Download as pdf or txt

You might also like

- Financial Accounting IFRS Student Mark Plan June 2019Document16 pagesFinancial Accounting IFRS Student Mark Plan June 2019scottNo ratings yet

- Caf-03 Cma Sir Nasir Sp-23Document48 pagesCaf-03 Cma Sir Nasir Sp-23Riot Skin0% (1)

- Answer Question 3Document27 pagesAnswer Question 3ummi sabrina100% (1)

- 4 5807634410916285735Document5 pages4 5807634410916285735magwazagroup33No ratings yet

- Statement of Profit or Loss and Other Comprehensive IncomeDocument4 pagesStatement of Profit or Loss and Other Comprehensive IncomeOnela BriannaNo ratings yet

- SS - TEST FAR270 - NOV 2022 Set 2 StudentDocument5 pagesSS - TEST FAR270 - NOV 2022 Set 2 Studentsharifah nurshahira sakinaNo ratings yet

- 4 HW On Gov't Grant, Depreciation, Revaluation and Impairment T3 Answer KeyDocument9 pages4 HW On Gov't Grant, Depreciation, Revaluation and Impairment T3 Answer KeyJessica Mikah Lim AgbayaniNo ratings yet

- QuizDocument4 pagesQuizRinconada Benori ReynalynNo ratings yet

- Depreciation Allowance (Parts 1 & 2) Tutorial Questions 1Document4 pagesDepreciation Allowance (Parts 1 & 2) Tutorial Questions 1ting ting shihNo ratings yet

- Reviewer in Auditing Problems by Ocampo/Ocampo (2021 Edition)Document7 pagesReviewer in Auditing Problems by Ocampo/Ocampo (2021 Edition)Rosevilla AbneNo ratings yet

- Trick TradersDocument2 pagesTrick Tradersrethaxaba82No ratings yet

- Business Taxation: (Malawi)Document10 pagesBusiness Taxation: (Malawi)angaNo ratings yet

- Solution Financial Accounting FundamentalsDocument7 pagesSolution Financial Accounting Fundamentalsone thymeNo ratings yet

- Summary CH 11 - Pert 9 10 - Kelas ADocument26 pagesSummary CH 11 - Pert 9 10 - Kelas AIzaktria KoehuanNo ratings yet

- Cost Accrual Production Report May 2023 - NORTHDocument13 pagesCost Accrual Production Report May 2023 - NORTHIan Jasper NamocNo ratings yet

- FF - Karil Koiriyah - 180421621551 - Tugas 4Document92 pagesFF - Karil Koiriyah - 180421621551 - Tugas 4karinaNo ratings yet

- J. Jarvis Trial Balance As at 31 December 2010Document3 pagesJ. Jarvis Trial Balance As at 31 December 2010Ahmad HaqqyNo ratings yet

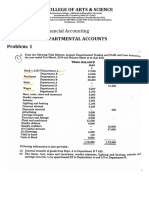

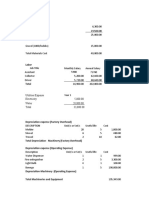

- Departmental Account Problems & AnswerDocument7 pagesDepartmental Account Problems & Answeranand dpiNo ratings yet

- Answer Far270 Feb2021Document8 pagesAnswer Far270 Feb2021Nur Fatin AmirahNo ratings yet

- (A) Alpha Bit Design Worksheet For The Month Ended October 31, 2020Document5 pages(A) Alpha Bit Design Worksheet For The Month Ended October 31, 2020Sergio NicolasNo ratings yet

- Financial Statements of FSDocument76 pagesFinancial Statements of FScarl fuerzasNo ratings yet

- Lembar JawabanDocument46 pagesLembar JawabanIndah SitanggangNo ratings yet

- Step Ahead 2023 Accounting Grade 12 Teacher GuideDocument60 pagesStep Ahead 2023 Accounting Grade 12 Teacher Guidethabileshab08No ratings yet

- 3 - IAS 36 SolutionDocument3 pages3 - IAS 36 Solutionsandeshjhanbia021No ratings yet

- S20 TX MWI Sample AnswersDocument8 pagesS20 TX MWI Sample AnswersangaNo ratings yet

- Gov't Grant, Depreciation, Revaluation and ImpairmentDocument6 pagesGov't Grant, Depreciation, Revaluation and Impairment夜晨曦No ratings yet

- Number 4Document5 pagesNumber 4Marie Fe GullesNo ratings yet

- Revaluation Problems Part 2Document32 pagesRevaluation Problems Part 2XNo ratings yet

- TT08 Feedback - 100Document3 pagesTT08 Feedback - 100Uyển Nhi TrầnNo ratings yet

- Solutions Tax InvestigationDocument15 pagesSolutions Tax InvestigationWahida AmalinNo ratings yet

- CPA 1 - Financial Acconting Sep 2022Document10 pagesCPA 1 - Financial Acconting Sep 2022Asaba GloriaNo ratings yet

- Financial Reporting IAS-16 Assignment F2021314036Document24 pagesFinancial Reporting IAS-16 Assignment F2021314036Abdullah MaqsoodNo ratings yet

- Description Income Expenses Assets LiabilitiesDocument12 pagesDescription Income Expenses Assets LiabilitiesNipuna Perera100% (1)

- Excel - Professional Services Inc.: Management Firm of Professional Review and Training Center (PRTC)Document5 pagesExcel - Professional Services Inc.: Management Firm of Professional Review and Training Center (PRTC)May Grethel Joy Perante100% (1)

- Lembar Jawaban Mahesa - SalinDocument10 pagesLembar Jawaban Mahesa - Salinricoananta10No ratings yet

- Flare GasificationDocument25 pagesFlare Gasificationtimir ghoseNo ratings yet

- Corporation Tax - Suggested AnswerDocument5 pagesCorporation Tax - Suggested AnswerQasimNo ratings yet

- Financial Accounting MAY / 2019 BBAW2103Document8 pagesFinancial Accounting MAY / 2019 BBAW2103Yung YeeNo ratings yet

- Ias16 Q3Document2 pagesIas16 Q3ziamz219No ratings yet

- Profit & Loss Accounts: Wing Chair GirogioDocument3 pagesProfit & Loss Accounts: Wing Chair Girogiofarsi786No ratings yet

- CPAR - AP Solutions 1st PB-BATCH 91Document5 pagesCPAR - AP Solutions 1st PB-BATCH 91Allyson VillalobosNo ratings yet

- AUDITDocument12 pagesAUDITdavid giriNo ratings yet

- Income Tax June 2023-Dec 2020Document116 pagesIncome Tax June 2023-Dec 2020binuNo ratings yet

- 93 - Final Preaboard AFAR SolutionsDocument11 pages93 - Final Preaboard AFAR SolutionsLeiNo ratings yet

- Appendix C End-Of-Period Spreadsheet (Work Sheet) For A Merchandising BusinessDocument14 pagesAppendix C End-Of-Period Spreadsheet (Work Sheet) For A Merchandising BusinessLan Hương Trần ThịNo ratings yet

- 4th Assessment STUDENTDocument5 pages4th Assessment STUDENTJOHANNA TORRESNo ratings yet

- FAC2601 Assignment 02Document4 pagesFAC2601 Assignment 02SibongileNo ratings yet

- Sabit FSDocument8 pagesSabit FSMilagrosa VillasNo ratings yet

- Accounts Revision QuestionDocument1 pageAccounts Revision QuestionZaara AshfaqNo ratings yet

- 1-1hkg 2002 Dec ADocument8 pages1-1hkg 2002 Dec AWing Yan KatieNo ratings yet

- Jawaban Soal UTS Akuntansi Keu - MenengahDocument4 pagesJawaban Soal UTS Akuntansi Keu - MenengahJessinthaNo ratings yet

- Assignment 1Document6 pagesAssignment 1Nichole TumulakNo ratings yet

- PRACTICE CLASS 3, 4 and 5Document6 pagesPRACTICE CLASS 3, 4 and 5Zain JamilNo ratings yet

- AUD of PPE Problem 2Document11 pagesAUD of PPE Problem 2Jay LloydNo ratings yet

- Lecture 2 - Practice QuestionsDocument2 pagesLecture 2 - Practice Questionsdonkhalif13No ratings yet

- Auditing Problem SolutionsDocument13 pagesAuditing Problem SolutionsjhobsNo ratings yet

- Audit and Corporate Governance Class 4. Non Current AssetDocument16 pagesAudit and Corporate Governance Class 4. Non Current AssetlucinossNo ratings yet

- P1. PRO (O.L) Solution CMA June-2021 Exam.Document5 pagesP1. PRO (O.L) Solution CMA June-2021 Exam.Tameemmahmud rokibNo ratings yet

- Problem 1Document5 pagesProblem 1jhie boterNo ratings yet

- Using Economic Indicators to Improve Investment AnalysisFrom EverandUsing Economic Indicators to Improve Investment AnalysisRating: 3.5 out of 5 stars3.5/5 (1)

- Schematic/Electrical Parts: 36021V5J, V7J 36026V5J, V7J 42026 & 42030V6J With "H" ControlsDocument55 pagesSchematic/Electrical Parts: 36021V5J, V7J 36026V5J, V7J 42026 & 42030V6J With "H" ControlsJose Moreno TorbiscoNo ratings yet

- The Condensed Satanic BibleDocument123 pagesThe Condensed Satanic Biblestregonebr100% (1)

- The Talent Company's HR Job Postings in The GTA Report - April 5, 2021Document180 pagesThe Talent Company's HR Job Postings in The GTA Report - April 5, 2021heymuraliNo ratings yet

- Orthodontic Treatment in The Management of Cleft Lip and PalateDocument13 pagesOrthodontic Treatment in The Management of Cleft Lip and PalatecareNo ratings yet

- Hand Hygiene and HandwashingDocument7 pagesHand Hygiene and HandwashingFaith Dianasas RequinaNo ratings yet

- 01 The QuizDocument7 pages01 The QuizJabriellaSanMiguel100% (1)

- 2040 - Cut-Off-Points - 2020 - 2021 of The Special Provision For Students Who Have Excelled in Extra Curricular Activities - New SyllabusDocument5 pages2040 - Cut-Off-Points - 2020 - 2021 of The Special Provision For Students Who Have Excelled in Extra Curricular Activities - New SyllabusGayanuka MendisNo ratings yet

- Increasing Awareness of Future Teachers About Health, Health Preservation and Health Saving Technologies of Preschool ChildrenDocument4 pagesIncreasing Awareness of Future Teachers About Health, Health Preservation and Health Saving Technologies of Preschool ChildrenResearch ParkNo ratings yet

- 073-116-020 (Accounting Practice in Bangladesh)Document26 pages073-116-020 (Accounting Practice in Bangladesh)Bazlur Rahman Khan67% (9)

- Water-Treatment (Rhen)Document13 pagesWater-Treatment (Rhen)Mark Anthony ReyesNo ratings yet

- English Essay Bros Before HosDocument5 pagesEnglish Essay Bros Before HosAndrés I. Rivera33% (3)

- Sheet 3 With SolutionsDocument6 pagesSheet 3 With SolutionsHager ElzayatNo ratings yet

- Notes On Ropes & Wires SOT I 2012 Unit 4Document21 pagesNotes On Ropes & Wires SOT I 2012 Unit 4James MonishNo ratings yet

- Series: LTJ: Toe Capacity: 2.5 - 25 Ton - Head Capacity: 5 - 50 Ton - Stroke Length For Toe: 50 MMDocument1 pageSeries: LTJ: Toe Capacity: 2.5 - 25 Ton - Head Capacity: 5 - 50 Ton - Stroke Length For Toe: 50 MM220479No ratings yet

- Zoho Interview QustionsDocument4 pagesZoho Interview QustionsRadheshyam Nayak0% (1)

- Critical Areas of Structural Concerns On Bulk Carriers / Dry Cargo ShipsDocument5 pagesCritical Areas of Structural Concerns On Bulk Carriers / Dry Cargo ShipsHUNG LE THANHNo ratings yet

- Optigenex v. Jeunesse Global Holdings Et. Al.Document57 pagesOptigenex v. Jeunesse Global Holdings Et. Al.PriorSmartNo ratings yet

- Hydraulics Stability (Anyer Geotube Project)Document4 pagesHydraulics Stability (Anyer Geotube Project)Anonymous IWHeUvNo ratings yet

- Communication and Presentation Skill 1Document229 pagesCommunication and Presentation Skill 1shanthakumargcNo ratings yet

- Jane Eyre Bertha Mason Teachers Notes UpdatedDocument4 pagesJane Eyre Bertha Mason Teachers Notes Updated04. Phan Thi Huyen Trang K17 HLNo ratings yet

- Chap 8 FrictionDocument32 pagesChap 8 FrictionAyan Kabir ChowdhuryNo ratings yet

- Slide Plate ApplicationsDocument2 pagesSlide Plate ApplicationsvietrossNo ratings yet

- Strain Index Scoring Sheet: Date: Task: Company: Supervisor: Dept: EvaluatorDocument1 pageStrain Index Scoring Sheet: Date: Task: Company: Supervisor: Dept: EvaluatorAngeline Henao BohorquezNo ratings yet

- CompTIA Security+ (SY0-701)Document405 pagesCompTIA Security+ (SY0-701)Calisto Junior100% (1)

- 7 Natural Law Readings and Activity PDFDocument5 pages7 Natural Law Readings and Activity PDFLorelene RomeroNo ratings yet

- Ignou Assignment Wala Ehi 1 Solved Assignment 2018-19Document7 pagesIgnou Assignment Wala Ehi 1 Solved Assignment 2018-19NEW THINK CLASSES100% (1)

- Ansi Scte74 2003 Ipssp001Document17 pagesAnsi Scte74 2003 Ipssp001Boris AguilarNo ratings yet

- Ec 604 HW 3 PDFDocument3 pagesEc 604 HW 3 PDFgattino gattinoNo ratings yet

- Dynamics of Machines - Part III - IFS PDFDocument96 pagesDynamics of Machines - Part III - IFS PDFAnonymous OFwyjaMyNo ratings yet

- Teacher CardDocument4 pagesTeacher CardMUTHYALA NEERAJANo ratings yet