Cours 4

Cours 4

You might also like

- Comprehensive Finance Cheat Sheet Collection 1698244606Document52 pagesComprehensive Finance Cheat Sheet Collection 1698244606muratgreywolf100% (1)

- CFA一级基础段衍生 Tom 打印版Document38 pagesCFA一级基础段衍生 Tom 打印版Evelyn YangNo ratings yet

- Discount RateDocument9 pagesDiscount RateNguyễn PhúcNo ratings yet

- Fra PDFDocument27 pagesFra PDFNeeraj KumarNo ratings yet

- BNP Paribas in Italy: Developing Our Second Domestic MarketDocument30 pagesBNP Paribas in Italy: Developing Our Second Domestic MarketAlezNgNo ratings yet

- Investment Banking ExcelDocument28 pagesInvestment Banking ExcelJohn ChiwaiNo ratings yet

- IFRS 17 For General InsurersDocument23 pagesIFRS 17 For General InsurersbaraalqasemNo ratings yet

- IFRS Vs US GAAP - 2024Document8 pagesIFRS Vs US GAAP - 2024AMARTYA KUMAR DAS PGP 2023-25 BatchNo ratings yet

- The Capm: Dong Lou London School of Economics LSE Summer SchoolDocument39 pagesThe Capm: Dong Lou London School of Economics LSE Summer SchoolAryan PandeyNo ratings yet

- Economic Value AddedDocument25 pagesEconomic Value AddedSagar KansalNo ratings yet

- NSE - National Stock Exchange of India LTD PDFDocument2 pagesNSE - National Stock Exchange of India LTD PDFChittaNo ratings yet

- Trader Vic IntroDocument12 pagesTrader Vic Intromatrixit0% (1)

- Konnor George MKT 487-002 Clean Edge Razor Written Case Dr. Houston March 11, 2016Document16 pagesKonnor George MKT 487-002 Clean Edge Razor Written Case Dr. Houston March 11, 2016Sunil KumarNo ratings yet

- Fund Profile: Field NameDocument1 pageFund Profile: Field NameJang CoiNo ratings yet

- MENA Inventory 2Document77 pagesMENA Inventory 2Vladyslav KalchevskiiNo ratings yet

- Accounting For DerivativesDocument42 pagesAccounting For DerivativesSanath Fernando100% (1)

- Distress PDFDocument65 pagesDistress PDFKhushal UpraityNo ratings yet

- Merus LabsDocument20 pagesMerus LabsJenny QuachNo ratings yet

- 4 - 1-A Macro Risk-Based Approach - J-TeiletcheDocument19 pages4 - 1-A Macro Risk-Based Approach - J-TeiletcheLoulou DePanamNo ratings yet

- Financial Statement Analysis and Security Valuation: - October 19, 2022 Arnt VerriestDocument62 pagesFinancial Statement Analysis and Security Valuation: - October 19, 2022 Arnt VerriestfelipeNo ratings yet

- Two Prime Institutional Investment GuideDocument31 pagesTwo Prime Institutional Investment GuideFabioNo ratings yet

- An Agile Arman: Q3 & 9M FY23 Investor PresentationDocument40 pagesAn Agile Arman: Q3 & 9M FY23 Investor PresentationNimesh PatelNo ratings yet

- ABN - Structured Rate ManualDocument35 pagesABN - Structured Rate Manuallulunese100% (2)

- Transformation Strategy Update: UBS Sydney Investor Session Presentation 18 March 2021Document34 pagesTransformation Strategy Update: UBS Sydney Investor Session Presentation 18 March 2021joel enciso enekeNo ratings yet

- CPF Performance and Risk Monitoring Report Q4 08Document38 pagesCPF Performance and Risk Monitoring Report Q4 08System AdministratorNo ratings yet

- Types of Financial Instrument: Corporate Financial Strategy 4th Edition DR Ruth BenderDocument16 pagesTypes of Financial Instrument: Corporate Financial Strategy 4th Edition DR Ruth BenderAin roseNo ratings yet

- PDF - Unpacking LRC and LIC Calculations For PC InsurersDocument14 pagesPDF - Unpacking LRC and LIC Calculations For PC Insurersnod32_1206No ratings yet

- Portafolio Management - Versión 2Document98 pagesPortafolio Management - Versión 2sebastiam10mNo ratings yet

- IFRS Vs US GAAPDocument8 pagesIFRS Vs US GAAPArpit MaheshwariNo ratings yet

- Corporate Sustainability: Jane Okun Bomba Chief Sustainability, IR and Comms Officer IHS Inc. February 2014Document24 pagesCorporate Sustainability: Jane Okun Bomba Chief Sustainability, IR and Comms Officer IHS Inc. February 2014ReveJoyNo ratings yet

- Top Down Goals 5Document53 pagesTop Down Goals 5Sylvia VhetiNo ratings yet

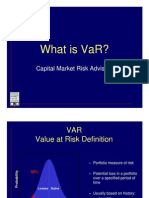

- What Is VaRDocument10 pagesWhat Is VaRjosephmeawadNo ratings yet

- Chapter 18 Valuation Closing ThoughtsDocument18 pagesChapter 18 Valuation Closing ThoughtsdemelashNo ratings yet

- Total Return Futures On Cac 40 PresentationDocument17 pagesTotal Return Futures On Cac 40 Presentationouattara dabilaNo ratings yet

- CH 02Document13 pagesCH 02Praveen BVSNo ratings yet

- Invest Oct 2022Document521 pagesInvest Oct 2022the kingfishNo ratings yet

- Lecture 3Document44 pagesLecture 3felipeNo ratings yet

- Ultimate Pivot Points™ - User GuideDocument26 pagesUltimate Pivot Points™ - User GuideAakaarNirakaar100% (1)

- PY19 Program Service ProviderDocument10 pagesPY19 Program Service ProviderMario LuizNo ratings yet

- Company Presentation - April - 2024Document51 pagesCompany Presentation - April - 2024koteshchoudaryNo ratings yet

- Brent Crude Front Month: Main CharacteristicsDocument2 pagesBrent Crude Front Month: Main CharacteristicsPaolo ScafettaNo ratings yet

- STRACOSMAN - Chapter 6Document6 pagesSTRACOSMAN - Chapter 6Rae WorksNo ratings yet

- Relative ValuationDocument59 pagesRelative ValuationAndre RobineNo ratings yet

- Class 5Document20 pagesClass 5nga.lehongNo ratings yet

- FRTB Standardised ApproachDocument14 pagesFRTB Standardised ApproachAlex YangNo ratings yet

- The Cost of MoneyDocument34 pagesThe Cost of Moneymarine19.vedelNo ratings yet

- What Is IFRS?: 2009 & Earlier 2010 2011 2012 No AdoptionDocument5 pagesWhat Is IFRS?: 2009 & Earlier 2010 2011 2012 No AdoptionArsal AliNo ratings yet

- CMSA Role-Based Learning PathsDocument3 pagesCMSA Role-Based Learning PathsPallav DaruNo ratings yet

- Refinitiv WebinarDocument16 pagesRefinitiv WebinarOthman Sou100% (1)

- Yield Curve Spread Trades PDFDocument12 pagesYield Curve Spread Trades PDFNicoLaza100% (1)

- ValuationDocument37 pagesValuationDivyam AgarwalNo ratings yet

- OneSumX - IFRS 9 BrochureDocument2 pagesOneSumX - IFRS 9 BrochureMauroNo ratings yet

- Volatility Risk Premium and Financial Distress: August 2016Document12 pagesVolatility Risk Premium and Financial Distress: August 2016DrNaveed Ul HaqNo ratings yet

- Session 1Document10 pagesSession 1rafat.jalladNo ratings yet

- Business Case EjDocument17 pagesBusiness Case EjgermanaramayoNo ratings yet

- Session 8Document30 pagesSession 8Aman VarshneyNo ratings yet

- Re1556954 PPT 16x9 V3libortransitionDocument26 pagesRe1556954 PPT 16x9 V3libortransitionLuiz LopesNo ratings yet

- How to Select Investment Managers and Evaluate Performance: A Guide for Pension Funds, Endowments, Foundations, and TrustsFrom EverandHow to Select Investment Managers and Evaluate Performance: A Guide for Pension Funds, Endowments, Foundations, and TrustsNo ratings yet

- Alternative Thinking Tail Hedging StrategiesDocument8 pagesAlternative Thinking Tail Hedging StrategiesSiddhartha Prabakar NadathurNo ratings yet

- An Explanation of Equity Drawdown and Maximum DrawdownDocument8 pagesAn Explanation of Equity Drawdown and Maximum DrawdownmghugaradareNo ratings yet

- Tail Hedging Strategies: Issam S. S The Cambridge Strategy (Asset Management) LTDDocument26 pagesTail Hedging Strategies: Issam S. S The Cambridge Strategy (Asset Management) LTDMatt EbrahimiNo ratings yet

- ING Group 2Document4 pagesING Group 2Puneet JainNo ratings yet

- Cours 4Document26 pagesCours 4axel.merlin2000No ratings yet

- Logica Capital PresentationDocument25 pagesLogica Capital PresentationjustinerocksNo ratings yet

- How To Trade Price ActionDocument44 pagesHow To Trade Price ActionHanuman SaiGupta100% (2)

- Journal of Financial Economics: Vikas Agarwal, Stefan Ruenzi, Florian WeigertDocument27 pagesJournal of Financial Economics: Vikas Agarwal, Stefan Ruenzi, Florian WeigertJuliana TessariNo ratings yet

- Nations TailDex Tail Risk IndexesDocument2 pagesNations TailDex Tail Risk IndexesEmanuele QuagliaNo ratings yet

- 00K - Antifragile Asset Allocation Model - GioeleGiordano - 1st PlaceDocument19 pages00K - Antifragile Asset Allocation Model - GioeleGiordano - 1st Placenaren.bansalNo ratings yet

- Normal DistributionDocument23 pagesNormal Distributionlemuel sardualNo ratings yet

- SSRN Id4378071Document24 pagesSSRN Id4378071AlexNo ratings yet

Download as pdf or txt

You might also like

- Comprehensive Finance Cheat Sheet Collection 1698244606Document52 pagesComprehensive Finance Cheat Sheet Collection 1698244606muratgreywolf100% (1)

- CFA一级基础段衍生 Tom 打印版Document38 pagesCFA一级基础段衍生 Tom 打印版Evelyn YangNo ratings yet

- Discount RateDocument9 pagesDiscount RateNguyễn PhúcNo ratings yet

- Fra PDFDocument27 pagesFra PDFNeeraj KumarNo ratings yet

- BNP Paribas in Italy: Developing Our Second Domestic MarketDocument30 pagesBNP Paribas in Italy: Developing Our Second Domestic MarketAlezNgNo ratings yet

- Investment Banking ExcelDocument28 pagesInvestment Banking ExcelJohn ChiwaiNo ratings yet

- IFRS 17 For General InsurersDocument23 pagesIFRS 17 For General InsurersbaraalqasemNo ratings yet

- IFRS Vs US GAAP - 2024Document8 pagesIFRS Vs US GAAP - 2024AMARTYA KUMAR DAS PGP 2023-25 BatchNo ratings yet

- The Capm: Dong Lou London School of Economics LSE Summer SchoolDocument39 pagesThe Capm: Dong Lou London School of Economics LSE Summer SchoolAryan PandeyNo ratings yet

- Economic Value AddedDocument25 pagesEconomic Value AddedSagar KansalNo ratings yet

- NSE - National Stock Exchange of India LTD PDFDocument2 pagesNSE - National Stock Exchange of India LTD PDFChittaNo ratings yet

- Trader Vic IntroDocument12 pagesTrader Vic Intromatrixit0% (1)

- Konnor George MKT 487-002 Clean Edge Razor Written Case Dr. Houston March 11, 2016Document16 pagesKonnor George MKT 487-002 Clean Edge Razor Written Case Dr. Houston March 11, 2016Sunil KumarNo ratings yet

- Fund Profile: Field NameDocument1 pageFund Profile: Field NameJang CoiNo ratings yet

- MENA Inventory 2Document77 pagesMENA Inventory 2Vladyslav KalchevskiiNo ratings yet

- Accounting For DerivativesDocument42 pagesAccounting For DerivativesSanath Fernando100% (1)

- Distress PDFDocument65 pagesDistress PDFKhushal UpraityNo ratings yet

- Merus LabsDocument20 pagesMerus LabsJenny QuachNo ratings yet

- 4 - 1-A Macro Risk-Based Approach - J-TeiletcheDocument19 pages4 - 1-A Macro Risk-Based Approach - J-TeiletcheLoulou DePanamNo ratings yet

- Financial Statement Analysis and Security Valuation: - October 19, 2022 Arnt VerriestDocument62 pagesFinancial Statement Analysis and Security Valuation: - October 19, 2022 Arnt VerriestfelipeNo ratings yet

- Two Prime Institutional Investment GuideDocument31 pagesTwo Prime Institutional Investment GuideFabioNo ratings yet

- An Agile Arman: Q3 & 9M FY23 Investor PresentationDocument40 pagesAn Agile Arman: Q3 & 9M FY23 Investor PresentationNimesh PatelNo ratings yet

- ABN - Structured Rate ManualDocument35 pagesABN - Structured Rate Manuallulunese100% (2)

- Transformation Strategy Update: UBS Sydney Investor Session Presentation 18 March 2021Document34 pagesTransformation Strategy Update: UBS Sydney Investor Session Presentation 18 March 2021joel enciso enekeNo ratings yet

- CPF Performance and Risk Monitoring Report Q4 08Document38 pagesCPF Performance and Risk Monitoring Report Q4 08System AdministratorNo ratings yet

- Types of Financial Instrument: Corporate Financial Strategy 4th Edition DR Ruth BenderDocument16 pagesTypes of Financial Instrument: Corporate Financial Strategy 4th Edition DR Ruth BenderAin roseNo ratings yet

- PDF - Unpacking LRC and LIC Calculations For PC InsurersDocument14 pagesPDF - Unpacking LRC and LIC Calculations For PC Insurersnod32_1206No ratings yet

- Portafolio Management - Versión 2Document98 pagesPortafolio Management - Versión 2sebastiam10mNo ratings yet

- IFRS Vs US GAAPDocument8 pagesIFRS Vs US GAAPArpit MaheshwariNo ratings yet

- Corporate Sustainability: Jane Okun Bomba Chief Sustainability, IR and Comms Officer IHS Inc. February 2014Document24 pagesCorporate Sustainability: Jane Okun Bomba Chief Sustainability, IR and Comms Officer IHS Inc. February 2014ReveJoyNo ratings yet

- Top Down Goals 5Document53 pagesTop Down Goals 5Sylvia VhetiNo ratings yet

- What Is VaRDocument10 pagesWhat Is VaRjosephmeawadNo ratings yet

- Chapter 18 Valuation Closing ThoughtsDocument18 pagesChapter 18 Valuation Closing ThoughtsdemelashNo ratings yet

- Total Return Futures On Cac 40 PresentationDocument17 pagesTotal Return Futures On Cac 40 Presentationouattara dabilaNo ratings yet

- CH 02Document13 pagesCH 02Praveen BVSNo ratings yet

- Invest Oct 2022Document521 pagesInvest Oct 2022the kingfishNo ratings yet

- Lecture 3Document44 pagesLecture 3felipeNo ratings yet

- Ultimate Pivot Points™ - User GuideDocument26 pagesUltimate Pivot Points™ - User GuideAakaarNirakaar100% (1)

- PY19 Program Service ProviderDocument10 pagesPY19 Program Service ProviderMario LuizNo ratings yet

- Company Presentation - April - 2024Document51 pagesCompany Presentation - April - 2024koteshchoudaryNo ratings yet

- Brent Crude Front Month: Main CharacteristicsDocument2 pagesBrent Crude Front Month: Main CharacteristicsPaolo ScafettaNo ratings yet

- STRACOSMAN - Chapter 6Document6 pagesSTRACOSMAN - Chapter 6Rae WorksNo ratings yet

- Relative ValuationDocument59 pagesRelative ValuationAndre RobineNo ratings yet

- Class 5Document20 pagesClass 5nga.lehongNo ratings yet

- FRTB Standardised ApproachDocument14 pagesFRTB Standardised ApproachAlex YangNo ratings yet

- The Cost of MoneyDocument34 pagesThe Cost of Moneymarine19.vedelNo ratings yet

- What Is IFRS?: 2009 & Earlier 2010 2011 2012 No AdoptionDocument5 pagesWhat Is IFRS?: 2009 & Earlier 2010 2011 2012 No AdoptionArsal AliNo ratings yet

- CMSA Role-Based Learning PathsDocument3 pagesCMSA Role-Based Learning PathsPallav DaruNo ratings yet

- Refinitiv WebinarDocument16 pagesRefinitiv WebinarOthman Sou100% (1)

- Yield Curve Spread Trades PDFDocument12 pagesYield Curve Spread Trades PDFNicoLaza100% (1)

- ValuationDocument37 pagesValuationDivyam AgarwalNo ratings yet

- OneSumX - IFRS 9 BrochureDocument2 pagesOneSumX - IFRS 9 BrochureMauroNo ratings yet

- Volatility Risk Premium and Financial Distress: August 2016Document12 pagesVolatility Risk Premium and Financial Distress: August 2016DrNaveed Ul HaqNo ratings yet

- Session 1Document10 pagesSession 1rafat.jalladNo ratings yet

- Business Case EjDocument17 pagesBusiness Case EjgermanaramayoNo ratings yet

- Session 8Document30 pagesSession 8Aman VarshneyNo ratings yet

- Re1556954 PPT 16x9 V3libortransitionDocument26 pagesRe1556954 PPT 16x9 V3libortransitionLuiz LopesNo ratings yet

- How to Select Investment Managers and Evaluate Performance: A Guide for Pension Funds, Endowments, Foundations, and TrustsFrom EverandHow to Select Investment Managers and Evaluate Performance: A Guide for Pension Funds, Endowments, Foundations, and TrustsNo ratings yet

- Alternative Thinking Tail Hedging StrategiesDocument8 pagesAlternative Thinking Tail Hedging StrategiesSiddhartha Prabakar NadathurNo ratings yet

- An Explanation of Equity Drawdown and Maximum DrawdownDocument8 pagesAn Explanation of Equity Drawdown and Maximum DrawdownmghugaradareNo ratings yet

- Tail Hedging Strategies: Issam S. S The Cambridge Strategy (Asset Management) LTDDocument26 pagesTail Hedging Strategies: Issam S. S The Cambridge Strategy (Asset Management) LTDMatt EbrahimiNo ratings yet

- ING Group 2Document4 pagesING Group 2Puneet JainNo ratings yet

- Cours 4Document26 pagesCours 4axel.merlin2000No ratings yet

- Logica Capital PresentationDocument25 pagesLogica Capital PresentationjustinerocksNo ratings yet

- How To Trade Price ActionDocument44 pagesHow To Trade Price ActionHanuman SaiGupta100% (2)

- Journal of Financial Economics: Vikas Agarwal, Stefan Ruenzi, Florian WeigertDocument27 pagesJournal of Financial Economics: Vikas Agarwal, Stefan Ruenzi, Florian WeigertJuliana TessariNo ratings yet

- Nations TailDex Tail Risk IndexesDocument2 pagesNations TailDex Tail Risk IndexesEmanuele QuagliaNo ratings yet

- 00K - Antifragile Asset Allocation Model - GioeleGiordano - 1st PlaceDocument19 pages00K - Antifragile Asset Allocation Model - GioeleGiordano - 1st Placenaren.bansalNo ratings yet

- Normal DistributionDocument23 pagesNormal Distributionlemuel sardualNo ratings yet

- SSRN Id4378071Document24 pagesSSRN Id4378071AlexNo ratings yet