Economic Footprint For The Canadian Commercial Helicopter Industry

Economic Footprint For The Canadian Commercial Helicopter Industry

You might also like

- Macroeconomics Canadian 5th Edition Mankiw Solutions ManualDocument25 pagesMacroeconomics Canadian 5th Edition Mankiw Solutions ManualMrJosephCruzMDfojy100% (55)

- 7100 Scheme of Work (For Examination From 2021)Document44 pages7100 Scheme of Work (For Examination From 2021)Saman NizamiNo ratings yet

- Solved Explain Where These Activities Appear in Japan S National Income andDocument1 pageSolved Explain Where These Activities Appear in Japan S National Income andM Bilal SaleemNo ratings yet

- Economics For Managers Online ON 5-2020 AT-2Document15 pagesEconomics For Managers Online ON 5-2020 AT-2Isabel WoodsNo ratings yet

- Senior Question SolveDocument5 pagesSenior Question SolveMD Hafizul Islam HafizNo ratings yet

- Assessing Export Industry: International ManagementDocument10 pagesAssessing Export Industry: International ManagementJanel BrincesNo ratings yet

- National Income Accounting: Adigrat University Department of Acfn MacroeconomicsDocument18 pagesNational Income Accounting: Adigrat University Department of Acfn Macroeconomicsabadi gebruNo ratings yet

- Aerospace Dec 4 12Document4 pagesAerospace Dec 4 12juddcochraneNo ratings yet

- Globalisation - Impcts On Indian EconomyDocument23 pagesGlobalisation - Impcts On Indian EconomyPrabhat MauryaNo ratings yet

- Oxford Economics Explaining Dubai's Aviation Model June 2011Document67 pagesOxford Economics Explaining Dubai's Aviation Model June 2011Saad AliNo ratings yet

- Abbb18 Global-Summary WebDocument8 pagesAbbb18 Global-Summary WebUsman GhaniNo ratings yet

- Measuring National Income: Nissan Car Plant On Tyne and WearDocument5 pagesMeasuring National Income: Nissan Car Plant On Tyne and WearprabhasrajuNo ratings yet

- GDP Quarterly ReportDocument8 pagesGDP Quarterly ReportRey CiaNo ratings yet

- Accounting and COVID 19Document15 pagesAccounting and COVID 19jeffreytoh1996No ratings yet

- National Income Accounting: Adigrat University Department of Acfn MacroeconomicsDocument18 pagesNational Income Accounting: Adigrat University Department of Acfn Macroeconomicsabadi gebruNo ratings yet

- MKTG 6650 - Individual AssignmentDocument14 pagesMKTG 6650 - Individual AssignmentShehriyar AhmedNo ratings yet

- Airline Industry Analysis - 1Document14 pagesAirline Industry Analysis - 1joshNo ratings yet

- Full Speed Ahead: Creating Green Jobs Through Freight Rail ExpansionDocument16 pagesFull Speed Ahead: Creating Green Jobs Through Freight Rail ExpansionProgressTXNo ratings yet

- The Following Year It Was Privatized by The Australian GovernmentDocument12 pagesThe Following Year It Was Privatized by The Australian Governmentfizza amjadNo ratings yet

- The Data of Macroeconomics: AcroeconomicsDocument54 pagesThe Data of Macroeconomics: Acroeconomicsaditya prudhviNo ratings yet

- APV MethodDocument18 pagesAPV Methodrohitoberoi11No ratings yet

- Econ - IB 1Document20 pagesEcon - IB 1SOURAV MONDAL100% (1)

- MKTG 6650 - Individual AssignmentDocument14 pagesMKTG 6650 - Individual AssignmentShehriyar AhmedNo ratings yet

- National - Income (1) & (11) & 2Document39 pagesNational - Income (1) & (11) & 2Gitanjali RajputNo ratings yet

- Solution Manual For Macroeconomics Canadian 5Th Edition Mankiw Scarth 1464168504 9781464168505 Full Chapter PDFDocument36 pagesSolution Manual For Macroeconomics Canadian 5Th Edition Mankiw Scarth 1464168504 9781464168505 Full Chapter PDFlinda.legendre519100% (22)

- Mankiw Chapter 2 Macroeconomics DataDocument54 pagesMankiw Chapter 2 Macroeconomics DataYusi Pramandari100% (2)

- Suggested Answer Intro To Macro & SOL (Students Upload)Document35 pagesSuggested Answer Intro To Macro & SOL (Students Upload)PotatoNo ratings yet

- KGAL Whitepaper The Corona Virus Outbreak - Impact On The Aviation Market April 2020Document8 pagesKGAL Whitepaper The Corona Virus Outbreak - Impact On The Aviation Market April 2020GrowlerJoeNo ratings yet

- Ekonomi MakroDocument24 pagesEkonomi MakroNovi NurainiNo ratings yet

- The Economic Impacts of A $1 Billion Annual Transportation Capital InvestmentDocument29 pagesThe Economic Impacts of A $1 Billion Annual Transportation Capital InvestmentThe Virginian-PilotNo ratings yet

- The Data of Macroeconomics (F19)Document11 pagesThe Data of Macroeconomics (F19)周杨No ratings yet

- Reviewer in Social Science 3RD GradingDocument7 pagesReviewer in Social Science 3RD GradingCarlos, Jolina R.No ratings yet

- Slidestopic 2 LecDocument49 pagesSlidestopic 2 Lecmahmudulhaquenafi8No ratings yet

- Marketing Essay - Lime Mobility - UAEDocument11 pagesMarketing Essay - Lime Mobility - UAEStephanie CliffNo ratings yet

- Economics Set II QPDocument4 pagesEconomics Set II QPVihaan BalotiaNo ratings yet

- Chapter 1.1 National Income & The Circular Flow of IncomeDocument10 pagesChapter 1.1 National Income & The Circular Flow of Incomedianime OtakuNo ratings yet

- Unit 1Document80 pagesUnit 1Ridhima AggarwalNo ratings yet

- TCD Atlanta Airport Newsletter q1 2011Document3 pagesTCD Atlanta Airport Newsletter q1 2011Jan SauerNo ratings yet

- Aviation IndustryDocument28 pagesAviation Industrymayank3478No ratings yet

- Balance of Payment - FOREXDocument18 pagesBalance of Payment - FOREXSumit PaswanNo ratings yet

- Pest Factors & Impact On International BusinessDocument35 pagesPest Factors & Impact On International BusinessvorachiragNo ratings yet

- Macroeconomics Canadian 5th Edition Mankiw Solutions ManualDocument20 pagesMacroeconomics Canadian 5th Edition Mankiw Solutions Manualjakeabbottrlcmjn100% (24)

- Dwnload Full Macroeconomics Canadian 5th Edition Mankiw Solutions Manual PDFDocument35 pagesDwnload Full Macroeconomics Canadian 5th Edition Mankiw Solutions Manual PDFmichelettigeorgianna100% (12)

- M.8 Wir1998overview enDocument37 pagesM.8 Wir1998overview enanderson costa limaNo ratings yet

- The Annual Revenues in Billion Dollars in Financial Year 2001Document1 pageThe Annual Revenues in Billion Dollars in Financial Year 2001Taimur TechnologistNo ratings yet

- Capital Budgeting CSTDDocument3 pagesCapital Budgeting CSTDSardar FaaizNo ratings yet

- WEEK 8 Module 2 - Lesson 2Document12 pagesWEEK 8 Module 2 - Lesson 2Genner RazNo ratings yet

- Exhibit 1 - Wayne K. Stensby ReferralDocument81 pagesExhibit 1 - Wayne K. Stensby ReferralLa Isla OesteNo ratings yet

- Adsız DokümanDocument9 pagesAdsız Dokümangoldcagan2009No ratings yet

- Lecture Notes: MacroeconomicDocument31 pagesLecture Notes: MacroeconomicHassan Ali KhanNo ratings yet

- Week 1 Macro2Document55 pagesWeek 1 Macro219. Vũ Anh KhoaNo ratings yet

- Case StudyDocument2 pagesCase StudyPrincess JuanNo ratings yet

- Module IVDocument34 pagesModule IVAshNo ratings yet

- ECO 415 Chapter 8Document34 pagesECO 415 Chapter 8Nur NazirahNo ratings yet

- Airasia-Group 1Document15 pagesAirasia-Group 1salman1992No ratings yet

- Contribution of Aviation Industry To GDP of Different Countries and in PakistanDocument9 pagesContribution of Aviation Industry To GDP of Different Countries and in PakistanasadNo ratings yet

- Macroeconomics (ECO 101) : National Economy and National Income AnalysisDocument23 pagesMacroeconomics (ECO 101) : National Economy and National Income AnalysisERICK MLINGWANo ratings yet

- India Will Be The 6 Largest Emerging Market by 2012: Presented By: (Inmantec) ) Ranjeet Kumar (PGDM) 2007-09 BATCHDocument25 pagesIndia Will Be The 6 Largest Emerging Market by 2012: Presented By: (Inmantec) ) Ranjeet Kumar (PGDM) 2007-09 BATCHRitesh VermaNo ratings yet

- Class 12th QuestionBank EconomicsDocument114 pagesClass 12th QuestionBank Economicsgamacode132No ratings yet

- Key Financial StatementsDocument25 pagesKey Financial Statementsakhilesh kumarNo ratings yet

- Trade and Development Issues in CARICOM: Key Considerations for Navigating DevelopmentFrom EverandTrade and Development Issues in CARICOM: Key Considerations for Navigating DevelopmentRoger HoseinNo ratings yet

- Determinants of GRI-based Sustainability Reporting: Evidence From An Emerging EconomyDocument25 pagesDeterminants of GRI-based Sustainability Reporting: Evidence From An Emerging EconomyDessy Permata SariNo ratings yet

- The Economist - July 8thDocument88 pagesThe Economist - July 8thAbdulahad NabievNo ratings yet

- The Good Family PropertyDocument1 pageThe Good Family PropertyMichelle SolomonNo ratings yet

- Nama 10 LP Ulc Custom 6020699 SpreadsheetDocument11 pagesNama 10 LP Ulc Custom 6020699 Spreadsheetlesha leeNo ratings yet

- Get FileDocument70 pagesGet FileMichaelPatrickMcSweeneyNo ratings yet

- Chapter 15 Revised Incl Blaine Intro 2022Document40 pagesChapter 15 Revised Incl Blaine Intro 2022SSNo ratings yet

- Economics Ss1 3Document11 pagesEconomics Ss1 3tjahmed87No ratings yet

- Quiz Maceda LawDocument3 pagesQuiz Maceda LawchmaburdeosNo ratings yet

- Manulife Philippines Annual Report 2021 PDFDocument33 pagesManulife Philippines Annual Report 2021 PDFJannah Victoria AmoraNo ratings yet

- CH 04Document40 pagesCH 04gadox47306No ratings yet

- Chapter 11 SummaryDocument5 pagesChapter 11 Summarynjerunick3060No ratings yet

- 2015-06-11 Ec CP Approval Decision C 2015 4053 Commission Implementing DecisionDocument7 pages2015-06-11 Ec CP Approval Decision C 2015 4053 Commission Implementing DecisionTatjana GuberinicNo ratings yet

- Literature Review On Customer Satisfaction in Insurance SectorDocument8 pagesLiterature Review On Customer Satisfaction in Insurance SectordafobrrifNo ratings yet

- Inventories NotesDocument7 pagesInventories NotesJessel Ann MontecilloNo ratings yet

- Emebet Tesema The Proposal Focuses On Effectiveness of Inventory Management Practice in CaseDocument29 pagesEmebet Tesema The Proposal Focuses On Effectiveness of Inventory Management Practice in Caseyedinkachaw shferawNo ratings yet

- 2011 1 Amcr 99Document15 pages2011 1 Amcr 99Joanne PriyaNo ratings yet

- Unit 3Document20 pagesUnit 3Ram KrishnaNo ratings yet

- PRO0750 Smart Value Income Plan BrochureDocument10 pagesPRO0750 Smart Value Income Plan BrochureJignesh PatelNo ratings yet

- ElectricityToday - Jul 27 2023Document8 pagesElectricityToday - Jul 27 2023jonazakNo ratings yet

- Economics 181 International Trade Homework 3 SolutionsDocument4 pagesEconomics 181 International Trade Homework 3 Solutionsh4a0nawc100% (2)

- The Political Environment A Critical Concern Chapter 6Document44 pagesThe Political Environment A Critical Concern Chapter 6Gabriela PachecoNo ratings yet

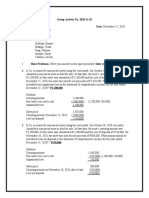

- Group Activity No. 2-Noncurrent Asset Held For Sale-2Document3 pagesGroup Activity No. 2-Noncurrent Asset Held For Sale-2Jericho VillalonNo ratings yet

- Kpi Ach 27 Desember 2021Document53 pagesKpi Ach 27 Desember 2021Rizki KurniadiNo ratings yet

- 67 5 2 - AccountancyDocument32 pages67 5 2 - Accountancydakshparashar973No ratings yet

- Capital Budgeting V2 - Click Read Only To View DocumentDocument40 pagesCapital Budgeting V2 - Click Read Only To View Documentzia hussain100% (1)

- Visanet FactsheetDocument1 pageVisanet Factsheetsalesuse2shopNo ratings yet

- Kalihari Port ProjectDocument12 pagesKalihari Port ProjectNandini sNo ratings yet

- Mushak 9.1 UpdatedDocument15 pagesMushak 9.1 UpdatedRakibul HassanNo ratings yet

- Diluted Earnings Per ShareDocument14 pagesDiluted Earnings Per Share2022920039No ratings yet

Download as pdf or txt

You might also like

- Macroeconomics Canadian 5th Edition Mankiw Solutions ManualDocument25 pagesMacroeconomics Canadian 5th Edition Mankiw Solutions ManualMrJosephCruzMDfojy100% (55)

- 7100 Scheme of Work (For Examination From 2021)Document44 pages7100 Scheme of Work (For Examination From 2021)Saman NizamiNo ratings yet

- Solved Explain Where These Activities Appear in Japan S National Income andDocument1 pageSolved Explain Where These Activities Appear in Japan S National Income andM Bilal SaleemNo ratings yet

- Economics For Managers Online ON 5-2020 AT-2Document15 pagesEconomics For Managers Online ON 5-2020 AT-2Isabel WoodsNo ratings yet

- Senior Question SolveDocument5 pagesSenior Question SolveMD Hafizul Islam HafizNo ratings yet

- Assessing Export Industry: International ManagementDocument10 pagesAssessing Export Industry: International ManagementJanel BrincesNo ratings yet

- National Income Accounting: Adigrat University Department of Acfn MacroeconomicsDocument18 pagesNational Income Accounting: Adigrat University Department of Acfn Macroeconomicsabadi gebruNo ratings yet

- Aerospace Dec 4 12Document4 pagesAerospace Dec 4 12juddcochraneNo ratings yet

- Globalisation - Impcts On Indian EconomyDocument23 pagesGlobalisation - Impcts On Indian EconomyPrabhat MauryaNo ratings yet

- Oxford Economics Explaining Dubai's Aviation Model June 2011Document67 pagesOxford Economics Explaining Dubai's Aviation Model June 2011Saad AliNo ratings yet

- Abbb18 Global-Summary WebDocument8 pagesAbbb18 Global-Summary WebUsman GhaniNo ratings yet

- Measuring National Income: Nissan Car Plant On Tyne and WearDocument5 pagesMeasuring National Income: Nissan Car Plant On Tyne and WearprabhasrajuNo ratings yet

- GDP Quarterly ReportDocument8 pagesGDP Quarterly ReportRey CiaNo ratings yet

- Accounting and COVID 19Document15 pagesAccounting and COVID 19jeffreytoh1996No ratings yet

- National Income Accounting: Adigrat University Department of Acfn MacroeconomicsDocument18 pagesNational Income Accounting: Adigrat University Department of Acfn Macroeconomicsabadi gebruNo ratings yet

- MKTG 6650 - Individual AssignmentDocument14 pagesMKTG 6650 - Individual AssignmentShehriyar AhmedNo ratings yet

- Airline Industry Analysis - 1Document14 pagesAirline Industry Analysis - 1joshNo ratings yet

- Full Speed Ahead: Creating Green Jobs Through Freight Rail ExpansionDocument16 pagesFull Speed Ahead: Creating Green Jobs Through Freight Rail ExpansionProgressTXNo ratings yet

- The Following Year It Was Privatized by The Australian GovernmentDocument12 pagesThe Following Year It Was Privatized by The Australian Governmentfizza amjadNo ratings yet

- The Data of Macroeconomics: AcroeconomicsDocument54 pagesThe Data of Macroeconomics: Acroeconomicsaditya prudhviNo ratings yet

- APV MethodDocument18 pagesAPV Methodrohitoberoi11No ratings yet

- Econ - IB 1Document20 pagesEcon - IB 1SOURAV MONDAL100% (1)

- MKTG 6650 - Individual AssignmentDocument14 pagesMKTG 6650 - Individual AssignmentShehriyar AhmedNo ratings yet

- National - Income (1) & (11) & 2Document39 pagesNational - Income (1) & (11) & 2Gitanjali RajputNo ratings yet

- Solution Manual For Macroeconomics Canadian 5Th Edition Mankiw Scarth 1464168504 9781464168505 Full Chapter PDFDocument36 pagesSolution Manual For Macroeconomics Canadian 5Th Edition Mankiw Scarth 1464168504 9781464168505 Full Chapter PDFlinda.legendre519100% (22)

- Mankiw Chapter 2 Macroeconomics DataDocument54 pagesMankiw Chapter 2 Macroeconomics DataYusi Pramandari100% (2)

- Suggested Answer Intro To Macro & SOL (Students Upload)Document35 pagesSuggested Answer Intro To Macro & SOL (Students Upload)PotatoNo ratings yet

- KGAL Whitepaper The Corona Virus Outbreak - Impact On The Aviation Market April 2020Document8 pagesKGAL Whitepaper The Corona Virus Outbreak - Impact On The Aviation Market April 2020GrowlerJoeNo ratings yet

- Ekonomi MakroDocument24 pagesEkonomi MakroNovi NurainiNo ratings yet

- The Economic Impacts of A $1 Billion Annual Transportation Capital InvestmentDocument29 pagesThe Economic Impacts of A $1 Billion Annual Transportation Capital InvestmentThe Virginian-PilotNo ratings yet

- The Data of Macroeconomics (F19)Document11 pagesThe Data of Macroeconomics (F19)周杨No ratings yet

- Reviewer in Social Science 3RD GradingDocument7 pagesReviewer in Social Science 3RD GradingCarlos, Jolina R.No ratings yet

- Slidestopic 2 LecDocument49 pagesSlidestopic 2 Lecmahmudulhaquenafi8No ratings yet

- Marketing Essay - Lime Mobility - UAEDocument11 pagesMarketing Essay - Lime Mobility - UAEStephanie CliffNo ratings yet

- Economics Set II QPDocument4 pagesEconomics Set II QPVihaan BalotiaNo ratings yet

- Chapter 1.1 National Income & The Circular Flow of IncomeDocument10 pagesChapter 1.1 National Income & The Circular Flow of Incomedianime OtakuNo ratings yet

- Unit 1Document80 pagesUnit 1Ridhima AggarwalNo ratings yet

- TCD Atlanta Airport Newsletter q1 2011Document3 pagesTCD Atlanta Airport Newsletter q1 2011Jan SauerNo ratings yet

- Aviation IndustryDocument28 pagesAviation Industrymayank3478No ratings yet

- Balance of Payment - FOREXDocument18 pagesBalance of Payment - FOREXSumit PaswanNo ratings yet

- Pest Factors & Impact On International BusinessDocument35 pagesPest Factors & Impact On International BusinessvorachiragNo ratings yet

- Macroeconomics Canadian 5th Edition Mankiw Solutions ManualDocument20 pagesMacroeconomics Canadian 5th Edition Mankiw Solutions Manualjakeabbottrlcmjn100% (24)

- Dwnload Full Macroeconomics Canadian 5th Edition Mankiw Solutions Manual PDFDocument35 pagesDwnload Full Macroeconomics Canadian 5th Edition Mankiw Solutions Manual PDFmichelettigeorgianna100% (12)

- M.8 Wir1998overview enDocument37 pagesM.8 Wir1998overview enanderson costa limaNo ratings yet

- The Annual Revenues in Billion Dollars in Financial Year 2001Document1 pageThe Annual Revenues in Billion Dollars in Financial Year 2001Taimur TechnologistNo ratings yet

- Capital Budgeting CSTDDocument3 pagesCapital Budgeting CSTDSardar FaaizNo ratings yet

- WEEK 8 Module 2 - Lesson 2Document12 pagesWEEK 8 Module 2 - Lesson 2Genner RazNo ratings yet

- Exhibit 1 - Wayne K. Stensby ReferralDocument81 pagesExhibit 1 - Wayne K. Stensby ReferralLa Isla OesteNo ratings yet

- Adsız DokümanDocument9 pagesAdsız Dokümangoldcagan2009No ratings yet

- Lecture Notes: MacroeconomicDocument31 pagesLecture Notes: MacroeconomicHassan Ali KhanNo ratings yet

- Week 1 Macro2Document55 pagesWeek 1 Macro219. Vũ Anh KhoaNo ratings yet

- Case StudyDocument2 pagesCase StudyPrincess JuanNo ratings yet

- Module IVDocument34 pagesModule IVAshNo ratings yet

- ECO 415 Chapter 8Document34 pagesECO 415 Chapter 8Nur NazirahNo ratings yet

- Airasia-Group 1Document15 pagesAirasia-Group 1salman1992No ratings yet

- Contribution of Aviation Industry To GDP of Different Countries and in PakistanDocument9 pagesContribution of Aviation Industry To GDP of Different Countries and in PakistanasadNo ratings yet

- Macroeconomics (ECO 101) : National Economy and National Income AnalysisDocument23 pagesMacroeconomics (ECO 101) : National Economy and National Income AnalysisERICK MLINGWANo ratings yet

- India Will Be The 6 Largest Emerging Market by 2012: Presented By: (Inmantec) ) Ranjeet Kumar (PGDM) 2007-09 BATCHDocument25 pagesIndia Will Be The 6 Largest Emerging Market by 2012: Presented By: (Inmantec) ) Ranjeet Kumar (PGDM) 2007-09 BATCHRitesh VermaNo ratings yet

- Class 12th QuestionBank EconomicsDocument114 pagesClass 12th QuestionBank Economicsgamacode132No ratings yet

- Key Financial StatementsDocument25 pagesKey Financial Statementsakhilesh kumarNo ratings yet

- Trade and Development Issues in CARICOM: Key Considerations for Navigating DevelopmentFrom EverandTrade and Development Issues in CARICOM: Key Considerations for Navigating DevelopmentRoger HoseinNo ratings yet

- Determinants of GRI-based Sustainability Reporting: Evidence From An Emerging EconomyDocument25 pagesDeterminants of GRI-based Sustainability Reporting: Evidence From An Emerging EconomyDessy Permata SariNo ratings yet

- The Economist - July 8thDocument88 pagesThe Economist - July 8thAbdulahad NabievNo ratings yet

- The Good Family PropertyDocument1 pageThe Good Family PropertyMichelle SolomonNo ratings yet

- Nama 10 LP Ulc Custom 6020699 SpreadsheetDocument11 pagesNama 10 LP Ulc Custom 6020699 Spreadsheetlesha leeNo ratings yet

- Get FileDocument70 pagesGet FileMichaelPatrickMcSweeneyNo ratings yet

- Chapter 15 Revised Incl Blaine Intro 2022Document40 pagesChapter 15 Revised Incl Blaine Intro 2022SSNo ratings yet

- Economics Ss1 3Document11 pagesEconomics Ss1 3tjahmed87No ratings yet

- Quiz Maceda LawDocument3 pagesQuiz Maceda LawchmaburdeosNo ratings yet

- Manulife Philippines Annual Report 2021 PDFDocument33 pagesManulife Philippines Annual Report 2021 PDFJannah Victoria AmoraNo ratings yet

- CH 04Document40 pagesCH 04gadox47306No ratings yet

- Chapter 11 SummaryDocument5 pagesChapter 11 Summarynjerunick3060No ratings yet

- 2015-06-11 Ec CP Approval Decision C 2015 4053 Commission Implementing DecisionDocument7 pages2015-06-11 Ec CP Approval Decision C 2015 4053 Commission Implementing DecisionTatjana GuberinicNo ratings yet

- Literature Review On Customer Satisfaction in Insurance SectorDocument8 pagesLiterature Review On Customer Satisfaction in Insurance SectordafobrrifNo ratings yet

- Inventories NotesDocument7 pagesInventories NotesJessel Ann MontecilloNo ratings yet

- Emebet Tesema The Proposal Focuses On Effectiveness of Inventory Management Practice in CaseDocument29 pagesEmebet Tesema The Proposal Focuses On Effectiveness of Inventory Management Practice in Caseyedinkachaw shferawNo ratings yet

- 2011 1 Amcr 99Document15 pages2011 1 Amcr 99Joanne PriyaNo ratings yet

- Unit 3Document20 pagesUnit 3Ram KrishnaNo ratings yet

- PRO0750 Smart Value Income Plan BrochureDocument10 pagesPRO0750 Smart Value Income Plan BrochureJignesh PatelNo ratings yet

- ElectricityToday - Jul 27 2023Document8 pagesElectricityToday - Jul 27 2023jonazakNo ratings yet

- Economics 181 International Trade Homework 3 SolutionsDocument4 pagesEconomics 181 International Trade Homework 3 Solutionsh4a0nawc100% (2)

- The Political Environment A Critical Concern Chapter 6Document44 pagesThe Political Environment A Critical Concern Chapter 6Gabriela PachecoNo ratings yet

- Group Activity No. 2-Noncurrent Asset Held For Sale-2Document3 pagesGroup Activity No. 2-Noncurrent Asset Held For Sale-2Jericho VillalonNo ratings yet

- Kpi Ach 27 Desember 2021Document53 pagesKpi Ach 27 Desember 2021Rizki KurniadiNo ratings yet

- 67 5 2 - AccountancyDocument32 pages67 5 2 - Accountancydakshparashar973No ratings yet

- Capital Budgeting V2 - Click Read Only To View DocumentDocument40 pagesCapital Budgeting V2 - Click Read Only To View Documentzia hussain100% (1)

- Visanet FactsheetDocument1 pageVisanet Factsheetsalesuse2shopNo ratings yet

- Kalihari Port ProjectDocument12 pagesKalihari Port ProjectNandini sNo ratings yet

- Mushak 9.1 UpdatedDocument15 pagesMushak 9.1 UpdatedRakibul HassanNo ratings yet

- Diluted Earnings Per ShareDocument14 pagesDiluted Earnings Per Share2022920039No ratings yet