatushar2296No ratings yet

- UntitledDocument3 pagesUntitledKim VelascoNo ratings yet

- Consolidated SOFP - Kaplan Questions.Document33 pagesConsolidated SOFP - Kaplan Questions.husseinNo ratings yet

- 3.2 Acco 2100 Milagros MelecioDocument11 pages3.2 Acco 2100 Milagros MelecioDorisNo ratings yet

- Corrected Problem 3-5A Pitman CompanyDocument5 pagesCorrected Problem 3-5A Pitman CompanyCamron PetilloNo ratings yet

- Consolidation Q30Document5 pagesConsolidation Q30johny SahaNo ratings yet

- Journal Adjustment From Practice P3.2Document2 pagesJournal Adjustment From Practice P3.2Audrey Christabel KwekNo ratings yet

- Problem 1: Show Your CalculationsDocument14 pagesProblem 1: Show Your CalculationsMaria Christy WoworNo ratings yet

- Business CombinationDocument3 pagesBusiness CombinationNicoleNo ratings yet

- Book-Keeping ProceduresDocument21 pagesBook-Keeping ProceduresOilandGas IndependentProjectNo ratings yet

- BUSCOM ActivityDocument14 pagesBUSCOM ActivityLerma MarianoNo ratings yet

- Accounting Compeleting The CycleDocument14 pagesAccounting Compeleting The CyclecamilleNo ratings yet

- Accounting II-2Document177 pagesAccounting II-2Adnan KanwalNo ratings yet

- Assets 2018 2019 Forecast: Balance SheetDocument12 pagesAssets 2018 2019 Forecast: Balance SheetJosephAmparoNo ratings yet

- Parent Subsi Dr. CR.: Consolidated FS With Intercompany Sale of Inventory (Downstream and Upstream)Document6 pagesParent Subsi Dr. CR.: Consolidated FS With Intercompany Sale of Inventory (Downstream and Upstream)Reika OgaliscoNo ratings yet

- Pyq (Dec 2013)Document3 pagesPyq (Dec 2013)farah sofeaNo ratings yet

- 6273 - 21010126079 - Corporate Accounting 2Document15 pages6273 - 21010126079 - Corporate Accounting 2APURVA RANJANNo ratings yet

- Quiz No 2Document5 pagesQuiz No 2Aubrey AsioNo ratings yet

- Accounting Review-Activity 1 Answers 1. B. 2,200,000Document6 pagesAccounting Review-Activity 1 Answers 1. B. 2,200,000Junvy AbordoNo ratings yet

- Chapter 31Document7 pagesChapter 31AnonnNo ratings yet

- CACell Intermediate Account Full Book-201-250Document50 pagesCACell Intermediate Account Full Book-201-250kalyanikamineniNo ratings yet

- gdsmdpg2420084 enDocument24 pagesgdsmdpg2420084 enUmmar FarooqNo ratings yet

- Global Protocol Community Scale GHG Inventories GuidanceDocument136 pagesGlobal Protocol Community Scale GHG Inventories GuidanceUmmar FarooqNo ratings yet

- IAS 36 CA Final Solution Class WorkDocument14 pagesIAS 36 CA Final Solution Class WorkUmmar FarooqNo ratings yet

- IAS 36 4th Class 16 June NotingDocument6 pagesIAS 36 4th Class 16 June NotingUmmar FarooqNo ratings yet

- IAASB Public Interest Table Exposure Draft ISA 204 Mapping Key ChangesDocument28 pagesIAASB Public Interest Table Exposure Draft ISA 204 Mapping Key ChangesUmmar FarooqNo ratings yet

- ICAP Comments Proposed ISSA 5000 Sustainability Assurance (Final)Document10 pagesICAP Comments Proposed ISSA 5000 Sustainability Assurance (Final)Ummar FarooqNo ratings yet

- IAS 36 3rd Class 13 June NotingDocument4 pagesIAS 36 3rd Class 13 June NotingUmmar FarooqNo ratings yet

- Eps Ias 33 2019-1Document26 pagesEps Ias 33 2019-1Ummar FarooqNo ratings yet

- FAFR 1st Official Class IAS 36 10 June 2020 1Document4 pagesFAFR 1st Official Class IAS 36 10 June 2020 1Ummar FarooqNo ratings yet

- 20 Sept Futures Stock FutureDocument9 pages20 Sept Futures Stock FutureUmmar FarooqNo ratings yet

- 18 Sept Forex ForwardDocument6 pages18 Sept Forex ForwardUmmar FarooqNo ratings yet

- 19 Sept 2020 Money Market HedgeDocument5 pages19 Sept 2020 Money Market HedgeUmmar FarooqNo ratings yet

- 19 September MPV and FOH VariancesDocument3 pages19 September MPV and FOH VariancesUmmar FarooqNo ratings yet

- 18 Sept Standard CostingDocument3 pages18 Sept Standard CostingUmmar FarooqNo ratings yet

- Lecture Notes: ACCT6374 - Managerial Accounting & Strategic PlanningDocument30 pagesLecture Notes: ACCT6374 - Managerial Accounting & Strategic PlanningarisNo ratings yet

- QA Presentation PT KorinaDocument15 pagesQA Presentation PT KorinaFido Ananda HNo ratings yet

- CV of ABM Ikram UddinDocument3 pagesCV of ABM Ikram UddinIsmat Mesbah UddinNo ratings yet

- Mba IV Semester Seminar TopicsDocument3 pagesMba IV Semester Seminar Topicsmadhunish100% (1)

- ISA 600 MindMapDocument2 pagesISA 600 MindMapAli HaiderNo ratings yet

- Career Planning and Skills DevelopmentDocument22 pagesCareer Planning and Skills DevelopmentShazia TajNo ratings yet

- Purchase Order Template 02 - TemplateLabDocument1 pagePurchase Order Template 02 - TemplateLabMorning BellNo ratings yet

- Ketomac Mixy MotorsDocument11 pagesKetomac Mixy MotorsomkarnadkarniNo ratings yet

- Transcend 2.0 - Team Noodle - IIM LucknowDocument7 pagesTranscend 2.0 - Team Noodle - IIM LucknowPRONOY BIKASH PHUKONNo ratings yet

- Questionnare BookletDocument36 pagesQuestionnare BookletCaldito RockNo ratings yet

- Original For Recipient Duplicate For Transporter Triplicate For SupplierDocument1 pageOriginal For Recipient Duplicate For Transporter Triplicate For SupplierPraveen KumarNo ratings yet

- Ergon Modern Slavery Progress 2018 ResourceDocument22 pagesErgon Modern Slavery Progress 2018 ResourceJOSEPHINE CUMMITINGNo ratings yet

- Qualification Title: Professional Diploma in Strategic Management and Leadership Unit Title: Strategic ManagementDocument2 pagesQualification Title: Professional Diploma in Strategic Management and Leadership Unit Title: Strategic ManagementZun Pwint KyuNo ratings yet

- MuhiimDocument8 pagesMuhiimCOSOB BILANo ratings yet

- Module 5 Franchise Sales Assignments 2bac May 2023Document6 pagesModule 5 Franchise Sales Assignments 2bac May 2023Aaron OsmaNo ratings yet

- BCB F001 (IB) - Application Form For IBs - Feb 2022Document13 pagesBCB F001 (IB) - Application Form For IBs - Feb 2022vidyaNo ratings yet

- LivspaceDocument13 pagesLivspaceTanvi JuikarNo ratings yet

- MIKOL Company BriefDocument29 pagesMIKOL Company BriefGalecio MoraNo ratings yet

- B. Tenet Healthcare Corporation 2023 Q3 Earnings Presentation 20231030Document24 pagesB. Tenet Healthcare Corporation 2023 Q3 Earnings Presentation 20231030yoongie253No ratings yet

- Real Estate: Aiswarya M Ankita Sadani Ashish Yadhav Nikhil Mehta Tamal Mandal Simran ShaDocument12 pagesReal Estate: Aiswarya M Ankita Sadani Ashish Yadhav Nikhil Mehta Tamal Mandal Simran ShaDIVYANSHU SHEKHARNo ratings yet

- Mohammed Saabir CVDocument2 pagesMohammed Saabir CVsabirbdkNo ratings yet

- 200 PMBOK 6th Edition Practice QuestionsDocument86 pages200 PMBOK 6th Edition Practice Questionsmichelle garcia80% (5)

- Orange and Pink Trendy Gradient Student Part-Time Product Marketing Manager Resume PresentationDocument14 pagesOrange and Pink Trendy Gradient Student Part-Time Product Marketing Manager Resume PresentationAdinda Lita RachmanNo ratings yet

- University of Northern Philippines: College of Health SciencesDocument9 pagesUniversity of Northern Philippines: College of Health SciencesSheryl MaganNo ratings yet

- Business-English-Commom Words, PhrasesDocument2 pagesBusiness-English-Commom Words, PhrasesMaria MoralesNo ratings yet

- Pengaruh Fleksibilitas Budaya Dan Kerangka Levers of Control Terhadap Kinerja PerusahaanDocument16 pagesPengaruh Fleksibilitas Budaya Dan Kerangka Levers of Control Terhadap Kinerja PerusahaanTruz junkyuNo ratings yet

- Task 1 - ModelAnswerDocument2 pagesTask 1 - ModelAnswerAryanNo ratings yet

- R2301F PDF ENG CompressedDocument18 pagesR2301F PDF ENG CompressedMarioAbuyeresNo ratings yet

- Risk Assessment For VA MenlynDocument6 pagesRisk Assessment For VA MenlynVictor Thembinkosi MakhubeleNo ratings yet

Download as pdf or txt

You might also like

- AKL Kel 8 - P5-1 P5-4 P5-8 - Eka NisrinaDocument8 pagesAKL Kel 8 - P5-1 P5-4 P5-8 - Eka NisrinaNur Ayu Mariya67% (3)

- Problems and Solutions Chapter 1 Advanced Accounting PDFDocument6 pagesProblems and Solutions Chapter 1 Advanced Accounting PDFMeera Khalil44% (9)

- Far410 - SS - Feb 2022Document9 pagesFar410 - SS - Feb 2022AFIZA JASMANNo ratings yet

- Summer Training ReportDocument11 pagesSummer Training ReportEncore GamingNo ratings yet

- Study Hub SECTION CDocument10 pagesStudy Hub SECTION Cgetcultured69No ratings yet

- Problem 1. The Balance Sheet of PX and SV Corporations at Year End 2007 AreDocument17 pagesProblem 1. The Balance Sheet of PX and SV Corporations at Year End 2007 AreMark Angelo BustosNo ratings yet

- Practice 6 Consolidated Statement One Year After AcquisitionDocument10 pagesPractice 6 Consolidated Statement One Year After AcquisitionGloria Lisa SusiloNo ratings yet

- Issued & Paid Up Capital: 14 Schedual of Fixed AssetsDocument6 pagesIssued & Paid Up Capital: 14 Schedual of Fixed AssetsShoukat KhaliqNo ratings yet

- Extra Session 3 (14 Oct 2022) Spreadsheet (CH 4)Document4 pagesExtra Session 3 (14 Oct 2022) Spreadsheet (CH 4)georgius gabrielNo ratings yet

- Book 1Document2 pagesBook 1Eman RehanNo ratings yet

- Consolidation (Study Hub)Document4 pagesConsolidation (Study Hub)HammadNo ratings yet

- Entry For The AcquisitionDocument5 pagesEntry For The AcquisitionEnalem OtsuepmeNo ratings yet

- Questionn 3-Dec 2018Document4 pagesQuestionn 3-Dec 2018GIROLYDIA EDDYNo ratings yet

- Exercise 5.3 (A)Document10 pagesExercise 5.3 (A)Stephanie XieNo ratings yet

- Problem 1 1. Record The Transactions To Account The Investment. P Corporation's BooksDocument2 pagesProblem 1 1. Record The Transactions To Account The Investment. P Corporation's BooksArtisanNo ratings yet

- FAR610 Consolidated Cashflow Past Semester FinalexamDocument18 pagesFAR610 Consolidated Cashflow Past Semester FinalexamANIS SYAKIRAH ADHWA MAHDILLAHNo ratings yet

- FR CH22 2023-24Document31 pagesFR CH22 2023-24ekambonga2No ratings yet

- Chap 13 - ProblemsDocument5 pagesChap 13 - ProblemsBuenaventura, Lara Jane T.No ratings yet

- Practice 2AssetAcquisitionDocument11 pagesPractice 2AssetAcquisitionEllen KokaliNo ratings yet

- Problem 3.1 - Financial Accounting With IFRS 4th Edition - UELDocument7 pagesProblem 3.1 - Financial Accounting With IFRS 4th Edition - UELChristyNo ratings yet

- Answer 4 - Excel For Diff. Acctg.Document42 pagesAnswer 4 - Excel For Diff. Acctg.Rheu ReyesNo ratings yet

- Practice 6 Consolidated Statement One Year After AcquisitionDocument12 pagesPractice 6 Consolidated Statement One Year After AcquisitionMario KaunangNo ratings yet

- S Man1 2008-2Document9 pagesS Man1 2008-2ExequielCamisaCrusperoNo ratings yet

- S1 SDocument7 pagesS1 SROHIT PANDEYNo ratings yet

- 5532 $FDocument1 page5532 $FSarahNo ratings yet

- Adv Acc 2 Sol Man 2008 BaysaDocument8 pagesAdv Acc 2 Sol Man 2008 BaysaNorman DelirioNo ratings yet

- Chapter 14 Business CombinationDocument5 pagesChapter 14 Business CombinationAshNor Randy0% (1)

- Preacquisition IncomeDocument39 pagesPreacquisition IncomeSentra SainsNo ratings yet

- B326 MTA REVISION Summer 2019 - Third UpdateDocument27 pagesB326 MTA REVISION Summer 2019 - Third UpdatemjlNo ratings yet

- Handout 1 Adjusting Entries Adjusted Trial Balance Financial Statements Answer KeyDocument3 pagesHandout 1 Adjusting Entries Adjusted Trial Balance Financial Statements Answer KeyKris Dela CruzNo ratings yet

- Conso FSDocument60 pagesConso FSAldrinNo ratings yet

- Chapter 4Document6 pagesChapter 4HelloWorldNowNo ratings yet

- Business Combination - EM Sample ProblemDocument32 pagesBusiness Combination - EM Sample ProblemJohn Stephen PendonNo ratings yet

- Tut 3Document5 pagesTut 3Đào Huyền Trang 4KT-20ACNNo ratings yet

- Profit and Loss Account For The Year Ended 31.03.2005: Expenditure Amt (RS.) Income Amt (RS.)Document2 pagesProfit and Loss Account For The Year Ended 31.03.2005: Expenditure Amt (RS.) Income Amt (RS.)Nayan NagdaNo ratings yet

- OLC Chap 5Document6 pagesOLC Chap 5Isha SinghNo ratings yet

- Working PaperDocument1 pageWorking PaperVina Rahma AuliyaNo ratings yet

- ACC132 MQ2 SolutionDocument4 pagesACC132 MQ2 SolutionRodNo ratings yet

- Consolidation and Equity Accounting - ExampleDocument12 pagesConsolidation and Equity Accounting - ExampleRobert lincolnNo ratings yet

- Cochin Marine FoodsDocument6 pagesCochin Marine Foodsmehtatushar2296No ratings yet

- UntitledDocument3 pagesUntitledKim VelascoNo ratings yet

- Consolidated SOFP - Kaplan Questions.Document33 pagesConsolidated SOFP - Kaplan Questions.husseinNo ratings yet

- 3.2 Acco 2100 Milagros MelecioDocument11 pages3.2 Acco 2100 Milagros MelecioDorisNo ratings yet

- Corrected Problem 3-5A Pitman CompanyDocument5 pagesCorrected Problem 3-5A Pitman CompanyCamron PetilloNo ratings yet

- Consolidation Q30Document5 pagesConsolidation Q30johny SahaNo ratings yet

- Journal Adjustment From Practice P3.2Document2 pagesJournal Adjustment From Practice P3.2Audrey Christabel KwekNo ratings yet

- Problem 1: Show Your CalculationsDocument14 pagesProblem 1: Show Your CalculationsMaria Christy WoworNo ratings yet

- Business CombinationDocument3 pagesBusiness CombinationNicoleNo ratings yet

- Book-Keeping ProceduresDocument21 pagesBook-Keeping ProceduresOilandGas IndependentProjectNo ratings yet

- BUSCOM ActivityDocument14 pagesBUSCOM ActivityLerma MarianoNo ratings yet

- Accounting Compeleting The CycleDocument14 pagesAccounting Compeleting The CyclecamilleNo ratings yet

- Accounting II-2Document177 pagesAccounting II-2Adnan KanwalNo ratings yet

- Assets 2018 2019 Forecast: Balance SheetDocument12 pagesAssets 2018 2019 Forecast: Balance SheetJosephAmparoNo ratings yet

- Parent Subsi Dr. CR.: Consolidated FS With Intercompany Sale of Inventory (Downstream and Upstream)Document6 pagesParent Subsi Dr. CR.: Consolidated FS With Intercompany Sale of Inventory (Downstream and Upstream)Reika OgaliscoNo ratings yet

- Pyq (Dec 2013)Document3 pagesPyq (Dec 2013)farah sofeaNo ratings yet

- 6273 - 21010126079 - Corporate Accounting 2Document15 pages6273 - 21010126079 - Corporate Accounting 2APURVA RANJANNo ratings yet

- Quiz No 2Document5 pagesQuiz No 2Aubrey AsioNo ratings yet

- Accounting Review-Activity 1 Answers 1. B. 2,200,000Document6 pagesAccounting Review-Activity 1 Answers 1. B. 2,200,000Junvy AbordoNo ratings yet

- Chapter 31Document7 pagesChapter 31AnonnNo ratings yet

- CACell Intermediate Account Full Book-201-250Document50 pagesCACell Intermediate Account Full Book-201-250kalyanikamineniNo ratings yet

- gdsmdpg2420084 enDocument24 pagesgdsmdpg2420084 enUmmar FarooqNo ratings yet

- Global Protocol Community Scale GHG Inventories GuidanceDocument136 pagesGlobal Protocol Community Scale GHG Inventories GuidanceUmmar FarooqNo ratings yet

- IAS 36 CA Final Solution Class WorkDocument14 pagesIAS 36 CA Final Solution Class WorkUmmar FarooqNo ratings yet

- IAS 36 4th Class 16 June NotingDocument6 pagesIAS 36 4th Class 16 June NotingUmmar FarooqNo ratings yet

- IAASB Public Interest Table Exposure Draft ISA 204 Mapping Key ChangesDocument28 pagesIAASB Public Interest Table Exposure Draft ISA 204 Mapping Key ChangesUmmar FarooqNo ratings yet

- ICAP Comments Proposed ISSA 5000 Sustainability Assurance (Final)Document10 pagesICAP Comments Proposed ISSA 5000 Sustainability Assurance (Final)Ummar FarooqNo ratings yet

- IAS 36 3rd Class 13 June NotingDocument4 pagesIAS 36 3rd Class 13 June NotingUmmar FarooqNo ratings yet

- Eps Ias 33 2019-1Document26 pagesEps Ias 33 2019-1Ummar FarooqNo ratings yet

- FAFR 1st Official Class IAS 36 10 June 2020 1Document4 pagesFAFR 1st Official Class IAS 36 10 June 2020 1Ummar FarooqNo ratings yet

- 20 Sept Futures Stock FutureDocument9 pages20 Sept Futures Stock FutureUmmar FarooqNo ratings yet

- 18 Sept Forex ForwardDocument6 pages18 Sept Forex ForwardUmmar FarooqNo ratings yet

- 19 Sept 2020 Money Market HedgeDocument5 pages19 Sept 2020 Money Market HedgeUmmar FarooqNo ratings yet

- 19 September MPV and FOH VariancesDocument3 pages19 September MPV and FOH VariancesUmmar FarooqNo ratings yet

- 18 Sept Standard CostingDocument3 pages18 Sept Standard CostingUmmar FarooqNo ratings yet

- Lecture Notes: ACCT6374 - Managerial Accounting & Strategic PlanningDocument30 pagesLecture Notes: ACCT6374 - Managerial Accounting & Strategic PlanningarisNo ratings yet

- QA Presentation PT KorinaDocument15 pagesQA Presentation PT KorinaFido Ananda HNo ratings yet

- CV of ABM Ikram UddinDocument3 pagesCV of ABM Ikram UddinIsmat Mesbah UddinNo ratings yet

- Mba IV Semester Seminar TopicsDocument3 pagesMba IV Semester Seminar Topicsmadhunish100% (1)

- ISA 600 MindMapDocument2 pagesISA 600 MindMapAli HaiderNo ratings yet

- Career Planning and Skills DevelopmentDocument22 pagesCareer Planning and Skills DevelopmentShazia TajNo ratings yet

- Purchase Order Template 02 - TemplateLabDocument1 pagePurchase Order Template 02 - TemplateLabMorning BellNo ratings yet

- Ketomac Mixy MotorsDocument11 pagesKetomac Mixy MotorsomkarnadkarniNo ratings yet

- Transcend 2.0 - Team Noodle - IIM LucknowDocument7 pagesTranscend 2.0 - Team Noodle - IIM LucknowPRONOY BIKASH PHUKONNo ratings yet

- Questionnare BookletDocument36 pagesQuestionnare BookletCaldito RockNo ratings yet

- Original For Recipient Duplicate For Transporter Triplicate For SupplierDocument1 pageOriginal For Recipient Duplicate For Transporter Triplicate For SupplierPraveen KumarNo ratings yet

- Ergon Modern Slavery Progress 2018 ResourceDocument22 pagesErgon Modern Slavery Progress 2018 ResourceJOSEPHINE CUMMITINGNo ratings yet

- Qualification Title: Professional Diploma in Strategic Management and Leadership Unit Title: Strategic ManagementDocument2 pagesQualification Title: Professional Diploma in Strategic Management and Leadership Unit Title: Strategic ManagementZun Pwint KyuNo ratings yet

- MuhiimDocument8 pagesMuhiimCOSOB BILANo ratings yet

- Module 5 Franchise Sales Assignments 2bac May 2023Document6 pagesModule 5 Franchise Sales Assignments 2bac May 2023Aaron OsmaNo ratings yet

- BCB F001 (IB) - Application Form For IBs - Feb 2022Document13 pagesBCB F001 (IB) - Application Form For IBs - Feb 2022vidyaNo ratings yet

- LivspaceDocument13 pagesLivspaceTanvi JuikarNo ratings yet

- MIKOL Company BriefDocument29 pagesMIKOL Company BriefGalecio MoraNo ratings yet

- B. Tenet Healthcare Corporation 2023 Q3 Earnings Presentation 20231030Document24 pagesB. Tenet Healthcare Corporation 2023 Q3 Earnings Presentation 20231030yoongie253No ratings yet

- Real Estate: Aiswarya M Ankita Sadani Ashish Yadhav Nikhil Mehta Tamal Mandal Simran ShaDocument12 pagesReal Estate: Aiswarya M Ankita Sadani Ashish Yadhav Nikhil Mehta Tamal Mandal Simran ShaDIVYANSHU SHEKHARNo ratings yet

- Mohammed Saabir CVDocument2 pagesMohammed Saabir CVsabirbdkNo ratings yet

- 200 PMBOK 6th Edition Practice QuestionsDocument86 pages200 PMBOK 6th Edition Practice Questionsmichelle garcia80% (5)

- Orange and Pink Trendy Gradient Student Part-Time Product Marketing Manager Resume PresentationDocument14 pagesOrange and Pink Trendy Gradient Student Part-Time Product Marketing Manager Resume PresentationAdinda Lita RachmanNo ratings yet

- University of Northern Philippines: College of Health SciencesDocument9 pagesUniversity of Northern Philippines: College of Health SciencesSheryl MaganNo ratings yet

- Business-English-Commom Words, PhrasesDocument2 pagesBusiness-English-Commom Words, PhrasesMaria MoralesNo ratings yet

- Pengaruh Fleksibilitas Budaya Dan Kerangka Levers of Control Terhadap Kinerja PerusahaanDocument16 pagesPengaruh Fleksibilitas Budaya Dan Kerangka Levers of Control Terhadap Kinerja PerusahaanTruz junkyuNo ratings yet

- Task 1 - ModelAnswerDocument2 pagesTask 1 - ModelAnswerAryanNo ratings yet

- R2301F PDF ENG CompressedDocument18 pagesR2301F PDF ENG CompressedMarioAbuyeresNo ratings yet

- Risk Assessment For VA MenlynDocument6 pagesRisk Assessment For VA MenlynVictor Thembinkosi MakhubeleNo ratings yet