Download as pdf or txt

You might also like

- Macroeconomics Canadian 5th Edition Mankiw Solutions ManualDocument25 pagesMacroeconomics Canadian 5th Edition Mankiw Solutions ManualMrJosephCruzMDfojy100% (54)

- How I Cured My Eye FloatersDocument6 pagesHow I Cured My Eye Floaters54321anon100% (2)

- Credit Policy Sample: Accounts Receivable AnalysisDocument3 pagesCredit Policy Sample: Accounts Receivable AnalysisAlinaNo ratings yet

- Character CreationDocument36 pagesCharacter CreationGracia Gagah100% (2)

- Quarterly Economic Bulletin - Sep 2023Document94 pagesQuarterly Economic Bulletin - Sep 2023Denis EliasNo ratings yet

- Economic PillarDocument4 pagesEconomic PillarAwarun EmmanuelNo ratings yet

- Section 1Document20 pagesSection 1EdwardNo ratings yet

- Nepal Macroeconomic Update 202309Document42 pagesNepal Macroeconomic Update 202309Saurabh ZhaaNo ratings yet

- Byblos Bank - CRWB-781Document10 pagesByblos Bank - CRWB-781Abeerh HallakNo ratings yet

- Market ResearchDocument4 pagesMarket ResearchAkhil sonuNo ratings yet

- Economic Activities of Ghana in The 2021 PHCDocument1 pageEconomic Activities of Ghana in The 2021 PHCkoomsonsilas8585No ratings yet

- Quartely Economic Bulletin - BOTDocument95 pagesQuartely Economic Bulletin - BOTEliezer Charles NgahyomaNo ratings yet

- Economic Update October 2022Document11 pagesEconomic Update October 2022Samya MuhammadNo ratings yet

- Turkey - Economic Studies - CofaceDocument2 pagesTurkey - Economic Studies - CofaceTifani RosaNo ratings yet

- Bengladesh Economic Review 2023 Chapter-6Document22 pagesBengladesh Economic Review 2023 Chapter-6Md. Abdur RakibNo ratings yet

- VGI Initiation 20181003 REDUCEDocument21 pagesVGI Initiation 20181003 REDUCEShan YoongNo ratings yet

- Economy of Sri LankaDocument24 pagesEconomy of Sri LankaAman DecoraterNo ratings yet

- Global Economic Prospects: South Asia: June 2020Document2 pagesGlobal Economic Prospects: South Asia: June 2020michel mboueNo ratings yet

- Bharti Airtel: Strong Growth in AfricaDocument13 pagesBharti Airtel: Strong Growth in AfricaJayJairamNo ratings yet

- Economic and Financial EnvironmentDocument11 pagesEconomic and Financial EnvironmentKent Leo BatuigasNo ratings yet

- CTI7 - 1 Rev 1 - Item 2 - Trends Reissued - 0Document20 pagesCTI7 - 1 Rev 1 - Item 2 - Trends Reissued - 0BRIJESHA MOHANTYNo ratings yet

- Viet Nam: Economic PerformanceDocument5 pagesViet Nam: Economic Performanceapi-3733336100% (1)

- Global Economic Prospects Jan 2019 Sub Saharan AfricaanalysisDocument20 pagesGlobal Economic Prospects Jan 2019 Sub Saharan Africaanalysiswebsterjemwa46No ratings yet

- Quarterly Economic Profile - FINAL - July 2023Document16 pagesQuarterly Economic Profile - FINAL - July 2023Binyam TayeNo ratings yet

- Global Investment Trends Monitor 42 (UNCTAD) Oct 2022Document5 pagesGlobal Investment Trends Monitor 42 (UNCTAD) Oct 2022Vương VõNo ratings yet

- ESCAP 2022 RP Trade Trends Goods Services Asia PacificDocument17 pagesESCAP 2022 RP Trade Trends Goods Services Asia PacificimamsetiadiNo ratings yet

- Viet Nam Market Pulse - Shared by WorldLine Technology-1Document21 pagesViet Nam Market Pulse - Shared by WorldLine Technology-1CHIÊM HÀNo ratings yet

- SPB Egypt's Currency DevaluationDocument12 pagesSPB Egypt's Currency DevaluationAhmed El ZareiNo ratings yet

- Vanuatu: Economic PerformanceDocument3 pagesVanuatu: Economic PerformanceViliame TawanakoroNo ratings yet

- Argentina - Economic Studies - CofaceDocument2 pagesArgentina - Economic Studies - CofaceTifani RosaNo ratings yet

- 15124-CardinalStone Research 2022 Macro Outlook Consolidating Recovery-ProshareDocument16 pages15124-CardinalStone Research 2022 Macro Outlook Consolidating Recovery-ProshareOladipo OlanyiNo ratings yet

- 2023 Asia Partners Internet ReportDocument332 pages2023 Asia Partners Internet ReportBen SetoNo ratings yet

- Budget Bulletin 2022 23Document27 pagesBudget Bulletin 2022 23Ssewanyana RonaldNo ratings yet

- NBG Macrooutlook FinalDocument14 pagesNBG Macrooutlook FinalLucas HOSTETTERNo ratings yet

- Report On MoroccoDocument10 pagesReport On Moroccoaimajunaid06No ratings yet

- Dubai Chamber Economist August 2010 Issue 34Document4 pagesDubai Chamber Economist August 2010 Issue 34BRR_DAGNo ratings yet

- Afrinvest August Monthly Market Review 1693659339Document16 pagesAfrinvest August Monthly Market Review 1693659339Krishan SapariaNo ratings yet

- Directors' Report: I. Economic Backdrop and Banking EnvironmentDocument53 pagesDirectors' Report: I. Economic Backdrop and Banking EnvironmentPuja BhallaNo ratings yet

- Country Risk Weekly Bulletin News Headlines: World MenaDocument10 pagesCountry Risk Weekly Bulletin News Headlines: World MenaHuante KandraNo ratings yet

- Data Center in The GambiaDocument18 pagesData Center in The Gambialalou4No ratings yet

- Aeo 2021 - Chap1 - enDocument38 pagesAeo 2021 - Chap1 - enkangwak27No ratings yet

- Global Economic Prospects - SubSaharan Africa AnalysisDocument20 pagesGlobal Economic Prospects - SubSaharan Africa Analysisbello imamNo ratings yet

- Global Economic Crisis and Macroeconomic Challenges For BangladeshDocument21 pagesGlobal Economic Crisis and Macroeconomic Challenges For BangladeshByezid LimonNo ratings yet

- KBSV - Macro Outlook 2Q - 2019Document16 pagesKBSV - Macro Outlook 2Q - 2019LinhNo ratings yet

- Economic Impact of CovidDocument7 pagesEconomic Impact of Covidrishi pereraNo ratings yet

- RESEARCH - Mobile Banking in The GambiaDocument10 pagesRESEARCH - Mobile Banking in The Gambiadaniel koikiNo ratings yet

- Indonesia Economic Update 2023 q2Document18 pagesIndonesia Economic Update 2023 q2Jaeysen CanilyNo ratings yet

- State of The UAE Retail Economy Q4-2022Document46 pagesState of The UAE Retail Economy Q4-2022Anirudh MahiNo ratings yet

- Nepal - Economic Studies - CofaceDocument2 pagesNepal - Economic Studies - CofaceMotiram paudelNo ratings yet

- Asia Partners 2019 Southeast Asia Internet Report PDFDocument77 pagesAsia Partners 2019 Southeast Asia Internet Report PDFRickyNo ratings yet

- Safari - 28 Jul 2022 at 9:02 PMDocument1 pageSafari - 28 Jul 2022 at 9:02 PMmrosemuelNo ratings yet

- The Effect of Commercial Banks Credit On Agricultural Sector's Contribution To Real Gross Domestic Product Evidence From Nigeria 1986 To 2020Document8 pagesThe Effect of Commercial Banks Credit On Agricultural Sector's Contribution To Real Gross Domestic Product Evidence From Nigeria 1986 To 2020Editor IJTSRDNo ratings yet

- BNPparibas Vietnam 10.13.05Document2 pagesBNPparibas Vietnam 10.13.05Anh TúNo ratings yet

- Economic Survey Summary 2022-23 EnglishDocument2 pagesEconomic Survey Summary 2022-23 EnglishKavya KaurNo ratings yet

- Page 5Document1 pagePage 5Nguyen ThuNo ratings yet

- Pacific Finance Sector Papua New GuineaDocument5 pagesPacific Finance Sector Papua New Guineaalfred kas Simon Lucas KasNo ratings yet

- 2borders ProjectDocument3 pages2borders ProjectBroadband Career Management in AINo ratings yet

- Nigeria +Macro-economic+and+Banking+Themes+for+2019+2019+Macro-economic+Outlook 26012019Document10 pagesNigeria +Macro-economic+and+Banking+Themes+for+2019+2019+Macro-economic+Outlook 26012019crystalNo ratings yet

- Dangote Cement FY2023 Results Statement FinalDocument12 pagesDangote Cement FY2023 Results Statement Finalokekeifechi21No ratings yet

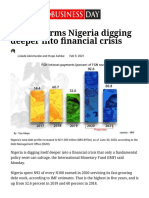

- IMF Confirms Nigeria Digging Deeper Into Financial Crisis - Businessday NGDocument4 pagesIMF Confirms Nigeria Digging Deeper Into Financial Crisis - Businessday NGAnneNo ratings yet

- Research and Forecast ReportDocument12 pagesResearch and Forecast Reportrisa dyNo ratings yet

- 2021 Macro Economic OutlookDocument18 pages2021 Macro Economic Outlookikperha jomafuvweNo ratings yet

- Cambodia Agriculture, Natural Resources, and Rural Development Sector Assessment, Strategy, and Road MapFrom EverandCambodia Agriculture, Natural Resources, and Rural Development Sector Assessment, Strategy, and Road MapNo ratings yet

- English in The Middle AgesDocument216 pagesEnglish in The Middle AgesAna Basarte100% (2)

- Effective Written CommunicationDocument3 pagesEffective Written CommunicationSudeb SarkarNo ratings yet

- Bba 820 - Managerial Functions - Blended ModuleDocument73 pagesBba 820 - Managerial Functions - Blended Modulemichael kimNo ratings yet

- Classification of FinishesDocument5 pagesClassification of FinishesOjasvee Kashyap100% (1)

- BUS 500 Skills in Business Communication PDFDocument8 pagesBUS 500 Skills in Business Communication PDFrakin tajwarNo ratings yet

- Cesc 10021 BomDocument91 pagesCesc 10021 Bomsitam_nitj4202No ratings yet

- Gas Bill AprilDocument4 pagesGas Bill AprilMozhie OicangiNo ratings yet

- Forecasting ExamplesDocument14 pagesForecasting ExamplesJudith DelRosario De RoxasNo ratings yet

- Kunci Gitar Bruno Mars - Talking To The Moon Chord Dasar ©Document5 pagesKunci Gitar Bruno Mars - Talking To The Moon Chord Dasar ©eppypurnamaNo ratings yet

- Computational Techniques in Quantum Chemistry and Molecular PhysicsDocument569 pagesComputational Techniques in Quantum Chemistry and Molecular PhysicsClóvis Batista Dos SantosNo ratings yet

- Spill Kit ChecklistDocument1 pageSpill Kit Checklistmd rafiqueNo ratings yet

- Vertex OSeries v7.0 SR2 MP12 Release Notes - 5Document97 pagesVertex OSeries v7.0 SR2 MP12 Release Notes - 5Krishna MadhavaNo ratings yet

- Aventurian Herald #173Document6 pagesAventurian Herald #173Andrew CountsNo ratings yet

- Formulas To Know For Exam PDocument4 pagesFormulas To Know For Exam Pkevin.nguyen268998No ratings yet

- Good To Great in Gods Eyes. Good To Great in God's Eyes (Part 1) Think Great Thoughts 10 Practices Great Christians Have in CommonDocument4 pagesGood To Great in Gods Eyes. Good To Great in God's Eyes (Part 1) Think Great Thoughts 10 Practices Great Christians Have in Commonad.adNo ratings yet

- Glaciers Notes Part 1Document6 pagesGlaciers Notes Part 1David ZhaoNo ratings yet

- Plan For Contract ID No. 16CM0078 (Part2)Document17 pagesPlan For Contract ID No. 16CM0078 (Part2)Ab CdNo ratings yet

- Unit 1 - 18EC61Document93 pagesUnit 1 - 18EC61Pritam SarkarNo ratings yet

- Eugenio Ochoa GonzalezDocument3 pagesEugenio Ochoa GonzalezEugenio Ochoa GonzalezNo ratings yet

- SBARDocument2 pagesSBARNabiela Aswaty 2011125083No ratings yet

- Marinediesels - Co.uk - Members Section Starting and Reversing Sulzer ZA40 Air Start SystemDocument2 pagesMarinediesels - Co.uk - Members Section Starting and Reversing Sulzer ZA40 Air Start SystemArun SNo ratings yet

- LaGard LG Basic Manager InstructionsDocument2 pagesLaGard LG Basic Manager InstructionsGCNo ratings yet

- SSL Stripping Technique DHCP Snooping and ARP Spoofing InspectionDocument7 pagesSSL Stripping Technique DHCP Snooping and ARP Spoofing InspectionRMNo ratings yet

- Pentosan PDFDocument54 pagesPentosan PDFCinthia StephensNo ratings yet

- New TIP Course 1 DepEd Teacher PDFDocument89 pagesNew TIP Course 1 DepEd Teacher PDFLenie TejadaNo ratings yet

- Chapter Five Tractors and Related EquipmentDocument21 pagesChapter Five Tractors and Related EquipmentMicky AlemuNo ratings yet