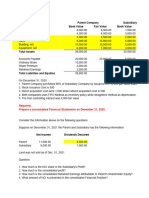

BusCom Part 1 Practice Set Solution

BusCom Part 1 Practice Set Solution

You might also like

- Sol. Man. Chapter 4 Consol. Fs Part 1Document37 pagesSol. Man. Chapter 4 Consol. Fs Part 1itsmenatoy43% (7)

- Abc & Management Case StudyDocument4 pagesAbc & Management Case StudyrajyalakshmiNo ratings yet

- Housing AssociationDocument30 pagesHousing AssociationgriffparryNo ratings yet

- Retailing Presentation of HardeesDocument23 pagesRetailing Presentation of HardeesFaizan Tufail Malik0% (2)

- AFAR 2 NotesDocument157 pagesAFAR 2 NotesAlexandria EvangelistaNo ratings yet

- BADVAC1XDocument8 pagesBADVAC1Xfaye pantiNo ratings yet

- Business CombinationDocument10 pagesBusiness CombinationJerome DizonNo ratings yet

- Chapter 1 Abc Suggested SolutionsDocument7 pagesChapter 1 Abc Suggested SolutionsAlthea Lyn ReyesNo ratings yet

- Business Combination - AcquisitionDocument16 pagesBusiness Combination - AcquisitionAries Gonzales CaraganNo ratings yet

- Owl Co. and Owlet Co. - NCI in Net AssetsDocument11 pagesOwl Co. and Owlet Co. - NCI in Net AssetsKristine Esplana ToraldeNo ratings yet

- Business Combination Subsequent To Date of Acquisition SolutionDocument3 pagesBusiness Combination Subsequent To Date of Acquisition SolutionGelliza Mae MontallaNo ratings yet

- 01 Control Premium and StepDocument15 pages01 Control Premium and StepANGELI GRACE GALVANNo ratings yet

- Quiz On Pension, Equity Investments - Answer KeyDocument3 pagesQuiz On Pension, Equity Investments - Answer KeyAlthea RubinNo ratings yet

- Castro, Geene - Activity 1 - Bsma 3205Document6 pagesCastro, Geene - Activity 1 - Bsma 3205Geene CastroNo ratings yet

- Final PB Exam - Answers - SolutionsDocument10 pagesFinal PB Exam - Answers - SolutionsJazehl ValdezNo ratings yet

- AFAR2 CH. 3 - Problem Quiz 1Document19 pagesAFAR2 CH. 3 - Problem Quiz 1Von Andrei MedinaNo ratings yet

- Business Combination at Date of Acquisition Problem 1Document8 pagesBusiness Combination at Date of Acquisition Problem 1Jason BautistaNo ratings yet

- Chap 4Document91 pagesChap 4randomlungs121223No ratings yet

- Interco Trans AnsDocument5 pagesInterco Trans Ansmartinfaith958No ratings yet

- Rulona, Kerby Gail P. Bsa-3A Problem 6 1. BDocument12 pagesRulona, Kerby Gail P. Bsa-3A Problem 6 1. BCassandra KarolinaNo ratings yet

- Module 2 AnswersDocument39 pagesModule 2 AnswersEy GuanlaoNo ratings yet

- Loan Loss Provision TaxDocument13 pagesLoan Loss Provision TaxSabin YadavNo ratings yet

- Quiz AE 120Document10 pagesQuiz AE 120Katrina MalecdanNo ratings yet

- ExampleDocument8 pagesExampleAli Akand AsifNo ratings yet

- Investment in Associate' 2Document9 pagesInvestment in Associate' 2Joefrey Pujadas BalumaNo ratings yet

- Year of SaleDocument12 pagesYear of SaleDarius DelacruzNo ratings yet

- 2076 - Varias, Aizel Ann B - Module 2Document20 pages2076 - Varias, Aizel Ann B - Module 2Aizel Ann VariasNo ratings yet

- Materi Accounting AdvancedDocument12 pagesMateri Accounting AdvancedRianty AstaniaNo ratings yet

- Chapter 4 - Consolidated Financial Statements (Part 1)Document32 pagesChapter 4 - Consolidated Financial Statements (Part 1)Philip RososNo ratings yet

- CH 27 - Ex 6Document11 pagesCH 27 - Ex 6Khandarmaa LkhagvaNo ratings yet

- Aud315 - Quizzes Solution PaperDocument6 pagesAud315 - Quizzes Solution PaperLorraineMartinNo ratings yet

- Responsiblity Accounting IllustrationDocument14 pagesResponsiblity Accounting IllustrationRianne NavidadNo ratings yet

- Solutions - Midterms Reviewer - Q1Document21 pagesSolutions - Midterms Reviewer - Q1Jack Herer100% (1)

- Chapter 4Document36 pagesChapter 4MARRIETTE JOY ABADNo ratings yet

- ACC 108 Debt RestructuringDocument24 pagesACC 108 Debt RestructuringMary PatalinghugNo ratings yet

- Accounting AssignmentDocument13 pagesAccounting AssignmentPetrinaNo ratings yet

- Advanced Accounting 2 - Chapter 4 James B. Cantorne Problem 1. T/FDocument7 pagesAdvanced Accounting 2 - Chapter 4 James B. Cantorne Problem 1. T/FJames CantorneNo ratings yet

- Particulars Debit CreditDocument10 pagesParticulars Debit CreditJasmine ActaNo ratings yet

- Compound Fnancial LiabDocument13 pagesCompound Fnancial LiabMary PatalinghugNo ratings yet

- Kaya Mo Yan-Finac - Chap 22 Investment PropertyDocument8 pagesKaya Mo Yan-Finac - Chap 22 Investment PropertyTrixie JeramieNo ratings yet

- Pension Part 1Document14 pagesPension Part 1Mary PatalinghugNo ratings yet

- Problem 5-1Document7 pagesProblem 5-1Tammy AckleyNo ratings yet

- Ffa ADocument5 pagesFfa Aaccounts officerNo ratings yet

- 9 & 10corporations - Final Tax, Capital Gains Tax, IAET and BPRT (Module 9 & 10) IllustrationsDocument4 pages9 & 10corporations - Final Tax, Capital Gains Tax, IAET and BPRT (Module 9 & 10) IllustrationsRyan CartaNo ratings yet

- SolutionsDocument3 pagesSolutionsRENZEL MAGBITANGNo ratings yet

- Consolidation Sample ProblemDocument3 pagesConsolidation Sample ProblemLeila Nicole FulgencioNo ratings yet

- AE 315 FM Sum2021 Week 3 Capital Budgeting Quiz Anserki B FOR DISTRIBDocument7 pagesAE 315 FM Sum2021 Week 3 Capital Budgeting Quiz Anserki B FOR DISTRIBArly Kurt TorresNo ratings yet

- Suggested Answers Assignment Notes PayableDocument4 pagesSuggested Answers Assignment Notes PayableKeikoNo ratings yet

- 95 AFAR Final Preboard SolutionsDocument10 pages95 AFAR Final Preboard Solutions20100723No ratings yet

- Kaya Mo Yan-Finac - Investment PropertyDocument8 pagesKaya Mo Yan-Finac - Investment PropertyTrixie JeramieNo ratings yet

- Chapter 1 Afar (Bus Com)Document24 pagesChapter 1 Afar (Bus Com)jajajaredredNo ratings yet

- Quiz Chapter 5 Consol. Fs Part 2Document7 pagesQuiz Chapter 5 Consol. Fs Part 2Meagan AndesNo ratings yet

- Business CombinationDocument10 pagesBusiness CombinationJaira ClavoNo ratings yet

- The Remaining Percent of The Sea-Breeze Shares Traded Near A Total Value of 200,000Document5 pagesThe Remaining Percent of The Sea-Breeze Shares Traded Near A Total Value of 200,000RomerNo ratings yet

- MCQsDocument11 pagesMCQsAllaine RogadorNo ratings yet

- Chapter 4 & 5 AbcDocument16 pagesChapter 4 & 5 AbcAlthea Lyn ReyesNo ratings yet

- Bizcom Problem 3-2Document1 pageBizcom Problem 3-2kate trishaNo ratings yet

- Quiz 1 SolutionsDocument4 pagesQuiz 1 SolutionsLJ BNo ratings yet

- LeahDocument6 pagesLeahJoebin Corporal LopezNo ratings yet

- Adv Acc 2 Module 1 Topic1.2Document5 pagesAdv Acc 2 Module 1 Topic1.2James CantorneNo ratings yet

- FS Consolidation at The Date of Acquisition v2Document16 pagesFS Consolidation at The Date of Acquisition v2Pagatpat, Apple Grace C.No ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Wiley Practitioner's Guide to GAAS 2017: Covering all SASs, SSAEs, SSARSs, and InterpretationsFrom EverandWiley Practitioner's Guide to GAAS 2017: Covering all SASs, SSAEs, SSARSs, and InterpretationsNo ratings yet

- Sleep IndexDocument174 pagesSleep IndexJude CumayaoNo ratings yet

- Physical Activity EditedDocument37 pagesPhysical Activity EditedJude CumayaoNo ratings yet

- Max 2-14-24Document2 pagesMax 2-14-24Jude CumayaoNo ratings yet

- RSHS Season 12Document21 pagesRSHS Season 12Jude CumayaoNo ratings yet

- Eugene Frederick C. YapDocument1 pageEugene Frederick C. YapJude CumayaoNo ratings yet

- Business Plans: How Are They Important?Document15 pagesBusiness Plans: How Are They Important?林恩右No ratings yet

- Leading ChangeDocument2 pagesLeading ChangeKuya MikolNo ratings yet

- Call Center Job Duties and ResponsibilitiesDocument2 pagesCall Center Job Duties and ResponsibilitiesOlaya alghareniNo ratings yet

- IT Program Project Manager in Washington DC Resume Dan WolfeDocument2 pagesIT Program Project Manager in Washington DC Resume Dan WolfeDanWolfe1No ratings yet

- Ad No 09-2014Document36 pagesAd No 09-2014burhan_qureshiNo ratings yet

- Mgt657-Group-Project KK Super MartDocument45 pagesMgt657-Group-Project KK Super MartFaireez HanafiahNo ratings yet

- EISSN Human Resource Incon XI 2016 (1) Page 274Document315 pagesEISSN Human Resource Incon XI 2016 (1) Page 274Dyp alumniNo ratings yet

- Nestle - Case StudyDocument4 pagesNestle - Case StudyCha Castillo0% (1)

- Production and Operations Management EssayDocument4 pagesProduction and Operations Management EssayShalini Maharaj100% (1)

- Slaus 520Document10 pagesSlaus 520Charitha LakmalNo ratings yet

- AN-1408 HI6005 MOG (Topic 14) (3000w)Document12 pagesAN-1408 HI6005 MOG (Topic 14) (3000w)Mehran RazaNo ratings yet

- SLAU Brochure 2021 Combined 2Document8 pagesSLAU Brochure 2021 Combined 2JonathanNo ratings yet

- Piping Installation Verification Procedure:: How To Use This DocumentDocument2 pagesPiping Installation Verification Procedure:: How To Use This DocumentBasha Yazn AnjakNo ratings yet

- SlideEgg - Best PowerPoint Template ProviderDocument10 pagesSlideEgg - Best PowerPoint Template ProviderSlideEggNo ratings yet

- Cooperative Education Policies and Procedures ManualDocument163 pagesCooperative Education Policies and Procedures Manualrexcris100% (2)

- Chapter 1 The Demand For Audit and Other Assurance ServicesDocument14 pagesChapter 1 The Demand For Audit and Other Assurance ServicesSarah GherdaouiNo ratings yet

- Advanced Marketing Management Course OutlineDocument4 pagesAdvanced Marketing Management Course OutlineJecka DuyagNo ratings yet

- Introduction To Retail Management - Unit 3 - Week 2 - Retail Formats & StrategiesDocument4 pagesIntroduction To Retail Management - Unit 3 - Week 2 - Retail Formats & StrategiesCHANDAN C KAMATHNo ratings yet

- Accy 360 Final Exam Study GuideDocument5 pagesAccy 360 Final Exam Study Guidebigbear1010No ratings yet

- Sample Topics For Research Paper About AccountingDocument7 pagesSample Topics For Research Paper About Accountingaflbmfjse100% (1)

- Strategic Direction Through Purchasing Portfolio Management - A Case StudyDocument13 pagesStrategic Direction Through Purchasing Portfolio Management - A Case StudyAhmad TabassumNo ratings yet

- CRISC Syllabus Outline 1Document4 pagesCRISC Syllabus Outline 1SyedNo ratings yet

- Ratio Analysis On Renuka Sugars Ltd.Document77 pagesRatio Analysis On Renuka Sugars Ltd.Punardatt Bhat100% (1)

- Brand Life Cycle (BLC)Document16 pagesBrand Life Cycle (BLC)shubhamy69% (13)

- Chapter 8 Alternative Costing SystemsDocument21 pagesChapter 8 Alternative Costing SystemsSaad KhanNo ratings yet

- BBA - Operations Management Practices 102Document100 pagesBBA - Operations Management Practices 10221620168No ratings yet

- Empresa ILEDocument6 pagesEmpresa ILEVerónica AlcívarNo ratings yet

Download as xlsx, pdf, or txt

You might also like

- Sol. Man. Chapter 4 Consol. Fs Part 1Document37 pagesSol. Man. Chapter 4 Consol. Fs Part 1itsmenatoy43% (7)

- Abc & Management Case StudyDocument4 pagesAbc & Management Case StudyrajyalakshmiNo ratings yet

- Housing AssociationDocument30 pagesHousing AssociationgriffparryNo ratings yet

- Retailing Presentation of HardeesDocument23 pagesRetailing Presentation of HardeesFaizan Tufail Malik0% (2)

- AFAR 2 NotesDocument157 pagesAFAR 2 NotesAlexandria EvangelistaNo ratings yet

- BADVAC1XDocument8 pagesBADVAC1Xfaye pantiNo ratings yet

- Business CombinationDocument10 pagesBusiness CombinationJerome DizonNo ratings yet

- Chapter 1 Abc Suggested SolutionsDocument7 pagesChapter 1 Abc Suggested SolutionsAlthea Lyn ReyesNo ratings yet

- Business Combination - AcquisitionDocument16 pagesBusiness Combination - AcquisitionAries Gonzales CaraganNo ratings yet

- Owl Co. and Owlet Co. - NCI in Net AssetsDocument11 pagesOwl Co. and Owlet Co. - NCI in Net AssetsKristine Esplana ToraldeNo ratings yet

- Business Combination Subsequent To Date of Acquisition SolutionDocument3 pagesBusiness Combination Subsequent To Date of Acquisition SolutionGelliza Mae MontallaNo ratings yet

- 01 Control Premium and StepDocument15 pages01 Control Premium and StepANGELI GRACE GALVANNo ratings yet

- Quiz On Pension, Equity Investments - Answer KeyDocument3 pagesQuiz On Pension, Equity Investments - Answer KeyAlthea RubinNo ratings yet

- Castro, Geene - Activity 1 - Bsma 3205Document6 pagesCastro, Geene - Activity 1 - Bsma 3205Geene CastroNo ratings yet

- Final PB Exam - Answers - SolutionsDocument10 pagesFinal PB Exam - Answers - SolutionsJazehl ValdezNo ratings yet

- AFAR2 CH. 3 - Problem Quiz 1Document19 pagesAFAR2 CH. 3 - Problem Quiz 1Von Andrei MedinaNo ratings yet

- Business Combination at Date of Acquisition Problem 1Document8 pagesBusiness Combination at Date of Acquisition Problem 1Jason BautistaNo ratings yet

- Chap 4Document91 pagesChap 4randomlungs121223No ratings yet

- Interco Trans AnsDocument5 pagesInterco Trans Ansmartinfaith958No ratings yet

- Rulona, Kerby Gail P. Bsa-3A Problem 6 1. BDocument12 pagesRulona, Kerby Gail P. Bsa-3A Problem 6 1. BCassandra KarolinaNo ratings yet

- Module 2 AnswersDocument39 pagesModule 2 AnswersEy GuanlaoNo ratings yet

- Loan Loss Provision TaxDocument13 pagesLoan Loss Provision TaxSabin YadavNo ratings yet

- Quiz AE 120Document10 pagesQuiz AE 120Katrina MalecdanNo ratings yet

- ExampleDocument8 pagesExampleAli Akand AsifNo ratings yet

- Investment in Associate' 2Document9 pagesInvestment in Associate' 2Joefrey Pujadas BalumaNo ratings yet

- Year of SaleDocument12 pagesYear of SaleDarius DelacruzNo ratings yet

- 2076 - Varias, Aizel Ann B - Module 2Document20 pages2076 - Varias, Aizel Ann B - Module 2Aizel Ann VariasNo ratings yet

- Materi Accounting AdvancedDocument12 pagesMateri Accounting AdvancedRianty AstaniaNo ratings yet

- Chapter 4 - Consolidated Financial Statements (Part 1)Document32 pagesChapter 4 - Consolidated Financial Statements (Part 1)Philip RososNo ratings yet

- CH 27 - Ex 6Document11 pagesCH 27 - Ex 6Khandarmaa LkhagvaNo ratings yet

- Aud315 - Quizzes Solution PaperDocument6 pagesAud315 - Quizzes Solution PaperLorraineMartinNo ratings yet

- Responsiblity Accounting IllustrationDocument14 pagesResponsiblity Accounting IllustrationRianne NavidadNo ratings yet

- Solutions - Midterms Reviewer - Q1Document21 pagesSolutions - Midterms Reviewer - Q1Jack Herer100% (1)

- Chapter 4Document36 pagesChapter 4MARRIETTE JOY ABADNo ratings yet

- ACC 108 Debt RestructuringDocument24 pagesACC 108 Debt RestructuringMary PatalinghugNo ratings yet

- Accounting AssignmentDocument13 pagesAccounting AssignmentPetrinaNo ratings yet

- Advanced Accounting 2 - Chapter 4 James B. Cantorne Problem 1. T/FDocument7 pagesAdvanced Accounting 2 - Chapter 4 James B. Cantorne Problem 1. T/FJames CantorneNo ratings yet

- Particulars Debit CreditDocument10 pagesParticulars Debit CreditJasmine ActaNo ratings yet

- Compound Fnancial LiabDocument13 pagesCompound Fnancial LiabMary PatalinghugNo ratings yet

- Kaya Mo Yan-Finac - Chap 22 Investment PropertyDocument8 pagesKaya Mo Yan-Finac - Chap 22 Investment PropertyTrixie JeramieNo ratings yet

- Pension Part 1Document14 pagesPension Part 1Mary PatalinghugNo ratings yet

- Problem 5-1Document7 pagesProblem 5-1Tammy AckleyNo ratings yet

- Ffa ADocument5 pagesFfa Aaccounts officerNo ratings yet

- 9 & 10corporations - Final Tax, Capital Gains Tax, IAET and BPRT (Module 9 & 10) IllustrationsDocument4 pages9 & 10corporations - Final Tax, Capital Gains Tax, IAET and BPRT (Module 9 & 10) IllustrationsRyan CartaNo ratings yet

- SolutionsDocument3 pagesSolutionsRENZEL MAGBITANGNo ratings yet

- Consolidation Sample ProblemDocument3 pagesConsolidation Sample ProblemLeila Nicole FulgencioNo ratings yet

- AE 315 FM Sum2021 Week 3 Capital Budgeting Quiz Anserki B FOR DISTRIBDocument7 pagesAE 315 FM Sum2021 Week 3 Capital Budgeting Quiz Anserki B FOR DISTRIBArly Kurt TorresNo ratings yet

- Suggested Answers Assignment Notes PayableDocument4 pagesSuggested Answers Assignment Notes PayableKeikoNo ratings yet

- 95 AFAR Final Preboard SolutionsDocument10 pages95 AFAR Final Preboard Solutions20100723No ratings yet

- Kaya Mo Yan-Finac - Investment PropertyDocument8 pagesKaya Mo Yan-Finac - Investment PropertyTrixie JeramieNo ratings yet

- Chapter 1 Afar (Bus Com)Document24 pagesChapter 1 Afar (Bus Com)jajajaredredNo ratings yet

- Quiz Chapter 5 Consol. Fs Part 2Document7 pagesQuiz Chapter 5 Consol. Fs Part 2Meagan AndesNo ratings yet

- Business CombinationDocument10 pagesBusiness CombinationJaira ClavoNo ratings yet

- The Remaining Percent of The Sea-Breeze Shares Traded Near A Total Value of 200,000Document5 pagesThe Remaining Percent of The Sea-Breeze Shares Traded Near A Total Value of 200,000RomerNo ratings yet

- MCQsDocument11 pagesMCQsAllaine RogadorNo ratings yet

- Chapter 4 & 5 AbcDocument16 pagesChapter 4 & 5 AbcAlthea Lyn ReyesNo ratings yet

- Bizcom Problem 3-2Document1 pageBizcom Problem 3-2kate trishaNo ratings yet

- Quiz 1 SolutionsDocument4 pagesQuiz 1 SolutionsLJ BNo ratings yet

- LeahDocument6 pagesLeahJoebin Corporal LopezNo ratings yet

- Adv Acc 2 Module 1 Topic1.2Document5 pagesAdv Acc 2 Module 1 Topic1.2James CantorneNo ratings yet

- FS Consolidation at The Date of Acquisition v2Document16 pagesFS Consolidation at The Date of Acquisition v2Pagatpat, Apple Grace C.No ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Wiley Practitioner's Guide to GAAS 2017: Covering all SASs, SSAEs, SSARSs, and InterpretationsFrom EverandWiley Practitioner's Guide to GAAS 2017: Covering all SASs, SSAEs, SSARSs, and InterpretationsNo ratings yet

- Sleep IndexDocument174 pagesSleep IndexJude CumayaoNo ratings yet

- Physical Activity EditedDocument37 pagesPhysical Activity EditedJude CumayaoNo ratings yet

- Max 2-14-24Document2 pagesMax 2-14-24Jude CumayaoNo ratings yet

- RSHS Season 12Document21 pagesRSHS Season 12Jude CumayaoNo ratings yet

- Eugene Frederick C. YapDocument1 pageEugene Frederick C. YapJude CumayaoNo ratings yet

- Business Plans: How Are They Important?Document15 pagesBusiness Plans: How Are They Important?林恩右No ratings yet

- Leading ChangeDocument2 pagesLeading ChangeKuya MikolNo ratings yet

- Call Center Job Duties and ResponsibilitiesDocument2 pagesCall Center Job Duties and ResponsibilitiesOlaya alghareniNo ratings yet

- IT Program Project Manager in Washington DC Resume Dan WolfeDocument2 pagesIT Program Project Manager in Washington DC Resume Dan WolfeDanWolfe1No ratings yet

- Ad No 09-2014Document36 pagesAd No 09-2014burhan_qureshiNo ratings yet

- Mgt657-Group-Project KK Super MartDocument45 pagesMgt657-Group-Project KK Super MartFaireez HanafiahNo ratings yet

- EISSN Human Resource Incon XI 2016 (1) Page 274Document315 pagesEISSN Human Resource Incon XI 2016 (1) Page 274Dyp alumniNo ratings yet

- Nestle - Case StudyDocument4 pagesNestle - Case StudyCha Castillo0% (1)

- Production and Operations Management EssayDocument4 pagesProduction and Operations Management EssayShalini Maharaj100% (1)

- Slaus 520Document10 pagesSlaus 520Charitha LakmalNo ratings yet

- AN-1408 HI6005 MOG (Topic 14) (3000w)Document12 pagesAN-1408 HI6005 MOG (Topic 14) (3000w)Mehran RazaNo ratings yet

- SLAU Brochure 2021 Combined 2Document8 pagesSLAU Brochure 2021 Combined 2JonathanNo ratings yet

- Piping Installation Verification Procedure:: How To Use This DocumentDocument2 pagesPiping Installation Verification Procedure:: How To Use This DocumentBasha Yazn AnjakNo ratings yet

- SlideEgg - Best PowerPoint Template ProviderDocument10 pagesSlideEgg - Best PowerPoint Template ProviderSlideEggNo ratings yet

- Cooperative Education Policies and Procedures ManualDocument163 pagesCooperative Education Policies and Procedures Manualrexcris100% (2)

- Chapter 1 The Demand For Audit and Other Assurance ServicesDocument14 pagesChapter 1 The Demand For Audit and Other Assurance ServicesSarah GherdaouiNo ratings yet

- Advanced Marketing Management Course OutlineDocument4 pagesAdvanced Marketing Management Course OutlineJecka DuyagNo ratings yet

- Introduction To Retail Management - Unit 3 - Week 2 - Retail Formats & StrategiesDocument4 pagesIntroduction To Retail Management - Unit 3 - Week 2 - Retail Formats & StrategiesCHANDAN C KAMATHNo ratings yet

- Accy 360 Final Exam Study GuideDocument5 pagesAccy 360 Final Exam Study Guidebigbear1010No ratings yet

- Sample Topics For Research Paper About AccountingDocument7 pagesSample Topics For Research Paper About Accountingaflbmfjse100% (1)

- Strategic Direction Through Purchasing Portfolio Management - A Case StudyDocument13 pagesStrategic Direction Through Purchasing Portfolio Management - A Case StudyAhmad TabassumNo ratings yet

- CRISC Syllabus Outline 1Document4 pagesCRISC Syllabus Outline 1SyedNo ratings yet

- Ratio Analysis On Renuka Sugars Ltd.Document77 pagesRatio Analysis On Renuka Sugars Ltd.Punardatt Bhat100% (1)

- Brand Life Cycle (BLC)Document16 pagesBrand Life Cycle (BLC)shubhamy69% (13)

- Chapter 8 Alternative Costing SystemsDocument21 pagesChapter 8 Alternative Costing SystemsSaad KhanNo ratings yet

- BBA - Operations Management Practices 102Document100 pagesBBA - Operations Management Practices 10221620168No ratings yet

- Empresa ILEDocument6 pagesEmpresa ILEVerónica AlcívarNo ratings yet