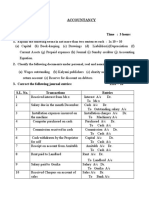

Accounts Test Paper From Jeegyasa

Accounts Test Paper From Jeegyasa

You might also like

- Statement - Nov 2019 2Document13 pagesStatement - Nov 2019 2Jack Carroll (Attorney Jack B. Carroll)No ratings yet

- Finance Case Study2 FINALDocument6 pagesFinance Case Study2 FINALDan Carlo Delgado PoblacionNo ratings yet

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionFrom EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionNo ratings yet

- Pitch Deck Sample For StartupsDocument24 pagesPitch Deck Sample For StartupsKetan JajuNo ratings yet

- Intro To Consulting SlidesDocument34 pagesIntro To Consulting Slidesmanojben100% (2)

- Blackbook Project On CSR of Mahindra Amp MahindraDocument56 pagesBlackbook Project On CSR of Mahindra Amp Mahindrasupriya patekar43% (7)

- Mock TestDocument8 pagesMock TestDiksha DudejaNo ratings yet

- Accountancy QP XiDocument4 pagesAccountancy QP XiMohammedNo ratings yet

- +1 Accountancy ONLINE Final Examination 2021Document5 pages+1 Accountancy ONLINE Final Examination 2021Rajwinder BansalNo ratings yet

- Cbse XI 2019-2020 Annual ExamDocument6 pagesCbse XI 2019-2020 Annual Exammadhavmanoj08No ratings yet

- 11th AccountDocument3 pages11th Accountnmzrv8jfq8No ratings yet

- Accounts ExamDocument5 pagesAccounts Examsoulvloggers321No ratings yet

- AtibhaDocument7 pagesAtibhaAangry VermaNo ratings yet

- Session Ending Examination 2019Document7 pagesSession Ending Examination 2019madhudevi06435No ratings yet

- Model Paper, Accountancy, XIDocument13 pagesModel Paper, Accountancy, XIanyaNo ratings yet

- Screenshot 2023-02-21 at 1.23.27 AMDocument12 pagesScreenshot 2023-02-21 at 1.23.27 AMGracy AroraNo ratings yet

- Account Test 2Document5 pagesAccount Test 2klaw6048No ratings yet

- Part - A: (Financial Accounting - I)Document16 pagesPart - A: (Financial Accounting - I)Adit Bohra VIII BNo ratings yet

- Namma Kalvi 11th Accountancy Model Questin Paper EM 221452Document8 pagesNamma Kalvi 11th Accountancy Model Questin Paper EM 221452sharonjamesappuNo ratings yet

- Accountancy PaperDocument7 pagesAccountancy PapersumitaNo ratings yet

- Book Keeping FivDocument6 pagesBook Keeping FivALE MEDIANo ratings yet

- Progress Test-4 (Chapters 1 and 2)Document4 pagesProgress Test-4 (Chapters 1 and 2)buraale94No ratings yet

- MCQ QuestionsDocument6 pagesMCQ QuestionsANo ratings yet

- 11 Sample Papers Accountancy 2Document10 pages11 Sample Papers Accountancy 2AvcelNo ratings yet

- 2) 3) Mark. 1. 2. A+C L-C A-L 4. 6. - 7. L Loan Debt: Examination, November-?Oi7Document4 pages2) 3) Mark. 1. 2. A+C L-C A-L 4. 6. - 7. L Loan Debt: Examination, November-?Oi7Best ThingsNo ratings yet

- 23 Accounts-RTP-DecemberDocument32 pages23 Accounts-RTP-Decemberjustinbieberm77No ratings yet

- Accounts Prelim Paper 28-11-23Document4 pagesAccounts Prelim Paper 28-11-23roshanchoudhary4350No ratings yet

- RTP Dec2023 p1Document32 pagesRTP Dec2023 p1Vaibhav M S100% (1)

- ICAI MOCK TEST CA FOUNDATION DECEMBER 2022 Paper 1 Principles andDocument6 pagesICAI MOCK TEST CA FOUNDATION DECEMBER 2022 Paper 1 Principles andArpit GuptaNo ratings yet

- Cbse 11 Accounts CH 9 To 15 Revision WorksheetDocument9 pagesCbse 11 Accounts CH 9 To 15 Revision WorksheetRiwaanNo ratings yet

- Exam Practice Questions - Holiday Work - Yr 10 - 2023 - 2024Document35 pagesExam Practice Questions - Holiday Work - Yr 10 - 2023 - 2024MUSTHARI KHANNo ratings yet

- Model Question Paper Class 11 AccountsDocument97 pagesModel Question Paper Class 11 AccountsAbel Soby Joseph100% (3)

- Explain The Following Terms in Not More Than Two Sentences Each: 1x 10 10Document4 pagesExplain The Following Terms in Not More Than Two Sentences Each: 1x 10 10Anita PanigrahiNo ratings yet

- Practice PaperDocument13 pagesPractice PaperArush BlagganaNo ratings yet

- 11 Accountancy First Term Set BDocument6 pages11 Accountancy First Term Set Bmcsworkshop777No ratings yet

- XI Account QPDocument7 pagesXI Account QPtanushsoni37No ratings yet

- Foundation Accounts Suggested May19Document23 pagesFoundation Accounts Suggested May19Aman SinghNo ratings yet

- 11 Accountancy First Term Set ADocument6 pages11 Accountancy First Term Set Amcsworkshop777No ratings yet

- FA Question Bank TT1-1Document14 pagesFA Question Bank TT1-1rock SINGHALNo ratings yet

- Accountancy Sample Paper Final ImportantDocument18 pagesAccountancy Sample Paper Final ImportantChitra Vasu100% (1)

- Amardeep XI First TermDocument8 pagesAmardeep XI First TermAnahita GuptaNo ratings yet

- Accountancy Sample Paper 2Document8 pagesAccountancy Sample Paper 2mcrekhaaNo ratings yet

- Accounts RTP Foundation Nov 2020Document25 pagesAccounts RTP Foundation Nov 2020Jayasurya MuruganathanNo ratings yet

- Acc Paper Class 11Document16 pagesAcc Paper Class 11Varsha AswaniNo ratings yet

- ACCT 1Document15 pagesACCT 1Joyce OcarizaNo ratings yet

- Acc Xi Class Test-I 2022Document4 pagesAcc Xi Class Test-I 2022shaurya kapoorNo ratings yet

- Sample Paper 5 (Final Exam XI Accountancy)Document9 pagesSample Paper 5 (Final Exam XI Accountancy)pritanshutripathi84No ratings yet

- 11 Sample Papers Accountancy 2020 English Medium Set 3Document10 pages11 Sample Papers Accountancy 2020 English Medium Set 3Joshi DrcpNo ratings yet

- Class XI Acc SM Arya Annual 2023-24Document5 pagesClass XI Acc SM Arya Annual 2023-24pandeyansh962No ratings yet

- Acct Practice PaperDocument11 pagesAcct Practice PaperKrish BajajNo ratings yet

- F3 Book Keeping Monthly Test Feb 2024Document6 pagesF3 Book Keeping Monthly Test Feb 2024abdulsamadm1982No ratings yet

- FA (1st) Dec2017Document3 pagesFA (1st) Dec2017dkdjfNo ratings yet

- Acctg1 MidtermDocument6 pagesAcctg1 MidtermKevin Elrey Arce50% (4)

- Book KeepingDocument6 pagesBook KeepingALE MEDIANo ratings yet

- Review Materials The Accounting Process To Accounts ReceivableDocument7 pagesReview Materials The Accounting Process To Accounts ReceivableMarin, Nicole DondoyanoNo ratings yet

- 2nd Quarter Final Exam Oct. 2019Document3 pages2nd Quarter Final Exam Oct. 2019awdasdNo ratings yet

- CA Foundation Paper 1 Principles and Practice of Accounting SADocument24 pagesCA Foundation Paper 1 Principles and Practice of Accounting SAavula Venkatrao100% (1)

- Test Paper Ca FoundDocument5 pagesTest Paper Ca FoundSarangapani KaliyamoorthyNo ratings yet

- FAR Midterm QuizDocument2 pagesFAR Midterm QuizAllyy DelacruzNo ratings yet

- CA Foundation Accounts RTP May 2023Document32 pagesCA Foundation Accounts RTP May 2023PushkarNo ratings yet

- FA Weekend TestDocument5 pagesFA Weekend TestIryne MerrieNo ratings yet

- 11 Accountancy SP 01Document33 pages11 Accountancy SP 01Haridas OngallurNo ratings yet

- RTP Accounting CA Foundation May 18Document35 pagesRTP Accounting CA Foundation May 18kanishk bahetiNo ratings yet

- 1st Puc Accountancy Midterm Question Paper Nov 2017-Mandya PDFDocument10 pages1st Puc Accountancy Midterm Question Paper Nov 2017-Mandya PDFBest ThingsNo ratings yet

- Am Banklaunches MalaysiasfirstonlinedebtDocument2 pagesAm Banklaunches MalaysiasfirstonlinedebthairyzaltNo ratings yet

- Measuring The Quality of Health Services in AlgeriaDocument14 pagesMeasuring The Quality of Health Services in Algeriaamialotfi20No ratings yet

- EBAY Five ForceDocument14 pagesEBAY Five ForceXiaofang Li100% (4)

- Unemployment and Underemploymentin Rural IndiaDocument9 pagesUnemployment and Underemploymentin Rural IndiaPranavVohraNo ratings yet

- Plan de AfacereDocument18 pagesPlan de AfacereYani CanciuNo ratings yet

- New Standing Order Instruction Nwi50000eDocument1 pageNew Standing Order Instruction Nwi50000ejamalazoz05No ratings yet

- Chapter 8Document31 pagesChapter 8laurenbondy44No ratings yet

- The Business 2.0 VocabularyDocument18 pagesThe Business 2.0 VocabularyGIBRAN CASTAÑEDANo ratings yet

- Cases CH 8Document4 pagesCases CH 8YurmaNo ratings yet

- COST SHEET NumericalsDocument9 pagesCOST SHEET Numericalsmisaki chanNo ratings yet

- Assignment Case Study NegotationDocument6 pagesAssignment Case Study Negotationfkjhvb,No ratings yet

- BUSINESS PROPOSAL SEC A - Group 3Document25 pagesBUSINESS PROPOSAL SEC A - Group 3sanandi DASNo ratings yet

- Thesis Paper On AIBLDocument131 pagesThesis Paper On AIBLMd Khaled NoorNo ratings yet

- The First Assignment For StrategyDocument7 pagesThe First Assignment For StrategySơn TùngNo ratings yet

- Dealings in Properties and The Withholding Tax SystemDocument38 pagesDealings in Properties and The Withholding Tax SystemKenzel lawasNo ratings yet

- BIS Sample Database - IIIDocument2 pagesBIS Sample Database - IIIAarti IyerNo ratings yet

- Importance of Consumer KnowledgeDocument66 pagesImportance of Consumer Knowledgezenith160% (1)

- Nisha CVDocument2 pagesNisha CVNisha SinhaNo ratings yet

- Brksec-1021 (2018)Document84 pagesBrksec-1021 (2018)Paul ZetoNo ratings yet

- Solutions Nss NC 19Document8 pagesSolutions Nss NC 19lethiphuongdanNo ratings yet

- Exporters and Shipping Importers in KuwaitDocument35 pagesExporters and Shipping Importers in Kuwaitgobudas3No ratings yet

- Little Oil CompanyDocument10 pagesLittle Oil CompanyJosann Welch100% (1)

- Business English 4 Test SamplesDocument2 pagesBusiness English 4 Test SamplesAlinaArcanaNo ratings yet

- How To Create Killer Sales Playbooks GuideDocument14 pagesHow To Create Killer Sales Playbooks GuideLeonie Newbury100% (1)

- Globalización? Análisis de Su Marketing-Mix Internacional: Mango: ¿Un Caso de Estrategia y Política deDocument15 pagesGlobalización? Análisis de Su Marketing-Mix Internacional: Mango: ¿Un Caso de Estrategia y Política demichxel psNo ratings yet

Download as pdf or txt

You might also like

- Statement - Nov 2019 2Document13 pagesStatement - Nov 2019 2Jack Carroll (Attorney Jack B. Carroll)No ratings yet

- Finance Case Study2 FINALDocument6 pagesFinance Case Study2 FINALDan Carlo Delgado PoblacionNo ratings yet

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionFrom EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionNo ratings yet

- Pitch Deck Sample For StartupsDocument24 pagesPitch Deck Sample For StartupsKetan JajuNo ratings yet

- Intro To Consulting SlidesDocument34 pagesIntro To Consulting Slidesmanojben100% (2)

- Blackbook Project On CSR of Mahindra Amp MahindraDocument56 pagesBlackbook Project On CSR of Mahindra Amp Mahindrasupriya patekar43% (7)

- Mock TestDocument8 pagesMock TestDiksha DudejaNo ratings yet

- Accountancy QP XiDocument4 pagesAccountancy QP XiMohammedNo ratings yet

- +1 Accountancy ONLINE Final Examination 2021Document5 pages+1 Accountancy ONLINE Final Examination 2021Rajwinder BansalNo ratings yet

- Cbse XI 2019-2020 Annual ExamDocument6 pagesCbse XI 2019-2020 Annual Exammadhavmanoj08No ratings yet

- 11th AccountDocument3 pages11th Accountnmzrv8jfq8No ratings yet

- Accounts ExamDocument5 pagesAccounts Examsoulvloggers321No ratings yet

- AtibhaDocument7 pagesAtibhaAangry VermaNo ratings yet

- Session Ending Examination 2019Document7 pagesSession Ending Examination 2019madhudevi06435No ratings yet

- Model Paper, Accountancy, XIDocument13 pagesModel Paper, Accountancy, XIanyaNo ratings yet

- Screenshot 2023-02-21 at 1.23.27 AMDocument12 pagesScreenshot 2023-02-21 at 1.23.27 AMGracy AroraNo ratings yet

- Account Test 2Document5 pagesAccount Test 2klaw6048No ratings yet

- Part - A: (Financial Accounting - I)Document16 pagesPart - A: (Financial Accounting - I)Adit Bohra VIII BNo ratings yet

- Namma Kalvi 11th Accountancy Model Questin Paper EM 221452Document8 pagesNamma Kalvi 11th Accountancy Model Questin Paper EM 221452sharonjamesappuNo ratings yet

- Accountancy PaperDocument7 pagesAccountancy PapersumitaNo ratings yet

- Book Keeping FivDocument6 pagesBook Keeping FivALE MEDIANo ratings yet

- Progress Test-4 (Chapters 1 and 2)Document4 pagesProgress Test-4 (Chapters 1 and 2)buraale94No ratings yet

- MCQ QuestionsDocument6 pagesMCQ QuestionsANo ratings yet

- 11 Sample Papers Accountancy 2Document10 pages11 Sample Papers Accountancy 2AvcelNo ratings yet

- 2) 3) Mark. 1. 2. A+C L-C A-L 4. 6. - 7. L Loan Debt: Examination, November-?Oi7Document4 pages2) 3) Mark. 1. 2. A+C L-C A-L 4. 6. - 7. L Loan Debt: Examination, November-?Oi7Best ThingsNo ratings yet

- 23 Accounts-RTP-DecemberDocument32 pages23 Accounts-RTP-Decemberjustinbieberm77No ratings yet

- Accounts Prelim Paper 28-11-23Document4 pagesAccounts Prelim Paper 28-11-23roshanchoudhary4350No ratings yet

- RTP Dec2023 p1Document32 pagesRTP Dec2023 p1Vaibhav M S100% (1)

- ICAI MOCK TEST CA FOUNDATION DECEMBER 2022 Paper 1 Principles andDocument6 pagesICAI MOCK TEST CA FOUNDATION DECEMBER 2022 Paper 1 Principles andArpit GuptaNo ratings yet

- Cbse 11 Accounts CH 9 To 15 Revision WorksheetDocument9 pagesCbse 11 Accounts CH 9 To 15 Revision WorksheetRiwaanNo ratings yet

- Exam Practice Questions - Holiday Work - Yr 10 - 2023 - 2024Document35 pagesExam Practice Questions - Holiday Work - Yr 10 - 2023 - 2024MUSTHARI KHANNo ratings yet

- Model Question Paper Class 11 AccountsDocument97 pagesModel Question Paper Class 11 AccountsAbel Soby Joseph100% (3)

- Explain The Following Terms in Not More Than Two Sentences Each: 1x 10 10Document4 pagesExplain The Following Terms in Not More Than Two Sentences Each: 1x 10 10Anita PanigrahiNo ratings yet

- Practice PaperDocument13 pagesPractice PaperArush BlagganaNo ratings yet

- 11 Accountancy First Term Set BDocument6 pages11 Accountancy First Term Set Bmcsworkshop777No ratings yet

- XI Account QPDocument7 pagesXI Account QPtanushsoni37No ratings yet

- Foundation Accounts Suggested May19Document23 pagesFoundation Accounts Suggested May19Aman SinghNo ratings yet

- 11 Accountancy First Term Set ADocument6 pages11 Accountancy First Term Set Amcsworkshop777No ratings yet

- FA Question Bank TT1-1Document14 pagesFA Question Bank TT1-1rock SINGHALNo ratings yet

- Accountancy Sample Paper Final ImportantDocument18 pagesAccountancy Sample Paper Final ImportantChitra Vasu100% (1)

- Amardeep XI First TermDocument8 pagesAmardeep XI First TermAnahita GuptaNo ratings yet

- Accountancy Sample Paper 2Document8 pagesAccountancy Sample Paper 2mcrekhaaNo ratings yet

- Accounts RTP Foundation Nov 2020Document25 pagesAccounts RTP Foundation Nov 2020Jayasurya MuruganathanNo ratings yet

- Acc Paper Class 11Document16 pagesAcc Paper Class 11Varsha AswaniNo ratings yet

- ACCT 1Document15 pagesACCT 1Joyce OcarizaNo ratings yet

- Acc Xi Class Test-I 2022Document4 pagesAcc Xi Class Test-I 2022shaurya kapoorNo ratings yet

- Sample Paper 5 (Final Exam XI Accountancy)Document9 pagesSample Paper 5 (Final Exam XI Accountancy)pritanshutripathi84No ratings yet

- 11 Sample Papers Accountancy 2020 English Medium Set 3Document10 pages11 Sample Papers Accountancy 2020 English Medium Set 3Joshi DrcpNo ratings yet

- Class XI Acc SM Arya Annual 2023-24Document5 pagesClass XI Acc SM Arya Annual 2023-24pandeyansh962No ratings yet

- Acct Practice PaperDocument11 pagesAcct Practice PaperKrish BajajNo ratings yet

- F3 Book Keeping Monthly Test Feb 2024Document6 pagesF3 Book Keeping Monthly Test Feb 2024abdulsamadm1982No ratings yet

- FA (1st) Dec2017Document3 pagesFA (1st) Dec2017dkdjfNo ratings yet

- Acctg1 MidtermDocument6 pagesAcctg1 MidtermKevin Elrey Arce50% (4)

- Book KeepingDocument6 pagesBook KeepingALE MEDIANo ratings yet

- Review Materials The Accounting Process To Accounts ReceivableDocument7 pagesReview Materials The Accounting Process To Accounts ReceivableMarin, Nicole DondoyanoNo ratings yet

- 2nd Quarter Final Exam Oct. 2019Document3 pages2nd Quarter Final Exam Oct. 2019awdasdNo ratings yet

- CA Foundation Paper 1 Principles and Practice of Accounting SADocument24 pagesCA Foundation Paper 1 Principles and Practice of Accounting SAavula Venkatrao100% (1)

- Test Paper Ca FoundDocument5 pagesTest Paper Ca FoundSarangapani KaliyamoorthyNo ratings yet

- FAR Midterm QuizDocument2 pagesFAR Midterm QuizAllyy DelacruzNo ratings yet

- CA Foundation Accounts RTP May 2023Document32 pagesCA Foundation Accounts RTP May 2023PushkarNo ratings yet

- FA Weekend TestDocument5 pagesFA Weekend TestIryne MerrieNo ratings yet

- 11 Accountancy SP 01Document33 pages11 Accountancy SP 01Haridas OngallurNo ratings yet

- RTP Accounting CA Foundation May 18Document35 pagesRTP Accounting CA Foundation May 18kanishk bahetiNo ratings yet

- 1st Puc Accountancy Midterm Question Paper Nov 2017-Mandya PDFDocument10 pages1st Puc Accountancy Midterm Question Paper Nov 2017-Mandya PDFBest ThingsNo ratings yet

- Am Banklaunches MalaysiasfirstonlinedebtDocument2 pagesAm Banklaunches MalaysiasfirstonlinedebthairyzaltNo ratings yet

- Measuring The Quality of Health Services in AlgeriaDocument14 pagesMeasuring The Quality of Health Services in Algeriaamialotfi20No ratings yet

- EBAY Five ForceDocument14 pagesEBAY Five ForceXiaofang Li100% (4)

- Unemployment and Underemploymentin Rural IndiaDocument9 pagesUnemployment and Underemploymentin Rural IndiaPranavVohraNo ratings yet

- Plan de AfacereDocument18 pagesPlan de AfacereYani CanciuNo ratings yet

- New Standing Order Instruction Nwi50000eDocument1 pageNew Standing Order Instruction Nwi50000ejamalazoz05No ratings yet

- Chapter 8Document31 pagesChapter 8laurenbondy44No ratings yet

- The Business 2.0 VocabularyDocument18 pagesThe Business 2.0 VocabularyGIBRAN CASTAÑEDANo ratings yet

- Cases CH 8Document4 pagesCases CH 8YurmaNo ratings yet

- COST SHEET NumericalsDocument9 pagesCOST SHEET Numericalsmisaki chanNo ratings yet

- Assignment Case Study NegotationDocument6 pagesAssignment Case Study Negotationfkjhvb,No ratings yet

- BUSINESS PROPOSAL SEC A - Group 3Document25 pagesBUSINESS PROPOSAL SEC A - Group 3sanandi DASNo ratings yet

- Thesis Paper On AIBLDocument131 pagesThesis Paper On AIBLMd Khaled NoorNo ratings yet

- The First Assignment For StrategyDocument7 pagesThe First Assignment For StrategySơn TùngNo ratings yet

- Dealings in Properties and The Withholding Tax SystemDocument38 pagesDealings in Properties and The Withholding Tax SystemKenzel lawasNo ratings yet

- BIS Sample Database - IIIDocument2 pagesBIS Sample Database - IIIAarti IyerNo ratings yet

- Importance of Consumer KnowledgeDocument66 pagesImportance of Consumer Knowledgezenith160% (1)

- Nisha CVDocument2 pagesNisha CVNisha SinhaNo ratings yet

- Brksec-1021 (2018)Document84 pagesBrksec-1021 (2018)Paul ZetoNo ratings yet

- Solutions Nss NC 19Document8 pagesSolutions Nss NC 19lethiphuongdanNo ratings yet

- Exporters and Shipping Importers in KuwaitDocument35 pagesExporters and Shipping Importers in Kuwaitgobudas3No ratings yet

- Little Oil CompanyDocument10 pagesLittle Oil CompanyJosann Welch100% (1)

- Business English 4 Test SamplesDocument2 pagesBusiness English 4 Test SamplesAlinaArcanaNo ratings yet

- How To Create Killer Sales Playbooks GuideDocument14 pagesHow To Create Killer Sales Playbooks GuideLeonie Newbury100% (1)

- Globalización? Análisis de Su Marketing-Mix Internacional: Mango: ¿Un Caso de Estrategia y Política deDocument15 pagesGlobalización? Análisis de Su Marketing-Mix Internacional: Mango: ¿Un Caso de Estrategia y Política demichxel psNo ratings yet