Download as pdf or txt

You might also like

- CGT Lecture Slides - IndividualsDocument27 pagesCGT Lecture Slides - IndividualsMusa NgobeniNo ratings yet

- Capital DepreciationDocument10 pagesCapital DepreciationRakesh RawtNo ratings yet

- CGT Notes - AnnotatedDocument54 pagesCGT Notes - AnnotatedDr SafaNo ratings yet

- Midterms TaxDocument4 pagesMidterms TaxPrincess Dianne CamachoNo ratings yet

- Capital Gains Tax Computation: Exempt AssetsDocument15 pagesCapital Gains Tax Computation: Exempt AssetsGayathri SudheerNo ratings yet

- L-27, Set Off and Carry Forward of LossesDocument20 pagesL-27, Set Off and Carry Forward of LosseswhoreNo ratings yet

- SC431 Lecture No. 5Document58 pagesSC431 Lecture No. 5Joseph BaruhiyeNo ratings yet

- Ia - Sketchnote Chap 8 Receivables N Chap 9 PpeDocument19 pagesIa - Sketchnote Chap 8 Receivables N Chap 9 PpeUyên Nguyễn Hoàng ThanhNo ratings yet

- Edited Plant AssetsDocument12 pagesEdited Plant AssetsMesele AdemeNo ratings yet

- HL Guide To CGT 0418 PDFDocument20 pagesHL Guide To CGT 0418 PDFbym87853No ratings yet

- P6 RN CGT ReliefsDocument15 pagesP6 RN CGT ReliefsHuda AkramNo ratings yet

- Futures and Options On Foreign Exchange: All Rights ReservedDocument45 pagesFutures and Options On Foreign Exchange: All Rights ReservedAnikaNo ratings yet

- Session 3 - Capital Gains Tax and RecoupmentsDocument28 pagesSession 3 - Capital Gains Tax and RecoupmentsLesediNo ratings yet

- Financial StatementsDocument8 pagesFinancial Statementsaryanparwani19No ratings yet

- Depreciation Accounting & Methods: Dr. Pallavi IngaleDocument37 pagesDepreciation Accounting & Methods: Dr. Pallavi IngalePallavi IngaleNo ratings yet

- SOE 401 - Engineering Econs - Entre Lecture1 - 3 Mr. Seini - DR Gazali - 2023Document54 pagesSOE 401 - Engineering Econs - Entre Lecture1 - 3 Mr. Seini - DR Gazali - 2023safianuharunNo ratings yet

- 03 - Tax On AssetsDocument6 pages03 - Tax On Assetsmails4vipsNo ratings yet

- Corporation Tax - AnnotatedDocument64 pagesCorporation Tax - AnnotatedDr SafaNo ratings yet

- Trading, P & L and BSDocument25 pagesTrading, P & L and BSshreyu14796No ratings yet

- Chapter 07Document17 pagesChapter 07Syeda Afsana Khanam 1611171630No ratings yet

- Long - Lived AssetsDocument25 pagesLong - Lived AssetsJeff KinutsNo ratings yet

- Lease AccountingDocument12 pagesLease AccountingJayachandran MalayidappadathNo ratings yet

- Topic 3Document26 pagesTopic 3michaelchris9068No ratings yet

- Prepare Financial Reports Edited HAND OUT1Document34 pagesPrepare Financial Reports Edited HAND OUT1getachewhabtamu361No ratings yet

- Accounts - Learning NotesDocument3 pagesAccounts - Learning NotesRoshni DashNo ratings yet

- Chapter 4 - CompleteDocument15 pagesChapter 4 - Completemohsin razaNo ratings yet

- Answer 1Document7 pagesAnswer 1sv03No ratings yet

- IAS 2 SummaryDocument3 pagesIAS 2 Summaryu22541617No ratings yet

- Property Dispositions Solutions Manual Discussion QuestionsDocument61 pagesProperty Dispositions Solutions Manual Discussion Questionscraig52292No ratings yet

- Stafford CaseDocument31 pagesStafford CaseJennineNo ratings yet

- Introduction To Income TaxationDocument32 pagesIntroduction To Income Taxationpara uqeenNo ratings yet

- Format of Trading Account & P&LDocument10 pagesFormat of Trading Account & P&L072 Yasmin AkhtarNo ratings yet

- Chapter 5 Part 2Document26 pagesChapter 5 Part 2ISLAM KHALED ZSCNo ratings yet

- Adv Buy BackDocument1 pageAdv Buy Backyewomit752No ratings yet

- UntitledDocument14 pagesUntitledjawaharkumar MBANo ratings yet

- Finance PDFDocument125 pagesFinance PDFRam Cherry VMNo ratings yet

- 9 Set Off & Carry ForwardDocument25 pages9 Set Off & Carry Forward21BAM025 RENGARAJANNo ratings yet

- 04 Royalty Accounts WebDocument4 pages04 Royalty Accounts WebRanjithNo ratings yet

- Capital Expenditure Revenue ExpenditureDocument2 pagesCapital Expenditure Revenue ExpenditureChong Kuan PeiNo ratings yet

- Budgeting (Refer To Chapter 9 of Hilton Text)Document3 pagesBudgeting (Refer To Chapter 9 of Hilton Text)ShiTheng Love UNo ratings yet

- Computation of Total Income & Tax LiabilityDocument5 pagesComputation of Total Income & Tax LiabilityMehtab MalikNo ratings yet

- ACCY963 Week 4 Lecture SlidesDocument102 pagesACCY963 Week 4 Lecture SlidesNIRAJ SharmaNo ratings yet

- Profit and Gain From BusinessDocument12 pagesProfit and Gain From BusinessAlokNo ratings yet

- Insolvency Account 222Document22 pagesInsolvency Account 222Sajjadur RahmanNo ratings yet

- Module-10 Accounting For Fixed Assets and DepreciationDocument23 pagesModule-10 Accounting For Fixed Assets and Depreciationmuhammadasghar8521No ratings yet

- State Govt Salary Package NBG PB C&ITU CSP 30 Dated 12 11 2010Document12 pagesState Govt Salary Package NBG PB C&ITU CSP 30 Dated 12 11 2010sudhakarNo ratings yet

- Trial Balance 01Document7 pagesTrial Balance 01Muhammad ZayanNo ratings yet

- 2022 Tax ComputationDocument7 pages2022 Tax ComputationGeo Mosaic Diaz (Jiyu)No ratings yet

- Week 8 Material - BEPDocument105 pagesWeek 8 Material - BEPDevashish PathakNo ratings yet

- Sketchnote Chap 9 2020 4th Ed - DungDocument12 pagesSketchnote Chap 9 2020 4th Ed - DungBành Đức HảiNo ratings yet

- Deductions To Gross IncomeDocument45 pagesDeductions To Gross IncomeKenzel lawasNo ratings yet

- Depriciation & Final Accounts: AmortisationDocument4 pagesDepriciation & Final Accounts: AmortisationVedant YadavNo ratings yet

- Capital Gains Tax: © AccaDocument29 pagesCapital Gains Tax: © AccaRai Ali WafaNo ratings yet

- Tax ReviewerDocument11 pagesTax Reviewerbertochristine10No ratings yet

- Partnership NotesDocument68 pagesPartnership NotesSandeepNo ratings yet

- 35 Corporate Accounting Repeaters 2013 14 and OnwardsDocument15 pages35 Corporate Accounting Repeaters 2013 14 and Onwardspremium info2222No ratings yet

- Depreciation O Level NotesDocument5 pagesDepreciation O Level NotesBijoy SalahuddinNo ratings yet

- S.Y.J.C. (Commerce) Book-Kkeping & Accoutancy Partnership Final Accounts Compiled By: Prof. Bosco FernandesDocument11 pagesS.Y.J.C. (Commerce) Book-Kkeping & Accoutancy Partnership Final Accounts Compiled By: Prof. Bosco FernandesDheer BhanushaliNo ratings yet

- 12th Accountancy Chapter 1Document4 pages12th Accountancy Chapter 1Ankit JainNo ratings yet

- Gift Relief 1638353123Document1 pageGift Relief 1638353123Dipesh MagratiNo ratings yet

- IPO and A Reverse TakeoverDocument1 pageIPO and A Reverse TakeoverDipesh MagratiNo ratings yet

- Day 2Document15 pagesDay 2Dipesh MagratiNo ratings yet

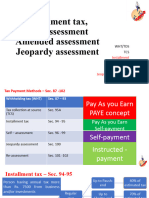

- Installment Assessment 94-102Document21 pagesInstallment Assessment 94-102Dipesh MagratiNo ratings yet

- J23 TRS AnswersDocument9 pagesJ23 TRS AnswersDipesh MagratiNo ratings yet

- Day 1Document9 pagesDay 1Dipesh MagratiNo ratings yet

- SBR06Document8 pagesSBR06Dipesh MagratiNo ratings yet

- Trs 2019 Dec QDocument19 pagesTrs 2019 Dec QDipesh MagratiNo ratings yet

- SBRIAS38 TutorSlidesDocument27 pagesSBRIAS38 TutorSlidesDipesh MagratiNo ratings yet

- J22 TRS AnswersDocument9 pagesJ22 TRS AnswersDipesh MagratiNo ratings yet

- SBRIAS40 TutorSlidesDocument10 pagesSBRIAS40 TutorSlidesDipesh MagratiNo ratings yet

- IFRS15Kit Q47TangCoDocument14 pagesIFRS15Kit Q47TangCoDipesh MagratiNo ratings yet

- SBRIFRS13 TutorSlidesDocument26 pagesSBRIFRS13 TutorSlidesDipesh MagratiNo ratings yet

- Motor CarsDocument9 pagesMotor CarsDipesh MagratiNo ratings yet

- Group Statements of CashFlowDocument24 pagesGroup Statements of CashFlowDipesh MagratiNo ratings yet

- Ethics - Moral Relativism (With A Focus On Moral Conventionalism) PDFDocument8 pagesEthics - Moral Relativism (With A Focus On Moral Conventionalism) PDFmaryaniNo ratings yet

- Appointment of External Auditors in Financial Institutions - Apr302015dfim04eDocument3 pagesAppointment of External Auditors in Financial Institutions - Apr302015dfim04enurul000No ratings yet

- Admission Policy of Clonberne Ns 2020Document12 pagesAdmission Policy of Clonberne Ns 2020api-356067070No ratings yet

- Criminal Law 1Document15 pagesCriminal Law 1Steven D Gerp100% (1)

- 060 MNS1 Coal Deposits and Coal Mining IDocument4 pages060 MNS1 Coal Deposits and Coal Mining ILalaNo ratings yet

- Qualifications of Party-List Nominees: (NRR - AB25)Document18 pagesQualifications of Party-List Nominees: (NRR - AB25)Zandra Andrea GlacitaNo ratings yet

- Commissioner of Internal Revenue, Petitioner, v. La Flor Dela Isabela, Inc., RespondentDocument9 pagesCommissioner of Internal Revenue, Petitioner, v. La Flor Dela Isabela, Inc., Respondentkristel jane caldozaNo ratings yet

- 07 - Focus - Sen - Memories of Partition's 'Forgotten Episode'. Refugee Resettlement in The Andaman IslandsDocument32 pages07 - Focus - Sen - Memories of Partition's 'Forgotten Episode'. Refugee Resettlement in The Andaman IslandsanandNo ratings yet

- Pak Mcqs National CA 2022-2023Document131 pagesPak Mcqs National CA 2022-2023Malik ZubairNo ratings yet

- Cdi 1 - Pre-Rev AssignmentsDocument10 pagesCdi 1 - Pre-Rev AssignmentsBelinda Viernes100% (1)

- DOWRY PROHIBITION (Repaired)Document20 pagesDOWRY PROHIBITION (Repaired)Mary Theresa JosephNo ratings yet

- Bbhi4103 Bi PDFDocument170 pagesBbhi4103 Bi PDFPAPPASSININo ratings yet

- Star Union Dai-Ichi Life Insurance Company Limited - CSR - ReportDocument14 pagesStar Union Dai-Ichi Life Insurance Company Limited - CSR - ReportAnuja GupteNo ratings yet

- 02 James Imbong Et Al vs. Hon. Paquito Ochoa Et AlDocument40 pages02 James Imbong Et Al vs. Hon. Paquito Ochoa Et AlJema LonaNo ratings yet

- CASES 1 Intro To Law WEEK 2 & 3Document36 pagesCASES 1 Intro To Law WEEK 2 & 3credit analystNo ratings yet

- FL All Family 140 Parenting Plan - 2022 07Document14 pagesFL All Family 140 Parenting Plan - 2022 07mom2asherloveNo ratings yet

- Case: Miguel Beluso vs. The Municipality of Panay (Capiz), G.R. No. 153974 August 7, 2006Document3 pagesCase: Miguel Beluso vs. The Municipality of Panay (Capiz), G.R. No. 153974 August 7, 2006PRINCESS MAGPATOCNo ratings yet

- BlockChain Reaction Paper Submitted by Mr. Red DumaliDocument3 pagesBlockChain Reaction Paper Submitted by Mr. Red DumaliReden DumaliNo ratings yet

- Invoice: Jet Airways (India) LimitedDocument1 pageInvoice: Jet Airways (India) LimitedVedant ShroffNo ratings yet

- in Re Columns of Amado MacasaetDocument59 pagesin Re Columns of Amado MacasaetKaren Daryl BritoNo ratings yet

- Contracts of Muqawala and Decennial LiabilityDocument3 pagesContracts of Muqawala and Decennial LiabilityJama 'Figo' MustafaNo ratings yet

- ANTP1Document72 pagesANTP1baji shaikNo ratings yet

- Dpb3063: Business Law: Chapter 4: AgencyDocument15 pagesDpb3063: Business Law: Chapter 4: AgencyDIVIYAHNo ratings yet

- Vlad Frunze 80015636 EncryptedDocument25 pagesVlad Frunze 80015636 Encryptedionmos78No ratings yet

- 125 Maintainance 144Document13 pages125 Maintainance 144Ishan AryanNo ratings yet

- College of Criminology: Midterm Exam For Crim 6 BE HONEST... Good Luck... Ten (10) Points EachDocument1 pageCollege of Criminology: Midterm Exam For Crim 6 BE HONEST... Good Luck... Ten (10) Points EachAnitaManzanilloNo ratings yet

- Buyer and SellerDocument2 pagesBuyer and SellerZidan ZaifNo ratings yet

- Test Bank Law 2 DiazDocument11 pagesTest Bank Law 2 DiazGray JavierNo ratings yet

- UntitledDocument13 pagesUntitledIzabelle KallyNo ratings yet

- Lessons in Horology PDFDocument303 pagesLessons in Horology PDFJames Finley100% (2)