IAS 1 Presentation of FS

IAS 1 Presentation of FS

You might also like

- Ias 01 Reference F12BDocument17 pagesIas 01 Reference F12BMaianh NguyễnNo ratings yet

- IAS 1 - Presentation of Financial StatementsDocument17 pagesIAS 1 - Presentation of Financial StatementsMạnh hưng LêNo ratings yet

- PAS1Document18 pagesPAS1Lyanna MormontNo ratings yet

- Indian & International Accounting Standards: Sarthak Agrawal Bba (1St Year) - Section - BDocument9 pagesIndian & International Accounting Standards: Sarthak Agrawal Bba (1St Year) - Section - Bbabu raoNo ratings yet

- IasDocument229 pagesIasPeter Apollo Latosa100% (1)

- IAS 1 - Presentation of Financial StatementsDocument7 pagesIAS 1 - Presentation of Financial StatementsNico Rivera CallangNo ratings yet

- History of IFRS 7: Reclassification of Financial Assets (Amendments To IAS 39 and IFRS 7) IssuedDocument5 pagesHistory of IFRS 7: Reclassification of Financial Assets (Amendments To IAS 39 and IFRS 7) IssuedTin BatacNo ratings yet

- IFRS 7 Financial Instruments: DisclosuresDocument2 pagesIFRS 7 Financial Instruments: DisclosuresAHMUDINNHOR DUMASILNo ratings yet

- IFRS 1 - First-Time Adoption of International Financial Reporting StandardsDocument49 pagesIFRS 1 - First-Time Adoption of International Financial Reporting StandardsTeofel John Alvizo PantaleonNo ratings yet

- IFRS 1-First-Time Adoption of International Financial Reporting StandardsDocument12 pagesIFRS 1-First-Time Adoption of International Financial Reporting StandardsShahid MahmudNo ratings yet

- Ias 1 - IfrsDocument13 pagesIas 1 - Ifrsglt0No ratings yet

- IAS 1 - Presentation of Financial StatementsDocument15 pagesIAS 1 - Presentation of Financial StatementsKamoheloNo ratings yet

- Ias 1 Presentation of Financial StatementsDocument13 pagesIas 1 Presentation of Financial StatementsShahbaz MalikNo ratings yet

- International Accounting Standards: # Name IssuedDocument44 pagesInternational Accounting Standards: # Name IssuedWasim Arif HashmiNo ratings yet

- IFRS 1 - First Time Adoption of IFRSDocument12 pagesIFRS 1 - First Time Adoption of IFRSEric Agyenim-BoatengNo ratings yet

- 84569159064Document3 pages84569159064fatimasani290No ratings yet

- International Accounting StandardsDocument24 pagesInternational Accounting StandardsWaqas WaraichNo ratings yet

- Ias 1Document11 pagesIas 1Vanessa Anavyl BuhisanNo ratings yet

- Timeline of IAS 19 - Employee BenefitsDocument4 pagesTimeline of IAS 19 - Employee BenefitsRey OñateNo ratings yet

- International Accounting StandardsDocument16 pagesInternational Accounting StandardsjanzzzzNo ratings yet

- Ias 1 Presentation of Financial StatementsDocument9 pagesIas 1 Presentation of Financial StatementsmelissayplNo ratings yet

- Bangladesh Accounting Standard (BAS)Document1 pageBangladesh Accounting Standard (BAS)Prabir Kumer Roy100% (3)

- First Time Adoption of International FinDocument34 pagesFirst Time Adoption of International FinFabrice uwubuhetaNo ratings yet

- IAS 19 - Employee Benefits (2011)Document6 pagesIAS 19 - Employee Benefits (2011)Katrina EustaceNo ratings yet

- IFRS Illustrative Financial Statements (Dec 2023)Document286 pagesIFRS Illustrative Financial Statements (Dec 2023)Vamsi Krishna GaragaNo ratings yet

- Ias1 - Example of Income Statement Presentation-1Document10 pagesIas1 - Example of Income Statement Presentation-1Denisa KollcinakuNo ratings yet

- Accounting Standards (Edited)Document5 pagesAccounting Standards (Edited)Jherico Gabriel B. OcomenNo ratings yet

- List of MFRS and FRSDocument10 pagesList of MFRS and FRSJulianne ChloeNo ratings yet

- EY-IFRS Adopted by EU 22122015Document8 pagesEY-IFRS Adopted by EU 22122015TiNo ratings yet

- Ias-Interim Financial ReportingDocument8 pagesIas-Interim Financial Reportingnguyenvy845No ratings yet

- Annotated BB2023 A IAS01 PartA PDFDocument62 pagesAnnotated BB2023 A IAS01 PartA PDFKhutso MabalaNo ratings yet

- AuditingDocument3 pagesAuditingMd. Abir HasanNo ratings yet

- A Project ON: (Impact On Banking Sector)Document21 pagesA Project ON: (Impact On Banking Sector)Akshay BhandeNo ratings yet

- Philippine Accounting Standards (PAS) : Number Title Effective DateDocument5 pagesPhilippine Accounting Standards (PAS) : Number Title Effective DateJherico Gabriel B. OcomenNo ratings yet

- Introduction of The Euro: SIC Interpretation 7Document4 pagesIntroduction of The Euro: SIC Interpretation 7Jerwin DaveNo ratings yet

- About: of Financial Statements Replaced IAS 1 Disclosure of Accounting Policies (Issued inDocument2 pagesAbout: of Financial Statements Replaced IAS 1 Disclosure of Accounting Policies (Issued inJolaica DiocolanoNo ratings yet

- Standard Title Effective Date Issuance Date Status: Amendment To Mfrs 2 (Annual Improvements To Mfrss 2010-2012 Cycle)Document9 pagesStandard Title Effective Date Issuance Date Status: Amendment To Mfrs 2 (Annual Improvements To Mfrss 2010-2012 Cycle)kaunseling dessoNo ratings yet

- Introduction of The Euro: SIC Interpretation 7Document4 pagesIntroduction of The Euro: SIC Interpretation 7Rolando G. Cua Jr.No ratings yet

- Ifrs 2021 - SicsDocument24 pagesIfrs 2021 - SicsAamir IkramNo ratings yet

- MFRS 121 042015 PDFDocument26 pagesMFRS 121 042015 PDFChessking Siew HeeNo ratings yet

- International Accounting Standards: 1977 S 1989 B IAS 27 IAS 28Document23 pagesInternational Accounting Standards: 1977 S 1989 B IAS 27 IAS 28TannaoNo ratings yet

- IFRS 12 Disclosure of Interests in Other EntitiesDocument5 pagesIFRS 12 Disclosure of Interests in Other EntitiesBernard DomasianNo ratings yet

- BV2021CR - MFRS1 First-Time Adoption of Malaysian Financial Reporting StandardsDocument43 pagesBV2021CR - MFRS1 First-Time Adoption of Malaysian Financial Reporting StandardsChee Juan PhangNo ratings yet

- List of Accounting StandardsDocument5 pagesList of Accounting StandardsSabaNo ratings yet

- BV2018 - MFRS 1Document41 pagesBV2018 - MFRS 1imieNo ratings yet

- IFRS1Document125 pagesIFRS1Sergiu CebanNo ratings yet

- MfrsDocument12 pagesMfrsiskandar027No ratings yet

- Ias 1 Presentation of Financial StatementsDocument42 pagesIas 1 Presentation of Financial StatementsEjaj-Ur-RahamanNo ratings yet

- Lkas1 Presentation of Financial StatementsDocument21 pagesLkas1 Presentation of Financial StatementssamaanNo ratings yet

- IAS Plus IAS 1, Presentati..Document10 pagesIAS Plus IAS 1, Presentati..Buddha BlessedNo ratings yet

- IFRS Illustrative Financial Statements (Dec 2021)Document292 pagesIFRS Illustrative Financial Statements (Dec 2021)bacha436No ratings yet

- IAS 1 SummaryDocument17 pagesIAS 1 SummaryperuparambilNo ratings yet

- History of The Project: Tions and Related Exposure DraftsDocument15 pagesHistory of The Project: Tions and Related Exposure DraftsalemayehuNo ratings yet

- Closing The GAAP: New IFRS Pronouncements Closing The GAAP: New Pronouncements Closing The GAAP: NewDocument6 pagesClosing The GAAP: New IFRS Pronouncements Closing The GAAP: New Pronouncements Closing The GAAP: NewMark Ronnier VedañaNo ratings yet

- Notes Q2FY2014Document10 pagesNotes Q2FY2014Shungchau WongNo ratings yet

- IFRS 8 - Operating Segments: Date Development CommentsDocument11 pagesIFRS 8 - Operating Segments: Date Development CommentsTeofel John Alvizo PantaleonNo ratings yet

- Toa First Time AdoptionDocument4 pagesToa First Time AdoptionreinaNo ratings yet

- Q2 2011 Disclosure Tip Sheet: Financial StatementsDocument1 pageQ2 2011 Disclosure Tip Sheet: Financial StatementsrayanNo ratings yet

- Industrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisFrom EverandIndustrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisNo ratings yet

- Creation Plmun As Local UniversityDocument11 pagesCreation Plmun As Local UniversityLeen LurNo ratings yet

- Dilg-Legalopinions Local EnterpriseDocument5 pagesDilg-Legalopinions Local EnterpriseLeen LurNo ratings yet

- IAS 8 - Accounting Policies, Changes in Accounting Estimates and ErrorsDocument7 pagesIAS 8 - Accounting Policies, Changes in Accounting Estimates and ErrorsLeen LurNo ratings yet

- IAS 7 Statement of Cash FlowDocument5 pagesIAS 7 Statement of Cash FlowLeen LurNo ratings yet

- El Patron The Goat Sheet Courses PC Android MacosDocument60 pagesEl Patron The Goat Sheet Courses PC Android MacosManav GodhaniNo ratings yet

- Presentation Arthur AndersenDocument23 pagesPresentation Arthur AndersenZohaibHassanNo ratings yet

- Final GEN Civil 2023Document5 pagesFinal GEN Civil 2023Youssef MohamedNo ratings yet

- Pi Emotional Quotient Digital AgeDocument88 pagesPi Emotional Quotient Digital AgeThai Hoa Pham100% (1)

- James Cantorne Corporation Liquidation and ReorganizationDocument8 pagesJames Cantorne Corporation Liquidation and ReorganizationJames CantorneNo ratings yet

- Exercise 1 Intro To Management ConsultancyDocument3 pagesExercise 1 Intro To Management ConsultancySiidolohNo ratings yet

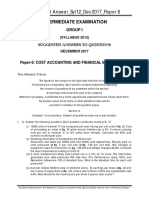

- Comparison of ABC and Traditional Costing ProblemDocument1 pageComparison of ABC and Traditional Costing ProblemallyssajabsNo ratings yet

- Financial Statements and AnalysisDocument40 pagesFinancial Statements and AnalysisZenedel De JesusNo ratings yet

- 4 Completing The Accounting Cycle PartDocument1 page4 Completing The Accounting Cycle PartTalionNo ratings yet

- SG Salary Guide 2021-22Document66 pagesSG Salary Guide 2021-22Gilbert ChiaNo ratings yet

- Nigeria Sas 10 and New Prudential Guidelines PDFDocument21 pagesNigeria Sas 10 and New Prudential Guidelines PDFiranadeNo ratings yet

- Two Major Types of Books in AccountingDocument13 pagesTwo Major Types of Books in AccountingJaneth Bootan ProtacioNo ratings yet

- Camille Realty Journal To FSDocument9 pagesCamille Realty Journal To FSVenus AriateNo ratings yet

- Journal of Cash TransactionsDocument2 pagesJournal of Cash TransactionsRobert Tayam, Jr.100% (1)

- Note 2Document7 pagesNote 2faizoolNo ratings yet

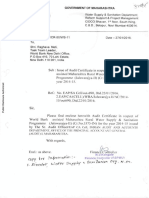

- Issue of Audit Certificate in Respect of World Bank &Document11 pagesIssue of Audit Certificate in Respect of World Bank &sharadNo ratings yet

- Seatwork 01 Conceptual FrameworkDocument7 pagesSeatwork 01 Conceptual FrameworkNah HamzaNo ratings yet

- Performance MeasurementDocument542 pagesPerformance Measurementdhimasaditya92100% (1)

- Noakhali Gold Foods Limited: Project CostDocument19 pagesNoakhali Gold Foods Limited: Project Costaktaruzzaman bethuNo ratings yet

- Transactions: Origin Of: Source Documents of AccountancyDocument4 pagesTransactions: Origin Of: Source Documents of AccountancyMradul AgrawalNo ratings yet

- Sub Ledger Setup For PayrollDocument9 pagesSub Ledger Setup For PayrollMaqbulhusenNo ratings yet

- CV ARV Final 30072021Document3 pagesCV ARV Final 30072021Kiran KumarNo ratings yet

- 4 Chart of AccountsDocument115 pages4 Chart of Accountsresti rahmawatiNo ratings yet

- Management Accounting Concepts and Techniques PDFDocument310 pagesManagement Accounting Concepts and Techniques PDFvishnupriya100% (1)

- 2019 AFR National Govt Volume I PDFDocument463 pages2019 AFR National Govt Volume I PDFLlanesca PantiNo ratings yet

- Year End and Month End Activities Carried in FIDocument8 pagesYear End and Month End Activities Carried in FIManas Kumar SahooNo ratings yet

- Lab Iii Audit of Sales and Collection Cycle: I. TujuanDocument8 pagesLab Iii Audit of Sales and Collection Cycle: I. TujuanyenitaNo ratings yet

- Acccob3 HW7Document12 pagesAcccob3 HW7Jenine Yamson100% (1)

- EOQ Problems Class NotesDocument18 pagesEOQ Problems Class NotesVikram KumarNo ratings yet

- Nimesh Gupta SIP ProposalDocument3 pagesNimesh Gupta SIP ProposalNimesh guptaNo ratings yet

Download as docx, pdf, or txt

You might also like

- Ias 01 Reference F12BDocument17 pagesIas 01 Reference F12BMaianh NguyễnNo ratings yet

- IAS 1 - Presentation of Financial StatementsDocument17 pagesIAS 1 - Presentation of Financial StatementsMạnh hưng LêNo ratings yet

- PAS1Document18 pagesPAS1Lyanna MormontNo ratings yet

- Indian & International Accounting Standards: Sarthak Agrawal Bba (1St Year) - Section - BDocument9 pagesIndian & International Accounting Standards: Sarthak Agrawal Bba (1St Year) - Section - Bbabu raoNo ratings yet

- IasDocument229 pagesIasPeter Apollo Latosa100% (1)

- IAS 1 - Presentation of Financial StatementsDocument7 pagesIAS 1 - Presentation of Financial StatementsNico Rivera CallangNo ratings yet

- History of IFRS 7: Reclassification of Financial Assets (Amendments To IAS 39 and IFRS 7) IssuedDocument5 pagesHistory of IFRS 7: Reclassification of Financial Assets (Amendments To IAS 39 and IFRS 7) IssuedTin BatacNo ratings yet

- IFRS 7 Financial Instruments: DisclosuresDocument2 pagesIFRS 7 Financial Instruments: DisclosuresAHMUDINNHOR DUMASILNo ratings yet

- IFRS 1 - First-Time Adoption of International Financial Reporting StandardsDocument49 pagesIFRS 1 - First-Time Adoption of International Financial Reporting StandardsTeofel John Alvizo PantaleonNo ratings yet

- IFRS 1-First-Time Adoption of International Financial Reporting StandardsDocument12 pagesIFRS 1-First-Time Adoption of International Financial Reporting StandardsShahid MahmudNo ratings yet

- Ias 1 - IfrsDocument13 pagesIas 1 - Ifrsglt0No ratings yet

- IAS 1 - Presentation of Financial StatementsDocument15 pagesIAS 1 - Presentation of Financial StatementsKamoheloNo ratings yet

- Ias 1 Presentation of Financial StatementsDocument13 pagesIas 1 Presentation of Financial StatementsShahbaz MalikNo ratings yet

- International Accounting Standards: # Name IssuedDocument44 pagesInternational Accounting Standards: # Name IssuedWasim Arif HashmiNo ratings yet

- IFRS 1 - First Time Adoption of IFRSDocument12 pagesIFRS 1 - First Time Adoption of IFRSEric Agyenim-BoatengNo ratings yet

- 84569159064Document3 pages84569159064fatimasani290No ratings yet

- International Accounting StandardsDocument24 pagesInternational Accounting StandardsWaqas WaraichNo ratings yet

- Ias 1Document11 pagesIas 1Vanessa Anavyl BuhisanNo ratings yet

- Timeline of IAS 19 - Employee BenefitsDocument4 pagesTimeline of IAS 19 - Employee BenefitsRey OñateNo ratings yet

- International Accounting StandardsDocument16 pagesInternational Accounting StandardsjanzzzzNo ratings yet

- Ias 1 Presentation of Financial StatementsDocument9 pagesIas 1 Presentation of Financial StatementsmelissayplNo ratings yet

- Bangladesh Accounting Standard (BAS)Document1 pageBangladesh Accounting Standard (BAS)Prabir Kumer Roy100% (3)

- First Time Adoption of International FinDocument34 pagesFirst Time Adoption of International FinFabrice uwubuhetaNo ratings yet

- IAS 19 - Employee Benefits (2011)Document6 pagesIAS 19 - Employee Benefits (2011)Katrina EustaceNo ratings yet

- IFRS Illustrative Financial Statements (Dec 2023)Document286 pagesIFRS Illustrative Financial Statements (Dec 2023)Vamsi Krishna GaragaNo ratings yet

- Ias1 - Example of Income Statement Presentation-1Document10 pagesIas1 - Example of Income Statement Presentation-1Denisa KollcinakuNo ratings yet

- Accounting Standards (Edited)Document5 pagesAccounting Standards (Edited)Jherico Gabriel B. OcomenNo ratings yet

- List of MFRS and FRSDocument10 pagesList of MFRS and FRSJulianne ChloeNo ratings yet

- EY-IFRS Adopted by EU 22122015Document8 pagesEY-IFRS Adopted by EU 22122015TiNo ratings yet

- Ias-Interim Financial ReportingDocument8 pagesIas-Interim Financial Reportingnguyenvy845No ratings yet

- Annotated BB2023 A IAS01 PartA PDFDocument62 pagesAnnotated BB2023 A IAS01 PartA PDFKhutso MabalaNo ratings yet

- AuditingDocument3 pagesAuditingMd. Abir HasanNo ratings yet

- A Project ON: (Impact On Banking Sector)Document21 pagesA Project ON: (Impact On Banking Sector)Akshay BhandeNo ratings yet

- Philippine Accounting Standards (PAS) : Number Title Effective DateDocument5 pagesPhilippine Accounting Standards (PAS) : Number Title Effective DateJherico Gabriel B. OcomenNo ratings yet

- Introduction of The Euro: SIC Interpretation 7Document4 pagesIntroduction of The Euro: SIC Interpretation 7Jerwin DaveNo ratings yet

- About: of Financial Statements Replaced IAS 1 Disclosure of Accounting Policies (Issued inDocument2 pagesAbout: of Financial Statements Replaced IAS 1 Disclosure of Accounting Policies (Issued inJolaica DiocolanoNo ratings yet

- Standard Title Effective Date Issuance Date Status: Amendment To Mfrs 2 (Annual Improvements To Mfrss 2010-2012 Cycle)Document9 pagesStandard Title Effective Date Issuance Date Status: Amendment To Mfrs 2 (Annual Improvements To Mfrss 2010-2012 Cycle)kaunseling dessoNo ratings yet

- Introduction of The Euro: SIC Interpretation 7Document4 pagesIntroduction of The Euro: SIC Interpretation 7Rolando G. Cua Jr.No ratings yet

- Ifrs 2021 - SicsDocument24 pagesIfrs 2021 - SicsAamir IkramNo ratings yet

- MFRS 121 042015 PDFDocument26 pagesMFRS 121 042015 PDFChessking Siew HeeNo ratings yet

- International Accounting Standards: 1977 S 1989 B IAS 27 IAS 28Document23 pagesInternational Accounting Standards: 1977 S 1989 B IAS 27 IAS 28TannaoNo ratings yet

- IFRS 12 Disclosure of Interests in Other EntitiesDocument5 pagesIFRS 12 Disclosure of Interests in Other EntitiesBernard DomasianNo ratings yet

- BV2021CR - MFRS1 First-Time Adoption of Malaysian Financial Reporting StandardsDocument43 pagesBV2021CR - MFRS1 First-Time Adoption of Malaysian Financial Reporting StandardsChee Juan PhangNo ratings yet

- List of Accounting StandardsDocument5 pagesList of Accounting StandardsSabaNo ratings yet

- BV2018 - MFRS 1Document41 pagesBV2018 - MFRS 1imieNo ratings yet

- IFRS1Document125 pagesIFRS1Sergiu CebanNo ratings yet

- MfrsDocument12 pagesMfrsiskandar027No ratings yet

- Ias 1 Presentation of Financial StatementsDocument42 pagesIas 1 Presentation of Financial StatementsEjaj-Ur-RahamanNo ratings yet

- Lkas1 Presentation of Financial StatementsDocument21 pagesLkas1 Presentation of Financial StatementssamaanNo ratings yet

- IAS Plus IAS 1, Presentati..Document10 pagesIAS Plus IAS 1, Presentati..Buddha BlessedNo ratings yet

- IFRS Illustrative Financial Statements (Dec 2021)Document292 pagesIFRS Illustrative Financial Statements (Dec 2021)bacha436No ratings yet

- IAS 1 SummaryDocument17 pagesIAS 1 SummaryperuparambilNo ratings yet

- History of The Project: Tions and Related Exposure DraftsDocument15 pagesHistory of The Project: Tions and Related Exposure DraftsalemayehuNo ratings yet

- Closing The GAAP: New IFRS Pronouncements Closing The GAAP: New Pronouncements Closing The GAAP: NewDocument6 pagesClosing The GAAP: New IFRS Pronouncements Closing The GAAP: New Pronouncements Closing The GAAP: NewMark Ronnier VedañaNo ratings yet

- Notes Q2FY2014Document10 pagesNotes Q2FY2014Shungchau WongNo ratings yet

- IFRS 8 - Operating Segments: Date Development CommentsDocument11 pagesIFRS 8 - Operating Segments: Date Development CommentsTeofel John Alvizo PantaleonNo ratings yet

- Toa First Time AdoptionDocument4 pagesToa First Time AdoptionreinaNo ratings yet

- Q2 2011 Disclosure Tip Sheet: Financial StatementsDocument1 pageQ2 2011 Disclosure Tip Sheet: Financial StatementsrayanNo ratings yet

- Industrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisFrom EverandIndustrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisNo ratings yet

- Creation Plmun As Local UniversityDocument11 pagesCreation Plmun As Local UniversityLeen LurNo ratings yet

- Dilg-Legalopinions Local EnterpriseDocument5 pagesDilg-Legalopinions Local EnterpriseLeen LurNo ratings yet

- IAS 8 - Accounting Policies, Changes in Accounting Estimates and ErrorsDocument7 pagesIAS 8 - Accounting Policies, Changes in Accounting Estimates and ErrorsLeen LurNo ratings yet

- IAS 7 Statement of Cash FlowDocument5 pagesIAS 7 Statement of Cash FlowLeen LurNo ratings yet

- El Patron The Goat Sheet Courses PC Android MacosDocument60 pagesEl Patron The Goat Sheet Courses PC Android MacosManav GodhaniNo ratings yet

- Presentation Arthur AndersenDocument23 pagesPresentation Arthur AndersenZohaibHassanNo ratings yet

- Final GEN Civil 2023Document5 pagesFinal GEN Civil 2023Youssef MohamedNo ratings yet

- Pi Emotional Quotient Digital AgeDocument88 pagesPi Emotional Quotient Digital AgeThai Hoa Pham100% (1)

- James Cantorne Corporation Liquidation and ReorganizationDocument8 pagesJames Cantorne Corporation Liquidation and ReorganizationJames CantorneNo ratings yet

- Exercise 1 Intro To Management ConsultancyDocument3 pagesExercise 1 Intro To Management ConsultancySiidolohNo ratings yet

- Comparison of ABC and Traditional Costing ProblemDocument1 pageComparison of ABC and Traditional Costing ProblemallyssajabsNo ratings yet

- Financial Statements and AnalysisDocument40 pagesFinancial Statements and AnalysisZenedel De JesusNo ratings yet

- 4 Completing The Accounting Cycle PartDocument1 page4 Completing The Accounting Cycle PartTalionNo ratings yet

- SG Salary Guide 2021-22Document66 pagesSG Salary Guide 2021-22Gilbert ChiaNo ratings yet

- Nigeria Sas 10 and New Prudential Guidelines PDFDocument21 pagesNigeria Sas 10 and New Prudential Guidelines PDFiranadeNo ratings yet

- Two Major Types of Books in AccountingDocument13 pagesTwo Major Types of Books in AccountingJaneth Bootan ProtacioNo ratings yet

- Camille Realty Journal To FSDocument9 pagesCamille Realty Journal To FSVenus AriateNo ratings yet

- Journal of Cash TransactionsDocument2 pagesJournal of Cash TransactionsRobert Tayam, Jr.100% (1)

- Note 2Document7 pagesNote 2faizoolNo ratings yet

- Issue of Audit Certificate in Respect of World Bank &Document11 pagesIssue of Audit Certificate in Respect of World Bank &sharadNo ratings yet

- Seatwork 01 Conceptual FrameworkDocument7 pagesSeatwork 01 Conceptual FrameworkNah HamzaNo ratings yet

- Performance MeasurementDocument542 pagesPerformance Measurementdhimasaditya92100% (1)

- Noakhali Gold Foods Limited: Project CostDocument19 pagesNoakhali Gold Foods Limited: Project Costaktaruzzaman bethuNo ratings yet

- Transactions: Origin Of: Source Documents of AccountancyDocument4 pagesTransactions: Origin Of: Source Documents of AccountancyMradul AgrawalNo ratings yet

- Sub Ledger Setup For PayrollDocument9 pagesSub Ledger Setup For PayrollMaqbulhusenNo ratings yet

- CV ARV Final 30072021Document3 pagesCV ARV Final 30072021Kiran KumarNo ratings yet

- 4 Chart of AccountsDocument115 pages4 Chart of Accountsresti rahmawatiNo ratings yet

- Management Accounting Concepts and Techniques PDFDocument310 pagesManagement Accounting Concepts and Techniques PDFvishnupriya100% (1)

- 2019 AFR National Govt Volume I PDFDocument463 pages2019 AFR National Govt Volume I PDFLlanesca PantiNo ratings yet

- Year End and Month End Activities Carried in FIDocument8 pagesYear End and Month End Activities Carried in FIManas Kumar SahooNo ratings yet

- Lab Iii Audit of Sales and Collection Cycle: I. TujuanDocument8 pagesLab Iii Audit of Sales and Collection Cycle: I. TujuanyenitaNo ratings yet

- Acccob3 HW7Document12 pagesAcccob3 HW7Jenine Yamson100% (1)

- EOQ Problems Class NotesDocument18 pagesEOQ Problems Class NotesVikram KumarNo ratings yet

- Nimesh Gupta SIP ProposalDocument3 pagesNimesh Gupta SIP ProposalNimesh guptaNo ratings yet