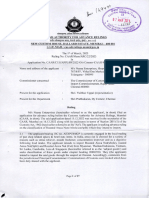

New Delhi CAAR Ruling Vaibhav Enterprises

New Delhi CAAR Ruling Vaibhav Enterprises

You might also like

- Neena Enteprises Advance Ruling (20081920)Document27 pagesNeena Enteprises Advance Ruling (20081920)ksvv prasadNo ratings yet

- Roadmap: A2+ Workbook Audio ScriptsDocument9 pagesRoadmap: A2+ Workbook Audio Scriptsveronica posseNo ratings yet

- Paryushan Cookbook by Neha Deepak ShahDocument77 pagesParyushan Cookbook by Neha Deepak ShahPrakrutiNo ratings yet

- The Essential Wood Fired Pizza Cookbook - Recipes and Techniques From My Wood-Fired Oven (PDFDrive)Document228 pagesThe Essential Wood Fired Pizza Cookbook - Recipes and Techniques From My Wood-Fired Oven (PDFDrive)Carolina Fierros75% (4)

- Lolashoes - A Little Crazy (Inc Outtake) by LolaShoes & TBY789Document61 pagesLolashoes - A Little Crazy (Inc Outtake) by LolaShoes & TBY789Lheinrich2No ratings yet

- Cotation Economode PDFDocument2 pagesCotation Economode PDFdinero dahustleNo ratings yet

- Accounting VoucherDocument2 pagesAccounting VoucherSiv global MarineNo ratings yet

- Nbri Bill 1Document1 pageNbri Bill 1Vivek YadavNo ratings yet

- GV - C2oDocument9 pagesGV - C2oParesh MondkarNo ratings yet

- In Re SGS India Private Limited GST AAR TamilnaduDocument22 pagesIn Re SGS India Private Limited GST AAR TamilnaduSantosh Kumar PadhiNo ratings yet

- Tax Invoice: Enliven EngineeringDocument1 pageTax Invoice: Enliven EngineeringenlivenplaningNo ratings yet

- Sale GST-23Document2 pagesSale GST-23Suhas TopkarNo ratings yet

- Maharashtra Pollution Control Board: SR No Product Maximum Quantity UOMDocument10 pagesMaharashtra Pollution Control Board: SR No Product Maximum Quantity UOMuser-402057No ratings yet

- Harit Industries Private Limited: InvoiceDocument2 pagesHarit Industries Private Limited: Invoiceemamoddin ahemadNo ratings yet

- Tax Invoice: Enliven EngineeringDocument1 pageTax Invoice: Enliven EngineeringenlivenplaningNo ratings yet

- Pi 84Document1 pagePi 84Prasad Madre KushalappaNo ratings yet

- Reprinted Bill of Supply: Gujarat Co-Operative Milk Marketing Federation LimitedDocument1 pageReprinted Bill of Supply: Gujarat Co-Operative Milk Marketing Federation Limitedshahistapravin09No ratings yet

- Inv# 278Document2 pagesInv# 278Monty SharmaNo ratings yet

- Cleaning Services Evaluation Report - NC150322Document16 pagesCleaning Services Evaluation Report - NC150322fatsoe1No ratings yet

- Rabi Industries: Quotation/ ProformaDocument1 pageRabi Industries: Quotation/ ProformaNitinNo ratings yet

- Swati EnterprisesDocument7 pagesSwati EnterprisesSharon SusmithaNo ratings yet

- Sales 2Document1 pageSales 2skgts787737No ratings yet

- 46 240624 VoucherDocument3 pages46 240624 VoucherSRIKANTH RAMADASSNo ratings yet

- 13 JAY AIR Ramee Techome Khar Raod 05.04.2024Document1 page13 JAY AIR Ramee Techome Khar Raod 05.04.2024vikti1199No ratings yet

- Devki EnterprisesDocument1 pageDevki EnterprisesNilesh YadavNo ratings yet

- REVA Electronics DT 22-Spet-22 (2239.4)Document2 pagesREVA Electronics DT 22-Spet-22 (2239.4)Swamy ChNo ratings yet

- TO: Kind Attn:: Grand TotalDocument2 pagesTO: Kind Attn:: Grand Totalashishkumar boharaNo ratings yet

- Esenpro Power Transmission Pvt. LTD: Jobwork Purchase OrderDocument1 pageEsenpro Power Transmission Pvt. LTD: Jobwork Purchase OrderSANDESHNo ratings yet

- Stroke-3 (3)Document2 pagesStroke-3 (3)saisaravana16597No ratings yet

- Accounting VoucherDocument2 pagesAccounting Vouchervenkat johnNo ratings yet

- Vineet Tex FabDocument7 pagesVineet Tex FabSharon SusmithaNo ratings yet

- Form 1 R&DDocument5 pagesForm 1 R&DHemanth KumarNo ratings yet

- Prepaid: Avenue E-Commerce LimitedDocument1 pagePrepaid: Avenue E-Commerce LimitedKavya shahNo ratings yet

- Govindaraja Mudaliar Sons (P) Ltd.Document1 pageGovindaraja Mudaliar Sons (P) Ltd.gvsairamchennaiNo ratings yet

- ABOVE Trade Marks Search Result For Class 40Document1 pageABOVE Trade Marks Search Result For Class 40rajender RightsandMarksNo ratings yet

- Gurnoor Traders: Sale & Purchase Of:-All Kinds of Old & New Industrial Machinery Specialist In: Shot Blast Labour JobDocument1 pageGurnoor Traders: Sale & Purchase Of:-All Kinds of Old & New Industrial Machinery Specialist In: Shot Blast Labour JobANMOLNo ratings yet

- TIPLPO2022 23 036 AIC-24June2022Document2 pagesTIPLPO2022 23 036 AIC-24June2022l8627352No ratings yet

- NEW SHIV SADAN CHS EstimateDocument1 pageNEW SHIV SADAN CHS EstimateanishkaneNo ratings yet

- Sales AJ 031 24-25Document3 pagesSales AJ 031 24-25A J INDUSTRIESNo ratings yet

- T John Mathew - Philips OCDocument2 pagesT John Mathew - Philips OCDAMBALENo ratings yet

- File RJ02 GC1237Document1 pageFile RJ02 GC1237vedanshu siddhaNo ratings yet

- Dt. 18.08.2020Document2 pagesDt. 18.08.2020DHANU DANGINo ratings yet

- Invoice: Consignee Gypsonite Industries Private LimitedDocument2 pagesInvoice: Consignee Gypsonite Industries Private LimitedRaunak ViNo ratings yet

- Anand Mechanical Services: Tax InvoiceDocument1 pageAnand Mechanical Services: Tax InvoicehdktaxNo ratings yet

- Tax Invoice: Transportation Charges On Sale Output CGST Output SGST Round OffDocument1 pageTax Invoice: Transportation Charges On Sale Output CGST Output SGST Round OffAlfiyaNo ratings yet

- 02.12.2020 Terms and Condition of Sale CompressedDocument4 pages02.12.2020 Terms and Condition of Sale CompressedbelemphousingtrustNo ratings yet

- PI Ambal Crane Service 12x42Document1 pagePI Ambal Crane Service 12x42gurunathan prabuNo ratings yet

- BABULIA - Sales-8780Document1 pageBABULIA - Sales-8780NI KONo ratings yet

- Creation PuOd 274 133709Document1 pageCreation PuOd 274 133709emamoddin ahemadNo ratings yet

- Sanchar Communication P.I ScaleDocument1 pageSanchar Communication P.I Scaleiamdenny2024No ratings yet

- Part 1Document527 pagesPart 1Rituj YadavNo ratings yet

- Invoice 7120075281Document1 pageInvoice 7120075281kaku131295No ratings yet

- BTI-013 Bolt, Nut, Washer Park GroveDocument2 pagesBTI-013 Bolt, Nut, Washer Park GroveGARIMANo ratings yet

- Reprinted Tax Invoice: Gujarat Co-Operative Milk Marketing Federation LimitedDocument2 pagesReprinted Tax Invoice: Gujarat Co-Operative Milk Marketing Federation Limitedshahistapravin09No ratings yet

- JivanDocument1 pageJivanRohitNo ratings yet

- Screenshot 2023-12-14 at 1.02.56 PMDocument1 pageScreenshot 2023-12-14 at 1.02.56 PMshashikumarsk0711No ratings yet

- Cash Invoice: Cable Crafts 10518 10-Feb-23Document2 pagesCash Invoice: Cable Crafts 10518 10-Feb-23naveenraj mNo ratings yet

- Sales 151Document1 pageSales 151skgts787737No ratings yet

- Brahans Polymers PVT LTD Proforma Invoice WK CastablesDocument1 pageBrahans Polymers PVT LTD Proforma Invoice WK CastablesRaj hegdeNo ratings yet

- Terms and Conditions 27 06 PDFDocument4 pagesTerms and Conditions 27 06 PDFShreyash NaikwadiNo ratings yet

- TRANSISTOR ROBU BILLDocument1 pageTRANSISTOR ROBU BILLbiomedicalvcareNo ratings yet

- (Duplicate For: Mode/Terms ofDocument2 pages(Duplicate For: Mode/Terms ofBabajan DoddmaniNo ratings yet

- Herbalife International India, Pvt. LTD.: Digitally Signed by Arnab Chakraborty Date: 12-Jun-2024 20:19:44 ISTDocument2 pagesHerbalife International India, Pvt. LTD.: Digitally Signed by Arnab Chakraborty Date: 12-Jun-2024 20:19:44 ISTmuthuselvamcr007No ratings yet

- Indore Municipal Corporation 153Document2 pagesIndore Municipal Corporation 153Babyboy2010No ratings yet

- GSTAT - Vacancy Circular MembersDocument13 pagesGSTAT - Vacancy Circular Membersksvv prasadNo ratings yet

- Circulars 2011 Circ01 2k11 CusDocument2 pagesCirculars 2011 Circ01 2k11 Cusksvv prasadNo ratings yet

- Amaravati Kathalu Online Telugu Sahityam-Find More Books at WWW - Telugubooks.tkDocument4 pagesAmaravati Kathalu Online Telugu Sahityam-Find More Books at WWW - Telugubooks.tkksvv prasadNo ratings yet

- Sudestada Food MenuDocument9 pagesSudestada Food Menuhans aajiNo ratings yet

- CM2023 Rule Book-230809-090506Document77 pagesCM2023 Rule Book-230809-090506nur asmaaNo ratings yet

- Catalogue Havells AppliancesDocument166 pagesCatalogue Havells AppliancesNiravBhalodiyaNo ratings yet

- '3ANS' Jam Business Proposal-1Document17 pages'3ANS' Jam Business Proposal-1Vicky Sarad100% (2)

- Squash and Radicchio Salad Recipe - Bon AppétitDocument3 pagesSquash and Radicchio Salad Recipe - Bon AppétitLison CapraisNo ratings yet

- A Long-Term Survival Guide - Equipment & SuppliesDocument18 pagesA Long-Term Survival Guide - Equipment & Suppliesbuckonbeach100% (14)

- VALENTIN'S DAY HEART - Le Journal Du Pâtissier PDFDocument1 pageVALENTIN'S DAY HEART - Le Journal Du Pâtissier PDFAhmedsabri SabriNo ratings yet

- Thanksgiving Budget Lesson PlanDocument3 pagesThanksgiving Budget Lesson Planapi-383711550No ratings yet

- Procedure TextsDocument5 pagesProcedure TextsMohamad WisnuNo ratings yet

- 8 P's ScriptDocument2 pages8 P's ScriptManasi JamsandekarNo ratings yet

- nestle- презентацияDocument17 pagesnestle- презентациямарияNo ratings yet

- English Pronunciation Spanish: VegetablesDocument6 pagesEnglish Pronunciation Spanish: VegetablesAlondra HernándezNo ratings yet

- TRAM Cocktails 3.19Document1 pageTRAM Cocktails 3.19Caleb PershanNo ratings yet

- Q3 G9 Tle Cookery M1Document32 pagesQ3 G9 Tle Cookery M1Mark Kenneth MallorcaNo ratings yet

- Saha Sir 1 DocumentDocument43 pagesSaha Sir 1 DocumentYogesh SinghNo ratings yet

- Compound SentencesDocument19 pagesCompound SentencesRebecca ThamNo ratings yet

- Pat Bahasa Inggris Kelas 5Document2 pagesPat Bahasa Inggris Kelas 5SMPIP Insan RobbaniNo ratings yet

- Desain Penggorengan Kerupuk Airfryer Tanpa MinyakDocument6 pagesDesain Penggorengan Kerupuk Airfryer Tanpa MinyakHilda SeptirianiNo ratings yet

- Ingredients: Bread and Pastry NC Ii Session Plan Document NO. Issued By: Page 1 of 8Document8 pagesIngredients: Bread and Pastry NC Ii Session Plan Document NO. Issued By: Page 1 of 8CharleneNo ratings yet

- Diabetes InfoDocument24 pagesDiabetes Infoalle manoharNo ratings yet

- Comparativos y SuperlativosDocument16 pagesComparativos y SuperlativosninaNo ratings yet

- Structure of EnglishDocument7 pagesStructure of EnglishVia Bianca R. BeguiaNo ratings yet

- Lesson 2 - Combination 02.20.21Document18 pagesLesson 2 - Combination 02.20.21Rosalyn CalapitcheNo ratings yet

- Supermarket CatalogDocument14 pagesSupermarket Catalogmehran book shoNo ratings yet

- Butter Chicken Recipe - NYT CookingDocument2 pagesButter Chicken Recipe - NYT CookinglisaNo ratings yet

- Oliver Song LyricsDocument4 pagesOliver Song LyricsMiehj ParreñoNo ratings yet

Download as pdf or txt

You might also like

- Neena Enteprises Advance Ruling (20081920)Document27 pagesNeena Enteprises Advance Ruling (20081920)ksvv prasadNo ratings yet

- Roadmap: A2+ Workbook Audio ScriptsDocument9 pagesRoadmap: A2+ Workbook Audio Scriptsveronica posseNo ratings yet

- Paryushan Cookbook by Neha Deepak ShahDocument77 pagesParyushan Cookbook by Neha Deepak ShahPrakrutiNo ratings yet

- The Essential Wood Fired Pizza Cookbook - Recipes and Techniques From My Wood-Fired Oven (PDFDrive)Document228 pagesThe Essential Wood Fired Pizza Cookbook - Recipes and Techniques From My Wood-Fired Oven (PDFDrive)Carolina Fierros75% (4)

- Lolashoes - A Little Crazy (Inc Outtake) by LolaShoes & TBY789Document61 pagesLolashoes - A Little Crazy (Inc Outtake) by LolaShoes & TBY789Lheinrich2No ratings yet

- Cotation Economode PDFDocument2 pagesCotation Economode PDFdinero dahustleNo ratings yet

- Accounting VoucherDocument2 pagesAccounting VoucherSiv global MarineNo ratings yet

- Nbri Bill 1Document1 pageNbri Bill 1Vivek YadavNo ratings yet

- GV - C2oDocument9 pagesGV - C2oParesh MondkarNo ratings yet

- In Re SGS India Private Limited GST AAR TamilnaduDocument22 pagesIn Re SGS India Private Limited GST AAR TamilnaduSantosh Kumar PadhiNo ratings yet

- Tax Invoice: Enliven EngineeringDocument1 pageTax Invoice: Enliven EngineeringenlivenplaningNo ratings yet

- Sale GST-23Document2 pagesSale GST-23Suhas TopkarNo ratings yet

- Maharashtra Pollution Control Board: SR No Product Maximum Quantity UOMDocument10 pagesMaharashtra Pollution Control Board: SR No Product Maximum Quantity UOMuser-402057No ratings yet

- Harit Industries Private Limited: InvoiceDocument2 pagesHarit Industries Private Limited: Invoiceemamoddin ahemadNo ratings yet

- Tax Invoice: Enliven EngineeringDocument1 pageTax Invoice: Enliven EngineeringenlivenplaningNo ratings yet

- Pi 84Document1 pagePi 84Prasad Madre KushalappaNo ratings yet

- Reprinted Bill of Supply: Gujarat Co-Operative Milk Marketing Federation LimitedDocument1 pageReprinted Bill of Supply: Gujarat Co-Operative Milk Marketing Federation Limitedshahistapravin09No ratings yet

- Inv# 278Document2 pagesInv# 278Monty SharmaNo ratings yet

- Cleaning Services Evaluation Report - NC150322Document16 pagesCleaning Services Evaluation Report - NC150322fatsoe1No ratings yet

- Rabi Industries: Quotation/ ProformaDocument1 pageRabi Industries: Quotation/ ProformaNitinNo ratings yet

- Swati EnterprisesDocument7 pagesSwati EnterprisesSharon SusmithaNo ratings yet

- Sales 2Document1 pageSales 2skgts787737No ratings yet

- 46 240624 VoucherDocument3 pages46 240624 VoucherSRIKANTH RAMADASSNo ratings yet

- 13 JAY AIR Ramee Techome Khar Raod 05.04.2024Document1 page13 JAY AIR Ramee Techome Khar Raod 05.04.2024vikti1199No ratings yet

- Devki EnterprisesDocument1 pageDevki EnterprisesNilesh YadavNo ratings yet

- REVA Electronics DT 22-Spet-22 (2239.4)Document2 pagesREVA Electronics DT 22-Spet-22 (2239.4)Swamy ChNo ratings yet

- TO: Kind Attn:: Grand TotalDocument2 pagesTO: Kind Attn:: Grand Totalashishkumar boharaNo ratings yet

- Esenpro Power Transmission Pvt. LTD: Jobwork Purchase OrderDocument1 pageEsenpro Power Transmission Pvt. LTD: Jobwork Purchase OrderSANDESHNo ratings yet

- Stroke-3 (3)Document2 pagesStroke-3 (3)saisaravana16597No ratings yet

- Accounting VoucherDocument2 pagesAccounting Vouchervenkat johnNo ratings yet

- Vineet Tex FabDocument7 pagesVineet Tex FabSharon SusmithaNo ratings yet

- Form 1 R&DDocument5 pagesForm 1 R&DHemanth KumarNo ratings yet

- Prepaid: Avenue E-Commerce LimitedDocument1 pagePrepaid: Avenue E-Commerce LimitedKavya shahNo ratings yet

- Govindaraja Mudaliar Sons (P) Ltd.Document1 pageGovindaraja Mudaliar Sons (P) Ltd.gvsairamchennaiNo ratings yet

- ABOVE Trade Marks Search Result For Class 40Document1 pageABOVE Trade Marks Search Result For Class 40rajender RightsandMarksNo ratings yet

- Gurnoor Traders: Sale & Purchase Of:-All Kinds of Old & New Industrial Machinery Specialist In: Shot Blast Labour JobDocument1 pageGurnoor Traders: Sale & Purchase Of:-All Kinds of Old & New Industrial Machinery Specialist In: Shot Blast Labour JobANMOLNo ratings yet

- TIPLPO2022 23 036 AIC-24June2022Document2 pagesTIPLPO2022 23 036 AIC-24June2022l8627352No ratings yet

- NEW SHIV SADAN CHS EstimateDocument1 pageNEW SHIV SADAN CHS EstimateanishkaneNo ratings yet

- Sales AJ 031 24-25Document3 pagesSales AJ 031 24-25A J INDUSTRIESNo ratings yet

- T John Mathew - Philips OCDocument2 pagesT John Mathew - Philips OCDAMBALENo ratings yet

- File RJ02 GC1237Document1 pageFile RJ02 GC1237vedanshu siddhaNo ratings yet

- Dt. 18.08.2020Document2 pagesDt. 18.08.2020DHANU DANGINo ratings yet

- Invoice: Consignee Gypsonite Industries Private LimitedDocument2 pagesInvoice: Consignee Gypsonite Industries Private LimitedRaunak ViNo ratings yet

- Anand Mechanical Services: Tax InvoiceDocument1 pageAnand Mechanical Services: Tax InvoicehdktaxNo ratings yet

- Tax Invoice: Transportation Charges On Sale Output CGST Output SGST Round OffDocument1 pageTax Invoice: Transportation Charges On Sale Output CGST Output SGST Round OffAlfiyaNo ratings yet

- 02.12.2020 Terms and Condition of Sale CompressedDocument4 pages02.12.2020 Terms and Condition of Sale CompressedbelemphousingtrustNo ratings yet

- PI Ambal Crane Service 12x42Document1 pagePI Ambal Crane Service 12x42gurunathan prabuNo ratings yet

- BABULIA - Sales-8780Document1 pageBABULIA - Sales-8780NI KONo ratings yet

- Creation PuOd 274 133709Document1 pageCreation PuOd 274 133709emamoddin ahemadNo ratings yet

- Sanchar Communication P.I ScaleDocument1 pageSanchar Communication P.I Scaleiamdenny2024No ratings yet

- Part 1Document527 pagesPart 1Rituj YadavNo ratings yet

- Invoice 7120075281Document1 pageInvoice 7120075281kaku131295No ratings yet

- BTI-013 Bolt, Nut, Washer Park GroveDocument2 pagesBTI-013 Bolt, Nut, Washer Park GroveGARIMANo ratings yet

- Reprinted Tax Invoice: Gujarat Co-Operative Milk Marketing Federation LimitedDocument2 pagesReprinted Tax Invoice: Gujarat Co-Operative Milk Marketing Federation Limitedshahistapravin09No ratings yet

- JivanDocument1 pageJivanRohitNo ratings yet

- Screenshot 2023-12-14 at 1.02.56 PMDocument1 pageScreenshot 2023-12-14 at 1.02.56 PMshashikumarsk0711No ratings yet

- Cash Invoice: Cable Crafts 10518 10-Feb-23Document2 pagesCash Invoice: Cable Crafts 10518 10-Feb-23naveenraj mNo ratings yet

- Sales 151Document1 pageSales 151skgts787737No ratings yet

- Brahans Polymers PVT LTD Proforma Invoice WK CastablesDocument1 pageBrahans Polymers PVT LTD Proforma Invoice WK CastablesRaj hegdeNo ratings yet

- Terms and Conditions 27 06 PDFDocument4 pagesTerms and Conditions 27 06 PDFShreyash NaikwadiNo ratings yet

- TRANSISTOR ROBU BILLDocument1 pageTRANSISTOR ROBU BILLbiomedicalvcareNo ratings yet

- (Duplicate For: Mode/Terms ofDocument2 pages(Duplicate For: Mode/Terms ofBabajan DoddmaniNo ratings yet

- Herbalife International India, Pvt. LTD.: Digitally Signed by Arnab Chakraborty Date: 12-Jun-2024 20:19:44 ISTDocument2 pagesHerbalife International India, Pvt. LTD.: Digitally Signed by Arnab Chakraborty Date: 12-Jun-2024 20:19:44 ISTmuthuselvamcr007No ratings yet

- Indore Municipal Corporation 153Document2 pagesIndore Municipal Corporation 153Babyboy2010No ratings yet

- GSTAT - Vacancy Circular MembersDocument13 pagesGSTAT - Vacancy Circular Membersksvv prasadNo ratings yet

- Circulars 2011 Circ01 2k11 CusDocument2 pagesCirculars 2011 Circ01 2k11 Cusksvv prasadNo ratings yet

- Amaravati Kathalu Online Telugu Sahityam-Find More Books at WWW - Telugubooks.tkDocument4 pagesAmaravati Kathalu Online Telugu Sahityam-Find More Books at WWW - Telugubooks.tkksvv prasadNo ratings yet

- Sudestada Food MenuDocument9 pagesSudestada Food Menuhans aajiNo ratings yet

- CM2023 Rule Book-230809-090506Document77 pagesCM2023 Rule Book-230809-090506nur asmaaNo ratings yet

- Catalogue Havells AppliancesDocument166 pagesCatalogue Havells AppliancesNiravBhalodiyaNo ratings yet

- '3ANS' Jam Business Proposal-1Document17 pages'3ANS' Jam Business Proposal-1Vicky Sarad100% (2)

- Squash and Radicchio Salad Recipe - Bon AppétitDocument3 pagesSquash and Radicchio Salad Recipe - Bon AppétitLison CapraisNo ratings yet

- A Long-Term Survival Guide - Equipment & SuppliesDocument18 pagesA Long-Term Survival Guide - Equipment & Suppliesbuckonbeach100% (14)

- VALENTIN'S DAY HEART - Le Journal Du Pâtissier PDFDocument1 pageVALENTIN'S DAY HEART - Le Journal Du Pâtissier PDFAhmedsabri SabriNo ratings yet

- Thanksgiving Budget Lesson PlanDocument3 pagesThanksgiving Budget Lesson Planapi-383711550No ratings yet

- Procedure TextsDocument5 pagesProcedure TextsMohamad WisnuNo ratings yet

- 8 P's ScriptDocument2 pages8 P's ScriptManasi JamsandekarNo ratings yet

- nestle- презентацияDocument17 pagesnestle- презентациямарияNo ratings yet

- English Pronunciation Spanish: VegetablesDocument6 pagesEnglish Pronunciation Spanish: VegetablesAlondra HernándezNo ratings yet

- TRAM Cocktails 3.19Document1 pageTRAM Cocktails 3.19Caleb PershanNo ratings yet

- Q3 G9 Tle Cookery M1Document32 pagesQ3 G9 Tle Cookery M1Mark Kenneth MallorcaNo ratings yet

- Saha Sir 1 DocumentDocument43 pagesSaha Sir 1 DocumentYogesh SinghNo ratings yet

- Compound SentencesDocument19 pagesCompound SentencesRebecca ThamNo ratings yet

- Pat Bahasa Inggris Kelas 5Document2 pagesPat Bahasa Inggris Kelas 5SMPIP Insan RobbaniNo ratings yet

- Desain Penggorengan Kerupuk Airfryer Tanpa MinyakDocument6 pagesDesain Penggorengan Kerupuk Airfryer Tanpa MinyakHilda SeptirianiNo ratings yet

- Ingredients: Bread and Pastry NC Ii Session Plan Document NO. Issued By: Page 1 of 8Document8 pagesIngredients: Bread and Pastry NC Ii Session Plan Document NO. Issued By: Page 1 of 8CharleneNo ratings yet

- Diabetes InfoDocument24 pagesDiabetes Infoalle manoharNo ratings yet

- Comparativos y SuperlativosDocument16 pagesComparativos y SuperlativosninaNo ratings yet

- Structure of EnglishDocument7 pagesStructure of EnglishVia Bianca R. BeguiaNo ratings yet

- Lesson 2 - Combination 02.20.21Document18 pagesLesson 2 - Combination 02.20.21Rosalyn CalapitcheNo ratings yet

- Supermarket CatalogDocument14 pagesSupermarket Catalogmehran book shoNo ratings yet

- Butter Chicken Recipe - NYT CookingDocument2 pagesButter Chicken Recipe - NYT CookinglisaNo ratings yet

- Oliver Song LyricsDocument4 pagesOliver Song LyricsMiehj ParreñoNo ratings yet