Download as docx, pdf, or txt

You might also like

- Case 1 Sample SolutionsDocument9 pagesCase 1 Sample SolutionsBillie JeanNo ratings yet

- Final Project - M 8116 PDFDocument133 pagesFinal Project - M 8116 PDFDinesh Murugan100% (1)

- Final Project - Credit Mgt. PNBDocument51 pagesFinal Project - Credit Mgt. PNBShankar BhagatNo ratings yet

- Employee Morale in Sbi: State Bank of IndiaDocument57 pagesEmployee Morale in Sbi: State Bank of Indiakaundilya1559No ratings yet

- College Project On Central Coalfields LimitedDocument74 pagesCollege Project On Central Coalfields LimitedDebzane PatiNo ratings yet

- Corporate Governance in Indian Banking Sector - PNBDocument85 pagesCorporate Governance in Indian Banking Sector - PNBSaiRaj NaikNo ratings yet

- A Project Report - 2Document62 pagesA Project Report - 2sandhyaNo ratings yet

- Aditya Shahi ProjectDocument74 pagesAditya Shahi Projectsairaj dombaleNo ratings yet

- Banking Sector Reforms in India Some ReflectionsDocument14 pagesBanking Sector Reforms in India Some ReflectionsAustin OliverNo ratings yet

- Study of GST Its Applications BHELDocument43 pagesStudy of GST Its Applications BHELBalram ModiNo ratings yet

- Major ProjectDocument80 pagesMajor ProjectAllan RajuNo ratings yet

- Dena BankDocument25 pagesDena BankJaved ShaikhNo ratings yet

- SIP Project Report 2Document52 pagesSIP Project Report 2pallabi singha royNo ratings yet

- Merger of SBI and Their Associate BanksDocument16 pagesMerger of SBI and Their Associate BanksVipulNo ratings yet

- Kotak FinalDocument46 pagesKotak FinalRahul FaliyaNo ratings yet

- Branch BankingDocument12 pagesBranch BankingPRIYANSH BHARGAVANo ratings yet

- A Study of Financial Analysis of ICICI BankDocument54 pagesA Study of Financial Analysis of ICICI BankVinayak PadaveNo ratings yet

- Capital Market Project1Document99 pagesCapital Market Project1Gary GaryNo ratings yet

- Marketing Project 2023Document40 pagesMarketing Project 2023rohanbhise77No ratings yet

- Sbi SynopsisDocument7 pagesSbi SynopsisvenkibgvNo ratings yet

- Project On Banking Sector in IndiaDocument32 pagesProject On Banking Sector in IndiaPatel SagarNo ratings yet

- Summer Project Report - Format - MmsDocument47 pagesSummer Project Report - Format - MmsVaishnavi khotNo ratings yet

- DissertationDocument85 pagesDissertationAbhijit MohantyNo ratings yet

- An Analysis of Mergers & Acquisitions in The Indian Banking IndustryDocument48 pagesAn Analysis of Mergers & Acquisitions in The Indian Banking Industrydebasri_chatterjeeNo ratings yet

- Micro Finance ProjectDocument50 pagesMicro Finance Projectnikesh moreNo ratings yet

- Summer Report Idbi (Avinash)Document84 pagesSummer Report Idbi (Avinash)Govind KushwahaNo ratings yet

- Main MatterDocument52 pagesMain MatterPraveen SehgalNo ratings yet

- Blackbook Final 456....Document71 pagesBlackbook Final 456....8784No ratings yet

- Riddhi Corporate FinanceDocument21 pagesRiddhi Corporate FinanceManas BhawsarNo ratings yet

- Final Project On Financial InclusionDocument33 pagesFinal Project On Financial InclusionPriyanshu ChoudharyNo ratings yet

- Performance Appraisal 2018Document81 pagesPerformance Appraisal 2018maria mercyNo ratings yet

- Minda LTDDocument82 pagesMinda LTDAnkit PandeyNo ratings yet

- Merchant Banking in IndiaDocument14 pagesMerchant Banking in IndiaMohitraheja007No ratings yet

- Minor Project On Mutual FundsDocument37 pagesMinor Project On Mutual FundsGauravNo ratings yet

- Final Project ON A Study On The Credit Appraisal Methods Adopted by Central Bank of IndiaDocument103 pagesFinal Project ON A Study On The Credit Appraisal Methods Adopted by Central Bank of IndiaPiyush SethiNo ratings yet

- INTRODUCTION To BancassuranceDocument53 pagesINTRODUCTION To BancassuranceharshitaNo ratings yet

- CRM in BankDocument78 pagesCRM in BankSaurabh MaheshwariNo ratings yet

- Role of IT Sector in India's Economic Development.Document21 pagesRole of IT Sector in India's Economic Development.Anurag SharmaNo ratings yet

- A Study On Performance Appraisal System at HDFC Bank LucknowDocument5 pagesA Study On Performance Appraisal System at HDFC Bank LucknowChandan SrivastavaNo ratings yet

- Retail Banking in India FULL - Doc Scribd (Repaired)Document54 pagesRetail Banking in India FULL - Doc Scribd (Repaired)RACHANA100% (1)

- Comparative Study On Working Capital Management. at Bhilai Steel by Anil SinghDocument86 pagesComparative Study On Working Capital Management. at Bhilai Steel by Anil Singhsattu_luvNo ratings yet

- Mutual Fund Report FinalDocument65 pagesMutual Fund Report FinaldeepthisantoshNo ratings yet

- A Comparative Study of Some Selected Mutual Fund Schemes: Project ReportDocument70 pagesA Comparative Study of Some Selected Mutual Fund Schemes: Project ReportNawnit KediaNo ratings yet

- Customer Satisfaction Towards Lic Housing FinancDocument69 pagesCustomer Satisfaction Towards Lic Housing Financboss_144569224100% (1)

- Impact of GST On Retail Business With Repect To Airoli, Maharashtra PDFDocument91 pagesImpact of GST On Retail Business With Repect To Airoli, Maharashtra PDFOmkar PatoleNo ratings yet

- Project PDFDocument92 pagesProject PDFUrvashi SharmaNo ratings yet

- Internship Report - 03 June 22Document12 pagesInternship Report - 03 June 22Alina KujurNo ratings yet

- A Project Report ON: "Customer Satisfaction Towards Icici Bank With Special Reference To Gondia Branch"Document72 pagesA Project Report ON: "Customer Satisfaction Towards Icici Bank With Special Reference To Gondia Branch"ravijoshi1010No ratings yet

- Summer Training Report: Cost Reduction or Increase in Revenue of Punjab National BankDocument46 pagesSummer Training Report: Cost Reduction or Increase in Revenue of Punjab National BankDeepu SinghNo ratings yet

- Challenges For Public Sector Banks in IndiaDocument63 pagesChallenges For Public Sector Banks in IndiaKahkashan Anjum100% (8)

- Innovations in InsuranceDocument47 pagesInnovations in InsuranceDouglas StoneNo ratings yet

- ProjectDocument42 pagesProjectVenkatesh VenkyNo ratings yet

- Aarti FinalsDocument63 pagesAarti FinalsBnaren NarenNo ratings yet

- Green Products A Complete Guide - 2020 EditionFrom EverandGreen Products A Complete Guide - 2020 EditionRating: 5 out of 5 stars5/5 (1)

- Wa0031.Document35 pagesWa0031.Tushar PagareNo ratings yet

- Capstone PROJECT FOR YEAR 2023 - 2024Document68 pagesCapstone PROJECT FOR YEAR 2023 - 2024Sahil DumbreNo ratings yet

- Comparative Analysis of Direct Banking Services of Kotak With Other BanksDocument105 pagesComparative Analysis of Direct Banking Services of Kotak With Other Bankssuruchiathavale221234No ratings yet

- A Project Report On Consumer Satisfaction of HDFC With Special RefernceDocument72 pagesA Project Report On Consumer Satisfaction of HDFC With Special RefernceAnmol koundalNo ratings yet

- MMS 22 24 C40 BBDocument61 pagesMMS 22 24 C40 BBS H RE ENo ratings yet

- Service Quality Customer Satisfaction and CustomerDocument10 pagesService Quality Customer Satisfaction and CustomerTanmay lalaNo ratings yet

- Lounge Access List World PDFDocument4 pagesLounge Access List World PDFashwin16No ratings yet

- MCQs Chapter 9 Financial CrisesDocument12 pagesMCQs Chapter 9 Financial Crisesphamhongphat2014No ratings yet

- Loan AgreementDocument3 pagesLoan AgreementArgin ButligNo ratings yet

- Yogi Apriyanto, Yuni Yulida, Aprida Siska Lestia: Asuransi Jiwa Berjangka Last SurvivorDocument11 pagesYogi Apriyanto, Yuni Yulida, Aprida Siska Lestia: Asuransi Jiwa Berjangka Last SurvivorSugeng KuswantoroNo ratings yet

- SAP Bank Accounting Configuration Steps - SAP TutorialDocument6 pagesSAP Bank Accounting Configuration Steps - SAP TutorialKapadia MritulNo ratings yet

- 33303XXXXXX 3ywn74giDocument4 pages33303XXXXXX 3ywn74giranjanpalei524No ratings yet

- ListDocument4 pagesListGeorge JacksonNo ratings yet

- Budget and Cashflow 2015 For Googlesheets - Budget Challenge CfsDocument19 pagesBudget and Cashflow 2015 For Googlesheets - Budget Challenge Cfsapi-309679929No ratings yet

- Statutory Liquid Ratio (SLR)Document4 pagesStatutory Liquid Ratio (SLR)BhuvisNo ratings yet

- ND THDocument5 pagesND THVishal BawaneNo ratings yet

- Form No 15GDocument4 pagesForm No 15GFinance & Health ExpressNo ratings yet

- U.S. Individual Income Tax ReturnDocument5 pagesU.S. Individual Income Tax ReturnTrish HitNo ratings yet

- Principles of Accounts: Name and Index No: Class: Date Topic: Level: ReferenceDocument2 pagesPrinciples of Accounts: Name and Index No: Class: Date Topic: Level: ReferenceCindy SweNo ratings yet

- Mano SettuDocument7 pagesMano SettuRobert RajuNo ratings yet

- Equation of ValueDocument17 pagesEquation of ValueKim TNo ratings yet

- Lesson 27: Finding Interest Rate and Time in Compound InterestDocument15 pagesLesson 27: Finding Interest Rate and Time in Compound InterestDonna Angela Zafra BalbuenaNo ratings yet

- Banking Law Practice Questions and Answers 2Document4 pagesBanking Law Practice Questions and Answers 2Phetho MachiliNo ratings yet

- Unit III-Leasing and Hire PurchaseDocument50 pagesUnit III-Leasing and Hire PurchaseAkashik GgNo ratings yet

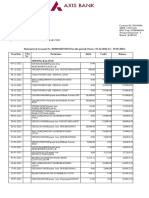

- Garima Axis Bank SDocument3 pagesGarima Axis Bank SSajan Sharma100% (1)

- Intermediate Accounting Chapter 7 Exercises - ValixDocument26 pagesIntermediate Accounting Chapter 7 Exercises - ValixAbbie ProfugoNo ratings yet

- Q4FY23 Investor PresentationDocument49 pagesQ4FY23 Investor PresentationAradhyaNo ratings yet

- PERSONAL BUDGETING - MEBC Financial Symposium v2Document12 pagesPERSONAL BUDGETING - MEBC Financial Symposium v2Ali ZiyanNo ratings yet

- Monzo Bank Statement 2024 01 01 2024 03 31 40 1Document10 pagesMonzo Bank Statement 2024 01 01 2024 03 31 40 1tsundereadamsNo ratings yet

- Seec F'orm 20Document23 pagesSeec F'orm 20The Valley IndyNo ratings yet

- Lic Jeevan Umang PlanDocument3 pagesLic Jeevan Umang PlanRAVINDRA SINGHNo ratings yet

- P9B2005 - Tax Free RenumerationDocument2 pagesP9B2005 - Tax Free RenumerationDavid SeweNo ratings yet

- Different Types of Debentures and Their UseDocument10 pagesDifferent Types of Debentures and Their UseMansangat Singh KohliNo ratings yet

- Annexure A-18 Declaration of Repatriation of Proceeds From Sale of Assets OR Maturity Proceeds Withdrawal of My InvestmentsDocument1 pageAnnexure A-18 Declaration of Repatriation of Proceeds From Sale of Assets OR Maturity Proceeds Withdrawal of My InvestmentstooheyshroffNo ratings yet

- SAVEINSTPL-3249953316714 001 SignedDocument14 pagesSAVEINSTPL-3249953316714 001 SignedAbhayNo ratings yet