Download as pdf or txt

You might also like

- Managing Filipino Teams by Mike GroganDocument107 pagesManaging Filipino Teams by Mike GroganglycerilkayeNo ratings yet

- IT Savings Proofs Submission - FY 2021-22: AuthorDocument9 pagesIT Savings Proofs Submission - FY 2021-22: Authormunash2kumarNo ratings yet

- WT IT - Declarations - Guidelines - FY - 2019-20 PDFDocument11 pagesWT IT - Declarations - Guidelines - FY - 2019-20 PDFGautham ReddyNo ratings yet

- Guide ITProof SubmissionDocument9 pagesGuide ITProof SubmissionSajid Raza RizviNo ratings yet

- Guidelines Tax Related DeclarationsDocument16 pagesGuidelines Tax Related DeclarationsRaghul MuthuNo ratings yet

- Guidelines TaxRelatedDeclarations2023 24Document22 pagesGuidelines TaxRelatedDeclarations2023 24karthik sNo ratings yet

- POI Submission GuidelinesDocument4 pagesPOI Submission Guidelinesswapna vijayNo ratings yet

- Annexure - Iv Information Sheet Name: Candidate ID:: 1. Role and Competency Based OrganizationDocument3 pagesAnnexure - Iv Information Sheet Name: Candidate ID:: 1. Role and Competency Based OrganizationdfsdfNo ratings yet

- Exit Process and FAQ'sDocument8 pagesExit Process and FAQ'snaimishamaniNo ratings yet

- R TSSDocument28 pagesR TSSAndri RodriguezNo ratings yet

- Key Points For Investment Proof Submission 2016-2017 Deadline and Mode of SubmissionDocument13 pagesKey Points For Investment Proof Submission 2016-2017 Deadline and Mode of SubmissionAjay TiwariNo ratings yet

- Information SheetDocument5 pagesInformation SheetShrishNo ratings yet

- Equity Program FAQDocument14 pagesEquity Program FAQNikhil SinghalNo ratings yet

- E-Filling of ReturnDocument6 pagesE-Filling of ReturnNeelanjan MitraNo ratings yet

- Input Tax CreditDocument8 pagesInput Tax CreditPranjal AgrawalNo ratings yet

- Bir60 EguideDocument15 pagesBir60 Eguidekumar.arasu8717No ratings yet

- Income Tax ComplianceDocument4 pagesIncome Tax ComplianceJusefNo ratings yet

- Itr 1 Ay 2023-24Document3 pagesItr 1 Ay 2023-24Arup MridhaNo ratings yet

- Tax Declaration Guide 2022-23Document15 pagesTax Declaration Guide 2022-23shasvinaNo ratings yet

- HRA, Chapter VI A - 80CCD, 80C, 80D, Other IncomeDocument9 pagesHRA, Chapter VI A - 80CCD, 80C, 80D, Other Incomefaiyaz432No ratings yet

- Single Desk - G.O. MS. 85Document151 pagesSingle Desk - G.O. MS. 85Sandilya CharanNo ratings yet

- Notes To Investment Proof SubmissionDocument10 pagesNotes To Investment Proof SubmissionVinayak DhotreNo ratings yet

- Direct Tax and Compliance Farheen 202200535 WordsDocument11 pagesDirect Tax and Compliance Farheen 202200535 Wordsnaazfarheen7777No ratings yet

- VAT - MCQ Test Questions by Mahbub SirDocument16 pagesVAT - MCQ Test Questions by Mahbub SirAysha Alam100% (1)

- H4 - GST at GVC: Spark For The Day "Document6 pagesH4 - GST at GVC: Spark For The Day "Kenny PhilipsNo ratings yet

- Annexure II Details of AllowancesDocument4 pagesAnnexure II Details of AllowancesPravin Balasaheb GunjalNo ratings yet

- Financial Year 2015-2016Document28 pagesFinancial Year 2015-2016Vinothini MuruganNo ratings yet

- IT-AE-41-G02 - Guide To Complete The Tax Directive Application Forms - External GuideDocument50 pagesIT-AE-41-G02 - Guide To Complete The Tax Directive Application Forms - External GuidercpretoriusNo ratings yet

- IT PolicyDocument2 pagesIT PolicyvarunNo ratings yet

- Instruction For Submitting ProofsDocument3 pagesInstruction For Submitting Proofssastrylanka_1980No ratings yet

- Tax. 23Document18 pagesTax. 23RahulNo ratings yet

- Investment Declaration Form (Hemarus)Document4 pagesInvestment Declaration Form (Hemarus)Shashi NaganurNo ratings yet

- Tax Planning AssignmentDocument10 pagesTax Planning AssignmentJayashree Mohandass100% (1)

- OfferLetter MetlifeDocument4 pagesOfferLetter Metlifeshekhawath13No ratings yet

- Gmail - Tata Steel Limited - Communication On Tax Deduction at Source On Dividend PayoutDocument7 pagesGmail - Tata Steel Limited - Communication On Tax Deduction at Source On Dividend PayoutDheeraj UppiNo ratings yet

- Tax Proof Submission Document 2022-23Document7 pagesTax Proof Submission Document 2022-23Jagadeesh DatlaNo ratings yet

- Bir60 EguideDocument12 pagesBir60 EguideRay Li Shing KitNo ratings yet

- Transfer of Input Tax Credit and Its Related Issues: Who Can Claim ITC?Document11 pagesTransfer of Input Tax Credit and Its Related Issues: Who Can Claim ITC?Vishal DubeyNo ratings yet

- A Guide To Your Personal Income TaxDocument7 pagesA Guide To Your Personal Income TaxRekha SinghNo ratings yet

- Computerised Accounting and e Filing of Tax ReturnsDocument8 pagesComputerised Accounting and e Filing of Tax ReturnsBishal BhandariNo ratings yet

- User Manual For Online Submission of Investment ProofsDocument10 pagesUser Manual For Online Submission of Investment ProofsAbc123No ratings yet

- Frequently Asked Questions: 1. How Is The Withholding Tax On Commission Calculated?Document9 pagesFrequently Asked Questions: 1. How Is The Withholding Tax On Commission Calculated?vanguardNo ratings yet

- GST-603 Unit-3Document23 pagesGST-603 Unit-3GauharNo ratings yet

- FAQ Reimbursement and Investment ProofsDocument8 pagesFAQ Reimbursement and Investment ProofsPrashant TiwariNo ratings yet

- Employee Self Service (ESS)Document13 pagesEmployee Self Service (ESS)Charanpreet SinghNo ratings yet

- Bir60 EguideDocument12 pagesBir60 EguidekunalkhubaniNo ratings yet

- "H & R Block India Pvt. LTD.": A Project Report OnDocument98 pages"H & R Block India Pvt. LTD.": A Project Report OnraviNo ratings yet

- Procedure For Prod - CertificateDocument166 pagesProcedure For Prod - CertificatePonduru TirmualaNo ratings yet

- Quiz 2Document24 pagesQuiz 2Lee TeukNo ratings yet

- Warehousing Development and Regulatory Authority: No. WDRA/2017/5-7/A&F Dated: 07.09.2017Document8 pagesWarehousing Development and Regulatory Authority: No. WDRA/2017/5-7/A&F Dated: 07.09.2017ravi kumarNo ratings yet

- Ulip RFC FutureDocument2 pagesUlip RFC Futuresuchak52No ratings yet

- Form 24QDocument10 pagesForm 24QNIKHILNo ratings yet

- FAQ For PIC and Cash GrantDocument4 pagesFAQ For PIC and Cash GrantSathis KumarNo ratings yet

- Offer: Computer Consultancy Ref: TCSL/DT20184248190/Ahmedabad Date: 11/01/2019Document17 pagesOffer: Computer Consultancy Ref: TCSL/DT20184248190/Ahmedabad Date: 11/01/2019Sandipan DasNo ratings yet

- CBDT - E-Filing - ITR 4 - Validation RulesDocument19 pagesCBDT - E-Filing - ITR 4 - Validation RulesAshish GuliaNo ratings yet

- Income TaxDocument11 pagesIncome Taxvikas_thNo ratings yet

- Taxation System in IndiaDocument46 pagesTaxation System in IndiaNiket Dattani100% (1)

- Chapter 12 Tds & TcsDocument28 pagesChapter 12 Tds & TcsRajNo ratings yet

- Income Tax Refund PDFDocument3 pagesIncome Tax Refund PDFArunDaniel100% (1)

- Zero Moment Point ZMP Elysium LabsDocument3 pagesZero Moment Point ZMP Elysium LabsKaren DuarteNo ratings yet

- Philosophical Issues in TourismDocument2 pagesPhilosophical Issues in TourismLana Talita100% (1)

- Module 2Document42 pagesModule 2miles razorNo ratings yet

- Masterlist - Course - Offerings - 2024 (As at 18 July 2023)Document3 pagesMasterlist - Course - Offerings - 2024 (As at 18 July 2023)limyihang17No ratings yet

- Smartotdr Ds Fop Nse AeDocument4 pagesSmartotdr Ds Fop Nse AemoneyminderNo ratings yet

- Dance Like A ManDocument4 pagesDance Like A ManShubhadip aichNo ratings yet

- Steamshovel Press Issue 04Document60 pagesSteamshovel Press Issue 04liondog1No ratings yet

- Guaranty and Suretyship CasesDocument82 pagesGuaranty and Suretyship Cases001nooneNo ratings yet

- Law and IT Assignment SEM IXDocument18 pagesLaw and IT Assignment SEM IXrenu tomarNo ratings yet

- Dial Plan Implementation: Introducing Call RoutingDocument180 pagesDial Plan Implementation: Introducing Call RoutingGuillermo Ex TottiNo ratings yet

- Annex VI - Final Narrative ReportDocument4 pagesAnnex VI - Final Narrative ReporttijanagruNo ratings yet

- General Electrical SystemDocument136 pagesGeneral Electrical SystemSales AydinkayaNo ratings yet

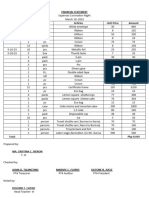

- Financial Statement Coronation NightDocument8 pagesFinancial Statement Coronation NightRuel Gapuz ManzanoNo ratings yet

- The Future of Talent Management: Four Stages of Evolution: An Oracle White Paper June 2012Document19 pagesThe Future of Talent Management: Four Stages of Evolution: An Oracle White Paper June 2012aini amanNo ratings yet

- Laporan Minggu 1 & 2 B.Inggris Nur Kholis-29-2AI1Document6 pagesLaporan Minggu 1 & 2 B.Inggris Nur Kholis-29-2AI1Kawek KagoelNo ratings yet

- HRM Project On Engro FoodsDocument20 pagesHRM Project On Engro FoodsSaad MughalNo ratings yet

- Ling Jing Five Buddhist TemplesDocument120 pagesLing Jing Five Buddhist Templessrimahakala100% (1)

- English - Fine - Tune Your English 2019Document3 pagesEnglish - Fine - Tune Your English 2019NishaNo ratings yet

- PESO PPA Feedback FormDocument2 pagesPESO PPA Feedback FormJover MarilouNo ratings yet

- Appendix 2 Works ListDocument18 pagesAppendix 2 Works ListAnonymous 4BZUZwNo ratings yet

- Recruitment Requisition FormDocument1 pageRecruitment Requisition FormrahulNo ratings yet

- Materials Letters: Featured LetterDocument4 pagesMaterials Letters: Featured Letterbiomedicalengineer 27No ratings yet

- Strategies For Weak & Crisis Ridden BusinessesDocument13 pagesStrategies For Weak & Crisis Ridden BusinessesApoorwa100% (1)

- Solution Manual For Transportation: A Global Supply Chain Perspective, 8th Edition, John J. Coyle, Robert A. Novack, Brian Gibson, Edward J. BardiDocument34 pagesSolution Manual For Transportation: A Global Supply Chain Perspective, 8th Edition, John J. Coyle, Robert A. Novack, Brian Gibson, Edward J. Bardielizabethsantosfawmpbnzjt100% (21)

- Day 2UNQ3-1.docx..bakDocument13 pagesDay 2UNQ3-1.docx..bakAurellia Shafitri100% (1)

- Fadi CV 030309Document5 pagesFadi CV 030309fkhaterNo ratings yet

- μου κάνειDocument43 pagesμου κάνειΚατερίνα ΠαπαδάκηNo ratings yet

- FD FanDocument42 pagesFD FanJAYKUMAR SINGHNo ratings yet

- Formal Register. Consultative Register-Casual Register. Intimate RegisterDocument2 pagesFormal Register. Consultative Register-Casual Register. Intimate RegisterTobio KageyamaNo ratings yet